Access comprehensive financial tools and services that are revolutionizing how small and medium enterprises approach business financing in the digital economy.

The Digital Transformation of SME Banking

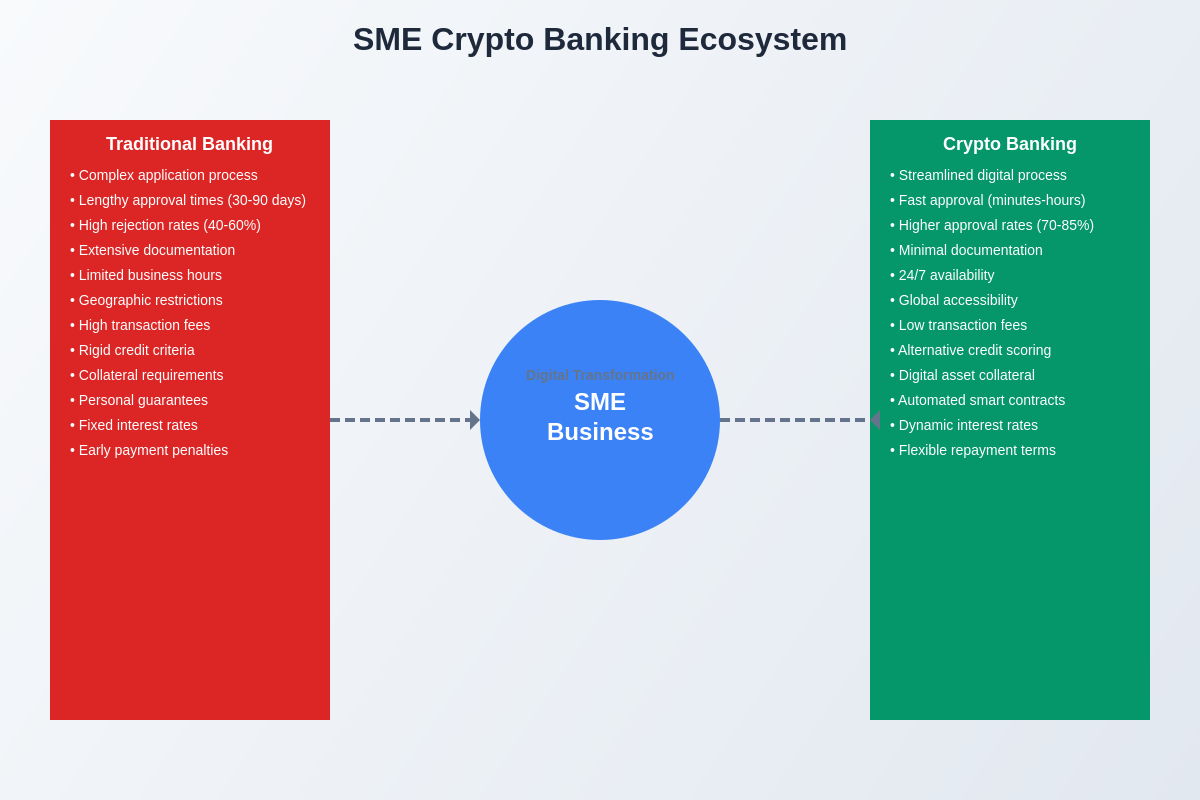

Small and medium enterprises represent the backbone of the global economy, accounting for over 90% of businesses worldwide while employing more than half of the global workforce. However, traditional banking systems have consistently failed to adequately serve these businesses, with complex application processes, lengthy approval times, and restrictive lending criteria that often exclude viable businesses from accessing essential capital. The emergence of cryptocurrency-based banking solutions is fundamentally transforming this landscape, offering SMEs unprecedented access to flexible, efficient, and innovative financial services that were previously available only to large corporations or high-net-worth individuals.

