Learn more about cross-chain lending on TradingView

The Revolutionary Promise of Cross-Chain Finance

Cross-chain lending represents one of the most significant innovations in decentralized finance, enabling users to leverage assets on one blockchain as collateral for borrowing assets on another blockchain without the need for centralized intermediaries or complex custody arrangements. This emerging financial primitive allows cryptocurrency holders to unlock liquidity from their Bitcoin holdings by using them as collateral to borrow Ethereum or other assets, creating unprecedented opportunities for capital efficiency and portfolio management strategies.

The fundamental challenge that cross-chain lending addresses stems from the isolated nature of blockchain networks, where assets naturally exist within their respective ecosystems and cannot be directly utilized across different chains. Traditional approaches to accessing cross-chain liquidity have required users to trust centralized exchanges or wrapped token systems, both of which introduce counterparty risk and operational complexities that many DeFi participants seek to avoid.

Cross-chain lending protocols utilize sophisticated cryptographic techniques, including atomic swaps, hash time-locked contracts, and bridge technologies, to enable secure collateralization and borrowing across different blockchain networks. These systems maintain the trustless and permissionless principles of decentralized finance while expanding the utility of cryptocurrency holdings beyond their native blockchain ecosystems.

The market opportunity for cross-chain lending continues to expand as the cryptocurrency ecosystem becomes increasingly multi-chain, with different blockchains offering unique advantages for specific use cases. Bitcoin holders, who possess the largest store of value in the cryptocurrency space, can now access the growing DeFi ecosystem on Ethereum and other smart contract platforms without selling their Bitcoin positions or relying on centralized intermediaries.

Historical Context and Evolution of Cross-Chain Protocols

The development of cross-chain lending protocols represents the culmination of years of research and development in blockchain interoperability, building upon earlier innovations in atomic swaps, payment channels, and bridge technologies. Early cross-chain transactions were limited to simple peer-to-peer exchanges using atomic swap protocols, which required both parties to be online simultaneously and provided limited flexibility for complex financial arrangements.

The introduction of wrapped Bitcoin tokens on Ethereum marked an important intermediate step toward cross-chain lending, allowing Bitcoin holders to participate in Ethereum DeFi protocols through centralized custodial systems. However, these solutions required users to trust centralized entities with their Bitcoin holdings, creating counterparty risk that many decentralized finance advocates found unacceptable.

Hash time-locked contracts emerged as a trustless alternative for cross-chain transactions, enabling conditional transfers that could be executed across different blockchain networks without requiring trusted intermediaries. These contracts form the foundation for many modern cross-chain lending protocols, providing cryptographic guarantees that funds can only be accessed when specific conditions are met on both chains.

The development of blockchain bridge technologies has significantly expanded the possibilities for cross-chain lending by enabling more sophisticated communication between different blockchain networks. These bridges can facilitate complex multi-step transactions, oracle price feeds, and automated liquidation mechanisms that are essential for robust lending protocols.

Layer 2 scaling solutions and sidechains have also contributed to the evolution of cross-chain lending by reducing transaction costs and improving the user experience for cross-chain operations. The ability to conduct cross-chain lending transactions with lower fees and faster confirmation times has made these protocols more accessible to a broader range of users.

Recent innovations in zero-knowledge proof systems and threshold cryptography are enabling even more advanced cross-chain lending protocols that can provide enhanced privacy protection and security guarantees. These technologies allow for verification of collateral and loan terms without revealing sensitive information about user positions or trading strategies.

