The convergence of decentralized identity systems and cryptocurrency lending is revolutionizing how creditworthiness is assessed and verified in the digital asset ecosystem, creating new opportunities for financial inclusion while addressing the persistent challenges of trust and identity verification that have long plagued decentralized finance protocols. Traditional credit scoring systems rely heavily on centralized data repositories and legacy financial institutions, creating barriers for individuals who lack traditional credit histories or operate primarily within cryptocurrency markets.

Decentralized identity solutions for crypto credit scoring represent a paradigm shift toward user-controlled financial reputation systems that leverage blockchain technology, zero-knowledge proofs, and distributed verification mechanisms to create portable, privacy-preserving credit profiles that can be used across multiple DeFi platforms and lending protocols. These systems promise to democratize access to credit while giving users unprecedented control over their financial data and reputation.

The Evolution of Credit Assessment in Cryptocurrency Markets

The traditional credit scoring model developed by agencies like Experian, Equifax, and TransUnion relies on centralized data collection and analysis of traditional financial behaviors including payment history, credit utilization, length of credit history, types of credit accounts, and recent credit inquiries. This model breaks down in cryptocurrency markets where transactions are pseudonymous, financial relationships are peer-to-peer, and traditional banking relationships may not exist.

Early cryptocurrency lending platforms attempted to address this challenge through over-collateralization requirements that eliminate the need for credit assessment by requiring borrowers to deposit cryptocurrency assets worth significantly more than the loan amount. While this approach reduces lender risk, it also excludes potential borrowers who lack sufficient collateral and fails to build sustainable credit relationships that could enable more efficient capital allocation.

The emergence of decentralized identity standards including DID (Decentralized Identifiers), verifiable credentials, and self-sovereign identity frameworks has created new possibilities for developing credit scoring systems that operate independently of traditional financial institutions while maintaining privacy and user control. These systems can aggregate on-chain transaction data, cross-reference multiple blockchain networks, and incorporate additional data sources to create comprehensive creditworthiness assessments.

