Explore advanced trading analytics and risk assessment tools to enhance your cryptocurrency investment strategies and lending decisions.

Revolutionary Credit Assessment in Decentralized Finance

The integration of artificial intelligence into cryptocurrency lending platforms represents a paradigm shift in how credit risk is assessed and managed in decentralized finance ecosystems. Traditional financial institutions have long relied on credit scores, employment history, and collateral assets to determine creditworthiness, but the pseudonymous nature of blockchain transactions and the absence of traditional financial identities in cryptocurrency markets necessitate entirely new approaches to credit assessment that leverage machine learning algorithms, blockchain analytics, and behavioral pattern recognition.

AI-powered credit assessment systems in crypto lending analyze vast amounts of on-chain data to create comprehensive risk profiles for borrowers without requiring traditional identification or credit history verification. These systems examine wallet addresses, transaction patterns, asset holdings, trading behavior, and smart contract interactions to determine the likelihood of loan repayment and appropriate interest rates for individual borrowers. The sophistication of these AI systems continues to evolve rapidly, incorporating advanced neural networks, natural language processing for social sentiment analysis, and predictive modeling that can assess credit risk with remarkable accuracy while maintaining the privacy and decentralization principles that make cryptocurrency lending attractive to users worldwide.

The revolution in AI-powered credit assessment extends beyond simple risk scoring to encompass dynamic pricing models that adjust interest rates in real-time based on market conditions, borrower behavior, and portfolio risk exposure. These systems can identify emerging risks before they manifest as defaults, automatically adjust lending parameters to maintain platform stability, and provide personalized lending products that optimize returns for both lenders and borrowers. The integration of artificial intelligence into crypto lending platforms has enabled the creation of sophisticated financial products that rival and often exceed the capabilities of traditional banking systems while operating in a completely decentralized environment.

Machine Learning Models and Blockchain Analytics

The foundation of AI-powered credit assessment in cryptocurrency lending rests on sophisticated machine learning models that can process and analyze the immense volume of blockchain data generated by millions of transactions daily. These models employ various algorithmic approaches including supervised learning for default prediction, unsupervised learning for anomaly detection, and reinforcement learning for dynamic strategy optimization. The complexity of blockchain data requires specialized preprocessing techniques that can extract meaningful signals from transaction graphs, temporal patterns, and multi-dimensional asset relationships.