Technical Architecture and Protocol Mechanics

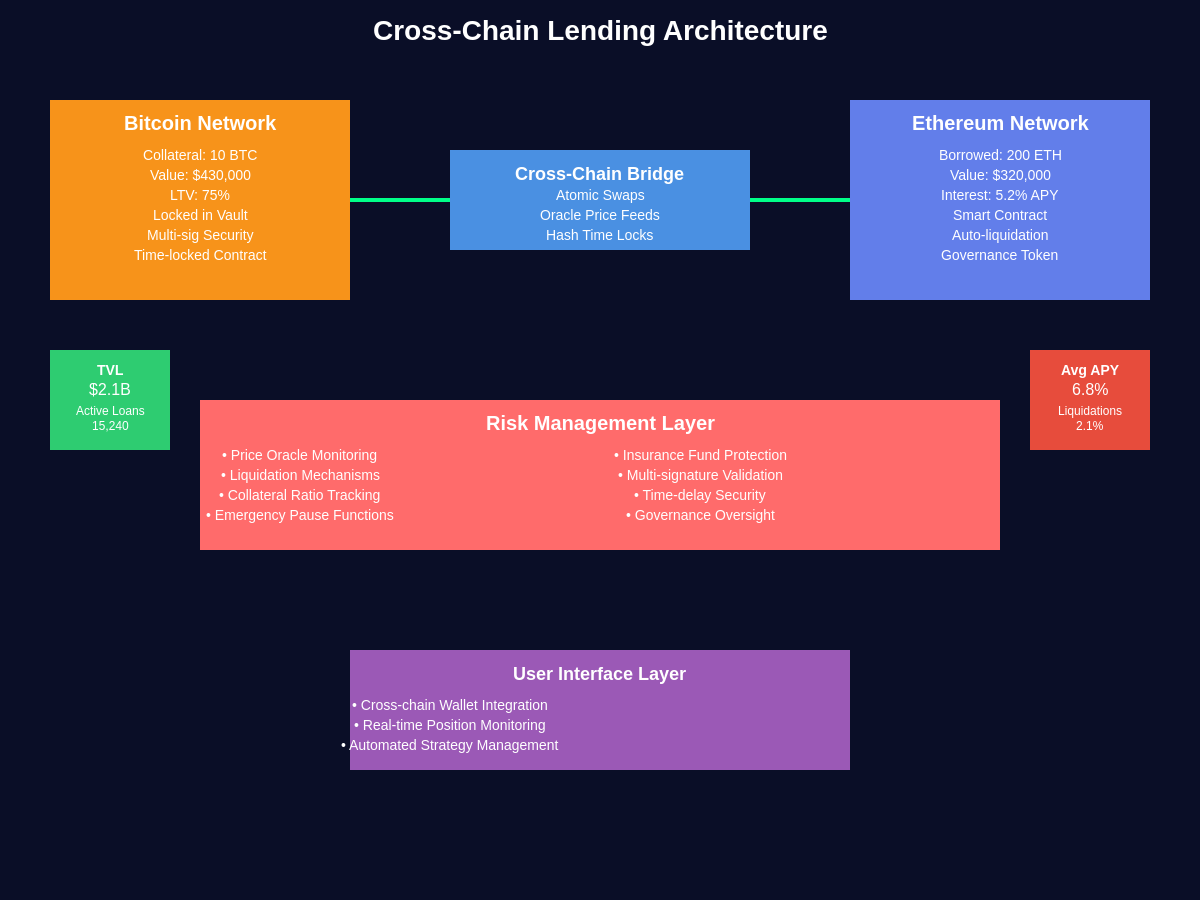

Cross-chain lending protocols employ sophisticated technical architectures that must address the unique challenges of operating across multiple blockchain networks while maintaining security, efficiency, and user experience standards comparable to single-chain DeFi protocols. The core technical challenge involves creating trustless mechanisms for collateral verification, loan origination, interest accrual, and liquidation processes that can operate reliably across different blockchain environments with varying confirmation times, fee structures, and consensus mechanisms.