The traditional banking sector’s approach to SME lending has been characterized by rigid assessment criteria, extensive documentation requirements, and prolonged decision-making processes that can extend for months before businesses receive funding. This antiquated system often fails to recognize the unique characteristics of modern digital businesses, gig economy participants, and innovative startups that may lack traditional credit histories or physical collateral but possess significant potential for growth and profitability. Cryptocurrency banking platforms are addressing these fundamental shortcomings by leveraging blockchain technology, automated underwriting systems, and alternative credit assessment methodologies to provide faster, more accessible, and more equitable financing solutions.

The integration of real-time market data and analytics into crypto banking platforms enables more sophisticated risk assessment models that consider a broader range of factors when evaluating SME loan applications. These platforms can analyze blockchain transaction histories, digital asset holdings, trading patterns, and business performance metrics to create comprehensive risk profiles that go beyond traditional credit scores and collateral requirements.

Decentralized Finance and SME Lending Protocols

Decentralized Finance protocols have emerged as powerful alternatives to traditional banking infrastructure, offering SMEs direct access to global capital markets without the need for intermediary financial institutions. These protocols utilize smart contracts and automated market makers to facilitate lending and borrowing activities, creating more efficient and transparent financial ecosystems that benefit both borrowers and lenders. The programmable nature of DeFi protocols allows for the creation of customized lending products that can be tailored to specific industry requirements, seasonal cash flow patterns, and unique business models that traditional banks struggle to understand or accommodate.

The liquidity pools that power DeFi lending protocols aggregate capital from diverse sources including individual investors, institutional funds, and protocol treasuries, creating deep and resilient funding sources that can support significant lending volumes. This distributed approach to capital provision reduces reliance on traditional banking infrastructure while providing more competitive interest rates and flexible terms for SME borrowers. The transparent and auditable nature of blockchain-based lending protocols also provides greater clarity regarding lending terms, interest calculations, and repayment schedules, reducing the information asymmetries that often disadvantage small businesses in traditional banking relationships.

