The Golden Age of Crypto Interest Accounts

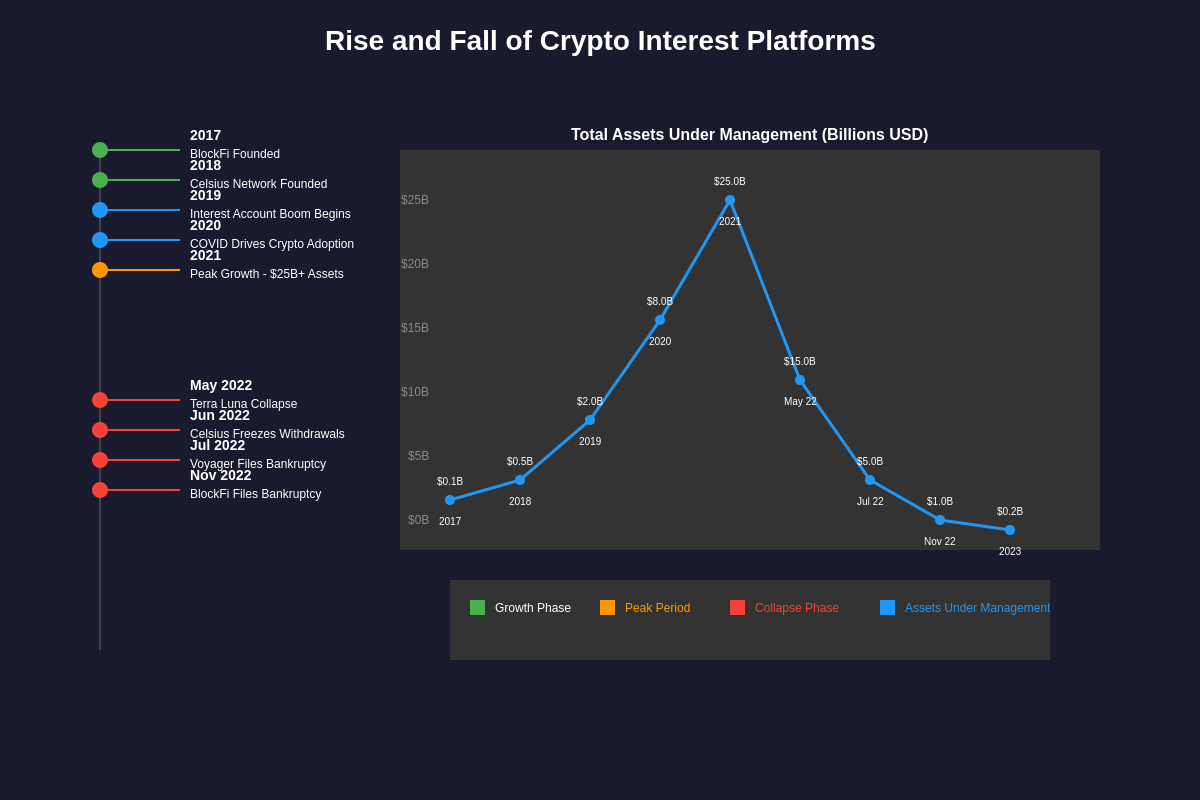

The cryptocurrency industry experienced an unprecedented period of growth and innovation between 2019 and 2022, characterized by the emergence of platforms promising extraordinary returns on digital asset deposits through what became known as crypto interest accounts. These platforms, led by companies like BlockFi, Celsius Network, and Voyager Digital, attracted billions of dollars from retail and institutional investors by offering yields that traditional banking products simply could not match, with some platforms advertising annual percentage yields exceeding 18% on major cryptocurrencies like Bitcoin and Ethereum.

https://www.tradingview.com/pine-script-reference/v6/?aff_id=112991&source=pine-04-tradingview

The fundamental promise of these platforms was deceptively simple yet revolutionary in concept: users could deposit their cryptocurrency holdings and earn substantial interest payments while maintaining exposure to the underlying asset’s price appreciation. This model attracted millions of users who saw an opportunity to generate passive income from their crypto holdings while the broader market experienced significant growth, creating what many described as a win-win scenario that seemed too good to be true.

The business models underlying these crypto interest accounts varied significantly, but most relied on a combination of lending activities, trading strategies, and yield farming operations that generated returns supposedly sufficient to pay the advertised interest rates while maintaining healthy profit margins. Platforms marketed themselves as sophisticated financial institutions capable of generating alpha through proprietary trading strategies, institutional relationships, and advanced risk management systems that traditional banks lacked.

The regulatory environment during this period was characterized by significant ambiguity, with most crypto interest platforms operating in jurisdictions with limited oversight while attracting customers from around the world through aggressive marketing campaigns that emphasized security, transparency, and regulatory compliance. Many platforms obtained various licenses and certifications to enhance their credibility, though the actual protection these provided to users would later prove insufficient when the business models collapsed.