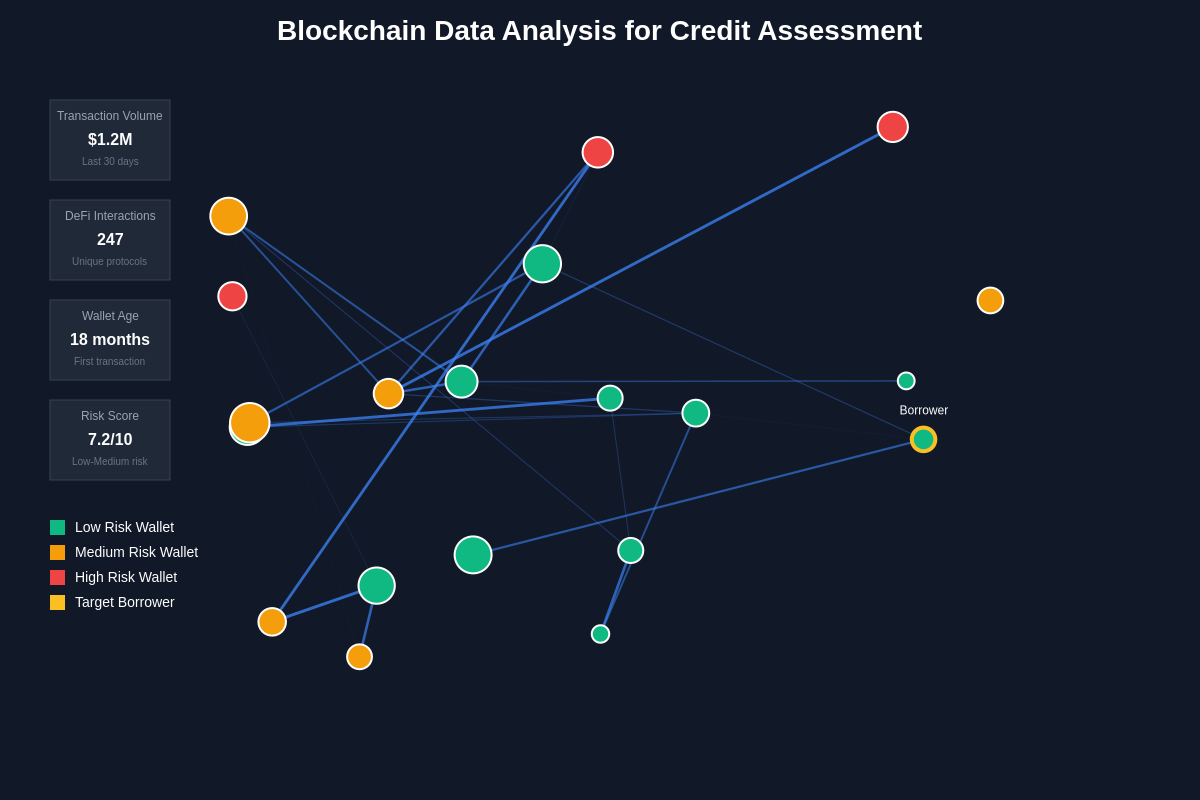

Deep learning architectures particularly excel at identifying subtle patterns in blockchain behavior that traditional analytical methods might miss. Convolutional neural networks analyze transaction graphs to identify community structures and influence patterns, while recurrent neural networks process temporal sequences of wallet activities to predict future behavior. Transformer models, originally developed for natural language processing, have been adapted to analyze blockchain transaction sequences, treating each transaction as a token in a complex financial language that reveals borrower intentions and risk characteristics.

The application of advanced technical analysis tools enhances the accuracy of AI credit assessment models by incorporating market sentiment and price action data into risk calculations. Graph neural networks represent another breakthrough in blockchain analytics, enabling AI systems to understand the complex relationships between different wallet addresses, smart contracts, and decentralized applications. These networks can identify clusters of related addresses, detect potential wash trading or market manipulation attempts, and assess the overall health of a borrower’s cryptocurrency portfolio across multiple blockchain networks.

Feature engineering for blockchain data requires deep understanding of cryptocurrency economics and user behavior patterns. AI systems extract hundreds of features from raw blockchain data including transaction frequency and timing patterns, asset diversification metrics, interaction with different types of smart contracts, participation in various DeFi protocols, and correlation with market movements. Advanced feature selection algorithms identify the most predictive variables while eliminating noise and redundant information that could lead to overfitting or biased assessments.

