The Digital Currency Revolution Unfolds

The financial world stands at a crossroads as central banks worldwide accelerate their development of Central Bank Digital Currencies, fundamentally challenging the existing cryptocurrency ecosystem. These government-issued digital currencies represent more than technological innovation; they embody a paradigm shift that could reshape the entire concept of money, payment systems, and financial sovereignty. As CBDCs move from experimental concepts to operational realities, the cryptocurrency community faces an existential question about the future relevance of decentralized digital assets in a world where governments control their own digital money.

The emergence of CBDCs represents the institutionalization of digital currency concepts that were pioneered by Bitcoin and subsequent cryptocurrencies. However, unlike their decentralized predecessors, CBDCs offer central banks unprecedented control over monetary policy implementation, transaction monitoring, and economic data collection. This fundamental difference in design philosophy has sparked intense debate about whether CBDCs will complement, compete with, or ultimately replace traditional cryptocurrencies in the global financial system.

Understanding Central Bank Digital Currencies

Central Bank Digital Currencies represent the digital equivalent of a nation’s fiat currency, issued and backed by the central bank with the same legal tender status as physical cash. Unlike cryptocurrencies such as Bitcoin or Ethereum, CBDCs operate within existing regulatory frameworks and maintain direct government oversight. These digital currencies can take various forms, from wholesale CBDCs designed for institutional settlement to retail CBDCs intended for consumer transactions, each serving different aspects of the monetary system.

The technological infrastructure underlying CBDCs varies significantly across implementations, with some utilizing blockchain technology while others employ centralized databases or hybrid approaches. China’s Digital Currency Electronic Payment system operates on a centralized architecture that enables real-time transaction monitoring and policy implementation, while other nations explore blockchain-based solutions that maintain some degree of distributed verification while preserving central authority. These design choices reflect fundamental trade-offs between efficiency, privacy, and control that define each CBDC’s relationship with existing cryptocurrencies.

The motivations driving CBDC development extend beyond technological modernization to encompass monetary sovereignty, financial inclusion, and economic surveillance capabilities. Central banks view CBDCs as tools for maintaining relevance in an increasingly digital economy while addressing challenges posed by declining cash usage, private cryptocurrency adoption, and potential future competition from foreign digital currencies. Advanced central bank digital currency research and policy analysis helps investors understand the macroeconomic implications of these developments.

The Current CBDC Landscape

Over ninety percent of central banks worldwide are currently researching, piloting, or implementing some form of digital currency, representing the most significant monetary innovation since the abandonment of the gold standard. China leads this transformation with its Digital Currency Electronic Payment system, which has processed billions of dollars in transactions across pilot programs involving millions of users. The People’s Bank of China’s approach demonstrates how CBDCs can integrate with existing payment systems while providing unprecedented transaction visibility and policy control capabilities.