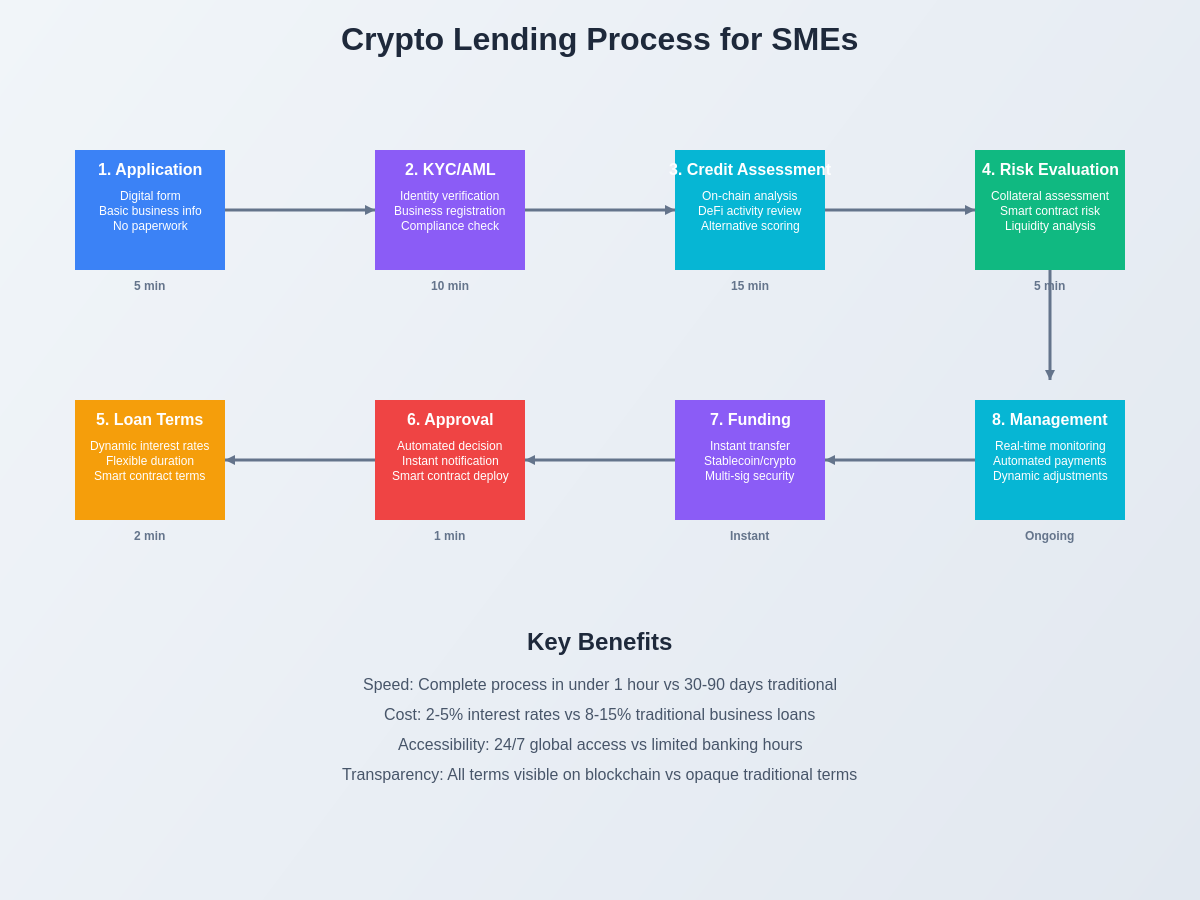

Smart contract automation within DeFi lending protocols enables instantaneous loan origination, automated interest calculations, and programmable repayment schedules that reduce operational overhead while improving the borrower experience. These automated systems can process loan applications, verify collateral, and execute funding transfers within minutes rather than the weeks or months required by traditional banking systems. The efficiency gains from automation are passed on to borrowers in the form of lower interest rates and reduced fees, making cryptocurrency-based lending increasingly attractive for SMEs seeking working capital or expansion funding.

Collateralized Lending Solutions

Cryptocurrency collateralized lending represents one of the most mature and widely adopted forms of crypto banking for SMEs, allowing businesses to unlock liquidity from their digital asset holdings without triggering taxable events through asset sales. This approach is particularly valuable for businesses that have accumulated cryptocurrency through operations, payments, or strategic investments and need to access traditional currency for operational expenses while maintaining their digital asset positions. The over-collateralization requirements typical of crypto lending platforms provide security for lenders while offering borrowers competitive interest rates and flexible repayment terms.

The diversity of acceptable collateral in cryptocurrency lending platforms extends beyond major cryptocurrencies to include stablecoins, tokenized real-world assets, and even NFTs in some cases, providing SMEs with multiple options for securing financing based on their specific asset holdings. Advanced collateral management systems automatically monitor collateral values and can trigger margin calls or liquidation events to protect lenders while providing borrowers with real-time visibility into their collateral positions and loan-to-value ratios.

Dynamic interest rate models used by cryptocurrency lending platforms adjust rates based on supply and demand dynamics, utilization rates, and market conditions, ensuring that SMEs have access to competitive pricing that reflects current market conditions. These algorithmic interest rate adjustments can result in significant cost savings compared to fixed-rate traditional loans, particularly during periods of high liquidity or favorable market conditions. The ability to repay loans early without prepayment penalties also provides SMEs with greater flexibility in managing their debt obligations and cash flow requirements.

Stablecoin-Based Business Banking

Stablecoin-based banking solutions offer SMEs the benefits of cryptocurrency technology while minimizing the volatility concerns associated with traditional cryptocurrencies, creating an ideal bridge between traditional business banking and the digital asset ecosystem. These platforms provide business checking accounts, payment processing, and lending services denominated in stablecoins pegged to major fiat currencies, enabling businesses to operate entirely within the cryptocurrency ecosystem while maintaining price stability for accounting and planning purposes.

The programmable nature of stablecoins enables sophisticated business banking features including automated payments, conditional transfers, and multi-signature approval workflows that can streamline business operations while providing enhanced security and control. Smart contract integration allows for the automation of recurring payments, supplier settlements, and employee compensation, reducing administrative overhead while ensuring timely and accurate transaction processing. These automated systems can significantly reduce the operational costs associated with business banking while providing greater transparency and auditability for financial operations.