Risk Assessment Algorithms and Credit Scoring

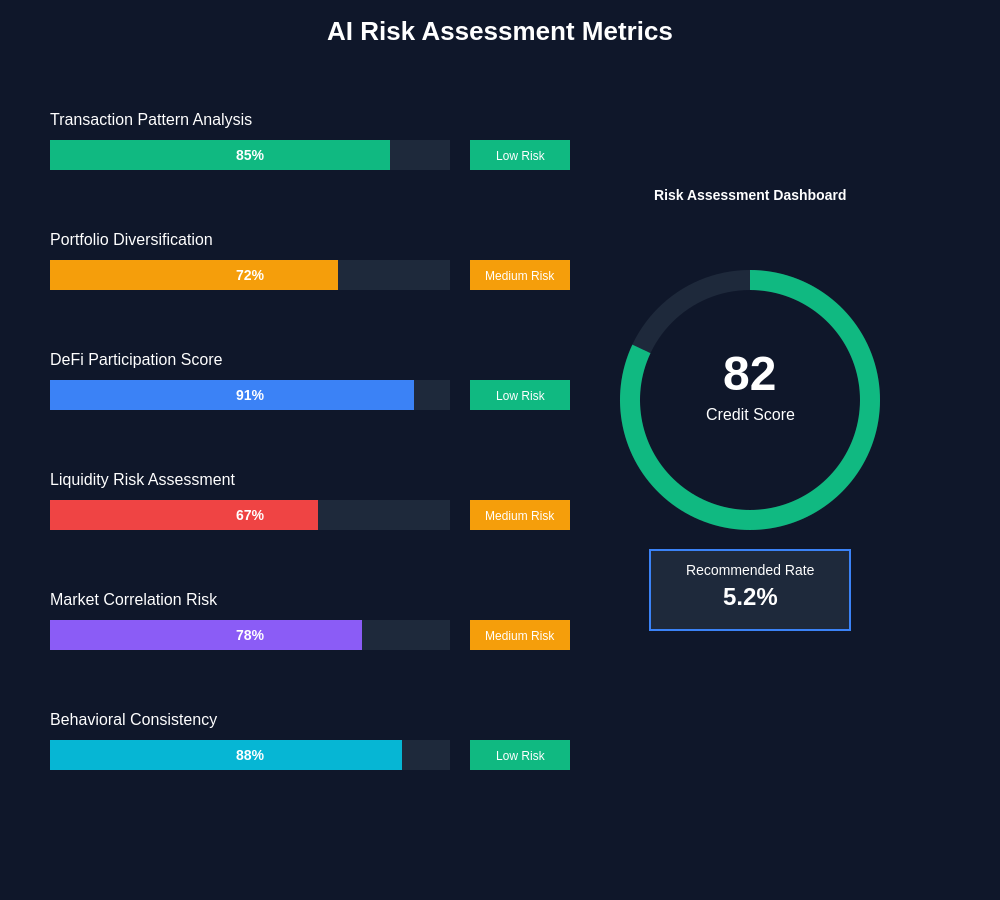

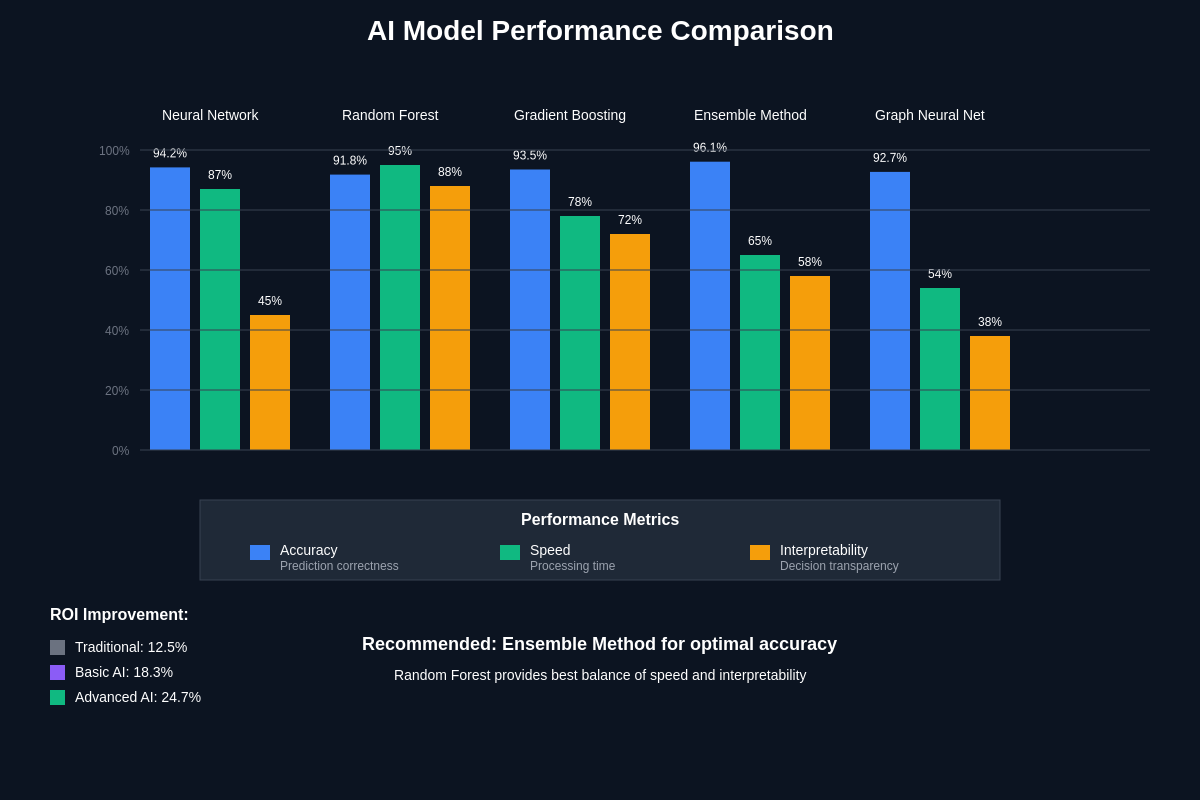

Contemporary AI-powered credit scoring systems for cryptocurrency lending employ ensemble methods that combine multiple algorithmic approaches to create robust and reliable risk assessments. These systems integrate traditional statistical methods with cutting-edge machine learning techniques to create credit scores that reflect the unique characteristics of cryptocurrency markets and user behavior. The challenge lies in creating scoring models that can adapt to the high volatility and rapid evolution of cryptocurrency markets while maintaining consistency and fairness in credit decisions.

Gradient boosting machines and random forest algorithms form the backbone of many AI credit scoring systems due to their ability to handle complex feature interactions and provide interpretable results that can be audited for fairness and accuracy. These algorithms excel at identifying non-linear relationships between borrower characteristics and default probability, enabling more nuanced risk assessment than traditional linear models. The ensemble approach combines predictions from multiple models to reduce variance and improve overall accuracy while providing confidence intervals for risk estimates.

Anomaly detection algorithms play a crucial role in identifying potentially fraudulent or high-risk borrowers by flagging unusual patterns in blockchain behavior that deviate from normal user activities. These systems can detect coordinated address clusters, unusual transaction timing patterns, interactions with known malicious contracts, and other red flags that might indicate elevated risk. The integration of real-time market data analysis enables AI systems to adjust risk assessments based on current market conditions and volatility levels.

The development of explainable AI techniques for credit scoring ensures that borrowers and regulators can understand the factors contributing to credit decisions, addressing concerns about algorithmic bias and transparency in automated lending systems. These techniques provide clear explanations of why specific credit scores were assigned and which factors were most influential in the decision-making process. Advanced calibration techniques ensure that predicted default probabilities accurately reflect actual default rates, enabling precise pricing of credit risk and optimal capital allocation across different risk segments.

