Explore CBDC trading opportunities and track digital currency developments with advanced technical analysis tools.

The Digital Revolution in Central Banking

Central Bank Digital Currencies represent one of the most significant transformations in monetary policy and banking infrastructure since the abandonment of the gold standard, fundamentally altering how governments issue currency, conduct monetary policy, and interact with financial institutions and citizens. The emergence of CBDCs marks a paradigm shift from traditional fiat currency systems toward programmable digital money that combines the stability and backing of central bank reserves with the technological advantages of blockchain and distributed ledger technologies.

The motivation for CBDC development stems from multiple converging factors including the declining use of physical cash, the rise of private digital currencies like Bitcoin and stablecoins, the need for more efficient payment systems, and the desire for central banks to maintain monetary sovereignty in an increasingly digital economy. Major economies worldwide are racing to develop and deploy CBDC systems that can provide the benefits of digital payments while preserving the central bank’s role as the primary issuer of money and conductor of monetary policy.

Historical Context and Global Development Timeline

The concept of central bank digital currencies has evolved rapidly from theoretical discussions to practical pilot programs and full-scale implementations across numerous jurisdictions, with China’s digital yuan leading the way as the first major economy to deploy a retail CBDC at scale. The People’s Bank of China began experimenting with digital currency concepts as early as 2014, launching pilot programs in major cities and expanding to cover over 100 million users by 2024.

The European Central Bank has pursued a more cautious approach with its digital euro project, conducting extensive research and consultation phases before moving toward implementation. The ECB’s methodical approach reflects concerns about privacy, financial stability, and the potential impact on commercial banking that have characterized European regulatory approaches to financial innovation. Similarly, the Federal Reserve has taken a research-focused approach to digital dollars, publishing discussion papers and conducting pilot programs while avoiding commitments to full deployment timelines.

The Bank of England, Bank of Japan, and numerous other central banks have established dedicated CBDC research teams and begun collaboration through international forums like the Bank for International Settlements, sharing technical specifications, regulatory frameworks, and lessons learned from pilot programs. This collaborative approach reflects the global nature of modern financial systems and the recognition that CBDC design decisions in major economies will have significant spillover effects on international trade and capital flows.

Smaller economies and developing nations have often moved more aggressively toward CBDC implementation, viewing digital currencies as opportunities to leapfrog traditional banking infrastructure limitations and provide financial services to unbanked populations. The Eastern Caribbean Central Bank’s DCash project and Nigeria’s eNaira represent examples of how CBDCs can address specific regional challenges while testing technical approaches that may inform larger implementations.