Cross-border payment capabilities of stablecoin-based banking platforms eliminate many of the friction points associated with international business transactions, including high fees, long settlement times, and complex compliance requirements. SMEs engaged in international trade can benefit from near-instantaneous settlement of payments, transparent fee structures, and 24/7 availability that enables business operations across different time zones without the constraints of traditional banking hours. The blockchain-based nature of these transactions also provides immutable records that can simplify accounting, audit, and compliance processes.

Alternative Credit Assessment Models

Cryptocurrency banking platforms are pioneering innovative credit assessment methodologies that go beyond traditional credit scores and financial statements to evaluate SME creditworthiness using on-chain data, business performance metrics, and alternative data sources. These models can analyze blockchain transaction histories to assess cash flow patterns, payment consistency, and business relationships, providing a more comprehensive and current view of business financial health than static credit reports or historical financial statements.

On-chain reputation systems aggregate data from multiple blockchain networks to create comprehensive profiles of business entities, including transaction volumes, counterparty relationships, smart contract interactions, and DeFi protocol participation. This holistic approach to credit assessment can identify creditworthy businesses that may be overlooked by traditional banking systems, particularly those operating in emerging markets, serving underbanked populations, or utilizing innovative business models that don’t fit conventional lending criteria.

Machine learning algorithms applied to blockchain data can identify patterns and relationships that human underwriters might miss, enabling more accurate risk assessment and pricing for SME loans. These systems can continuously update risk assessments based on real-time on-chain activity, allowing for dynamic loan terms and credit limits that reflect current business performance rather than historical data. The transparency and immutability of blockchain data also reduces the potential for fraud or misrepresentation in the credit assessment process, creating more reliable and trustworthy lending relationships.

Regulatory Frameworks and Compliance

The regulatory landscape for cryptocurrency banking services is rapidly evolving as governments and financial authorities worldwide develop frameworks to govern digital asset banking and lending activities. SMEs considering cryptocurrency banking solutions must navigate complex and often changing regulatory requirements that vary significantly across jurisdictions, with some regions embracing innovation while others maintain restrictive approaches to cryptocurrency financial services.

Compliance requirements for cryptocurrency banking platforms typically include anti-money laundering procedures, know-your-customer verification, suspicious activity reporting, and consumer protection measures that mirror traditional banking regulations while addressing unique risks associated with digital assets. Leading cryptocurrency banking platforms invest heavily in compliance infrastructure and legal expertise to ensure adherence to applicable regulations while providing businesses with confidence in the legitimacy and sustainability of their services.

The emergence of regulatory sandboxes and pilot programs in various jurisdictions provides opportunities for cryptocurrency banking platforms to operate under experimental licenses while regulators study the implications of these new financial technologies. These programs enable innovation while maintaining appropriate oversight and consumer protection, creating pathways for the gradual integration of cryptocurrency banking services into the broader financial system. SMEs operating in jurisdictions with supportive regulatory frameworks may have access to more comprehensive and mature cryptocurrency banking services compared to those in regions with restrictive or uncertain regulatory environments.

Risk Management and Security Considerations

Cryptocurrency banking for SMEs introduces unique risk management challenges that require sophisticated security measures and risk mitigation strategies to protect business assets and operations. The irreversible nature of blockchain transactions means that security breaches or operational errors can result in permanent loss of funds, making robust security protocols essential for any business considering cryptocurrency banking solutions. Multi-signature wallet architectures, hardware security modules, and cold storage systems are standard security measures that protect business funds while maintaining operational efficiency.

Smart contract risk represents a significant consideration for SMEs utilizing DeFi lending protocols, as bugs or vulnerabilities in smart contract code can potentially result in loss of funds or unexpected behavior. Due diligence processes for evaluating DeFi protocols should include code audits, historical performance analysis, and assessment of development team credentials to minimize exposure to smart contract risks. Insurance products specifically designed for DeFi activities are beginning to emerge, providing additional protection for businesses utilizing decentralized lending protocols.