Temporal modeling represents another critical component of AI credit assessment, with algorithms designed to track how borrower risk profiles evolve over time based on changing market conditions, portfolio composition, and behavioral patterns. These dynamic models can identify borrowers whose risk profiles are improving or deteriorating, enabling proactive portfolio management and early intervention strategies that minimize losses while maximizing lending opportunities.

Integration with Traditional Financial Data

The convergence of cryptocurrency lending with traditional financial systems has created opportunities for AI-powered credit assessment systems to incorporate conventional financial data alongside blockchain analytics, creating more comprehensive and accurate risk profiles for borrowers who maintain both traditional and cryptocurrency financial activities. This integration presents significant technical and privacy challenges while offering substantial improvements in credit assessment accuracy and risk management capabilities.

Open banking APIs and financial data aggregation services enable AI systems to access traditional bank account information, credit card transactions, investment portfolio data, and employment records with borrower consent, creating a holistic view of financial behavior that spans both centralized and decentralized financial ecosystems. The challenge lies in creating unified data models that can effectively combine structured traditional financial data with the unstructured and pseudonymous nature of blockchain transactions while maintaining privacy and regulatory compliance.

Machine learning models that integrate traditional and cryptocurrency financial data must account for the different characteristics and risk factors associated with each domain. Traditional financial data provides insights into income stability, spending patterns, and credit history, while cryptocurrency data reveals risk tolerance, market sophistication, and decentralized finance participation levels. Advanced feature fusion techniques enable AI systems to create synthetic features that capture the interactions between traditional and cryptocurrency financial behaviors.