The BlockFi Phenomenon and Business Model Evolution

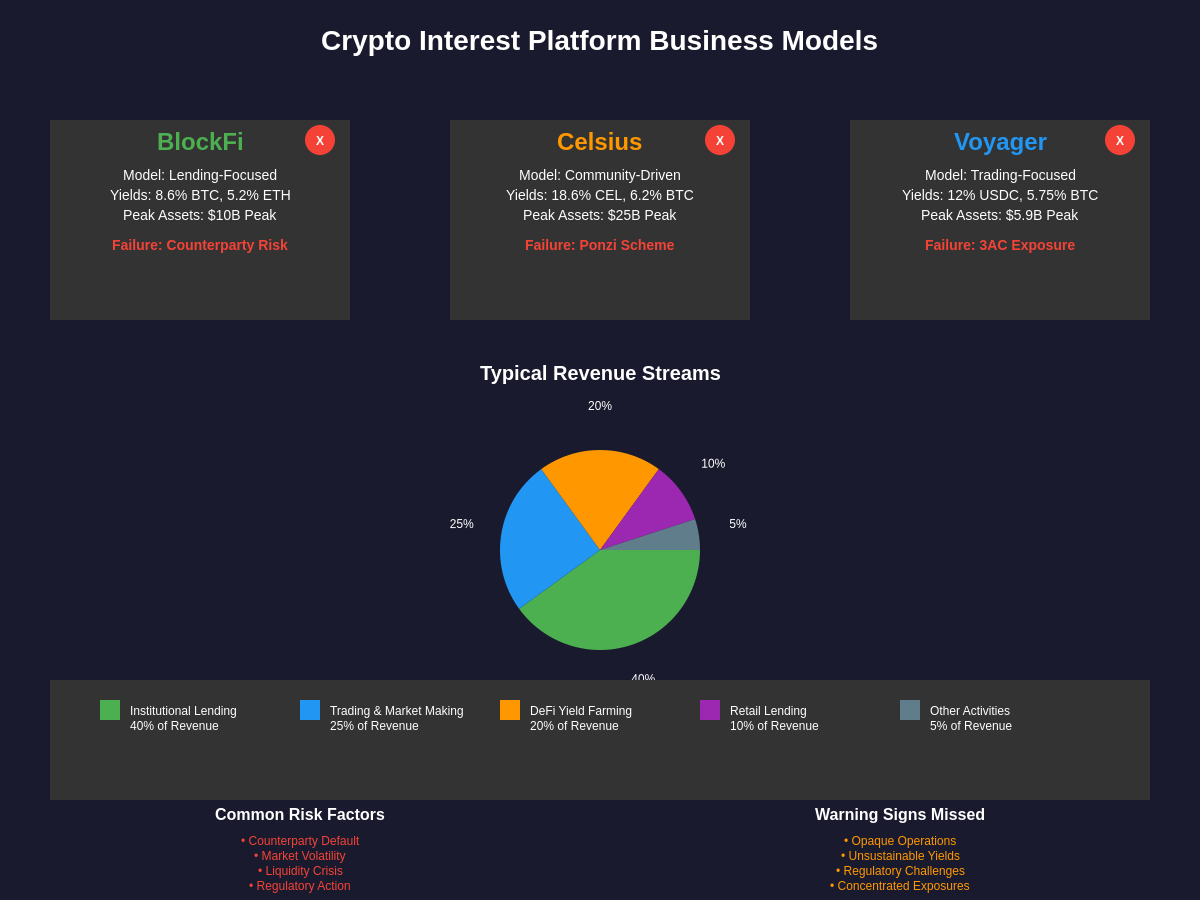

BlockFi emerged as one of the pioneering companies in the crypto interest account space, founded in 2017 by Zac Prince and Flori Marquez with the vision of creating a bridge between traditional finance and the cryptocurrency ecosystem. The platform initially focused on crypto-backed lending services, allowing users to borrow fiat currency against their cryptocurrency holdings, but gradually expanded into interest-bearing accounts that would become its primary growth driver and ultimate source of regulatory scrutiny.

The BlockFi interest account model was built around the concept of taking customer deposits and deploying them across various revenue-generating activities including lending to institutional borrowers, market making operations, and yield farming strategies across different DeFi protocols. The platform promoted itself as a safer alternative to many DeFi platforms by maintaining institutional-grade security measures, comprehensive insurance coverage, and partnerships with established financial institutions that provided additional credibility and operational infrastructure.

BlockFi’s marketing strategy emphasized the platform’s relationships with prominent investors including Galaxy Digital, Coinbase Ventures, and other well-known cryptocurrency investment firms, creating an impression of institutional backing and professional management that differentiated it from smaller competitors. The company raised significant venture capital funding across multiple rounds, reaching a valuation of over $3 billion at its peak, which provided additional validation for users considering whether to trust the platform with their cryptocurrency holdings.