Operational security measures for cryptocurrency banking include secure key management practices, regular security audits, employee training programs, and incident response procedures that can minimize the impact of security breaches or operational errors. The distributed nature of cryptocurrency systems means that businesses must take greater responsibility for their own security compared to traditional banking relationships where financial institutions assume much of the security burden. However, this increased responsibility also provides businesses with greater control over their financial operations and reduced dependence on third-party institutions.

Integration with Traditional Business Operations

The successful implementation of cryptocurrency banking solutions requires careful integration with existing business operations, accounting systems, and workflow processes to maximize benefits while minimizing disruption to daily operations. Modern cryptocurrency banking platforms provide APIs and integration tools that enable seamless connection with popular business software including accounting packages, payment processors, and enterprise resource planning systems, ensuring that cryptocurrency-based financial activities are properly recorded and reconciled with traditional business records.

Accounting considerations for cryptocurrency banking include proper classification of digital assets, recognition of gains and losses from cryptocurrency holdings, and compliance with tax reporting requirements that vary significantly across jurisdictions. Many businesses work with specialized accounting firms or utilize cryptocurrency-specific accounting software to ensure accurate record-keeping and tax compliance for their digital asset activities. The increasing sophistication of cryptocurrency accounting tools is making it easier for SMEs to integrate cryptocurrency banking into their existing financial management processes.

Staff training and change management processes are essential for successful cryptocurrency banking adoption, as employees must understand new technologies, security procedures, and operational workflows associated with digital asset management. Leading cryptocurrency banking platforms provide comprehensive training resources, customer support, and onboarding assistance to help businesses transition smoothly from traditional banking relationships to cryptocurrency-based financial services.