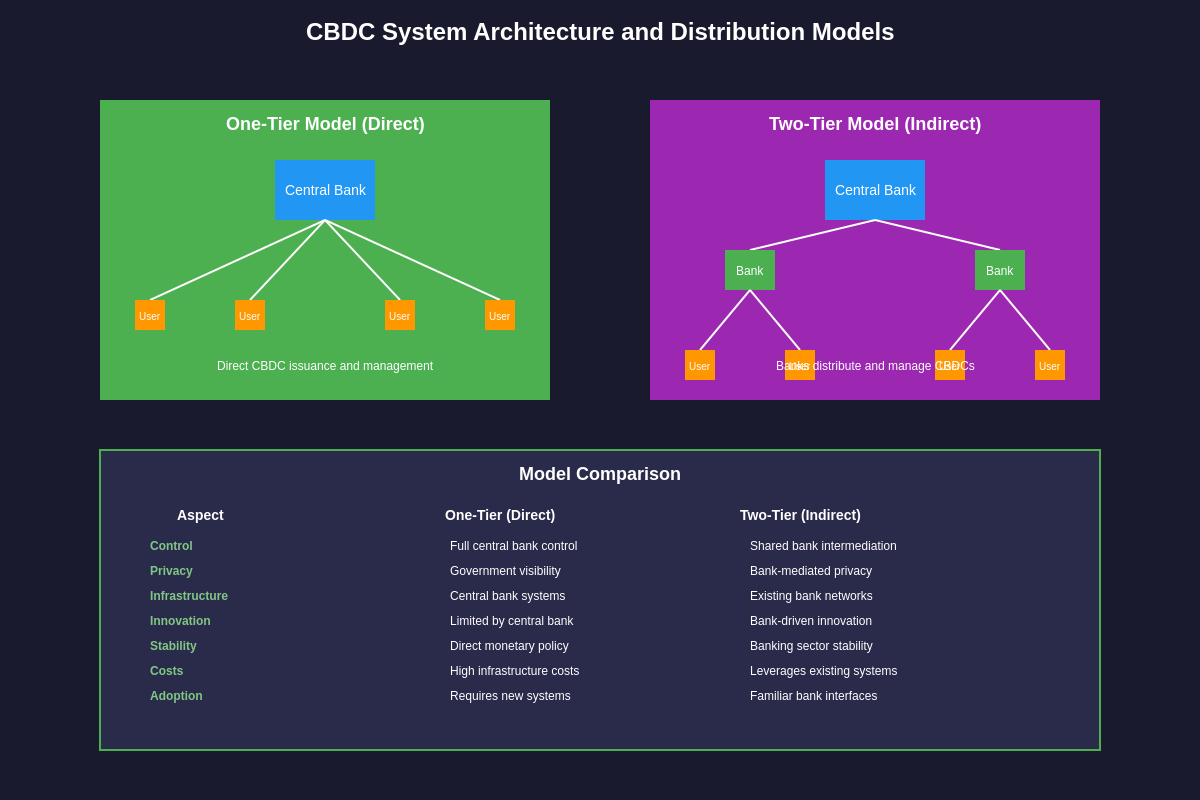

European Central Bank preparations for a digital euro reflect sophisticated considerations about privacy, cross-border payments, and monetary union dynamics. The proposed digital euro would operate alongside physical cash and commercial bank deposits, utilizing a two-tier distribution system that preserves banking sector roles while introducing programmable money capabilities. These design decisions illustrate how CBDCs can maintain existing financial intermediation structures while fundamentally altering the nature of money itself.

The Federal Reserve’s exploration of a digital dollar involves extensive consultation with financial institutions, technology providers, and policy experts to understand implications for monetary policy transmission, financial stability, and privacy protection. Unlike more centralized approaches, the Fed’s research emphasizes maintaining the private sector’s role in customer relationships and payment innovations while providing secure, efficient central bank money for digital transactions. Market participants tracking Federal Reserve policy developments and interest rate decisions recognize how CBDC implementation could significantly impact traditional monetary policy mechanisms.

Smaller nations and emerging economies view CBDCs as opportunities to leapfrog traditional banking infrastructure while reducing dependence on foreign payment systems and currencies. The Eastern Caribbean Central Bank’s DCash implementation demonstrates how digital currencies can enhance financial inclusion in regions with limited banking access while providing central banks with improved monetary policy tools. These early implementations provide valuable insights into operational challenges and user adoption patterns that will influence global CBDC development.

CBDCs vs Traditional Cryptocurrencies: Fundamental Differences

The philosophical divide between CBDCs and traditional cryptocurrencies extends far beyond technical implementation to encompass fundamentally different visions of monetary systems and financial sovereignty. Bitcoin and similar cryptocurrencies emerged from libertarian ideals emphasizing decentralization, censorship resistance, and limited monetary supply, directly challenging central bank authority over money creation and distribution. CBDCs represent the antithesis of these principles, offering central banks enhanced control mechanisms and surveillance capabilities that cryptocurrency advocates specifically sought to eliminate.

Decentralization versus centralization represents the most significant distinction between these digital currency approaches. Traditional cryptocurrencies derive security and legitimacy from distributed consensus mechanisms that prevent any single entity from controlling the network, while CBDCs rely on central authority and government backing for their value and operational integrity. This fundamental difference affects everything from transaction validation and monetary policy implementation to privacy protection and financial censorship resistance.

The monetary policy implications of CBDCs versus cryptocurrencies reveal starkly different approaches to economic management and individual financial autonomy. Central banks can program CBDCs with expiration dates, spending restrictions, or automatic tax collection, capabilities that traditional cryptocurrencies explicitly reject through their decentralized architecture. Bitcoin’s fixed supply schedule contrasts sharply with CBDCs’ unlimited issuance potential, reflecting different theories about optimal monetary systems and inflation control.