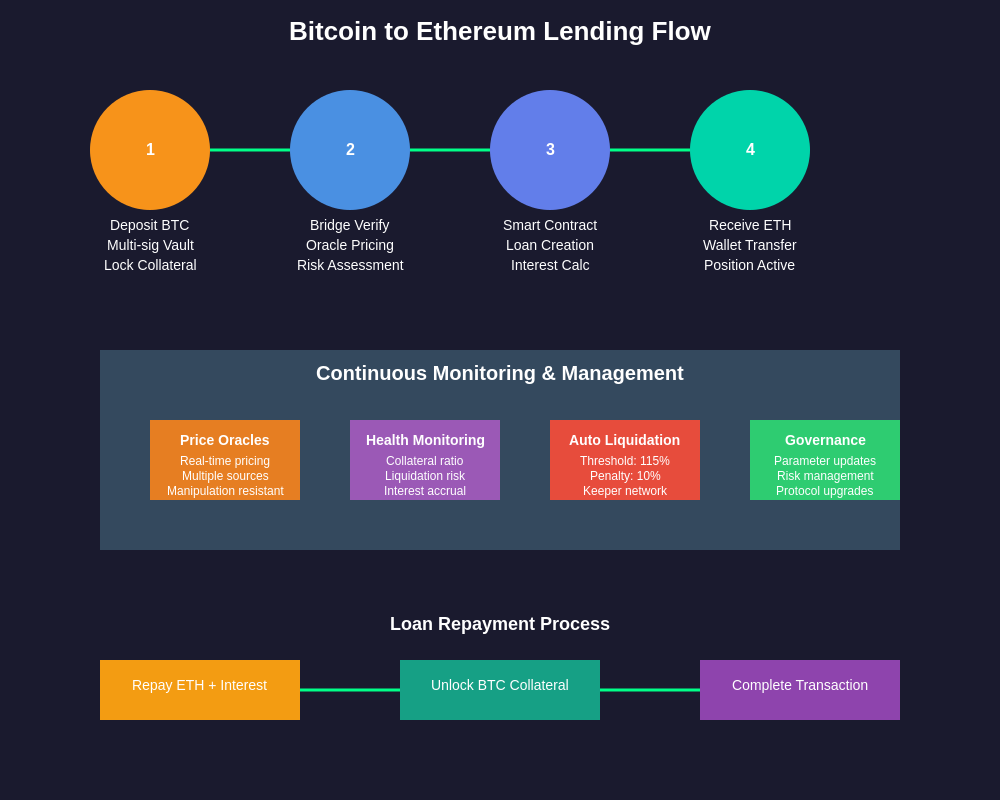

The collateral verification process in cross-chain lending requires robust oracle systems that can accurately track asset prices and collateral values across different blockchain networks in real-time. These oracles must be resistant to manipulation and provide consistent pricing data that can be used for loan-to-value calculations and liquidation triggers. Advanced protocols implement multiple oracle sources and sophisticated aggregation mechanisms to ensure pricing accuracy and reliability.

Smart contract architecture for cross-chain lending typically involves deploying contract systems on multiple blockchain networks that can communicate through bridge protocols or relay networks. These contracts must implement complex state synchronization mechanisms to ensure that collateral locks, loan disbursements, and repayment processes are properly coordinated across different chains while maintaining atomicity and preventing double-spending or other security vulnerabilities.

The liquidation mechanism represents one of the most technically challenging aspects of cross-chain lending protocols, as it must be able to operate efficiently across multiple blockchain networks with different transaction processing speeds and cost structures. Advanced liquidation systems must account for network congestion, gas price volatility, and cross-chain communication delays to ensure that underwater positions can be liquidated promptly to protect protocol solvency.

Interest rate mechanisms in cross-chain lending protocols must consider the complexities of operating across multiple blockchain networks, including varying transaction costs, confirmation times, and market liquidity conditions. Some protocols implement dynamic interest rate models that adjust based on cross-chain market conditions and protocol utilization across different networks.

Security considerations for cross-chain lending protocols are significantly more complex than single-chain systems, as they must protect against attack vectors that could exploit weaknesses in bridge protocols, oracle systems, or cross-chain communication mechanisms. Multi-signature schemes, time delays, and emergency pause mechanisms are commonly implemented to provide additional security layers and recovery options in case of protocol vulnerabilities or attacks.