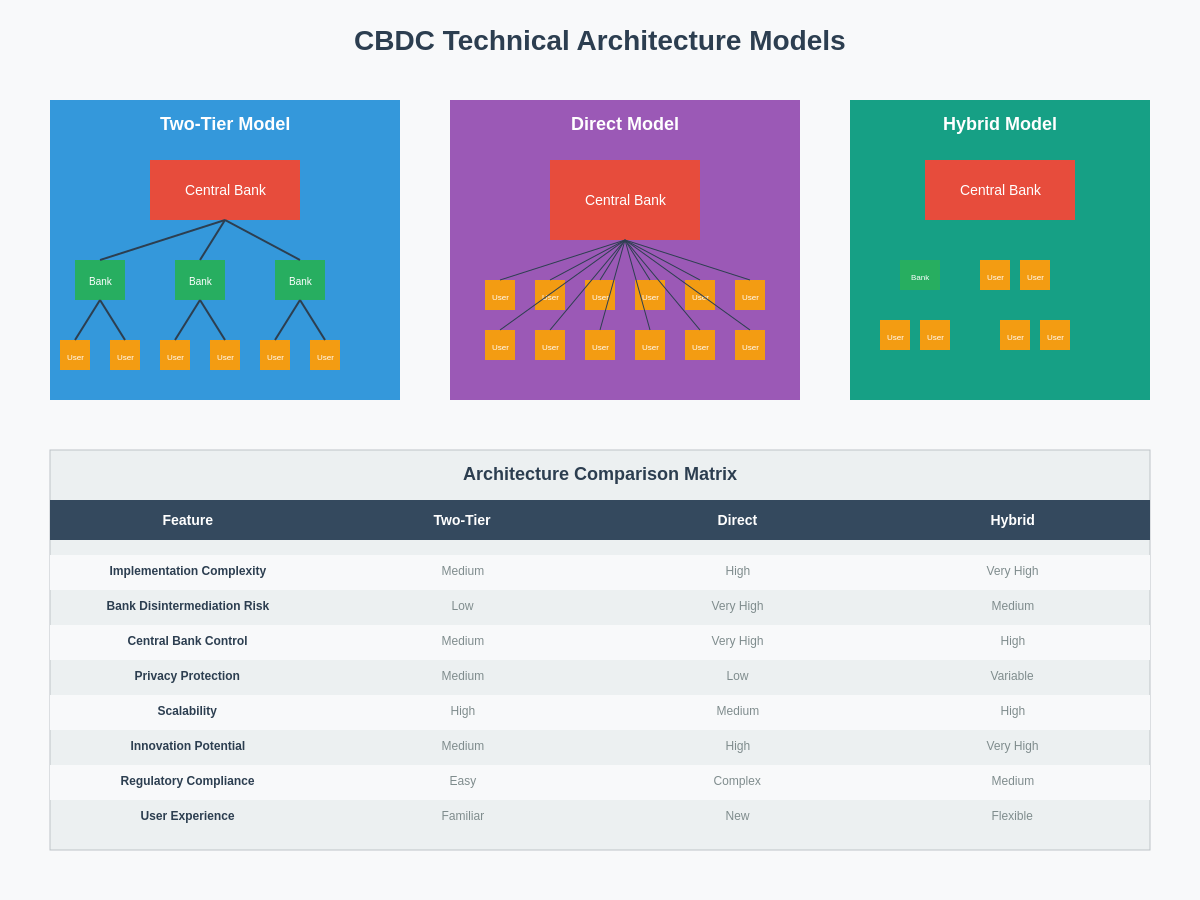

Technical Architecture and Implementation Models

The technical architecture underlying CBDC systems varies significantly based on design choices regarding centralization, privacy, programmability, and interoperability with existing payment systems. Most CBDC implementations utilize some form of distributed ledger technology, though the specific blockchain protocols, consensus mechanisms, and network topologies differ substantially based on central bank priorities and technical requirements.

Two-tier architecture models have emerged as the dominant approach for retail CBDCs, with central banks issuing digital currency to commercial banks and other authorized intermediaries who then distribute CBDCs to end users through existing account relationships and payment interfaces. This model preserves the role of commercial banks in customer onboarding, compliance, and customer service while enabling central banks to maintain control over monetary policy and systemic risk management.

Direct central bank accounts represent an alternative model where citizens hold CBDC directly with the central bank, eliminating intermediaries but requiring central banks to develop retail banking capabilities and customer service infrastructure. This model offers greater central bank control but raises concerns about competition with commercial banks and the central bank’s capacity to serve millions of individual accounts.

Advanced CBDC analysis tools enable traders and analysts to monitor the development and impact of digital currencies on traditional financial markets.

Hybrid models combine elements of both approaches, allowing users to hold CBDCs in commercial bank accounts while enabling direct central bank oversight and the ability to bypass intermediaries during crisis situations. These models attempt to balance the efficiency of commercial bank distribution with the control and stability provided by direct central bank relationships.