Privacy-preserving machine learning techniques such as federated learning and homomorphic encryption enable the integration of sensitive traditional financial data without compromising user privacy or exposing personal information to unauthorized parties. These approaches allow AI models to learn from combined datasets while ensuring that individual financial records remain confidential and secure. Zero-knowledge proof systems offer another avenue for verifying traditional financial credentials without revealing underlying data.

The regulatory landscape surrounding the integration of traditional financial data with cryptocurrency lending continues to evolve, with different jurisdictions taking varying approaches to data privacy, cross-border data transfers, and algorithmic decision-making transparency. AI systems must be designed with sufficient flexibility to adapt to changing regulatory requirements while maintaining their predictive accuracy and operational efficiency.

Cross-validation between traditional and cryptocurrency financial behaviors enables AI systems to identify inconsistencies that might indicate fraud, money laundering, or other illicit activities. These systems can detect when borrower behavior in traditional financial systems contradicts their cryptocurrency activities, flagging potential risks that might not be apparent when analyzing either data source in isolation.

Real-Time Risk Monitoring and Adaptive Models

The dynamic nature of cryptocurrency markets and the 24/7 operation of blockchain networks necessitate real-time risk monitoring systems that can continuously assess and update borrower risk profiles as new information becomes available. These systems represent a significant advancement over traditional lending practices, which typically rely on periodic credit reviews and static risk assessments that may not reflect current borrower circumstances or market conditions.

Real-time monitoring systems process streaming blockchain data to detect changes in borrower behavior, portfolio composition, market exposure, and external risk factors that could affect loan performance. Advanced event processing engines analyze thousands of transactions per second, identifying patterns and anomalies that require immediate attention or risk parameter adjustments. These systems can detect early warning signs of financial distress, such as liquidation cascades, portfolio concentration increases, or unusual trading patterns that might indicate desperate attempts to avoid default.

Adaptive machine learning models continuously retrain on new data to maintain their predictive accuracy as market conditions and user behaviors evolve. Online learning algorithms enable these systems to update their parameters in real-time without requiring complete model retraining, ensuring that risk assessments remain current and relevant. The challenge lies in balancing model stability with adaptability, preventing overfitting to short-term market fluctuations while ensuring that models can capture genuine changes in risk patterns.

Stream processing architectures built on technologies like Apache Kafka and Apache Flink enable the real-time ingestion and analysis of multiple data streams including blockchain transactions, market prices, social media sentiment, and macroeconomic indicators. These systems can correlate events across different data sources to identify emerging risks or opportunities that might not be apparent when analyzing individual data streams in isolation.

Automated risk management responses triggered by real-time monitoring systems can adjust lending parameters, modify interest rates, request additional collateral, or initiate early repayment procedures based on predefined risk thresholds and borrower agreements. These automated responses help maintain platform stability while minimizing manual intervention requirements and reducing operational costs. Advanced charting and analysis tools support real-time decision-making by providing visual representations of risk trends and portfolio exposures.

The implementation of circuit breakers and risk limits prevents automated systems from making extreme adjustments during periods of market stress or data anomalies, ensuring that risk management responses remain proportionate and reasonable. These safeguards protect both borrowers and lenders from potentially harmful automated decisions while maintaining the benefits of real-time risk monitoring and adaptive model updates.

Privacy and Data Protection Considerations

The implementation of AI-powered credit assessment systems in cryptocurrency lending raises significant privacy and data protection concerns that must be addressed through careful system design and adherence to evolving regulatory frameworks. The pseudonymous nature of blockchain transactions provides some privacy protection, but the extensive data analysis required for accurate credit assessment can potentially compromise user anonymity and reveal sensitive financial information.

Differential privacy techniques enable AI systems to extract useful insights from user data while providing mathematical guarantees about individual privacy protection. These methods add carefully calibrated noise to datasets and query results, ensuring that the presence or absence of any individual’s data cannot be determined from the system’s outputs. The challenge lies in balancing privacy protection with the accuracy requirements of credit assessment models, as excessive noise can degrade model performance and reduce lending efficiency.