The platform’s interest rate structure was designed to be competitive with other crypto interest platforms while appearing sustainable through diversified revenue streams, though the specific mechanics of how these rates were generated remained largely opaque to users. BlockFi offered tiered interest rates based on account balances and cryptocurrency types, with promotional rates occasionally reaching double digits for popular cryptocurrencies during periods of intense competition with rival platforms.

The integration of traditional financial services with cryptocurrency operations created unique operational complexities for BlockFi, requiring the company to navigate multiple regulatory frameworks while maintaining relationships with traditional banking partners who were often skeptical of cryptocurrency-related activities. These challenges would ultimately contribute to the platform’s difficulties as regulatory scrutiny increased and market conditions deteriorated throughout 2022.

Celsius Network’s Meteoric Rise and Community Building

Celsius Network, founded by Alex Mashinsky in 2017, represented perhaps the most ambitious and controversial example of the crypto interest account phenomenon, growing from a startup concept to a platform managing over $25 billion in assets at its peak through an aggressive combination of high yield offerings, community engagement, and promotional activities that created an almost cult-like following among cryptocurrency enthusiasts.

The Celsius business model was built around the concept of “unbanking” traditional financial institutions by offering dramatically higher interest rates than traditional banks while positioning itself as a community-driven platform that shared profits with users rather than enriching shareholders. This messaging resonated strongly with cryptocurrency enthusiasts who were already skeptical of traditional financial institutions and attracted to the idea of participating in a more equitable financial system.

Mashinsky’s background as a serial entrepreneur and inventor, including claims of inventing Voice over Internet Protocol (VoIP) technology, provided credibility and helped establish Celsius as a technology-forward platform capable of generating superior returns through proprietary trading strategies and institutional relationships. The platform’s weekly “AMA” (Ask Me Anything) sessions hosted by Mashinsky became legendary within the crypto community, often featuring bold predictions about cryptocurrency prices and confident assertions about Celsius’s ability to weather any market conditions.

The Celsius token (CEL) played a central role in the platform’s ecosystem, offering users enhanced interest rates and other benefits for holding and using the token within the platform’s services. This created a self-reinforcing mechanism where user loyalty was rewarded with additional benefits, while the token’s price appreciation provided additional marketing ammunition for the platform’s growth strategy and helped attract new users seeking both interest payments and token appreciation.

The platform’s lending activities were presented as sophisticated institutional operations involving carefully vetted counterparties and comprehensive risk management procedures, though the specific details of these operations remained largely confidential for competitive reasons. Celsius claimed to generate returns through a combination of lending to institutional borrowers, market making activities, and strategic investments in various cryptocurrency projects and trading strategies.

The community aspect of Celsius was particularly noteworthy, with the platform hosting regular events, meetups, and promotional activities that created strong emotional connections between users and the platform. This community building proved to be both a significant asset during the platform’s growth phase and a major liability when problems emerged, as loyal users continued depositing funds even as warning signs became increasingly apparent to outside observers.

Risk Management Failures and Warning Signs

The crypto interest account industry’s approach to risk management was characterized by significant gaps between public representations and actual practices, with most platforms failing to adequately disclose the true risks associated with their business models or implement sufficient safeguards to protect user funds during periods of market stress. These failures became increasingly apparent as market conditions deteriorated throughout 2022, revealing fundamental flaws in how these platforms assessed and managed various types of risk.

Counterparty risk represented perhaps the most significant and underappreciated danger facing crypto interest platforms, with many companies extending large unsecured loans to trading firms, hedge funds, and other institutional borrowers without adequate collateral or risk assessment procedures. The interconnected nature of the cryptocurrency industry meant that many of these borrowers were exposed to similar market risks, creating concentration risk that was often not properly disclosed to users or adequately modeled by platform risk management systems.

Market risk management at many platforms proved inadequate for the extreme volatility that characterized cryptocurrency markets during 2022, with some platforms failing to maintain adequate liquidity buffers or implement proper hedging strategies to protect against adverse price movements. The correlation between different cryptocurrency assets during market downturns meant that diversification strategies that appeared effective during bull markets provided little protection when needed most.

Operational risk factors including inadequate internal controls, insufficient segregation of customer funds, and poor governance structures created additional vulnerabilities that were exploited during the crisis period. Many platforms lacked proper financial reporting systems, independent auditing procedures, or effective oversight mechanisms that might have identified problems before they became catastrophic for users.

https://www.tradingview.com/symbols/BTCUSD/?aff_id=112991&source=pine-04-tradingview

The transparency challenges facing crypto interest platforms made it difficult for users and regulators to assess the true risk profile of these operations, with most platforms providing limited information about their specific lending activities, counterparty exposures, or risk management procedures. This lack of transparency was often justified as necessary for competitive reasons, but ultimately prevented proper risk assessment by stakeholders who might have been able to identify problems earlier.