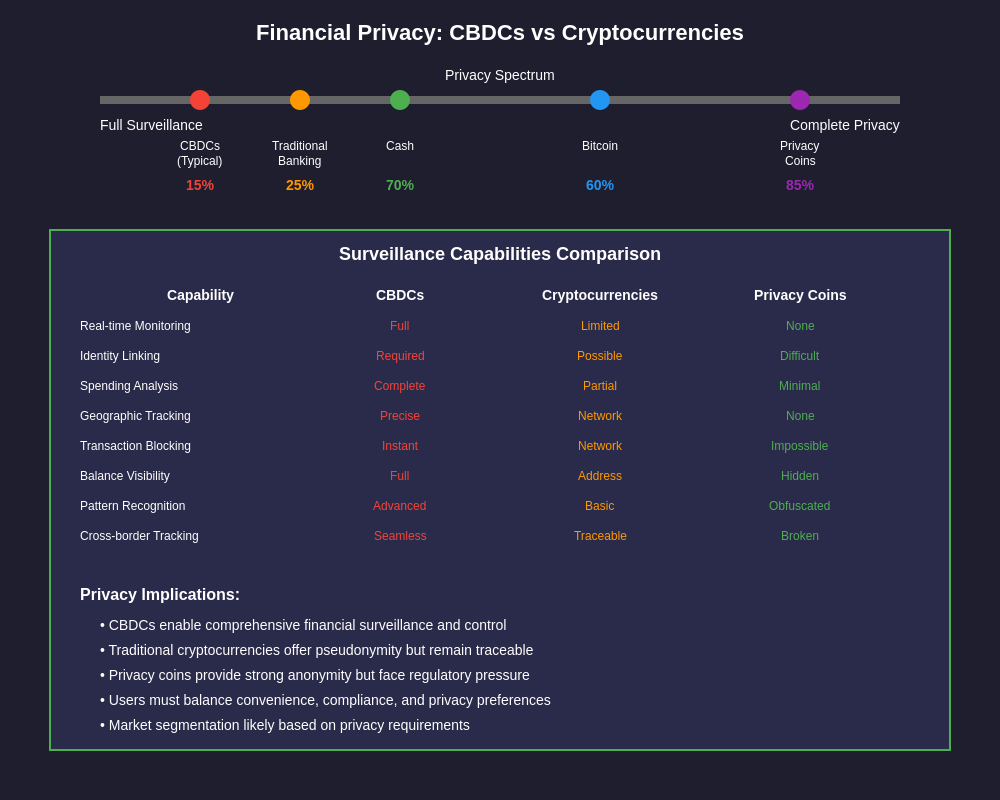

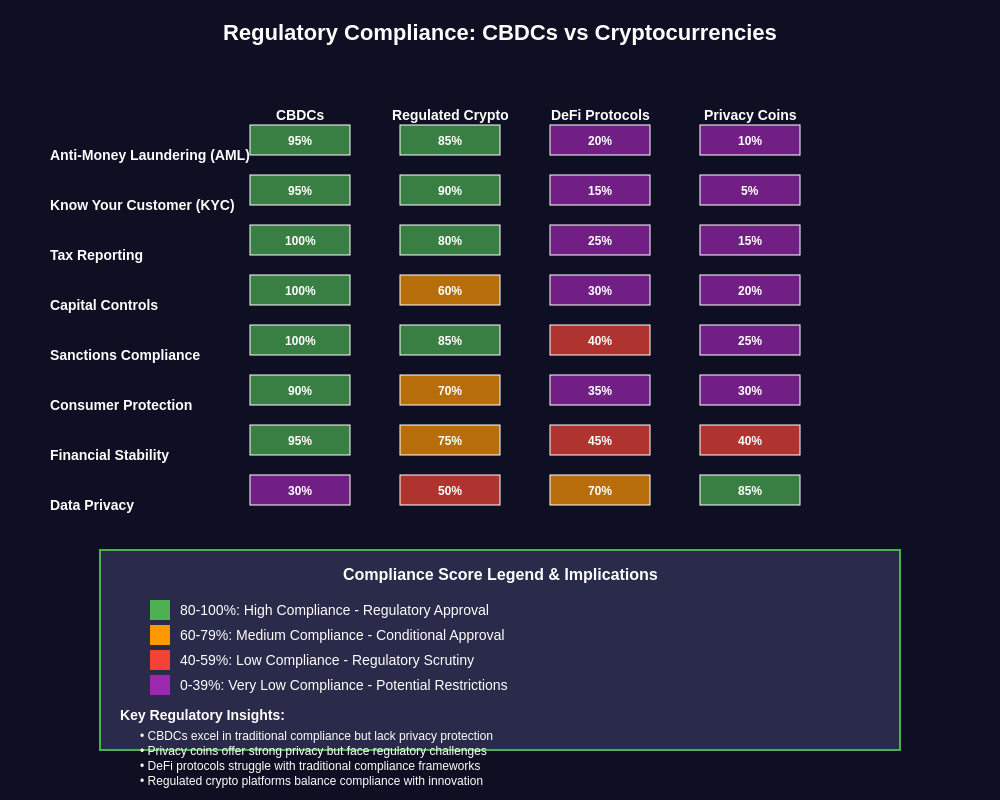

Privacy considerations highlight another crucial distinction between these digital currency paradigms. While cryptocurrencies like Bitcoin provide pseudonymous transactions that can be analyzed but not easily linked to individual identities, CBDCs typically enable comprehensive transaction monitoring and user identification. This surveillance capability allows central banks to combat money laundering and tax evasion while raising concerns about financial privacy and government overreach that motivated cryptocurrency development.

Traders analyzing cryptocurrency market dynamics and institutional adoption trends must consider how CBDC implementation affects the fundamental value propositions that drive crypto asset valuations and market sentiment.

Economic and Monetary Policy Implications

CBDC implementation fundamentally alters monetary policy transmission mechanisms by providing central banks with direct channels to influence consumer spending and saving behavior. Traditional monetary policy operates through interest rate adjustments that affect bank lending and deposit rates, creating indirect effects on economic activity. CBDCs enable central banks to implement negative interest rates directly on consumer holdings, distribute stimulus payments instantly, or impose spending deadlines that encourage immediate consumption rather than saving.

The disintermediation of commercial banks represents a significant structural change as CBDCs allow consumers to hold central bank liabilities directly, potentially reducing demand for bank deposits and traditional financial intermediation services. This shift could affect bank profitability, lending capacity, and the overall structure of financial systems, particularly during economic stress when consumers might prefer the safety of central bank digital currency over commercial bank deposits. Central banks are designing CBDCs with holding limits and interest rate structures to mitigate these disruptive effects while preserving existing banking relationships.

International monetary competition intensifies as CBDCs enable direct cross-border transactions without correspondent banking relationships or foreign exchange market intermediation. A widely adopted digital yuan could challenge dollar dominance in international trade by offering efficient, government-backed settlement mechanisms that bypass traditional Swift network dependencies. This prospect motivates other major economies to accelerate their own CBDC development to maintain monetary sovereignty and international influence.

The impact on cryptocurrency valuations depends partly on whether CBDCs satisfy the same user needs that drive crypto adoption or whether they address different market segments entirely. CBDCs provide stability, regulatory clarity, and government backing that cryptocurrencies cannot offer, potentially reducing demand for crypto assets among users primarily seeking efficient digital payments. However, CBDCs’ surveillance capabilities and centralized control may reinforce the value proposition of privacy-focused cryptocurrencies and decentralized alternatives for users prioritizing financial autonomy.