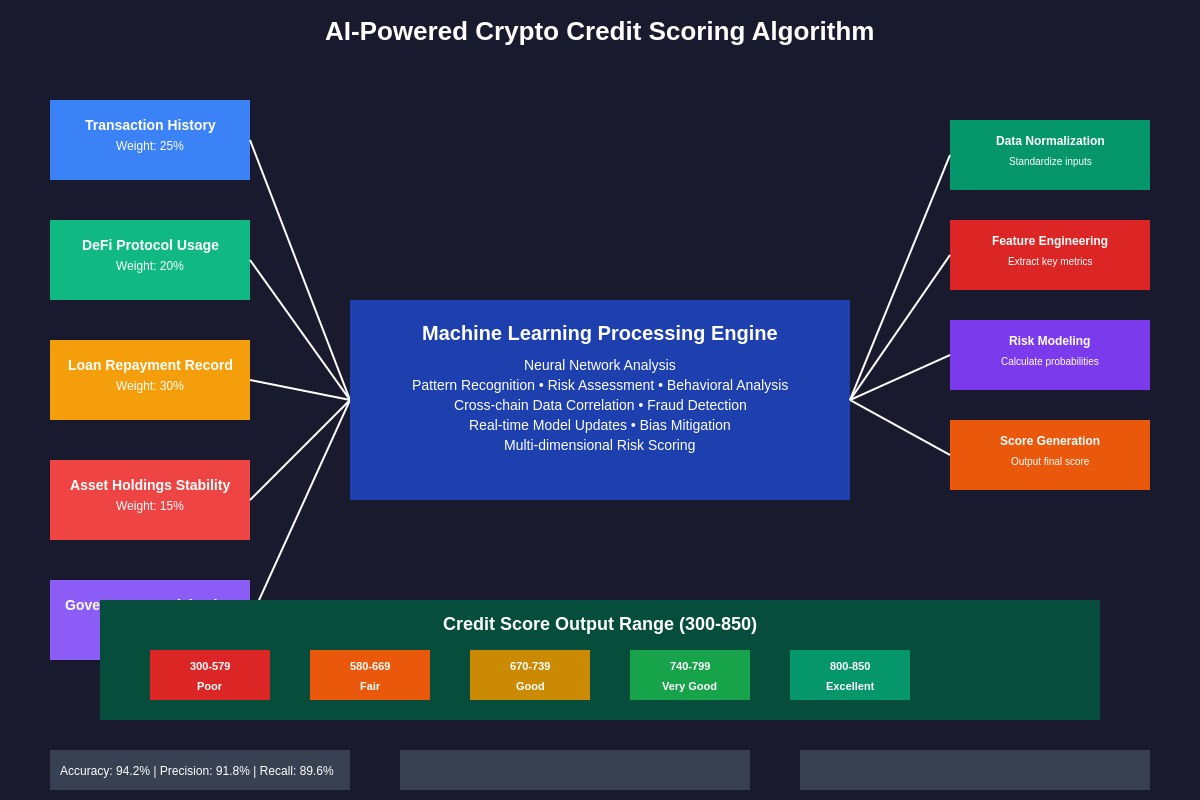

Advanced analysis of on-chain behavior patterns provides rich insights into borrower reliability including transaction frequency and consistency, wallet balance volatility, interaction with different DeFi protocols, loan repayment history across platforms, and participation in governance and staking activities. When it comes to analyzing historical cryptocurrency price movements and lending trends, professional traders and institutions rely on sophisticated charting platforms to make informed decisions about credit risk assessment and portfolio management strategies.

Machine learning algorithms can process vast amounts of blockchain data to identify patterns and correlations that human analysts might miss, enabling more accurate risk assessment and potentially reducing default rates compared to traditional credit scoring methods. These algorithms can adapt to changing market conditions and borrower behaviors, continuously improving their predictive accuracy through ongoing analysis of loan performance data.