Regulatory arbitrage strategies employed by many platforms, including operating from jurisdictions with limited oversight or structuring operations to avoid specific regulatory requirements, created additional risks that were often not properly communicated to users. These strategies may have provided short-term competitive advantages but ultimately left platforms and users vulnerable when regulatory scrutiny increased or when platforms needed to access traditional financial system resources during crisis periods.

The Terra Luna Collapse and Market Contagion

The collapse of the Terra ecosystem in May 2022, including the depegging of TerraUSD (UST) and the subsequent crash of LUNA tokens, served as the catalyst that exposed the interconnected vulnerabilities throughout the crypto interest account industry and triggered a cascade of failures that would ultimately bring down several major platforms. The Terra collapse demonstrated how quickly confidence could evaporate in cryptocurrency markets and how concentrated exposures to specific projects could create systemic risks across the broader ecosystem.

Many crypto interest platforms had significant direct or indirect exposures to the Terra ecosystem through various lending relationships, token holdings, or trading strategies that were not properly disclosed to users or adequately hedged against the risk of a complete ecosystem collapse. The speed and severity of the Terra crash caught many risk management systems off guard, creating immediate liquidity pressures and margin calls that platforms struggled to meet without accessing customer funds.

The psychological impact of the Terra collapse extended far beyond the direct financial losses, creating a crisis of confidence that led to widespread withdrawal requests across all crypto interest platforms as users began questioning the sustainability of high yield offerings and the adequacy of platform risk management procedures. This shift in sentiment created a classic bank run scenario where platforms faced enormous withdrawal pressure precisely when their ability to meet those withdrawals was most constrained.

Three Arrows Capital (3AC), one of the largest cryptocurrency hedge funds and a major borrower from several crypto interest platforms, became insolvent following its exposure to the Terra collapse, creating immediate and severe losses for platforms that had extended large unsecured loans to the fund. The 3AC bankruptcy revealed the extent to which major crypto interest platforms were exposed to a single counterparty and highlighted the inadequate due diligence and risk management procedures that had allowed such concentrations to develop.

The contagion effects of the Terra collapse and 3AC bankruptcy extended throughout the cryptocurrency lending ecosystem, affecting not only direct creditors but also platforms with indirect exposures or those that were perceived as having similar risk profiles. This created a self-reinforcing cycle where platforms faced increasing withdrawal pressure and deteriorating market conditions simultaneously, making it extremely difficult to maintain operations even for platforms that had previously appeared financially stable.

The regulatory response to the Terra collapse and subsequent platform failures included increased scrutiny of cryptocurrency interest platforms, with regulators in multiple jurisdictions launching investigations and enforcement actions that further complicated the operating environment for surviving platforms. This regulatory pressure created additional operational costs and compliance requirements that further strained platform resources during an already challenging period.