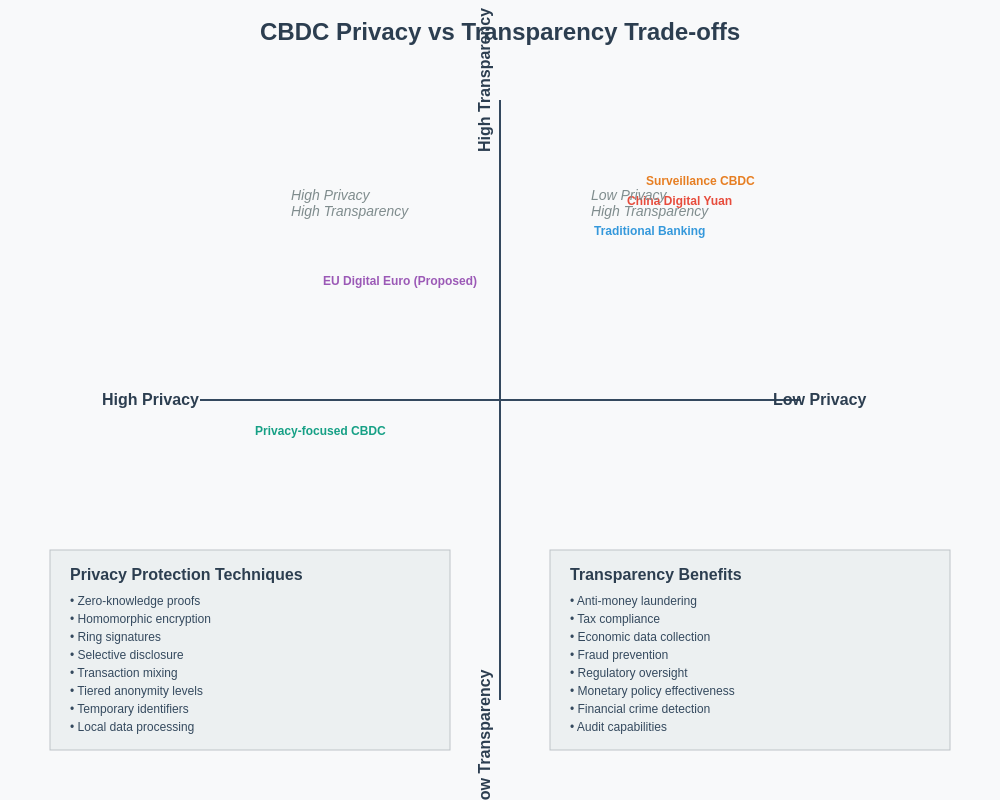

Privacy-preserving technologies represent a critical component of CBDC technical architecture, with different implementations offering varying levels of anonymity and transaction privacy. Zero-knowledge proof systems, homomorphic encryption, and selective disclosure mechanisms enable CBDCs to provide privacy protections similar to physical cash while maintaining the ability to prevent money laundering, tax evasion, and terrorist financing.

Programmable money features distinguish CBDCs from traditional digital payment systems by enabling automated execution of monetary policy, conditional transfers, and smart contract functionality. These capabilities allow central banks to implement negative interest rates more effectively, provide targeted stimulus payments with spending restrictions, and automate compliance with regulatory requirements.

Monetary Policy Implications and Interest Rate Mechanisms

Central Bank Digital Currencies provide unprecedented tools for monetary policy implementation, enabling central banks to bypass traditional transmission mechanisms and directly influence money supply, interest rates, and economic activity through programmable currency features. The ability to implement negative interest rates without the constraint of physical cash represents one of the most significant monetary policy implications of CBDC adoption, as citizens cannot simply convert digital currency to cash to avoid negative rates.

Real-time economic data collection through CBDC transaction monitoring enables central banks to observe economic activity with much greater granularity and timeliness than traditional economic indicators, potentially allowing for more precise and responsive monetary policy adjustments. The velocity of money, spending patterns, and sectoral economic activity become immediately visible to central banks through CBDC transaction data, reducing the lag time between economic changes and policy responses.

Interest rate transmission mechanisms are fundamentally altered in CBDC systems, as central banks can directly set rates on digital currency holdings rather than relying on interbank markets and commercial bank pricing decisions to transmit policy rates to consumers and businesses. This direct transmission could make monetary policy more effective while reducing the role of commercial banks in the monetary policy transmission mechanism.