Technical Architecture of Decentralized Identity Systems

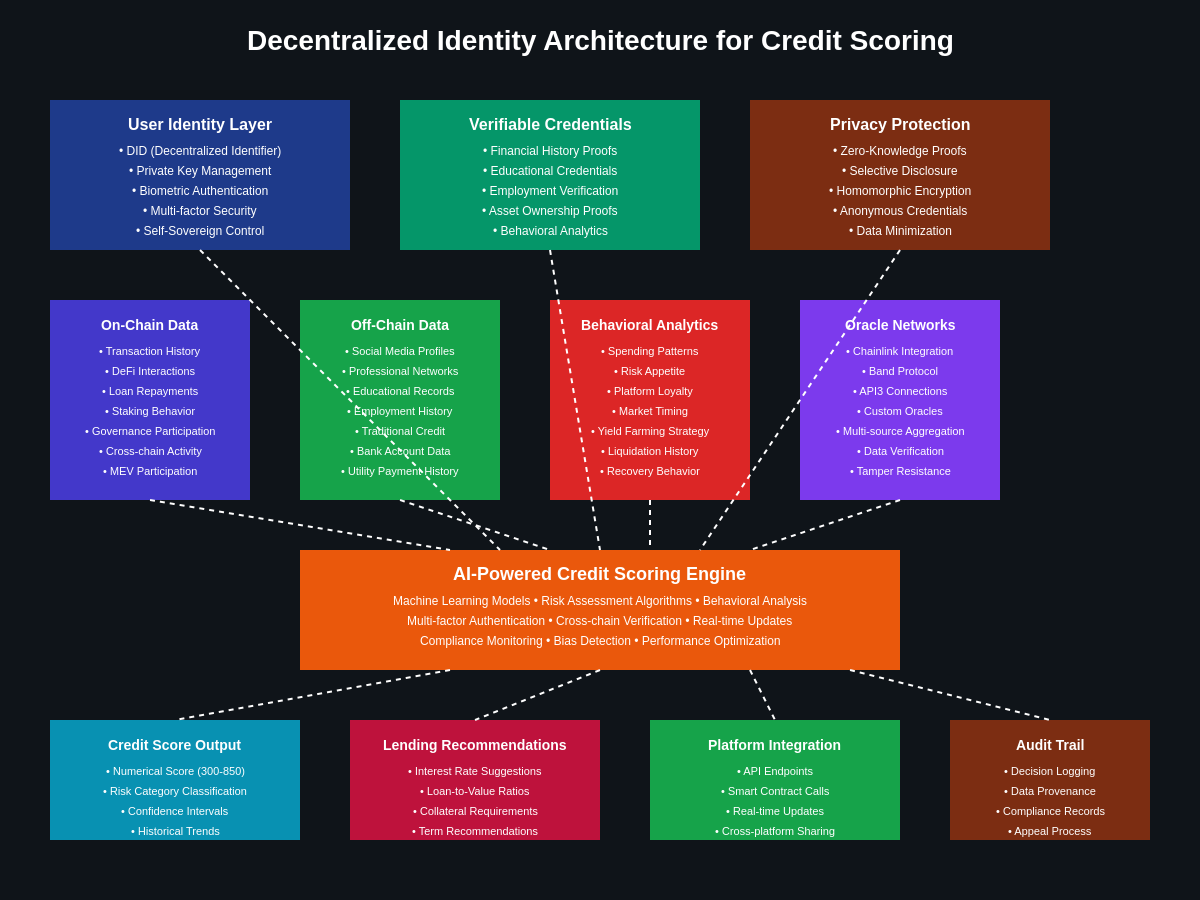

The technical foundation of decentralized identity for crypto credit scoring relies on several interconnected components including blockchain-based identity verification, cryptographic proof systems, distributed data storage, and cross-platform interoperability protocols. At the core of these systems are decentralized identifiers that provide persistent, cryptographically verifiable identifiers that users control without relying on centralized authorities.

Verifiable credentials enable the issuance and verification of claims about identity attributes, financial behaviors, and creditworthiness without requiring direct access to underlying personal data. These credentials can be issued by various entities including DeFi protocols, traditional financial institutions, educational institutions, employers, and government agencies, creating a comprehensive picture of an individual’s financial and personal reliability.

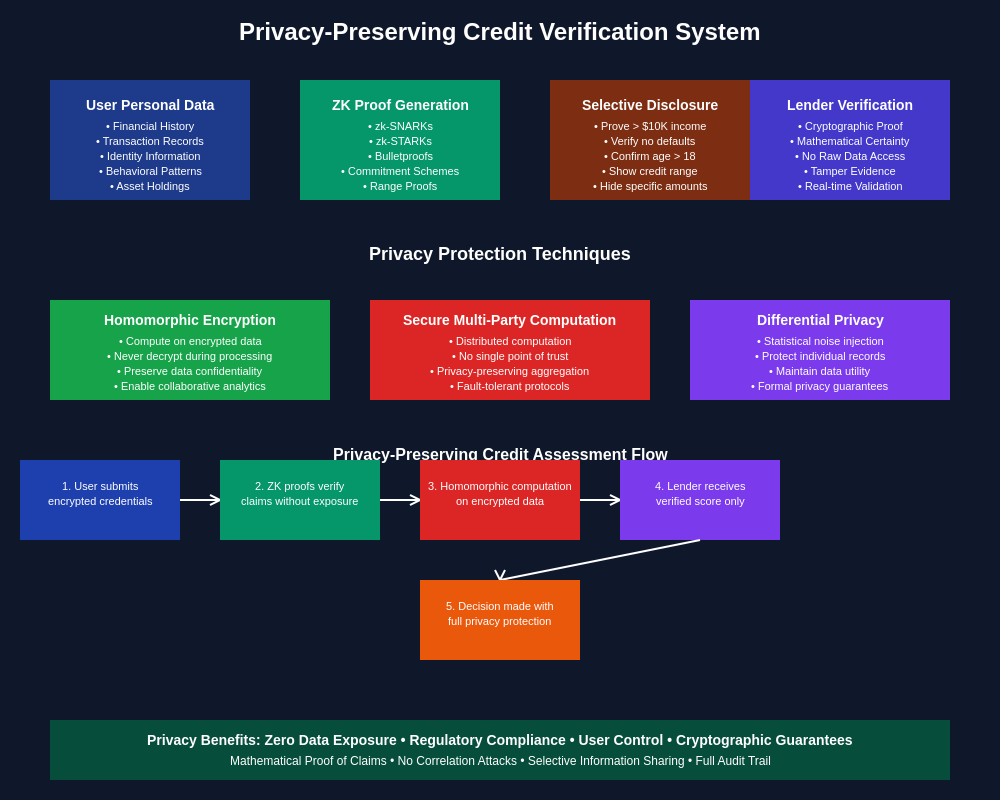

Zero-knowledge proof systems play a crucial role in enabling privacy-preserving credit verification by allowing borrowers to prove specific attributes about their financial history without revealing sensitive details. For example, a borrower could prove they have never defaulted on a loan without revealing the specific loans, amounts, or lenders involved, maintaining privacy while providing necessary assurance to potential lenders.