Financial Surveillance and Privacy Concerns

Central Bank Digital Currencies enable unprecedented transaction monitoring capabilities that transform the relationship between governments and individual financial privacy. Unlike cash transactions that leave no digital trail, CBDC payments create comprehensive records of spending patterns, transaction counterparties, and economic behavior that central banks can analyze in real-time. This surveillance potential allows governments to detect tax evasion, monitor compliance with sanctions, and track economic activity with precision impossible under current payment systems.

The programmable nature of CBDCs extends surveillance capabilities beyond transaction monitoring to include behavioral modification through conditional spending restrictions and automated policy enforcement. Governments could program CBDCs to prevent purchases of specific goods, limit transaction amounts, or require additional verification for certain types of payments. These capabilities, while potentially useful for combating illegal activities, raise fundamental questions about financial freedom and the appropriate scope of government control over individual economic choices.

Privacy protection mechanisms in CBDC design vary significantly across implementations, reflecting different cultural attitudes toward government surveillance and individual privacy rights. Some CBDCs incorporate privacy features similar to cash for small transactions while maintaining monitoring capabilities for larger amounts, attempting to balance law enforcement needs with individual privacy expectations. However, the technical architecture required for comprehensive privacy protection often conflicts with the regulatory compliance and policy implementation features that motivate CBDC development.

The contrast between CBDC surveillance capabilities and cryptocurrency privacy features may drive increased demand for privacy-focused crypto assets among users prioritizing financial anonymity. Monero, Zcash, and similar privacy coins offer transaction obfuscation features that directly counter the transparency requirements built into most CBDC implementations. This dynamic could create a bifurcated digital currency ecosystem where CBDCs serve mainstream payment needs while privacy cryptocurrencies serve users seeking financial anonymity.

Cross-Border Payments and International Competition

CBDCs promise to revolutionize international payments by enabling direct government-to-government settlement mechanisms that bypass traditional correspondent banking networks and foreign exchange intermediaries. Current cross-border payments involve multiple intermediaries, currency conversions, and settlement delays that increase costs and reduce efficiency, particularly for smaller transactions and developing country participants. CBDCs could enable instant, low-cost international transfers between participating central banks, fundamentally altering global payment infrastructure.

The geopolitical implications of CBDC-enabled international payments extend beyond efficiency improvements to encompass questions of monetary sovereignty and economic influence. Countries with widely accepted CBDCs could reduce dependence on dollar-denominated payment systems while extending their own monetary influence through digital currency adoption. China’s digital yuan pilots with international partners demonstrate how CBDCs can facilitate trade settlement and economic integration while reducing reliance on Western-controlled payment networks.

Multi-CBDC platform development represents collaborative efforts to create interoperable international payment systems that maintain individual monetary sovereignty while enabling efficient cross-border transactions. Projects like the Bank for International Settlements’ Project Dunbar explore how multiple CBDCs can interact through shared technical standards and governance frameworks, potentially creating alternatives to current international payment systems dominated by private sector intermediaries.

The competitive dynamics between CBDCs and international cryptocurrencies depend partly on relative adoption rates and network effects. Bitcoin and other cryptocurrencies already provide cross-border payment capabilities without requiring bilateral agreements or central bank cooperation, potentially maintaining advantages in markets where CBDC interoperability remains limited. However, the regulatory clarity and stability offered by CBDCs may prove more attractive for institutional and commercial users requiring predictable settlement and compliance frameworks.

Investors monitoring international currency markets and central bank policy coordination need to understand how CBDC development affects traditional foreign exchange dynamics and currency valuation mechanisms.

Impact on Cryptocurrency Markets and Adoption

The introduction of CBDCs creates complex competitive dynamics that could either validate cryptocurrency concepts by demonstrating digital currency utility or undermine crypto markets by providing government-backed alternatives to decentralized assets. CBDCs may increase overall digital currency acceptance among conservative users who previously avoided cryptocurrencies due to volatility or regulatory uncertainty, potentially expanding the total addressable market for all digital assets. Alternatively, CBDCs might satisfy mainstream digital payment needs currently driving cryptocurrency adoption, reducing demand for crypto assets except among users specifically seeking decentralization and censorship resistance.

Institutional cryptocurrency adoption patterns may shift as CBDCs provide regulated alternatives for digital asset exposure and treasury management. Corporations currently holding Bitcoin as a hedge against monetary debasement might prefer CBDCs for operational purposes while maintaining crypto positions for investment diversification. Financial institutions could utilize CBDCs for settlement and regulatory compliance while offering cryptocurrency services to clients seeking alternative investment exposure.

The regulatory environment surrounding cryptocurrencies may become more restrictive as governments promote CBDC adoption and reduce perceived competition from private digital currencies. Some jurisdictions might ban or heavily regulate cryptocurrency usage while promoting their own digital currencies as safe, legal alternatives. This regulatory pressure could drive cryptocurrency trading and usage toward more permissive jurisdictions or privacy-focused platforms that resist government oversight.

Market structure evolution reflects the changing relationship between traditional financial institutions and cryptocurrency platforms as CBDCs bridge these previously distinct sectors. Banks might integrate CBDC functionality while offering cryptocurrency trading services, creating hybrid platforms that serve both government digital currency users and crypto investors. Exchange platforms could expand to include CBDC trading pairs and custody services while maintaining their core cryptocurrency offerings.