Collateral Management and Risk Assessment

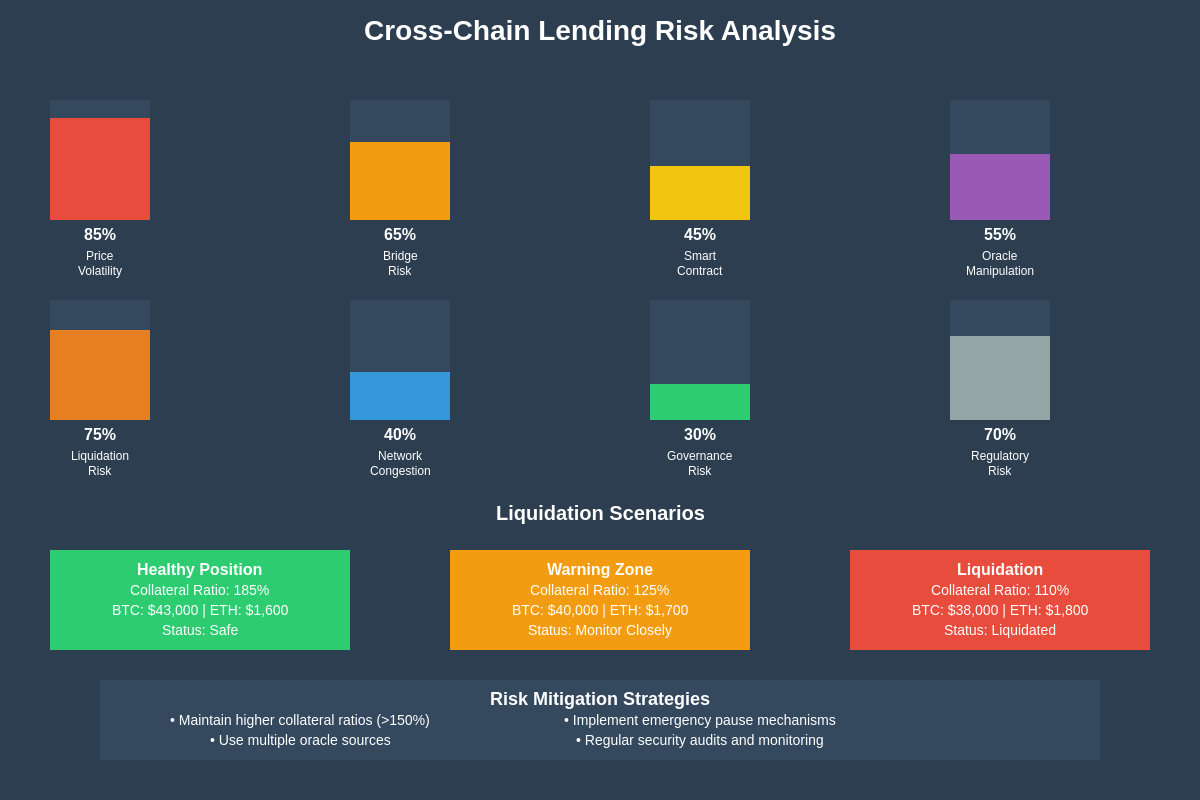

Effective collateral management in cross-chain lending requires sophisticated systems for evaluating, monitoring, and managing assets held on different blockchain networks as security for loans issued on other chains. The fundamental challenge lies in maintaining accurate real-time valuations of collateral assets while accounting for the volatility, liquidity, and technical risks associated with different cryptocurrency assets and blockchain networks.

Collateral evaluation processes must consider not only the market value of pledged assets but also their liquidity characteristics, historical volatility patterns, and the technical risks associated with their underlying blockchain networks. Bitcoin collateral, for example, offers exceptional liquidity and established market depth but operates on a blockchain with different technical characteristics than Ethereum, requiring specialized bridge technologies and longer confirmation times for certain operations.

Risk assessment frameworks for cross-chain lending must account for correlation risks between collateral and borrowed assets, as well as the additional technical risks introduced by cross-chain protocols themselves. When borrowing Ethereum against Bitcoin collateral, lenders must consider not only the price relationship between these assets but also the operational risks associated with bridge protocols, oracle systems, and cross-chain communication mechanisms.

Dynamic collateral ratios represent an important innovation in cross-chain lending, allowing protocols to adjust loan-to-value requirements based on market conditions, asset volatility, and protocol-specific risk factors. These systems can automatically increase collateral requirements during periods of high market volatility or technical uncertainty while relaxing requirements during stable market conditions to improve capital efficiency.

Collateral diversification mechanisms enable borrowers to pledge multiple types of assets across different blockchain networks as security for their loans, reducing concentration risk and providing more flexible collateral management options. However, these systems introduce additional complexity in terms of valuation, monitoring, and liquidation processes that must be carefully managed to maintain protocol security.

The integration of decentralized identity and reputation systems is beginning to enable more sophisticated risk assessment approaches that consider borrower history, transaction patterns, and other behavioral factors in addition to traditional collateral-based risk metrics. These systems could potentially enable lower collateral requirements for trusted borrowers while maintaining appropriate risk controls.

Popular Cross-Chain Lending Platforms and Protocols

The cross-chain lending ecosystem has developed around several pioneering platforms that have implemented different technical approaches to address the challenges of multi-chain finance, each offering unique features, supported assets, and risk profiles that cater to different user needs and market segments.