Targeted monetary policy becomes feasible through programmable CBDC features, enabling central banks to provide different interest rates to different user segments, implement geographic or sectoral spending incentives, and automatically adjust monetary conditions based on real-time economic indicators. These capabilities could enhance the effectiveness of counter-cyclical monetary policy while raising questions about fairness and the appropriate scope of central bank intervention in economic allocation decisions.

The interaction between CBDC interest rates and commercial bank deposit rates creates complex dynamics that could affect the stability and profitability of traditional banking systems. If CBDC rates are set too high relative to bank deposit rates, massive disintermediation could occur as depositors move funds from commercial banks to central bank digital currencies, potentially destabilizing the banking system and reducing credit availability.

Impact on Commercial Banking and Financial Intermediation

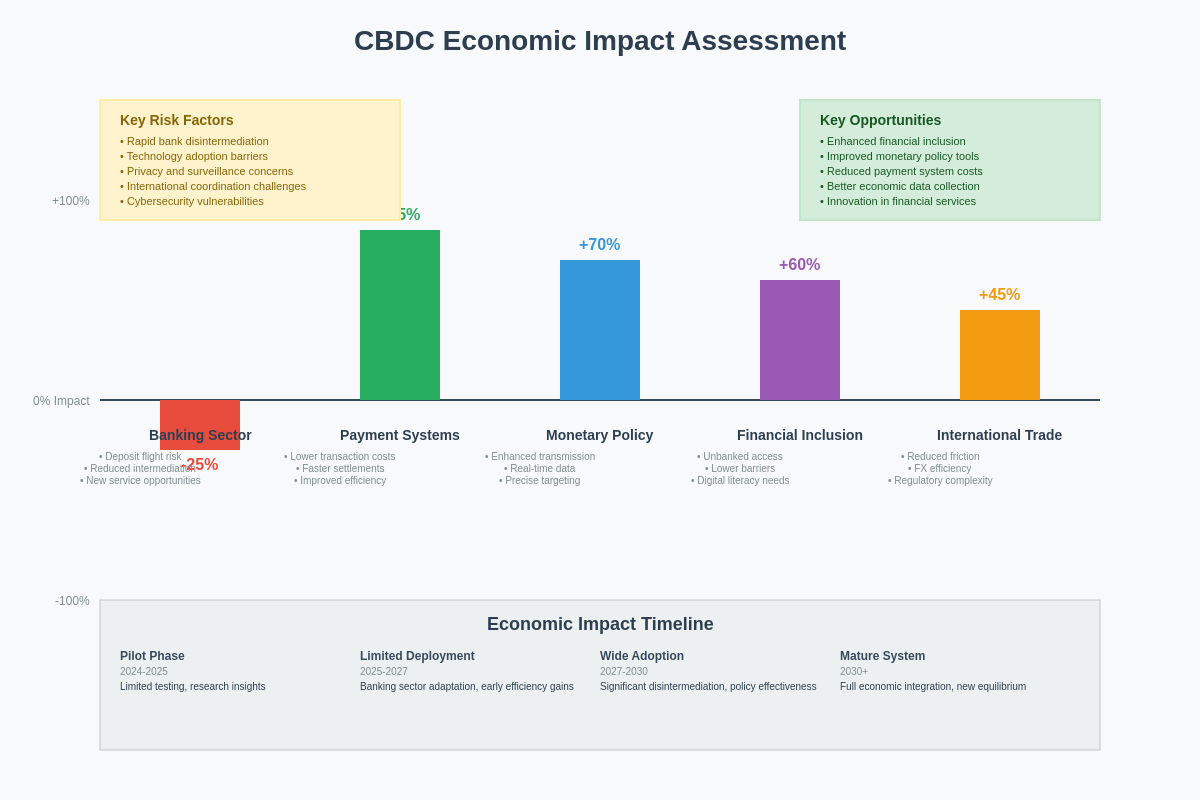

The introduction of Central Bank Digital Currencies poses fundamental challenges to the traditional business model of commercial banks, potentially reducing their role as financial intermediaries and affecting their primary sources of revenue including deposit gathering, payment processing, and lending operations. The extent of this disruption depends heavily on CBDC design choices, particularly regarding interest rates, holding limits, and the degree to which CBDCs compete directly with commercial bank deposits.