Secure multi-party computation protocols allow multiple parties to jointly compute credit scores and risk assessments without revealing their individual data contributions to other participants. These techniques enable collaboration between different lending platforms, credit agencies, and financial institutions while maintaining data confidentiality and competitive advantages. Homomorphic encryption extends these capabilities by enabling computations on encrypted data, allowing AI models to process sensitive financial information without ever decrypting it.

Data minimization principles guide the design of AI credit assessment systems to collect and process only the minimum amount of personal information necessary for accurate risk evaluation. Advanced feature selection algorithms identify the most predictive variables while eliminating unnecessary data collection, reducing privacy risks and compliance burdens. Temporal data retention policies ensure that historical information is purged when it is no longer relevant for credit decisions, further protecting user privacy.

Blockchain-based identity management systems offer potential solutions for verified anonymous credit assessment, enabling users to prove their creditworthiness without revealing their underlying identity or transaction history. Zero-knowledge proof systems can verify specific financial criteria such as income levels, asset holdings, or payment history without disclosing the actual values or sources of this information.

Regulatory compliance frameworks such as GDPR, CCPA, and emerging cryptocurrency-specific regulations require AI credit assessment systems to provide users with transparency about data collection practices, algorithmic decision-making processes, and rights regarding their personal information. These requirements necessitate the development of explainable AI systems that can provide clear justifications for credit decisions while maintaining the sophistication required for accurate risk assessment.

Regulatory Compliance and Algorithmic Auditing

The regulatory landscape for AI-powered credit assessment in cryptocurrency lending continues to evolve rapidly, with different jurisdictions developing frameworks that balance innovation promotion with consumer protection and financial stability concerns. Compliance requirements span multiple domains including fair lending practices, algorithmic transparency, data protection, anti-money laundering procedures, and capital adequacy standards that collectively shape how AI systems can be designed and deployed.

Algorithmic auditing procedures ensure that AI credit assessment systems comply with fair lending regulations and do not discriminate against protected classes or engage in predatory lending practices. These audits examine model training data for bias, test algorithmic outputs across different demographic groups, and verify that credit decisions are based on legitimate financial factors rather than prohibited characteristics. The challenge lies in conducting meaningful fairness assessments when traditional demographic information may not be available in pseudonymous cryptocurrency lending environments.

Model governance frameworks establish formal procedures for AI system development, validation, deployment, and ongoing monitoring to ensure compliance with regulatory requirements and internal risk management standards. These frameworks include documentation requirements, change management procedures, performance monitoring protocols, and escalation processes for addressing model failures or regulatory violations. Regulatory sandboxes in various jurisdictions provide opportunities for testing innovative AI credit assessment approaches under relaxed regulatory requirements while gathering data about their effectiveness and risks.

Stress testing and scenario analysis requirements mandate that AI credit assessment systems demonstrate their resilience under adverse market conditions and their ability to maintain accurate risk assessments during periods of high volatility or systemic stress. These tests evaluate model performance across various economic scenarios, assess the impact of extreme market events, and verify that automated risk management responses remain appropriate under challenging conditions.

International coordination efforts aim to develop harmonized standards for AI-powered financial services that can facilitate cross-border lending while maintaining appropriate regulatory oversight and consumer protection. These efforts address challenges related to jurisdictional conflicts, regulatory arbitrage, and the global nature of cryptocurrency markets that transcend traditional financial regulatory boundaries.

The development of regulatory technology solutions enables automated compliance monitoring and reporting, reducing the operational burden of regulatory compliance while improving accuracy and timeliness of regulatory submissions. Market analysis platforms support compliance efforts by providing comprehensive market data and analytics that can be integrated into regulatory reporting systems.

Market Impact and Economic Implications

The widespread adoption of AI-powered credit assessment in cryptocurrency lending has profound implications for financial market structure, capital allocation efficiency, and economic growth patterns that extend far beyond the immediate benefits to individual borrowers and lenders. These systems are fundamentally altering how credit risk is priced and managed in decentralized financial markets while creating new opportunities for financial inclusion and economic participation.