Cost Analysis and Economic Benefits

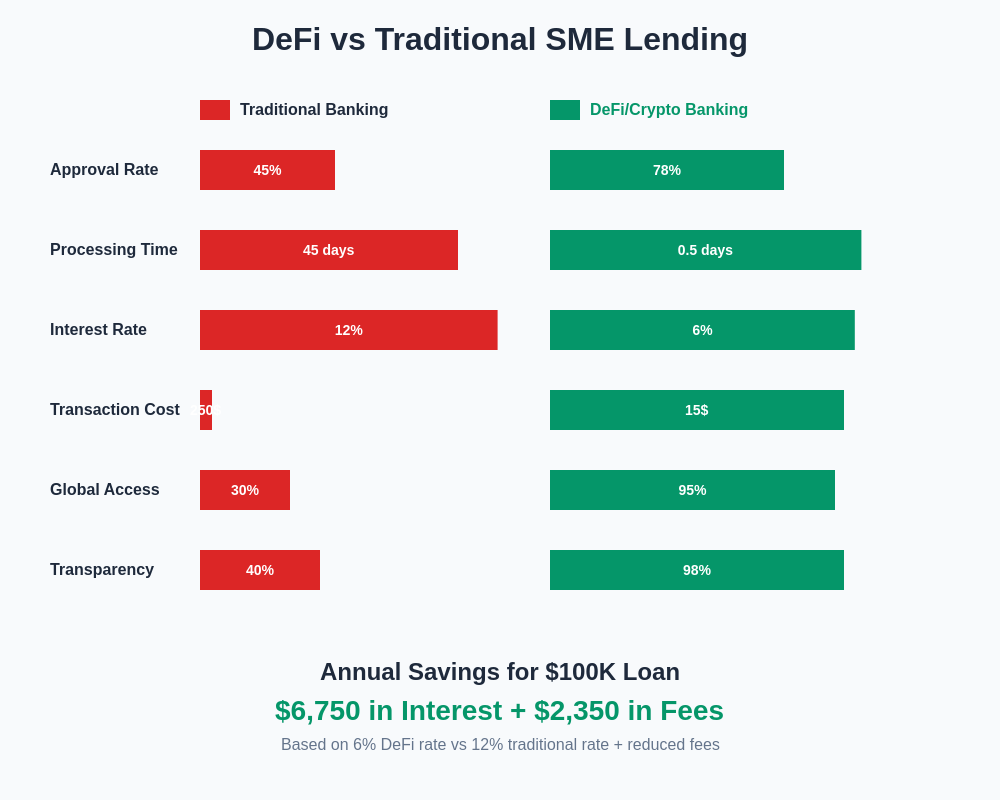

The economic benefits of cryptocurrency banking for SMEs extend beyond lower transaction costs to include improved cash flow management, faster access to capital, and reduced dependence on traditional banking infrastructure that may be expensive or unavailable in certain markets. Transaction costs for cryptocurrency-based payments and transfers are typically significantly lower than traditional wire transfers, credit card processing, or international remittances, providing immediate cost savings for businesses with high transaction volumes or international operations.

Interest rates for cryptocurrency-based lending can be more competitive than traditional business loans, particularly for businesses with strong digital asset holdings or on-chain credit histories that demonstrate creditworthiness. The elimination of traditional banking intermediaries in DeFi lending protocols reduces overhead costs that are typically passed on to borrowers in the form of higher interest rates and fees. Variable interest rate models that adjust based on market conditions can provide additional cost savings during periods of high liquidity or favorable market conditions.

The efficiency gains from automated cryptocurrency banking processes can reduce operational costs associated with payment processing, reconciliation, and financial management, freeing up resources that can be deployed for business growth and development. The 24/7 availability of cryptocurrency banking services eliminates delays associated with traditional banking hours and processing schedules, enabling businesses to respond more quickly to opportunities and customer needs.

Global Market Access and Cross-Border Solutions

Cryptocurrency banking solutions provide SMEs with unprecedented access to global markets and customers by eliminating many of the barriers associated with traditional cross-border banking and payment processing. The borderless nature of cryptocurrency networks enables businesses to accept payments, settle invoices, and access funding from anywhere in the world without the need for correspondent banking relationships or complex international wire transfer procedures.

The programmable nature of cryptocurrency payments enables sophisticated international trade finance solutions including documentary credits, trade financing, and supply chain finance products that can automate and streamline complex international transactions. Smart contracts can be programmed to automatically execute payments upon delivery confirmation, quality verification, or other predetermined conditions, reducing counterparty risk while improving transaction efficiency for international trade relationships.

Currency hedging and exchange rate risk management tools available through cryptocurrency platforms can help SMEs manage the financial risks associated with international operations while taking advantage of global market opportunities. Stablecoin-based solutions provide natural hedging against local currency volatility while maintaining the operational benefits of cryptocurrency-based payments and banking services.

Technology Infrastructure and Platform Selection

The selection of appropriate cryptocurrency banking platforms requires careful evaluation of technology infrastructure, security measures, regulatory compliance, and feature sets that align with specific business requirements and risk tolerance. Established platforms with proven track records, comprehensive insurance coverage, and robust compliance frameworks may be more suitable for conservative businesses, while newer platforms with innovative features and competitive rates might appeal to more risk-tolerant SMEs seeking cutting-edge financial solutions.

Due diligence processes for cryptocurrency banking platform selection should include assessment of the platform’s financial stability, technical architecture, security measures, regulatory status, and customer support capabilities. The rapidly evolving nature of the cryptocurrency industry means that platform selection criteria must consider not only current capabilities but also the platform’s ability to adapt to changing market conditions, regulatory requirements, and technological developments.

Integration capabilities and technical requirements for cryptocurrency banking platforms vary significantly, with some solutions requiring minimal technical expertise while others may need dedicated IT resources or specialized knowledge for proper implementation and management. Businesses should carefully assess their technical capabilities and resource availability when selecting cryptocurrency banking solutions to ensure successful implementation and ongoing management of their digital asset banking relationships.