Deposit disintermediation represents the most immediate threat to commercial banks from CBDC introduction, as customers may prefer to hold risk-free central bank digital currency rather than deposits in commercial banks that are subject to credit risk and may offer lower interest rates. This migration of deposits to CBDCs could reduce banks’ funding base and force them to rely more heavily on wholesale funding markets, potentially increasing their funding costs and reducing profitability.

Payment processing revenues face significant pressure from CBDC systems that enable direct peer-to-peer transfers without requiring commercial bank intermediation, potentially eliminating lucrative interchange fees and payment processing charges that have become increasingly important revenue sources for banks. The efficiency of CBDC payment systems could force banks to compete on value-added services rather than basic payment processing capabilities.

Lending operations may be affected indirectly through reduced deposit funding and directly through central bank ability to provide credit through CBDC systems, though most central banks have indicated reluctance to compete directly with commercial banks in lending markets. However, the data transparency of CBDC systems could enable alternative credit assessment methods and facilitate direct lending relationships between savers and borrowers that bypass traditional bank intermediation.

Track banking sector performance amid CBDC developments using comprehensive financial analysis tools.

Regulatory compliance and customer service requirements may become more significant competitive advantages for commercial banks in a CBDC environment, as central banks are unlikely to want to provide comprehensive retail banking services directly to consumers. Banks that can demonstrate superior compliance capabilities, customer service, and value-added financial services may maintain their intermediation role even as basic payment and deposit functions migrate to CBDC systems.

The concentration of the banking industry may accelerate as smaller banks struggle to compete with CBDC systems for basic services while lacking the scale necessary to invest in advanced technology and value-added services that can differentiate them from central bank offerings. This concentration could have implications for financial stability and competition in banking markets.

Privacy Concerns and Surveillance Implications

The implementation of Central Bank Digital Currencies raises profound questions about financial privacy, government surveillance capabilities, and the balance between law enforcement needs and individual privacy rights. Unlike physical cash transactions that leave no digital trace, CBDC transactions are inherently recorded and potentially subject to comprehensive monitoring by central bank and government authorities.

Transaction-level visibility enables unprecedented government insight into individual spending patterns, financial relationships, and economic behavior, creating possibilities for surveillance that extend far beyond current banking monitoring capabilities. The granular, real-time nature of CBDC transaction data could enable governments to track individual purchases, identify political affiliations through spending patterns, and monitor personal relationships through payment flows.

Privacy-preserving technologies offer potential solutions to surveillance concerns, with various cryptographic approaches enabling selective disclosure of transaction information based on regulatory requirements and user preferences. Zero-knowledge proofs can enable verification of transaction legitimacy without revealing specific transaction details, while homomorphic encryption allows statistical analysis of transaction patterns without exposing individual transactions.

The design of privacy protections in CBDC systems reflects broader societal values and legal frameworks, with different jurisdictions likely to adopt different approaches based on their constitutional protections, cultural attitudes toward privacy, and law enforcement priorities. European implementations may emphasize privacy protections more strongly than authoritarian regimes that view transaction monitoring as a tool for social control.

Tiered privacy models represent a common approach that provides greater anonymity for small transactions while requiring identity disclosure for larger amounts, similar to current cash transaction reporting requirements. These models attempt to balance privacy concerns with anti-money laundering and tax compliance objectives, though the appropriate threshold levels remain subjects of ongoing debate.