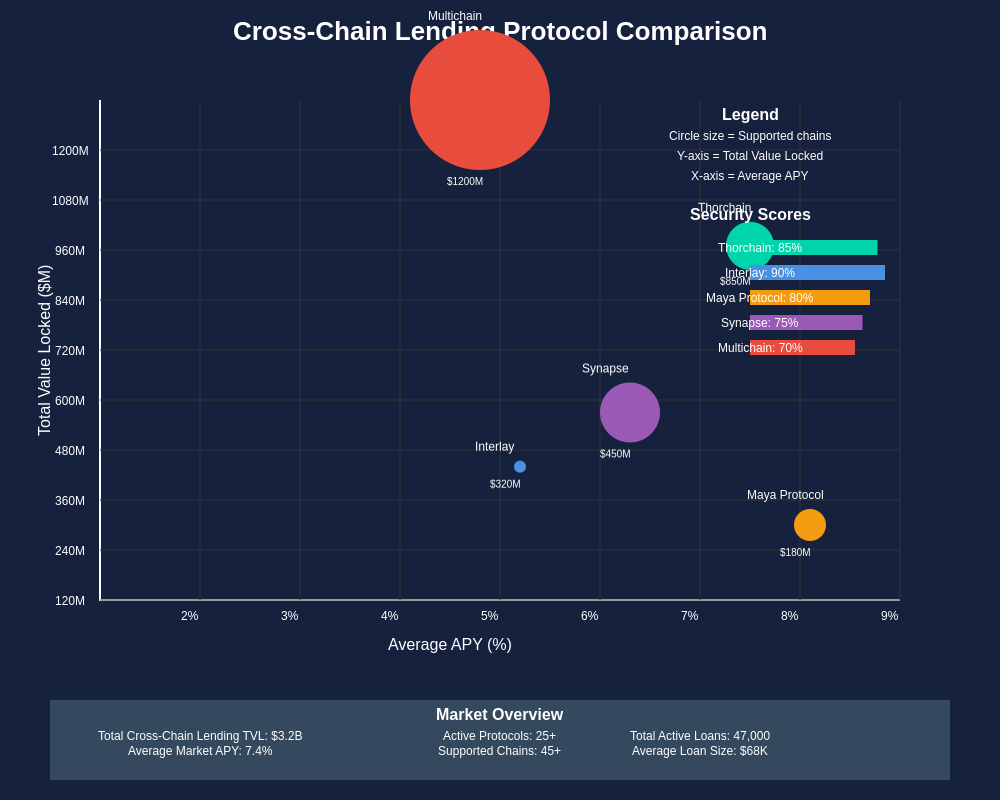

Thorchain represents one of the most ambitious approaches to cross-chain lending, implementing a comprehensive cross-chain automated market maker that enables lending and borrowing across multiple blockchain networks including Bitcoin, Ethereum, and various other cryptocurrency ecosystems. The protocol uses a network of validator nodes to facilitate cross-chain transactions and maintain protocol security while enabling users to earn yield on their assets across different chains.

Ren Protocol has established itself as a leading bridge technology provider, enabling the creation of wrapped Bitcoin tokens that can be used as collateral in Ethereum-based lending protocols. While not a lending protocol itself, Ren’s infrastructure powers many cross-chain lending applications by providing secure and decentralized mechanisms for moving Bitcoin value to other blockchain networks.

Maya Protocol builds upon Thorchain’s technology to provide additional cross-chain lending features, including more sophisticated loan terms, enhanced privacy features, and support for additional blockchain networks. The protocol emphasizes user sovereignty and capital efficiency while maintaining the security and decentralization principles of the broader cross-chain ecosystem.

Interlay’s iBTC protocol provides a Bitcoin-backed synthetic asset on Polkadot that can be used for lending and borrowing within the Polkadot ecosystem while maintaining backing by actual Bitcoin held in a decentralized vault system. This approach combines the benefits of Bitcoin’s store of value properties with the advanced smart contract capabilities of the Polkadot ecosystem.

Multichain (formerly Anyswap) operates one of the largest cross-chain bridge networks, enabling various cross-chain lending applications through its infrastructure for moving assets between different blockchain networks. The platform supports hundreds of different tokens across dozens of blockchain networks, providing the foundational infrastructure for numerous cross-chain lending applications.

Synapse Protocol focuses specifically on cross-chain yield farming and lending opportunities, enabling users to access high-yield lending markets across different blockchain networks while managing their positions through a unified interface. The protocol emphasizes user experience and capital efficiency while maintaining robust security standards.

Economic Models and Interest Rate Mechanisms

Cross-chain lending protocols implement sophisticated economic models that must account for the unique characteristics of operating across multiple blockchain networks, including varying transaction costs, confirmation times, market dynamics, and technical risks that can significantly impact protocol economics and user incentives.

Interest rate determination in cross-chain lending involves complex algorithms that consider supply and demand dynamics across multiple blockchain networks, as well as the additional risks and costs associated with cross-chain operations. Protocol economics must balance competitive rates with sustainable protocol revenue and appropriate risk compensation for the technical complexities of cross-chain operations.