Stablecoin Competition and Central Bank Responses

Central Bank Digital Currencies directly compete with stablecoins by offering government-backed stability without relying on private sector reserves or algorithmic mechanisms. Stablecoins like USDT and USDC currently serve as cryptocurrency trading intermediaries and value transfer mechanisms, roles that CBDCs could potentially fulfill with superior regulatory backing and systemic stability. This competition has prompted stablecoin issuers to emphasize international accessibility, programmability, and integration with decentralized finance protocols as differentiating features.

Regulatory pressure on stablecoin operators intensifies as central banks view private stable value digital currencies as potential threats to monetary sovereignty and financial stability. Recent regulatory proposals require stablecoin issuers to obtain banking licenses, maintain full reserves, and submit to central bank oversight, effectively transforming private stablecoins into quasi-public utilities. These requirements may reduce stablecoin innovation and market competition while favoring CBDC adoption for mainstream use cases.

The technical capabilities of CBDCs versus stablecoins reveal different trade-offs between functionality, control, and innovation. Stablecoins often integrate with smart contract platforms and decentralized applications, enabling complex financial instruments and automated transactions that CBDCs may not support due to regulatory constraints or technical limitations. However, CBDCs offer finality, legal tender status, and crisis resilience that private stablecoins cannot guarantee regardless of their technical sophistication.

Innovation in CBDC design increasingly incorporates features pioneered by stablecoins, including programmability, smart contract integration, and multi-platform compatibility. Some CBDCs explore tokenized implementations that enable blockchain-based applications while maintaining central bank control over issuance and redemption. This convergence suggests that the boundaries between CBDCs and advanced stablecoins may blur as both evolve to serve similar market needs with different governance structures.

Decentralized Finance and CBDC Integration

The relationship between Decentralized Finance protocols and Central Bank Digital Currencies presents fascinating tensions between permissionless innovation and regulatory compliance. DeFi platforms built on public blockchains emphasize open access, algorithmic governance, and censorship resistance, values that conflict with CBDC requirements for user identification, transaction monitoring, and policy enforcement. However, the programmable nature of many CBDC designs could enable integration with DeFi protocols under appropriate regulatory frameworks.

CBDC programmability features might support automated compliance, tax collection, and policy implementation within DeFi applications, creating hybrid systems that combine decentralized innovation with centralized oversight. Smart contracts could automatically enforce spending restrictions, collect taxes, or implement monetary policy tools while enabling complex financial instruments and yield farming strategies. This integration would represent a significant departure from current DeFi philosophy while potentially expanding the total value locked in decentralized protocols.

Regulatory frameworks for DeFi integration with CBDCs remain largely undefined, creating uncertainty about which applications and protocols might achieve compliance approval. Traditional DeFi features like flash loans, anonymous liquidity provision, and governance token voting may prove incompatible with CBDC compliance requirements, forcing protocol developers to choose between decentralization principles and mainstream adoption. Some projects are already developing compliance-friendly DeFi platforms designed to integrate with regulated digital currencies.

The competitive dynamics between CBDC-integrated DeFi platforms and traditional crypto-native protocols could fragment the decentralized finance ecosystem along regulatory lines. Compliant platforms might attract institutional users and larger liquidity pools while sacrificing the permissionless innovation that originally drove DeFi growth. Meanwhile, traditional DeFi protocols might maintain their core user base among privacy-conscious users while facing reduced mainstream adoption and regulatory pressure.

Professional traders utilizing decentralized finance protocols and yield farming strategies must evaluate how CBDC integration affects protocol tokenomics and risk-reward profiles across different regulatory environments.