The international implications of privacy design choices become significant when CBDCs are used for cross-border transactions, as different privacy standards between jurisdictions could create compliance challenges and affect the ability of CBDCs to facilitate international trade and remittances. Harmonization of privacy standards may be necessary to realize the full benefits of CBDC interoperability.

Cross-Border Payments and International Trade

Central Bank Digital Currencies offer significant potential to improve the efficiency, cost, and speed of cross-border payments, which currently suffer from high fees, slow settlement times, and complex correspondent banking relationships that create friction in international trade and remittances. CBDC systems designed for international interoperability could eliminate many of these inefficiencies while providing greater transparency and regulatory oversight of cross-border flows.

Direct central bank settlement mechanisms enabled by CBDC systems could bypass traditional correspondent banking networks, reducing the number of intermediaries involved in cross-border payments and enabling near-instantaneous settlement at significantly lower costs. This direct settlement capability could be particularly beneficial for smaller economies that currently face high costs and limited access to international payment systems.

Currency exchange and settlement efficiency improvements through CBDC systems could facilitate international trade by reducing transaction costs and settlement risks associated with foreign exchange transactions. Programmable currency features could enable automatic conversion at predetermined rates, hedging of currency risk, and conditional payments that execute only when specific trade conditions are met.

The development of international CBDC interoperability standards represents a critical challenge that requires coordination among central banks, standard-setting organizations, and technology providers. Different technical architectures, legal frameworks, and regulatory requirements must be harmonized to enable seamless cross-border CBDC transactions while preserving national monetary sovereignty.

Monitor international currency markets and track CBDC developments affecting global trade flows with professional analysis tools.

Geopolitical implications of CBDC adoption in international payments include the potential for major economies to reduce reliance on dominant international currencies like the US dollar, particularly in bilateral trading relationships where both countries have developed CBDC systems. This could gradually alter the structure of international monetary system and affect the global influence of reserve currency issuers.

The role of international organizations like the International Monetary Fund and Bank for International Settlements becomes crucial in coordinating CBDC development standards, ensuring financial stability, and preventing the fragmentation of international payment systems along geopolitical lines. Technical standards, legal frameworks, and operational procedures must be coordinated to maintain the benefits of integrated global financial markets.

Regulatory Frameworks and Legal Considerations

The regulatory landscape surrounding Central Bank Digital Currencies requires the development of entirely new legal frameworks that address the unique characteristics of programmable digital money while ensuring compatibility with existing financial regulations and constitutional protections. Legal questions regarding the status of CBDCs as legal tender, their relationship to existing currency laws, and the scope of central bank authority in digital currency operations remain largely unresolved in most jurisdictions.

Constitutional and legal tender issues arise from the fundamental differences between physical currency and programmable digital money, particularly regarding government authority to monitor transactions, implement spending restrictions, and potentially confiscate or freeze digital currency holdings. The programmable nature of CBDCs enables enforcement capabilities that exceed those available with physical currency, raising questions about the limits of government power and individual financial autonomy.

Anti-money laundering and financial crime prevention frameworks must be adapted to address the unique characteristics of CBDC systems, including their potential for enhanced transaction monitoring while maintaining appropriate privacy protections. The ability to program compliance requirements directly into digital currency could automate many regulatory processes while creating new challenges for balancing compliance with user privacy and system efficiency.

International regulatory coordination becomes essential as CBDCs are deployed across multiple jurisdictions, particularly for cross-border transactions that involve multiple regulatory frameworks simultaneously. Conflicts between different legal systems, privacy requirements, and compliance standards could create significant operational challenges for international CBDC systems.

Data protection and privacy regulations like the European Union’s General Data Protection Regulation create additional complexity for CBDC systems that inherently collect and process large amounts of personal financial data. The right to be forgotten, data minimization principles, and consent requirements may conflict with the permanent, transparent nature of blockchain-based CBDC systems.

The relationship between CBDC regulations and existing financial services laws requires careful coordination to prevent regulatory gaps or conflicts that could create systemic risks or competitive distortions. Banking regulations, payment system oversight, and consumer protection laws may need significant modification to address the unique characteristics of central bank digital currencies.