Distributed storage systems ensure that identity and credit data remains accessible and tamper-resistant without relying on centralized servers that could become points of failure or censorship. Technologies like IPFS (InterPlanetary File System), Arweave, and other decentralized storage networks provide redundant, distributed storage that can maintain data integrity across network disruptions and attempts at censorship.

Interoperability protocols enable different blockchain networks and DeFi platforms to share and verify identity and credit information, creating network effects that make decentralized identity systems more valuable as adoption increases. Cross-chain communication protocols like Cosmos IBC, Polkadot’s XCMP, and various bridge technologies facilitate the flow of identity and reputation data across blockchain ecosystems.

Smart contract frameworks automate the verification and utilization of decentralized identity credentials in lending decisions, reducing the need for manual underwriting while ensuring consistent application of credit policies. These frameworks can integrate with various DeFi lending protocols to provide seamless access to credit based on verified identity and credit scoring data.

Privacy and Security Considerations

Privacy protection in decentralized identity systems for credit scoring requires careful balance between providing sufficient information for accurate risk assessment while protecting sensitive personal and financial data from unauthorized access or misuse. Zero-knowledge proofs enable selective disclosure of information, allowing borrowers to share only the minimum necessary data to qualify for specific loan products or interest rates.

Encryption and access control mechanisms ensure that even when identity and credit data is stored on distributed networks, it remains accessible only to authorized parties with proper cryptographic keys or credentials. Advanced encryption schemes including attribute-based encryption and proxy re-encryption enable fine-grained control over data access while maintaining system usability and performance.

Biometric and multi-factor authentication systems provide additional security layers to prevent identity theft and unauthorized access to decentralized identity credentials. These systems can incorporate hardware security modules, mobile device biometrics, and behavioral analysis to ensure that only legitimate credential holders can access and utilize their identity profiles.

Regular security audits and vulnerability assessments of decentralized identity systems are essential for maintaining trust and preventing exploitation by malicious actors who might attempt to manipulate credit scores or steal identity credentials. Professional security firms specializing in blockchain and cryptocurrency systems conduct comprehensive audits of smart contracts, cryptographic implementations, and system architectures.

Incident response and recovery procedures must be established to handle potential security breaches, credential compromises, or system failures that could affect users’ ability to access credit or could compromise sensitive identity information. These procedures should include coordination with affected platforms, user notification systems, and mechanisms for credential revocation and reissuance.

Regulatory Compliance and Legal Frameworks

The regulatory landscape for decentralized identity and credit scoring systems intersects with multiple areas of financial regulation including consumer protection laws, data privacy regulations, fair lending practices, and anti-money laundering requirements. Different jurisdictions have varying approaches to regulating these systems, creating compliance challenges for platforms operating across multiple regions.

Data protection regulations like GDPR in Europe and CCPA in California impose specific requirements on how personal data is collected, processed, stored, and shared, even in decentralized systems. Compliance with these regulations requires careful consideration of data minimization principles, user consent mechanisms, and data portability requirements that may conflict with the immutable nature of blockchain systems.

Fair lending laws in various jurisdictions require that credit decisions are made without discrimination based on protected characteristics like race, gender, religion, or national origin. Decentralized identity systems must incorporate safeguards to prevent algorithmic bias in credit scoring while maintaining the privacy protections that make these systems attractive to users.

Anti-money laundering and know-your-customer requirements present particular challenges for decentralized identity systems that prioritize privacy and user control. Regulatory authorities may require identity verification and transaction monitoring capabilities that could compromise the privacy benefits of decentralized systems, requiring innovative approaches to compliance that balance regulatory requirements with user privacy.

Cross-border regulatory coordination becomes increasingly important as decentralized identity systems operate across national boundaries and traditional jurisdictional frameworks. International cooperation and standardization efforts may be necessary to create coherent regulatory frameworks that support innovation while protecting consumers and maintaining financial system integrity.