The Celsius Meltdown and Customer Fallout

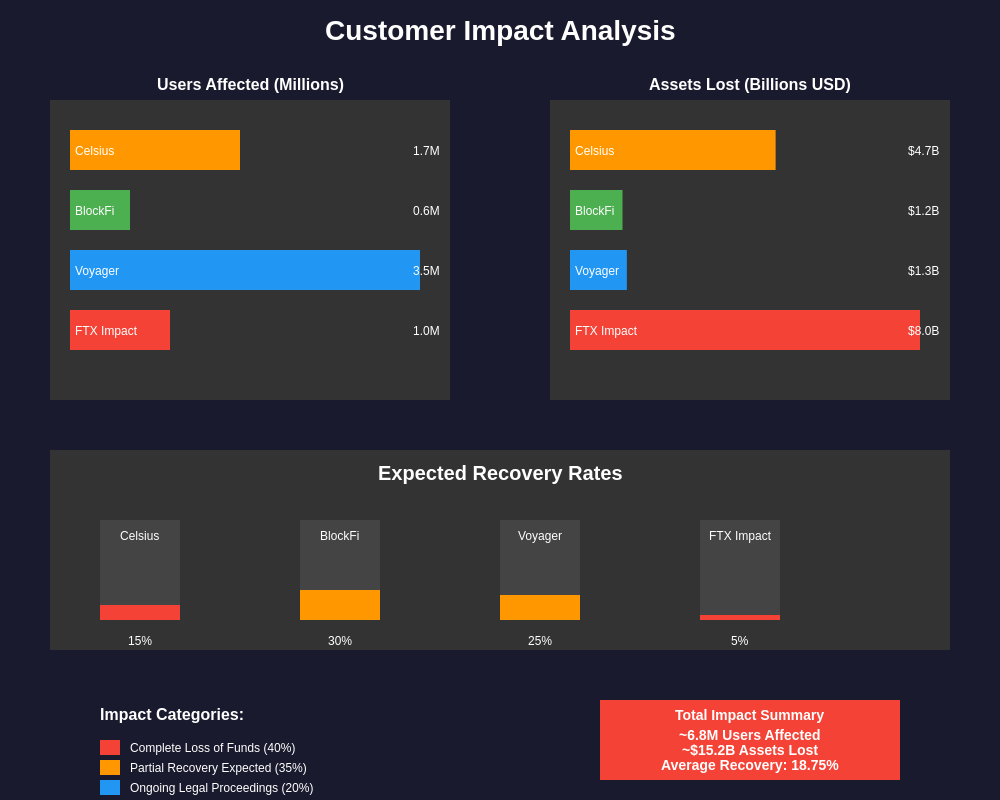

The Celsius Network collapse in June 2022 represented perhaps the most dramatic and devastating failure in the crypto interest account space, affecting over 1.7 million users and involving approximately $4.7 billion in customer assets that became frozen when the platform announced the suspension of all withdrawals, swaps, and transfers. The Celsius bankruptcy became a cautionary tale about the risks of unregulated cryptocurrency lending and the inadequate protections available to retail investors in the cryptocurrency ecosystem.

The immediate catalyst for Celsius’s collapse was a liquidity crisis triggered by massive withdrawal requests following the Terra ecosystem collapse and growing concerns about the platform’s financial stability, but subsequent bankruptcy proceedings revealed much deeper problems including inadequate risk management procedures, questionable lending practices, and potential misuse of customer funds that had been developing for months or years before the final crisis.

Bankruptcy court documents revealed that Celsius had been operating essentially as a Ponzi scheme during its final months, using new customer deposits to fund withdrawal requests from existing customers while maintaining the facade of normal operations through continued marketing activities and public reassurances from leadership. This practice meant that customers who deposited funds during the platform’s final months were essentially funding the withdrawals of earlier customers rather than participating in legitimate yield-generating activities.

The role of Alex Mashinsky during the Celsius collapse became particularly controversial, with evidence emerging that he had been withdrawing his own cryptocurrency holdings from the platform while publicly encouraging users to continue depositing and maintaining their holdings. This behavior, along with other questionable actions by platform leadership, led to criminal charges and civil enforcement actions that highlighted the inadequate governance and ethical standards that characterized much of the crypto interest account industry.

The customer recovery process for Celsius users has been complicated by the complex legal and regulatory framework governing cryptocurrency bankruptcy proceedings, with different classes of creditors facing vastly different recovery prospects depending on the specific terms under which they held assets on the platform. The lack of deposit insurance or other customer protections meant that most users faced the prospect of losing most or all of their deposited cryptocurrency.

The broader impact of the Celsius collapse extended far beyond the immediate financial losses to users, creating lasting damage to the reputation of the cryptocurrency industry and providing ammunition for critics who argued that the sector was characterized by fraud, mismanagement, and inadequate consumer protections. The collapse also highlighted the need for better regulatory frameworks to protect consumers while allowing legitimate innovation to continue.