Economic Implications and Market Effects

The introduction of Central Bank Digital Currencies creates far-reaching economic implications that extend beyond immediate effects on payment systems and banking to influence inflation dynamics, financial stability, international trade, and the structure of global financial markets. The economic impact of CBDCs depends heavily on design choices, adoption rates, and the degree to which they substitute for or complement existing financial instruments.

Inflation measurement and monetary policy effectiveness may be enhanced through real-time transaction data provided by CBDC systems, enabling central banks to observe price changes, spending patterns, and economic activity with unprecedented granularity and timeliness. This enhanced economic visibility could improve the accuracy of inflation targeting and enable more responsive monetary policy adjustments, though it also raises questions about the appropriate use of individual transaction data for macroeconomic policy purposes.

Financial stability implications include both risks and benefits, with CBDC systems potentially reducing risks associated with private payment systems and bank runs while creating new risks related to rapid fund movements, technological failures, and cyber attacks on critical infrastructure. The ability of users to instantly convert bank deposits to risk-free CBDCs could accelerate bank runs during financial stress, requiring new stabilization mechanisms and potentially higher levels of deposit insurance.

Market structure changes resulting from CBDC adoption could affect competition in financial services, with traditional intermediaries facing pressure from direct central bank services while new technology providers and fintech companies gain opportunities to provide value-added services on top of CBDC infrastructure. These structural changes could alter the distribution of economic rents in the financial system and affect innovation incentives.

The velocity of money may be affected by CBDC characteristics including interest rates, programmable features, and user interface design, with implications for the relationship between money supply and economic activity that could require adjustments to traditional monetary policy models. Enhanced transaction efficiency could increase money velocity, while holding incentives and programmable restrictions could have opposite effects.

International trade and capital flow effects from CBDC adoption could alter exchange rate dynamics, reduce transaction costs in international commerce, and affect the international monetary system’s structure. Countries with advanced CBDC systems may gain competitive advantages in international trade, while the potential for reduced reliance on dominant international currencies could gradually affect global monetary arrangements.

Technological Challenges and Innovation Opportunities

The development and deployment of Central Bank Digital Currency systems present numerous technological challenges that require innovative solutions while creating opportunities for advancement in distributed systems, cryptography, user interface design, and financial technology integration. The scale requirements for national CBDC systems far exceed those of existing blockchain implementations, requiring novel approaches to transaction throughput, energy efficiency, and system resilience.

Scalability represents perhaps the most significant technical challenge for CBDC systems, as national payment systems must process millions of transactions per second during peak periods while maintaining low latency and high availability. Traditional blockchain systems like Bitcoin and Ethereum cannot support this transaction volume, requiring the development of new consensus mechanisms, network architectures, and data management approaches specifically designed for central bank requirements.

Interoperability with existing payment systems, banking infrastructure, and international CBDC implementations requires sophisticated technical integration that preserves the benefits of legacy systems while enabling new capabilities. Application programming interfaces, messaging standards, and data formats must be designed to enable seamless integration without compromising security or performance.

Cybersecurity challenges for CBDC systems include protection against sophisticated nation-state attacks, criminal organizations, and insider threats that could compromise system integrity or steal user funds. The critical infrastructure nature of CBDC systems requires security measures that exceed those typically employed in commercial systems, including advanced threat detection, incident response capabilities, and recovery mechanisms.

Explore blockchain technology developments and track innovation in digital currency infrastructure with comprehensive market analysis.

User experience design becomes crucial for CBDC adoption, as systems must be accessible to users with varying levels of technological sophistication while providing intuitive interfaces for complex functionality like programmable payments, privacy controls, and integration with existing financial applications. The user experience must be superior to existing payment methods to drive adoption while accommodating diverse user needs and preferences.