Credit market efficiency has improved significantly through AI-powered assessment systems that can more accurately price risk and match borrowers with appropriate lenders based on sophisticated risk-return profiles. This enhanced efficiency reduces borrowing costs for creditworthy borrowers while ensuring that lenders receive appropriate compensation for the risks they assume. The result is a more liquid and competitive credit market that can better allocate capital to productive uses while minimizing the misallocation of resources that can occur with less sophisticated risk assessment methods.

Financial inclusion benefits emerge as AI systems can assess creditworthiness for individuals and businesses that lack traditional credit histories or access to conventional banking services. These systems can identify creditworthy borrowers based on cryptocurrency transaction patterns, decentralized finance participation, and other alternative data sources that may not be captured by traditional credit scoring methods. The global accessibility of cryptocurrency lending platforms combined with AI-powered risk assessment creates opportunities for economic participation that transcend geographic and institutional barriers.

Systemic risk considerations arise from the increasing reliance on AI systems for credit decisions across multiple lending platforms, potentially creating new forms of correlation and vulnerability in financial markets. If multiple platforms use similar AI models or data sources, they may make correlated lending decisions that could amplify market cycles or create unexpected concentrations of risk. Regulatory authorities are increasingly focused on understanding and mitigating these systemic risks through enhanced oversight and stress testing requirements.

The competitive landscape in financial services is being reshaped as traditional banks and financial institutions seek to compete with AI-powered cryptocurrency lending platforms that can offer faster decisions, lower costs, and more personalized products. This competition is driving innovation in traditional financial services while potentially reducing the market share and profitability of conventional lending institutions that cannot match the efficiency and accessibility of AI-powered alternatives.

Cross-border capital flows are facilitated by AI-powered cryptocurrency lending platforms that can assess credit risk across different jurisdictions and currencies without requiring traditional banking relationships or correspondent banking networks. This capability has significant implications for international trade finance, emerging market development, and global economic integration patterns that continue to evolve as these platforms mature and gain adoption.

Technological Infrastructure and Scalability

The implementation of AI-powered credit assessment systems for cryptocurrency lending requires sophisticated technological infrastructure capable of processing vast amounts of blockchain data in real-time while maintaining high availability, security, and performance standards. These systems must handle the computational demands of machine learning algorithms, the storage requirements of comprehensive blockchain analytics, and the networking challenges of integrating multiple data sources and service providers.

Cloud computing architectures provide the scalability and flexibility required for AI credit assessment systems, enabling dynamic resource allocation based on demand patterns and computational requirements. Multi-cloud deployments distribute processing across different providers to improve resilience and avoid vendor lock-in while leveraging specialized services optimized for machine learning workloads. Container orchestration platforms like Kubernetes enable efficient deployment and management of microservices that comprise the complex ecosystem of AI lending platforms.

Distributed computing frameworks such as Apache Spark and TensorFlow enable the parallel processing of large-scale blockchain datasets required for comprehensive credit assessment. These frameworks can distribute machine learning training and inference across multiple nodes to achieve the performance levels required for real-time decision-making while managing the complexity of coordinating computations across distributed systems. Graphics processing units and specialized AI accelerators provide additional computational power for the most demanding machine learning workloads.

Data storage architectures must accommodate the unique requirements of blockchain data analysis, including time-series databases for transaction history, graph databases for relationship analysis, and traditional relational databases for structured financial information. Data lake architectures enable the storage and processing of diverse data types while maintaining the flexibility to adapt to changing analytical requirements and new data sources.

API design and integration challenges arise from the need to connect AI credit assessment systems with multiple blockchain networks, traditional financial data providers, identity verification services, and regulatory reporting systems. These integrations must maintain high performance and reliability while handling the diverse data formats, authentication mechanisms, and rate limiting policies of different service providers. Comprehensive trading platforms demonstrate the complexity of integrating multiple data sources and services in financial applications.

Monitoring and observability systems track the performance, accuracy, and operational health of AI credit assessment systems while providing insights into model behavior and system performance that enable proactive maintenance and optimization. These systems must detect anomalies in model predictions, identify performance degradation, and provide alerting mechanisms that enable rapid response to system issues or security incidents.