The cost structure of cross-chain lending includes not only traditional lending risks such as default and liquidation costs but also additional expenses related to bridge operations, cross-chain transaction fees, and oracle maintenance. These costs must be factored into interest rate models to ensure protocol sustainability while maintaining competitive rates for users.

Yield optimization strategies in cross-chain lending often involve dynamic allocation of assets across different blockchain networks and lending protocols to maximize returns while managing risk exposure. These strategies require sophisticated algorithms that can account for gas costs, bridge fees, and market conditions across multiple networks to identify optimal lending opportunities.

Token economics for cross-chain lending protocols typically involve governance tokens that provide voting rights over protocol parameters, fee distributions, and upgrade decisions. These tokens may also be used for staking to secure cross-chain operations, providing additional yield opportunities for token holders while enhancing protocol security.

Revenue sharing mechanisms in cross-chain lending protocols must distribute fees and rewards across different stakeholders, including liquidity providers, validators, oracle operators, and protocol developers. The complexity of operating across multiple chains requires carefully designed incentive structures to ensure all participants are appropriately compensated for their contributions to protocol operation.

Insurance and risk mitigation mechanisms represent important components of cross-chain lending economics, with some protocols implementing insurance funds or partnering with decentralized insurance providers to protect users against technical risks associated with cross-chain operations. These protection mechanisms add to protocol costs but can significantly enhance user confidence and adoption.

Regulatory Landscape and Compliance Challenges

The regulatory environment for cross-chain lending presents unique challenges that stem from the multi-jurisdictional nature of these protocols, which may be subject to different regulatory frameworks depending on the blockchain networks involved and the jurisdictions where users and protocol operators are located. Traditional financial regulations often struggle to address the novel characteristics of cross-chain protocols, creating uncertainty for both developers and users.

Securities regulations represent a primary concern for cross-chain lending protocols, particularly regarding the classification of governance tokens, lending terms, and cross-chain derivative products. Different jurisdictions may classify the same protocol features differently, creating compliance challenges for protocols that operate globally across multiple blockchain networks and serve users in various regulatory environments.

Anti-money laundering and know-your-customer requirements present significant implementation challenges for decentralized cross-chain lending protocols, which are designed to operate without central authority or user identification systems. Some protocols are exploring zero-knowledge proof solutions that could enable compliance with identification requirements while preserving user privacy.

Cross-border financial regulations add additional complexity to cross-chain lending, as these protocols may be subject to international banking regulations, foreign exchange controls, and cross-border payment restrictions depending on how regulatory authorities classify cross-chain lending transactions and the assets involved.

The evolving regulatory landscape for decentralized finance continues to impact cross-chain lending protocols, with new regulations and enforcement actions potentially affecting protocol operation, token distribution, and user access. Protocol developers must carefully monitor regulatory developments across multiple jurisdictions and implement appropriate compliance measures.

Tax implications for cross-chain lending vary significantly across different jurisdictions, with users potentially subject to different tax treatments for collateral posting, interest payments, and liquidation events depending on their location and the specific characteristics of their cross-chain lending activities. The complexity of tracking and reporting cross-chain transactions for tax purposes creates additional burdens for users and may impact protocol adoption.

Security Considerations and Risk Vectors

Cross-chain lending protocols face a complex array of security challenges that extend beyond traditional DeFi security considerations to include risks associated with bridge protocols, oracle systems, and multi-chain coordination mechanisms. These protocols must protect against both well-known DeFi attack vectors and novel risks that emerge from the additional complexity of cross-chain operations.

Bridge security represents one of the most critical risk factors for cross-chain lending protocols, as compromised bridge systems could potentially allow attackers to manipulate collateral balances, create unauthorized tokens, or drain protocol funds. The security of cross-chain lending protocols is fundamentally dependent on the security of the underlying bridge infrastructure they utilize.

Oracle manipulation attacks pose heightened risks in cross-chain environments, where price feeds must be coordinated across multiple blockchain networks with different update frequencies, cost structures, and potential attack vectors. Sophisticated attackers may attempt to exploit discrepancies between oracle systems or manipulate prices on specific chains to trigger improper liquidations or enable over-borrowing.

Smart contract risks in cross-chain lending are amplified by the complexity of coordinating contract execution across multiple blockchain networks, with potential vulnerabilities in cross-chain communication protocols, state synchronization mechanisms, and atomic transaction processing. Bugs or vulnerabilities in any component of the cross-chain system could potentially compromise the entire protocol.