Future Developments and Industry Trends

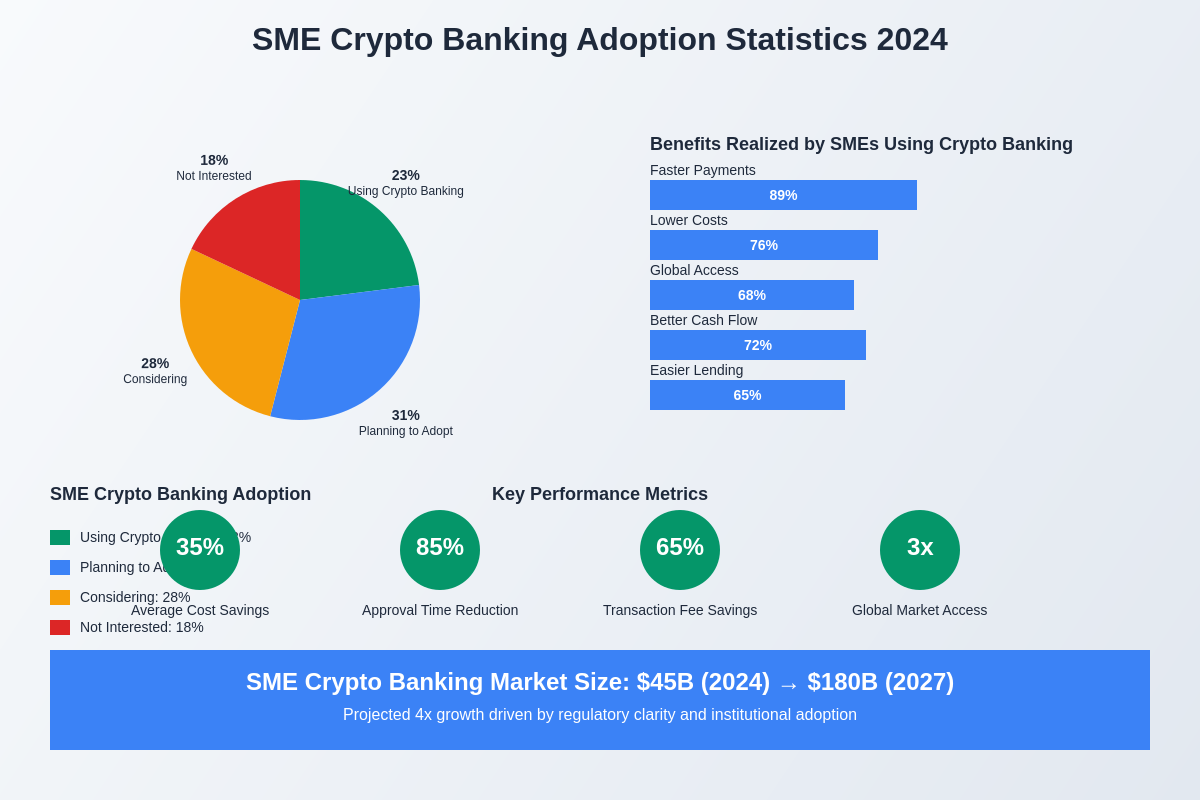

The cryptocurrency banking industry for SMEs is rapidly evolving with new products, services, and technologies emerging regularly to address the unique needs of small and medium enterprises. Central bank digital currencies are beginning to be deployed in various jurisdictions, potentially providing government-backed alternatives to private stablecoins while maintaining many of the operational benefits of cryptocurrency-based banking systems. These developments could significantly expand the mainstream adoption of digital currency banking while providing greater regulatory clarity and consumer protection.

Artificial intelligence and machine learning technologies are being integrated into cryptocurrency banking platforms to provide more sophisticated risk assessment, fraud detection, and personalized financial services that can better serve the diverse needs of SME customers. These technologies enable more accurate credit scoring, automated customer service, and predictive analytics that can help businesses optimize their financial management and planning processes.

The integration of Internet of Things devices and real-world asset tokenization is creating new opportunities for asset-backed lending and supply chain finance solutions that leverage physical assets and operational data to provide innovative financing options for SMEs. These developments are expanding the range of collateral types and credit assessment methodologies available through cryptocurrency banking platforms while creating new opportunities for businesses to monetize their assets and operations.