BlockFi’s Regulatory Challenges and Eventual Collapse

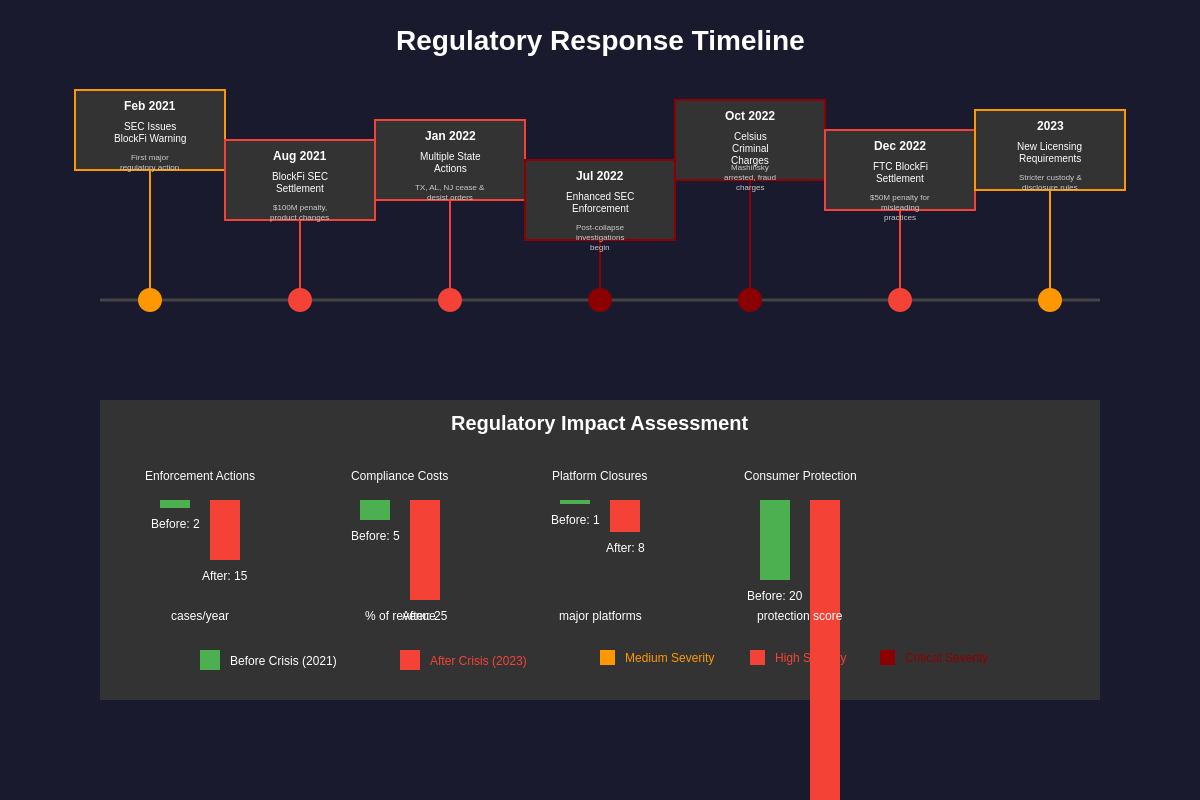

BlockFi’s relationship with regulatory authorities was complicated from the platform’s inception, as the company operated in a legal gray area where traditional securities regulations intersected with emerging cryptocurrency business models in ways that were not clearly defined by existing regulatory frameworks. The platform’s attempts to navigate this complex environment ultimately proved unsuccessful, leading to significant enforcement actions and regulatory settlements that contributed to its eventual bankruptcy.

The Securities and Exchange Commission (SEC) and multiple state securities regulators took enforcement actions against BlockFi related to its interest account offerings, arguing that these products constituted unregistered securities offerings that violated existing investor protection laws. These enforcement actions resulted in significant financial penalties and operational restrictions that fundamentally altered BlockFi’s business model and competitive position within the crypto interest account market.

The regulatory settlement agreements required BlockFi to cease offering its interest accounts to new customers and implement significant changes to its existing operations, including enhanced disclosure requirements, modified terms of service, and additional compliance procedures that increased operational costs while reducing revenue potential. These requirements made it extremely difficult for BlockFi to compete effectively with platforms operating in less regulated jurisdictions or with different legal structures.

The Federal Trade Commission (FTC) also brought enforcement actions against BlockFi related to allegedly misleading marketing practices and inadequate disclosure of risks associated with the platform’s services, resulting in additional financial penalties and operational restrictions that further constrained the company’s ability to operate profitably. These actions highlighted the challenges facing crypto interest platforms in communicating complex risk profiles to retail customers in ways that met regulatory standards.

BlockFi’s attempts to restructure its operations to comply with regulatory requirements while maintaining a viable business model proved unsuccessful, particularly as market conditions deteriorated throughout 2022 and the platform faced the same liquidity pressures and counterparty losses that affected other crypto interest platforms. The combination of regulatory compliance costs, reduced revenue opportunities, and adverse market conditions created an unsustainable situation that ultimately led to bankruptcy.

The BlockFi bankruptcy process revealed additional challenges related to customer asset recovery, with the platform’s complex operational structure and regulatory compliance requirements creating complications for determining how customer assets should be treated in bankruptcy proceedings. The lack of clear legal precedents for cryptocurrency platform bankruptcies meant that the recovery process was likely to be lengthy and uncertain for affected users.

Regulatory Response and Policy Implications

The collapse of major crypto interest platforms prompted a comprehensive regulatory response from authorities in multiple jurisdictions, as regulators sought to address the consumer protection failures and systemic risks that had been revealed by the industry’s spectacular collapse. This regulatory response has had far-reaching implications for the cryptocurrency industry and has fundamentally altered the landscape for companies seeking to offer yield-generating products to retail investors.

The Securities and Exchange Commission significantly increased its enforcement activities targeting cryptocurrency interest platforms, bringing cases against multiple companies for allegedly offering unregistered securities and implementing enhanced supervision and examination procedures for cryptocurrency-related businesses. These enforcement actions established important legal precedents regarding how traditional securities laws apply to cryptocurrency business models and clarified that many crypto interest products would be subject to existing investor protection requirements.

State securities regulators also played a crucial role in the regulatory response, with many states bringing their own enforcement actions and implementing new licensing requirements specifically designed to address the risks associated with cryptocurrency lending and interest account products. This state-level activity created a complex patchwork of regulatory requirements that made it challenging for companies to operate nationally while maintaining compliance with all applicable regulations.

The Federal Deposit Insurance Corporation (FDIC) and other banking regulators issued guidance clarifying that cryptocurrency interest accounts were not eligible for deposit insurance protection and warning consumers about the risks associated with these products. This guidance helped educate consumers about the fundamental differences between traditional bank deposits and cryptocurrency interest accounts, though it came too late to prevent significant consumer losses.

https://www.tradingview.com/chart/?symbol=CRYPTOCAP%3ATOTAL&aff_id=112991&source=pine-04-tradingview

International regulatory coordination has become increasingly important as regulators recognize that cryptocurrency markets are global in nature and that regulatory arbitrage can undermine consumer protection efforts in individual jurisdictions. Organizations like the Financial Stability Board and the Bank for International Settlements have developed frameworks for coordinating regulatory approaches to cryptocurrency markets that are being implemented by member countries.