Regional CBDC Developments and Global Implications

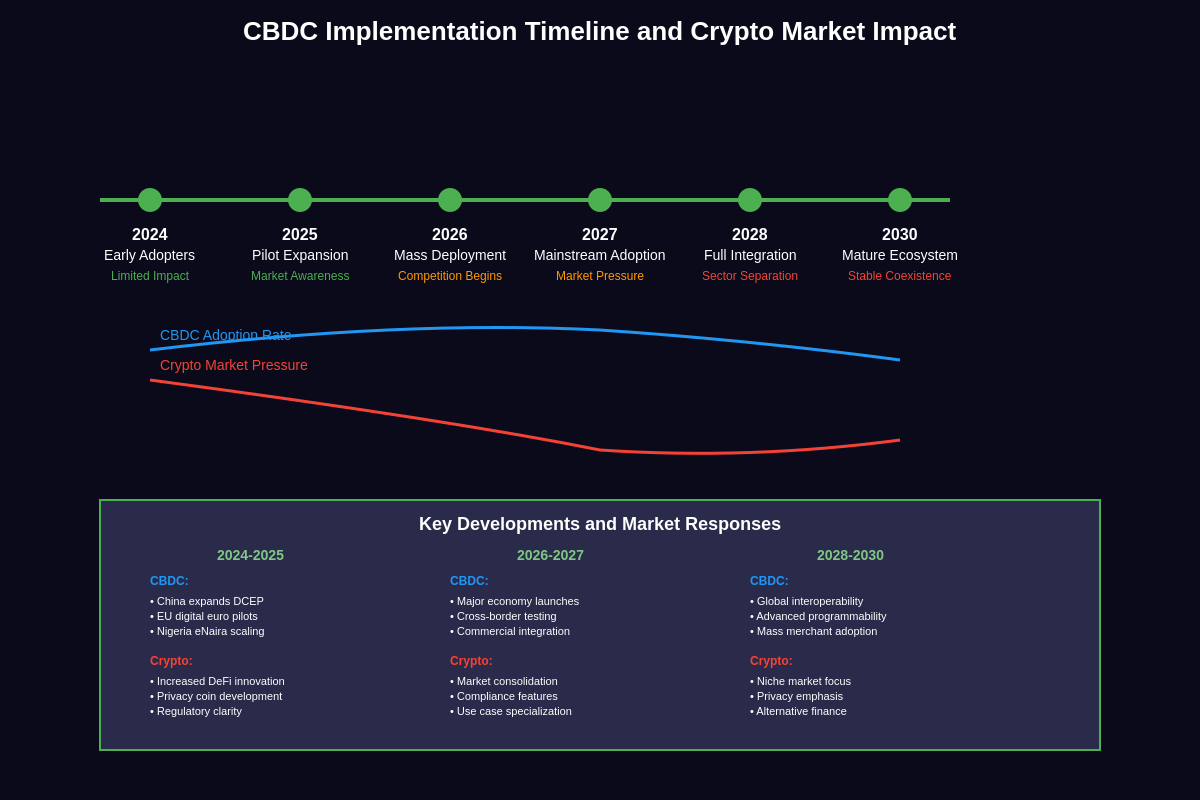

Asia-Pacific nations lead global CBDC implementation with China’s Digital Currency Electronic Payment system processing substantial transaction volumes across multiple pilot cities and use cases. The Chinese approach emphasizes transaction efficiency, policy implementation, and economic data collection while maintaining compatibility with existing payment infrastructure. South Korea, Japan, and Singapore pursue different CBDC strategies that reflect their unique monetary systems, regulatory frameworks, and international relationships, creating a diverse regional landscape of digital currency approaches.

European Union coordination on digital euro development demonstrates how monetary unions can implement CBDCs while preserving member state sovereignty and existing banking relationships. The proposed digital euro design balances privacy protection with anti-money laundering compliance, cross-border efficiency with national monetary authority, and innovation support with financial stability preservation. These complex trade-offs illustrate the challenges facing currency unions in implementing unified digital currency systems.

African nations explore CBDCs as tools for financial inclusion, reducing payment costs, and decreasing dependence on foreign currencies and payment systems. Nigeria’s eNaira launch represents one of the first retail CBDC implementations in a major developing economy, providing insights into user adoption patterns, technical infrastructure requirements, and economic impacts in markets with significant unbanked populations. Ghana, South Africa, and other African countries are pursuing similar initiatives with different technical approaches and policy objectives.

The Americas present diverse CBDC development patterns reflecting different economic conditions, monetary frameworks, and regulatory approaches. The Federal Reserve’s cautious research contrasts with more aggressive implementation timelines in smaller economies seeking to modernize payment infrastructure or reduce dollarization. Canada, Brazil, and other major economies balance innovation objectives with financial stability concerns while considering implications for existing banking sectors and international competitiveness.