Future Developments and Emerging Technologies

The future evolution of AI-powered credit assessment in cryptocurrency lending will be shaped by advances in artificial intelligence research, blockchain technology development, and regulatory framework evolution that collectively enable new capabilities and applications while addressing current limitations and challenges. Emerging technologies offer the potential for more sophisticated risk assessment, enhanced privacy protection, and improved user experiences that could further accelerate adoption and innovation in decentralized finance.

Quantum computing represents a potential paradigm shift for AI credit assessment systems, offering computational capabilities that could enable more sophisticated machine learning algorithms and cryptographic methods while also posing security challenges for current encryption and privacy protection mechanisms. Quantum machine learning algorithms could process blockchain data more efficiently and identify patterns that are computationally intractable for classical computers, potentially revolutionizing credit risk assessment accuracy and speed.

Federated learning architectures enable collaborative model training across multiple lending platforms without sharing sensitive data, potentially improving model accuracy while maintaining competitive advantages and privacy protection. These approaches could create industry-wide credit assessment standards while allowing individual platforms to maintain their proprietary advantages and comply with data protection regulations.

Advanced natural language processing techniques integrated with social media analysis and alternative data sources could provide additional insights into borrower creditworthiness and risk characteristics. These systems could analyze communication patterns, professional networks, and online behavior to supplement blockchain analytics with broader indicators of financial responsibility and business success.

Biometric authentication and behavioral analysis technologies offer potential solutions for identity verification and fraud prevention in cryptocurrency lending while maintaining user privacy and convenience. These systems could verify borrower identity without traditional documentation requirements while detecting potential account takeovers or identity theft attempts through analysis of typing patterns, device usage, and other behavioral characteristics.

Internet of Things integration could enable new forms of collateral verification and asset monitoring that expand the range of assets that can secure cryptocurrency loans. Smart contracts could automatically monitor collateral conditions and trigger appropriate responses based on real-time asset status, location, and condition data provided by IoT sensors and devices.

Central bank digital currencies and stablecoins backed by traditional financial institutions could bridge the gap between traditional and cryptocurrency lending markets, enabling AI systems to access broader data sources while reducing volatility risks associated with cryptocurrency collateral. These developments could accelerate institutional adoption of AI-powered cryptocurrency lending while creating new regulatory and technical integration challenges.

Conclusion and Industry Outlook

AI-powered credit assessment represents a transformative development in cryptocurrency lending that addresses fundamental challenges in decentralized finance while creating new opportunities for innovation, financial inclusion, and economic growth. The sophisticated machine learning algorithms and blockchain analytics capabilities demonstrated by current systems provide a foundation for continued evolution and improvement that could reshape global credit markets and financial services delivery.

The integration of artificial intelligence with cryptocurrency lending platforms has demonstrated clear benefits in terms of risk assessment accuracy, operational efficiency, and user accessibility while highlighting important considerations related to privacy protection, regulatory compliance, and systemic risk management. As these systems continue to mature and gain adoption, their impact on traditional financial services and global economic patterns will likely accelerate and intensify.

The future success of AI-powered cryptocurrency lending will depend on continued technological innovation, thoughtful regulatory development, and industry collaboration to address challenges while maximizing benefits for all stakeholders. The potential for these systems to democratize access to credit and create more efficient capital markets represents a significant opportunity for positive economic impact, particularly in underserved markets and developing economies.

Investment in research and development, regulatory clarity, and infrastructure development will be critical for realizing the full potential of AI-powered credit assessment in cryptocurrency lending while managing associated risks and challenges. The continued evolution of this technology represents one of the most promising developments in the intersection of artificial intelligence and decentralized finance, with implications that extend far beyond the immediate cryptocurrency ecosystem.

Advanced analytics and market intelligence tools will continue to play an essential role in supporting the development and operation of AI-powered credit assessment systems as they evolve to meet the changing needs of global financial markets and regulatory requirements.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency lending involves significant risks including total loss of funds, regulatory changes, and market volatility. AI-powered credit assessment systems are experimental technologies that may contain errors or biases. Always conduct thorough research and consult with qualified professionals before making financial decisions. Past performance does not guarantee future results. Regulatory frameworks for cryptocurrency lending and AI-powered financial services continue to evolve and may impact the availability and operation of these systems.