Offline transaction capabilities represent a unique technical challenge for CBDC systems, as users may need to conduct transactions without internet connectivity while maintaining security and preventing double-spending. Various approaches including cryptographic tokens, secure hardware elements, and delayed settlement mechanisms are being explored to enable offline CBDC transactions.

Future Outlook and Implementation Timeline

The future development of Central Bank Digital Currencies will likely proceed along multiple parallel tracks, with different countries adopting varying approaches based on their economic conditions, regulatory environments, and technological capabilities, creating a diverse landscape of CBDC implementations that may eventually converge around common standards and interoperability protocols.

Timeline projections for major CBDC implementations suggest that several significant economies will deploy retail CBDCs within the next five years, with wholesale CBDC systems for interbank payments likely to be implemented sooner due to their more limited scope and fewer technical challenges. The People’s Bank of China’s digital yuan will likely achieve full nationwide deployment by 2025, while European and North American implementations may follow by 2027-2030.

Technology evolution will continue to address current limitations in scalability, privacy, and energy efficiency, with advances in consensus mechanisms, cryptographic protocols, and distributed systems architecture enabling more efficient and capable CBDC systems. Quantum-resistant cryptography will become increasingly important as quantum computing capabilities advance and threaten current cryptographic assumptions.

International coordination efforts through organizations like the Bank for International Settlements will likely produce common technical standards, legal frameworks, and operational procedures that enable interoperability between different CBDC systems while preserving national sovereignty over monetary policy. These standards will be crucial for realizing the full benefits of CBDC systems in international trade and cross-border payments.

The competitive landscape between CBDCs and private digital currencies will likely evolve toward coexistence rather than replacement, with CBDCs providing stability and regulatory compliance while private cryptocurrencies continue to serve specialized use cases like decentralized finance, cross-border remittances in regions with limited CBDC availability, and store of value applications where central bank monetary policy is viewed as inadequate.

Economic and social adaptation to CBDC systems will require significant changes in financial behavior, business models, and regulatory approaches, with the full implications of programmable money likely to emerge only after widespread adoption and experimentation with various features and use cases. The transformation of monetary systems through CBDC adoption represents one of the most significant economic innovations since the development of central banking itself.

The integration of artificial intelligence and machine learning capabilities into CBDC systems will enable more sophisticated fraud detection, personalized financial services, and automated policy implementation, though these capabilities must be balanced against privacy concerns and the risk of algorithmic bias in financial services. The combination of programmable money with artificial intelligence could create unprecedented capabilities for economic management and individual financial optimization.

Stay updated on CBDC developments and their impact on global financial markets through advanced technical analysis and market monitoring tools.

Conclusion

Central Bank Digital Currencies represent a fundamental transformation in the nature of money and banking that will reshape monetary policy, financial intermediation, and economic relationships in ways that are only beginning to be understood. The successful implementation of CBDC systems requires careful balance between innovation and stability, privacy and transparency, efficiency and security, and national sovereignty and international cooperation.

The implications of CBDCs extend far beyond technical considerations to encompass questions of economic policy, individual rights, international relations, and the appropriate role of government in financial systems. As these systems move from experimental pilots to full deployment, their impact on traditional banking, monetary policy effectiveness, and financial inclusion will become increasingly apparent.

The future of banking and monetary systems will likely be characterized by the coexistence of traditional and digital currencies, with CBDCs providing the backbone for efficient, transparent, and policy-responsive payment systems while maintaining the stability and democratic accountability that citizens expect from their monetary institutions. The successful navigation of this transition will require unprecedented cooperation between central banks, commercial financial institutions, technology providers, and regulatory authorities to ensure that the benefits of digital currency innovation are realized while managing the associated risks and challenges.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Central Bank Digital Currency developments involve significant risks and uncertainties. The regulatory landscape for CBDCs is evolving rapidly, and implementations may differ significantly from current proposals. Readers should conduct their own research and consult with qualified financial advisors before making any investment or financial decisions related to digital currencies or affected financial institutions. The analysis presented here is based on publicly available information and current market conditions, which may change substantially as CBDC projects develop.