The regulatory response has also included enhanced disclosure requirements for cryptocurrency companies, with many jurisdictions implementing rules requiring clearer communication about risks, more detailed financial reporting, and stronger governance structures. These requirements are designed to provide consumers with the information they need to make informed decisions while ensuring that companies maintain adequate safeguards to protect customer assets.

Impact on Traditional Financial Services

The rise and fall of crypto interest accounts has had significant implications for traditional financial services, both in terms of competitive dynamics during the growth phase and regulatory spillover effects following the industry’s collapse. Traditional banks initially viewed crypto interest platforms as a niche threat that primarily affected early adopters and cryptocurrency enthusiasts, but the scale of customer migration and the marketing effectiveness of high-yield offerings eventually prompted more serious competitive responses.

Many traditional financial institutions began developing their own cryptocurrency-related products and services during the height of the crypto interest account boom, including custody services, trading platforms, and investment products designed to capture some of the customer interest that was flowing to specialized cryptocurrency platforms. These efforts were often hampered by regulatory uncertainty, internal risk management concerns, and the technical complexity of integrating cryptocurrency operations with existing banking infrastructure.

The collapse of major crypto interest platforms provided validation for the conservative approach taken by most traditional financial institutions, while also highlighting the importance of proper risk management, regulatory compliance, and customer protection measures that had been developed over decades of banking industry evolution. This experience reinforced the value of traditional banking regulations and deposit insurance systems that many cryptocurrency enthusiasts had dismissed as unnecessary or outdated.

Traditional financial institutions have also been affected by the regulatory response to crypto interest platform failures, with banking regulators implementing enhanced supervision and risk management requirements for institutions with cryptocurrency exposures or customer relationships. These requirements have made it more challenging for traditional banks to develop cryptocurrency-related products and services, potentially slowing the integration of cryptocurrency and traditional finance.

The customer experience improvements and technological innovations introduced by crypto interest platforms have influenced traditional banking products, with many banks enhancing their digital offerings, improving customer communication, and developing more competitive interest rate structures in response to the challenge posed by cryptocurrency alternatives. These improvements have benefited consumers even as the cryptocurrency platforms that inspired them have largely disappeared.

The long-term implications of the crypto interest account phenomenon for traditional banking remain unclear, but the experience has demonstrated both the potential for financial innovation and the importance of appropriate regulatory frameworks and consumer protections. Traditional financial institutions are likely to continue developing cryptocurrency-related products and services, but with greater attention to risk management and regulatory compliance than was characteristic of the specialized platforms that preceded them.

Lessons Learned and Risk Assessment

The spectacular rise and fall of crypto interest accounts provides valuable lessons about financial innovation, risk management, and consumer protection that extend far beyond the cryptocurrency industry and have relevance for regulators, financial institutions, and investors across all market sectors. These lessons highlight both the potential benefits of financial innovation and the importance of maintaining appropriate safeguards to protect consumers and maintain market stability.

The importance of transparency in financial services was dramatically illustrated by the crypto interest account failures, as platforms that maintained opacity about their operations and risk exposures were ultimately unable to maintain customer confidence when market conditions deteriorated. Future financial innovation efforts should prioritize clear communication about risks, detailed disclosure of operational practices, and regular reporting that allows stakeholders to make informed decisions about participation.

Risk management practices in the crypto interest account industry proved fundamentally inadequate for the volatility and interconnectedness that characterized cryptocurrency markets, with most platforms failing to maintain adequate liquidity buffers, implement proper diversification strategies, or develop contingency plans for adverse market conditions. These failures highlight the importance of stress testing, scenario planning, and conservative risk management practices that can protect customer assets during challenging periods.

The regulatory environment for financial innovation requires careful balance between allowing beneficial innovation and maintaining appropriate consumer protections, with the crypto interest account experience demonstrating the dangers of both excessive regulatory restraint and overly aggressive enforcement after problems have already developed. Proactive regulatory engagement with emerging business models may be more effective than reactive enforcement actions in protecting consumers while preserving innovation incentives.

Consumer education and financial literacy proved crucial factors in the crypto interest account phenomenon, as many users who suffered losses had inadequate understanding of the risks they were accepting in exchange for high yield offerings. Educational initiatives that help consumers understand the relationship between risk and return, the importance of diversification, and the protections available in different types of financial products could help prevent similar losses in future innovation cycles.

The systemic risk implications of interconnected financial platforms became apparent during the crypto interest account collapse, as problems at individual platforms quickly spread throughout the ecosystem through shared counterparties, similar business models, and psychological contagion effects. Financial system stability considerations should be incorporated into the regulatory framework for emerging financial services to prevent localized problems from becoming systemic crises.