Case Studies and Implementation Examples

Successful implementations of cryptocurrency banking solutions across various industries demonstrate the practical benefits and challenges associated with digital asset banking for SMEs. E-commerce businesses have leveraged cryptocurrency payment processing and lending solutions to reduce transaction costs, access global markets, and manage seasonal cash flow variations more effectively than traditional banking solutions would allow. The ability to accept cryptocurrency payments directly and convert them to stablecoins for operational use provides these businesses with operational flexibility while reducing payment processing costs and chargeback risks.

Manufacturing companies have utilized cryptocurrency-based supply chain finance solutions to improve working capital management and strengthen supplier relationships through faster payment settlement and transparent payment terms. The programmable nature of cryptocurrency payments enables automated payment schedules tied to delivery milestones and quality verification, reducing administrative overhead while improving supplier cash flow and relationships.

Professional services firms have adopted cryptocurrency banking solutions to serve clients in emerging markets where traditional banking infrastructure may be limited or expensive, enabling them to expand their global reach while maintaining competitive pricing. The ability to receive payments in cryptocurrency and access global funding sources through DeFi platforms provides these businesses with operational advantages that would be difficult to achieve through traditional banking relationships.

Risk Mitigation Strategies

Comprehensive risk mitigation strategies for cryptocurrency banking involve diversification across multiple platforms and protocols, maintenance of traditional banking relationships for operational flexibility, and implementation of robust security and operational procedures that address the unique risks associated with digital asset management. Businesses should avoid concentrating all their financial activities on single platforms or protocols, instead spreading risk across multiple service providers while maintaining the ability to quickly adapt to changing market conditions or platform issues.

Insurance coverage specifically designed for cryptocurrency business activities is becoming increasingly available and sophisticated, providing protection against exchange hacks, smart contract failures, key loss, and other risks unique to digital asset management. While cryptocurrency insurance markets are still developing, leading platforms and service providers are partnering with specialized insurers to provide comprehensive coverage options for business customers.

Professional advisory services specializing in cryptocurrency business applications can provide valuable guidance for SMEs navigating the complex landscape of digital asset banking, helping businesses assess risks, evaluate platforms, and implement appropriate security and operational procedures. These advisory relationships can be particularly valuable for businesses new to cryptocurrency banking or those operating in highly regulated industries where compliance considerations are paramount.

Conclusion and Strategic Recommendations

The transformation of SME banking through cryptocurrency and blockchain technologies represents one of the most significant developments in business finance since the advent of online banking, offering unprecedented opportunities for businesses to access capital, reduce costs, and operate more efficiently in the global digital economy. However, successful adoption of cryptocurrency banking solutions requires careful planning, risk assessment, and ongoing management to maximize benefits while mitigating potential risks and challenges.

SMEs considering cryptocurrency banking solutions should begin with pilot programs or limited implementations that allow them to gain experience and assess the practical benefits and challenges of digital asset banking without exposing their entire business to new risks. This measured approach enables businesses to build internal expertise, establish appropriate security procedures, and evaluate different platforms and services before making larger commitments to cryptocurrency-based financial infrastructure.

Advanced trading tools and market analysis continue to evolve alongside cryptocurrency banking platforms, providing SMEs with sophisticated financial management capabilities that were previously available only to large corporations with substantial resources.

The regulatory landscape for cryptocurrency banking will continue to evolve, and SMEs should stay informed about developments in their jurisdictions while maintaining flexibility to adapt their strategies as new regulations and opportunities emerge. The businesses that successfully navigate this transition will be well-positioned to capitalize on the efficiency gains, cost savings, and global market access that cryptocurrency banking solutions provide, while those that fail to adapt may find themselves at a competitive disadvantage in an increasingly digital business environment.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments and banking services involve significant risks including potential loss of capital. The regulatory status of cryptocurrency banking services varies by jurisdiction and may change. Readers should conduct their own research and consult with qualified financial and legal advisors before making any investment or business decisions. Past performance does not guarantee future results, and the cryptocurrency market is highly volatile and unpredictable.