Future Scenarios: Coexistence or Dominance

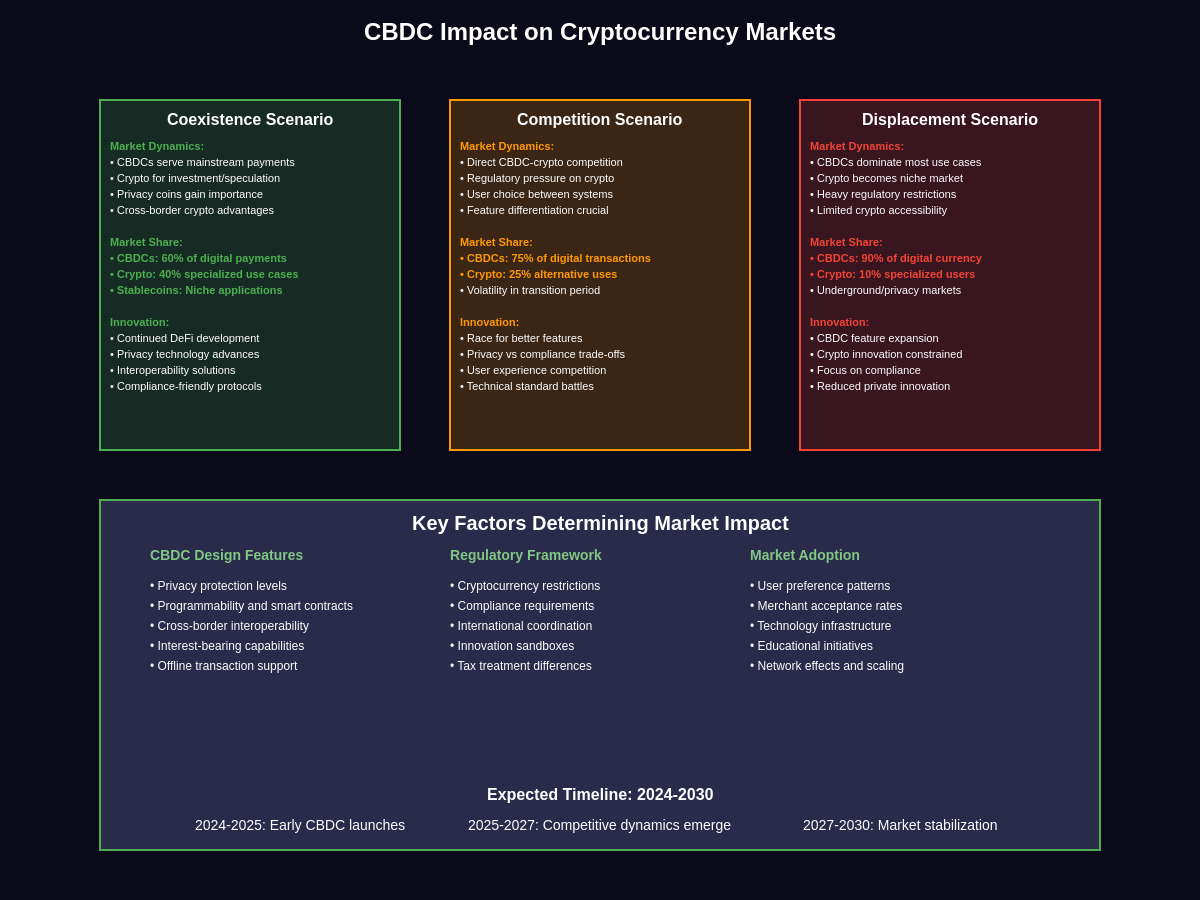

The relationship between CBDCs and traditional cryptocurrencies will likely evolve along multiple possible trajectories depending on regulatory decisions, technological developments, and user preferences. A coexistence scenario might see CBDCs serving mainstream payment needs while cryptocurrencies maintain relevance for international transfers, investment speculation, and privacy-conscious users. This bifurcated market could resemble current distinctions between government-issued currency and alternative stores of value like gold or foreign currencies.

Cryptocurrency dominance in specific use cases could persist despite widespread CBDC adoption if decentralized assets continue providing unique value propositions that government digital currencies cannot replicate. Bitcoin’s fixed supply schedule and censorship resistance may remain attractive to users hedging against monetary debasement or seeking financial sovereignty regardless of CBDC availability. Privacy coins might gain importance as CBDC surveillance capabilities drive demand for anonymous transaction options.

CBDC dominance scenarios could unfold if government digital currencies successfully address most user needs currently driving cryptocurrency adoption while regulatory pressure reduces crypto accessibility and utility. Comprehensive CBDC systems offering programmability, international interoperability, and attractive interest rates might satisfy payment, store of value, and investment functions currently served by multiple cryptocurrency projects. This consolidation could reduce cryptocurrency markets to niche applications serving specialized user communities.

Hybrid evolution paths might see traditional cryptocurrencies adapting to complement rather than compete with CBDCs through enhanced privacy features, specialized use cases, or integration with CBDC-compatible platforms. Some cryptocurrency projects are already exploring compliance-friendly designs that could coexist with government digital currencies while maintaining core decentralization principles. This adaptation strategy acknowledges regulatory realities while preserving cryptocurrency innovation and user choice.

The timeline for these competitive dynamics depends largely on CBDC implementation speed, regulatory frameworks, and user adoption patterns. Rapid CBDC deployment with attractive features and broad merchant acceptance could quickly reduce cryptocurrency market share, while slower implementation or limited functionality might allow crypto markets to evolve and strengthen their competitive positions. Market participants require sophisticated cryptocurrency market analysis and institutional flow tracking to navigate these evolving competitive dynamics and identify emerging opportunities.

Innovation and Technological Evolution

The competitive pressure from CBDCs is accelerating innovation within the cryptocurrency ecosystem as projects seek to differentiate themselves through enhanced privacy, improved scalability, novel use cases, and superior user experiences. Layer-2 scaling solutions, privacy protocols, and interoperability bridges represent technological responses to CBDC challenges while expanding cryptocurrency utility beyond current limitations. This innovation race benefits the entire digital currency ecosystem by advancing the state of the art in cryptographic techniques, consensus mechanisms, and distributed system design.

Central banks are incorporating lessons learned from cryptocurrency innovation into their CBDC designs, adopting blockchain technology, smart contract functionality, and programmable money concepts pioneered by crypto projects. This technology transfer validates cryptocurrency contributions to monetary innovation while creating more sophisticated CBDC implementations that better compete with private digital currencies. The resulting technological convergence may blur distinctions between government and private digital currencies at the technical level while maintaining philosophical and governance differences.

Interoperability development between CBDCs and cryptocurrency platforms could create hybrid ecosystems where users seamlessly transact across government and private digital currencies depending on specific needs and preferences. Cross-chain protocols, atomic swaps, and bridge technologies enable value transfer between different blockchain networks, potentially allowing CBDCs built on compatible infrastructure to interact with cryptocurrency platforms. This technical integration could reduce friction between competing digital currency systems while preserving user choice and innovation incentives.

The evolution of cryptocurrency mining and validation mechanisms responds to environmental concerns and regulatory pressure that also influence CBDC design decisions. Proof-of-stake consensus, carbon-neutral mining initiatives, and energy-efficient blockchain architectures address sustainability criticisms while maintaining decentralization principles. These improvements help cryptocurrencies compete with CBDCs on environmental impact metrics while preserving the distributed trust mechanisms that differentiate crypto assets from centralized digital currencies.

Investment and Market Structure Implications

Portfolio allocation strategies must account for the changing risk-return profiles of cryptocurrency investments as CBDCs alter competitive dynamics and regulatory environments. Traditional cryptocurrency investment theses based on digital payment adoption, store of value properties, and monetary debasement hedging require updating to reflect CBDC alternatives and changing government policies. Sophisticated investors are developing new frameworks for evaluating cryptocurrency projects based on their ability to coexist with or differentiate from government digital currencies.