Governance attacks represent a particular concern for cross-chain protocols, where attackers might attempt to gain control over governance mechanisms to modify protocol parameters, upgrade smart contracts, or redirect funds. The distributed nature of cross-chain protocols can make governance coordination more challenging while potentially creating new attack vectors.

Network-specific risks must be considered for each blockchain network supported by cross-chain lending protocols, including consensus mechanism vulnerabilities, network congestion impacts, and hard fork risks that could affect protocol operation. Protocols must implement appropriate monitoring and response mechanisms for network-specific events that could impact protocol security or functionality.

Operational security for cross-chain lending protocols requires robust monitoring systems that can track protocol health across multiple blockchain networks, detect anomalous activity, and coordinate emergency responses when necessary. The complexity of monitoring cross-chain systems requires specialized tools and expertise that may not be readily available to all protocol teams.

Technical Integration and Implementation Challenges

Implementing cross-chain lending protocols requires addressing numerous technical challenges related to blockchain interoperability, smart contract coordination, and user experience optimization across multiple network environments with different technical characteristics and operational requirements.

Cross-chain communication protocols must provide reliable mechanisms for transmitting transaction data, state updates, and execution confirmations between different blockchain networks while maintaining security guarantees and preventing various attack vectors. The latency and reliability characteristics of these communication systems directly impact the user experience and operational efficiency of cross-chain lending protocols.

State synchronization across multiple blockchain networks presents complex technical challenges, particularly when dealing with different block confirmation times, reorg possibilities, and network congestion patterns that can affect the timing and reliability of cross-chain operations. Protocols must implement sophisticated coordination mechanisms to ensure consistent state across all supported networks.

User experience optimization for cross-chain lending requires careful design of interfaces and workflows that can abstract away the technical complexity of multi-chain operations while providing users with clear visibility into transaction status, fees, and confirmation requirements across different networks. Cross-chain transaction management must balance simplicity with the inherent complexity of multi-network operations.

Gas optimization strategies for cross-chain lending must account for varying fee structures and transaction costs across different blockchain networks, potentially implementing dynamic routing algorithms that can select optimal execution paths based on current network conditions and user preferences. These optimizations become particularly important during periods of network congestion when transaction costs can vary dramatically.

Wallet integration challenges arise from the need to support multiple blockchain networks within unified user interfaces while maintaining security standards and providing seamless user experiences. Cross-chain lending protocols must work with wallet providers to ensure compatibility and optimize user workflows for multi-chain operations.

Testing and deployment strategies for cross-chain lending protocols require comprehensive approaches that can validate protocol behavior across multiple blockchain networks and various network conditions. The complexity of cross-chain systems makes traditional testing approaches insufficient, requiring specialized tools and methodologies for multi-chain protocol validation.

Market Impact and Adoption Trends

The emergence of cross-chain lending has begun to significantly impact cryptocurrency markets by increasing capital efficiency, reducing market fragmentation, and enabling new trading and arbitrage strategies that were previously impossible or prohibitively expensive to execute across different blockchain networks.

Capital efficiency improvements from cross-chain lending allow cryptocurrency holders to generate returns from their assets without selling positions or moving funds to centralized exchanges, potentially reducing selling pressure on major cryptocurrency markets while increasing overall market liquidity and efficiency. Bitcoin holders can now access yield opportunities in DeFi markets without converting their holdings to other assets.

Market arbitrage opportunities created by cross-chain lending protocols enable more efficient price discovery across different blockchain networks and cryptocurrency exchanges, potentially reducing price disparities and improving overall market efficiency. These arbitrage mechanisms help maintain price consistency across different trading venues and blockchain networks.

Institutional adoption of cross-chain lending has been limited by regulatory uncertainty and technical complexity, though several institutional cryptocurrency service providers are exploring cross-chain lending solutions as part of their broader DeFi integration strategies. The maturation of cross-chain lending protocols could significantly expand institutional participation in DeFi markets.

Retail user adoption has grown steadily as user interfaces improve and transaction costs decrease, with many cryptocurrency holders attracted to the ability to earn yield on their holdings without selling positions or using centralized services. However, adoption remains limited by technical complexity and security concerns among less sophisticated users.

The impact on traditional cryptocurrency lending markets has been mixed, with some centralized lending platforms experiencing reduced demand as users migrate to decentralized alternatives, while others have integrated cross-chain capabilities to remain competitive. The overall lending market has expanded as new use cases and user segments have emerged.