The Current Landscape and Future Outlook

The crypto interest account industry as it existed during its peak period from 2019 to 2022 has largely ceased to exist, with most major platforms either bankrupt, under regulatory enforcement actions, or operating under significantly restricted business models that bear little resemblance to their original offerings. The few surviving platforms have generally pivoted toward more traditional financial services or have relocated to jurisdictions with more favorable regulatory environments.

The regulatory environment for cryptocurrency interest products continues to evolve, with most jurisdictions implementing stricter requirements for licensing, disclosure, and consumer protection that make it challenging to operate profitable high-yield cryptocurrency lending businesses. These regulatory changes have effectively eliminated many of the business models that supported the original crypto interest account boom, while creating opportunities for more compliant and conservative approaches to cryptocurrency financial services.

Traditional financial institutions have gradually increased their cryptocurrency-related service offerings, but generally with much more conservative risk management approaches and lower yield offerings than were characteristic of the specialized platforms that preceded them. This transition represents a maturation of the cryptocurrency financial services sector, with greater emphasis on regulatory compliance and customer protection rather than maximum yield generation.

The customer recovery process for users of failed crypto interest platforms continues to progress through various bankruptcy proceedings and legal processes, though most users face the prospect of recovering only a fraction of their deposited assets. These proceedings have provided valuable precedents for how cryptocurrency platform failures should be handled, which may improve outcomes for customers of any future platform failures.

https://www.tradingview.com/symbols/BTCUSD/technicals/?aff_id=112991&source=pine-04-tradingview

Innovation in cryptocurrency financial services continues, but with greater emphasis on regulatory compliance, risk management, and customer protection than was characteristic of the previous generation of platforms. New business models are emerging that seek to provide yield opportunities for cryptocurrency holders while maintaining appropriate safeguards and regulatory compliance, though these generally offer lower returns than the unsustainable rates that characterized the previous boom period.

The long-term outlook for cryptocurrency interest accounts depends largely on the development of sustainable business models that can generate attractive returns for customers while maintaining appropriate risk management and regulatory compliance standards. The experience of the 2019-2022 period suggests that extremely high yield offerings are likely unsustainable, but more modest returns may be achievable through legitimate business activities that properly manage risk and maintain customer asset protection.

Conclusion and Market Evolution

The rise and fall of crypto interest accounts represents one of the most significant episodes in cryptocurrency industry history, demonstrating both the enormous potential for financial innovation and the devastating consequences that can result when innovation proceeds without adequate risk management, regulatory oversight, or consumer protection measures. The billions of dollars in customer losses and the destruction of major industry players serves as a lasting cautionary tale about the importance of sustainable business models and appropriate safeguards in financial services.

The crypto interest account phenomenon attracted millions of customers and billions of dollars in assets by promising returns that traditional financial institutions could not match, but these promises ultimately proved unsustainable when underlying business models were tested by adverse market conditions and increased regulatory scrutiny. The collapse of major platforms like Celsius Network and BlockFi revealed fundamental flaws in risk management, governance, and customer asset protection that had been masked by favorable market conditions and aggressive marketing strategies.

The regulatory response to these failures has fundamentally altered the landscape for cryptocurrency financial services, with new requirements for licensing, disclosure, and consumer protection that make it much more challenging to operate high-yield cryptocurrency lending businesses. While these regulatory changes have reduced innovation and eliminated some potentially beneficial services, they have also helped protect consumers from the types of losses that characterized the previous period of largely unregulated growth.

The lessons learned from the crypto interest account boom and bust extend far beyond the cryptocurrency industry, providing valuable insights about financial innovation, risk management, and consumer protection that are relevant for regulators, financial institutions, and investors across all sectors. The experience highlights the importance of maintaining appropriate balance between encouraging beneficial innovation and protecting consumers from unsustainable or fraudulent business practices.

The future of yield-generating cryptocurrency products will likely involve more conservative business models, greater regulatory compliance, and stronger customer protection measures than characterized the previous generation of platforms. While this may result in lower returns for customers, it should also provide greater stability and security that will be essential for the long-term development of legitimate cryptocurrency financial services.

The cryptocurrency industry continues to evolve and mature, with the painful lessons learned from the crypto interest account failures contributing to the development of more sustainable and responsible business practices. The ultimate legacy of this episode may be the establishment of better regulatory frameworks and industry standards that protect consumers while allowing beneficial innovation to continue, creating a foundation for more stable and trustworthy cryptocurrency financial services in the future.

Disclaimer: This content is for informational purposes only and should not be considered financial advice. Cryptocurrency investments carry significant risks, including the potential for total loss of capital. Past performance does not guarantee future results. Always conduct thorough research and consider consulting with qualified financial professionals before making investment decisions. The author and publisher are not responsible for any financial losses that may result from the use of this information.