Institutional cryptocurrency adoption patterns are evolving as CBDCs provide regulated alternatives for digital currency exposure while regulatory clarity improves for compliant crypto assets. Some institutions may prefer CBDC exposure for operational purposes while maintaining cryptocurrency positions for portfolio diversification and alternative asset allocation. Others might concentrate on cryptocurrency projects with clear competitive advantages over CBDCs, such as enhanced privacy, international accessibility, or specialized financial applications.

Market infrastructure development reflects the growing sophistication of cryptocurrency markets and their integration with traditional financial systems. Custody services, derivatives markets, and institutional trading platforms are expanding to serve professional investors while maintaining compliance with evolving regulatory requirements. This infrastructure maturation helps cryptocurrency markets compete with CBDC-based systems for institutional adoption while providing the tools necessary for sophisticated portfolio management and risk hedging.

The emergence of CBDC-cryptocurrency exchange traded products and structured investments creates new vehicles for gaining exposure to digital currency trends while managing regulatory and custody risks. These products allow traditional investors to participate in digital currency markets through familiar investment structures while professional managers handle the technical complexities of cryptocurrency trading and storage. This accessibility could accelerate institutional adoption regardless of CBDC competitive pressure.

Regulatory Evolution and Global Coordination

International regulatory coordination on digital currencies increasingly encompasses both CBDCs and cryptocurrencies as governments seek consistent approaches to digital asset oversight and cross-border financial crime prevention. Organizations like the Financial Stability Board and Bank for International Settlements are developing frameworks that address CBDC interoperability, cryptocurrency market regulation, and systemic risk management in hybrid digital currency ecosystems. This coordination effort aims to prevent regulatory arbitrage while preserving monetary sovereignty and innovation incentives.

The development of international standards for CBDC implementation affects cryptocurrency regulations by establishing technical benchmarks, privacy expectations, and cross-border transaction protocols that private digital currencies may need to meet for continued regulatory acceptance. Some jurisdictions are requiring cryptocurrency platforms to achieve CBDC-compatible compliance standards, effectively using central bank digital currency requirements as regulatory baselines for private sector digital assets.

Anti-money laundering and tax compliance frameworks are evolving to address both CBDC transaction monitoring and cryptocurrency privacy features through coordinated international enforcement and information sharing agreements. The contrast between CBDC transparency and cryptocurrency anonymity creates regulatory tensions that governments are addressing through enhanced compliance requirements, international cooperation, and technological solutions for transaction analysis. These developments affect the relative attractiveness of different digital currency options for legitimate users while creating compliance costs for cryptocurrency platforms.

Central bank coordination on CBDC policies influences global cryptocurrency market conditions through indirect effects on regulatory sentiment, international payment infrastructure, and monetary policy transmission mechanisms. Coordinated CBDC launches or regulatory frameworks could create synchronized market pressures that affect cryptocurrency valuations and adoption patterns across multiple jurisdictions simultaneously. Market participants must monitor these coordination efforts to anticipate regulatory developments and market structure changes.

Conclusion: The Future of Digital Money

The emergence of Central Bank Digital Currencies represents a pivotal moment in monetary history that will fundamentally reshape the digital currency landscape over the coming decade. Rather than simply competing with or replacing traditional cryptocurrencies, CBDCs are likely to catalyze the evolution of a more complex, differentiated digital currency ecosystem where government and private digital assets serve complementary roles for different user needs and preferences. This transformation challenges existing assumptions about money, payments, and financial sovereignty while creating new opportunities for innovation and investment.

The ultimate impact of CBDCs on traditional cryptocurrencies depends on implementation decisions currently being made by central banks, regulatory agencies, and technology developers worldwide. Design choices regarding privacy protection, programmability, international interoperability, and private sector integration will determine whether CBDCs primarily compete with or complement existing cryptocurrency use cases. Early evidence suggests that CBDCs will satisfy some but not all of the needs currently driving cryptocurrency adoption, leaving substantial market opportunities for differentiated crypto assets.

The coexistence of CBDCs and cryptocurrencies seems more likely than the complete dominance of either approach, given the fundamental philosophical differences between centralized government control and decentralized private networks. Users seeking government backing, regulatory clarity, and monetary stability may prefer CBDCs, while those prioritizing privacy, censorship resistance, and alternative monetary policies may continue choosing cryptocurrencies. This market segmentation could support sustainable demand for both types of digital currencies while driving continued innovation in both sectors.

The broader implications of this digital currency revolution extend beyond immediate market impacts to encompass questions about the future of money, financial privacy, and economic sovereignty that will influence policy debates and investment decisions for generations. As CBDCs and cryptocurrencies continue evolving through technological innovation and regulatory adaptation, market participants must remain adaptable and informed about emerging developments that could fundamentally alter competitive dynamics and investment opportunities in the digital currency space.

Sophisticated investors and policy analysts require comprehensive macroeconomic analysis and digital currency market intelligence to navigate this transformation successfully and identify the most promising opportunities in an increasingly complex digital currency ecosystem.

Disclaimer: This article is for educational and informational purposes only and should not be construed as financial advice. Cryptocurrency investments carry significant risks, including the potential for total loss of capital. Central Bank Digital Currency developments and regulatory changes may significantly impact cryptocurrency markets in unpredictable ways. Always conduct your own research and consult with qualified financial advisors before making investment decisions. The author and publisher are not responsible for any financial losses that may occur from acting on the information provided in this article.