Cross-chain lending has also influenced the development of other DeFi protocols, inspiring innovations in cross-chain derivatives, yield farming, and liquidity mining that build upon the foundational technologies developed for cross-chain lending applications.

Future Developments and Emerging Technologies

The future of cross-chain lending is likely to be shaped by several emerging technologies and development trends that could significantly expand the capabilities, security, and user experience of cross-chain financial protocols while addressing current limitations and enabling new use cases.

Zero-knowledge proof technologies are being explored for enhancing privacy and security in cross-chain lending, potentially enabling private collateral verification, confidential loan terms, and privacy-preserving liquidation mechanisms that could attract users who require enhanced privacy protection for their financial activities.

Layer 2 scaling solutions and rollup technologies are being integrated into cross-chain lending protocols to reduce transaction costs and improve performance while maintaining security guarantees. These technologies could make cross-chain lending more accessible to smaller users and enable more sophisticated financial products that require frequent cross-chain interactions.

Artificial intelligence and machine learning applications are being developed for risk assessment, yield optimization, and automated portfolio management in cross-chain lending environments. These technologies could enable more sophisticated risk models and automated strategies that optimize returns while managing exposure across multiple blockchain networks.

Quantum-resistant cryptography research is beginning to influence cross-chain protocol design as developers prepare for potential future threats to current cryptographic systems. Quantum-resistant cross-chain lending protocols could provide enhanced long-term security guarantees for users with extended investment horizons.

Central bank digital currency integration represents a potential future development that could significantly impact cross-chain lending markets, particularly if CBDCs are designed with interoperability features that enable integration with existing DeFi protocols and cross-chain infrastructure.

Regulatory technology solutions are being developed to help cross-chain lending protocols navigate complex compliance requirements while maintaining decentralization and user privacy. These solutions could enable broader adoption by addressing regulatory concerns that currently limit institutional participation.

The integration of real-world assets into cross-chain lending protocols represents an emerging trend that could significantly expand the collateral types and use cases supported by these systems. Tokenized real estate, commodities, and other traditional assets could provide new opportunities for diversified collateral strategies.

Conclusion and Market Outlook

Cross-chain lending represents a fundamental evolution in decentralized finance that addresses one of the key limitations of the current blockchain ecosystem by enabling efficient capital utilization across different networks without sacrificing the security and decentralization principles that make DeFi attractive to users seeking alternatives to traditional financial systems.

The technical achievements of current cross-chain lending protocols demonstrate the feasibility of sophisticated financial applications that operate across multiple blockchain networks while maintaining robust security and user experience standards. However, the technology remains in its early stages, with significant opportunities for improvement in areas such as user experience, capital efficiency, and security mechanisms.

Market adoption of cross-chain lending is likely to accelerate as the cryptocurrency ecosystem becomes increasingly multi-chain and users seek more efficient ways to manage their digital asset portfolios across different blockchain networks. The ability to use Bitcoin as collateral for accessing Ethereum DeFi applications represents just one example of the powerful financial applications enabled by cross-chain lending technology.

The regulatory landscape for cross-chain lending will continue to evolve as governments and regulatory agencies develop frameworks for addressing the unique characteristics of cross-chain financial protocols. Clear regulatory guidance could significantly accelerate institutional adoption while providing greater certainty for protocol developers and users.

Technical innovation in cross-chain lending will likely focus on improving security, reducing costs, and enhancing user experience while expanding the range of supported assets and blockchain networks. The integration of emerging technologies such as zero-knowledge proofs and layer 2 scaling solutions could address many current limitations.

The long-term impact of cross-chain lending on cryptocurrency markets and the broader financial system could be profound, potentially enabling new forms of capital allocation, risk management, and financial innovation that bridge the gap between different blockchain ecosystems and traditional financial markets. As the technology matures and adoption increases, cross-chain lending could become a fundamental component of the global financial infrastructure, providing efficient and accessible lending services that operate across any blockchain network or geographic boundary.

Disclaimer

This article is for informational and educational purposes only and should not be construed as financial advice. Cryptocurrency investments and DeFi protocols involve significant risks, including the potential loss of principal. Cross-chain lending protocols are experimental technologies that may contain bugs, vulnerabilities, or other issues that could result in financial losses. Users should conduct thorough research and consider their risk tolerance before participating in any cross-chain lending activities. Past performance does not guarantee future results, and cryptocurrency markets are highly volatile and unpredictable. Always consult with qualified financial advisors before making investment decisions.