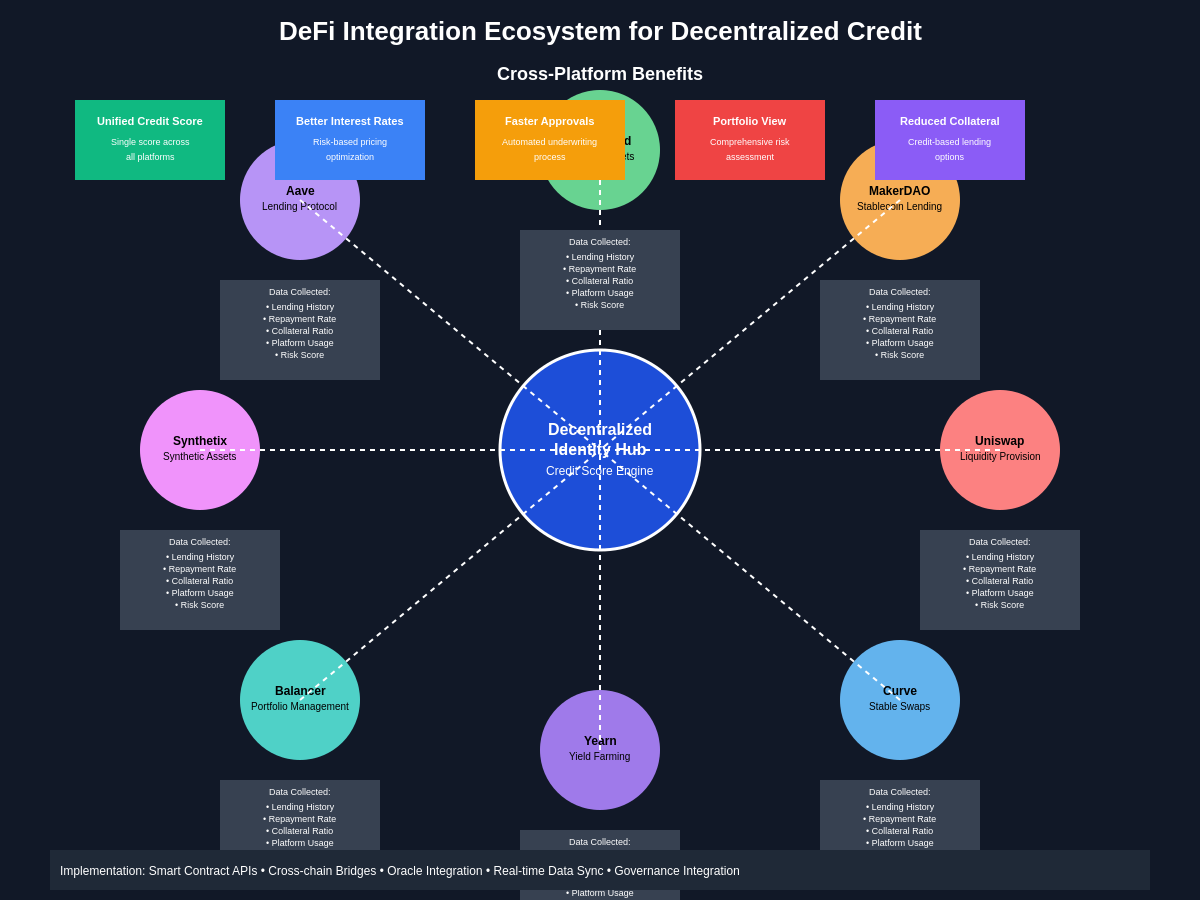

Integration with Existing DeFi Protocols

The integration of decentralized identity systems with existing DeFi lending protocols requires significant technical and operational changes to support identity verification, credit scoring, and risk management functions. Many existing protocols were designed around over-collateralization models that eliminate the need for identity verification, requiring substantial modifications to incorporate credit-based lending.

Governance token holders in various DeFi protocols must evaluate and approve proposals to integrate decentralized identity systems, weighing the potential benefits of expanded lending opportunities against the risks and costs associated with implementing new identity verification requirements. These decisions often require extensive community discussion and technical analysis to ensure that integration efforts align with protocol objectives and user expectations.

Smart contract upgrades to support decentralized identity integration must be carefully planned and tested to avoid introducing vulnerabilities or disrupting existing protocol functionality. Many DeFi protocols utilize proxy contracts or modular architectures that can facilitate integration with identity systems while maintaining backward compatibility with existing users and integrations.

Liquidity management becomes more complex when incorporating credit-based lending alongside traditional over-collateralized loans, requiring sophisticated risk management systems that can balance different types of loan products while maintaining protocol solvency. Dynamic interest rate models may need adjustment to account for varying risk profiles associated with different identity verification levels and credit scores.

User experience design for identity-integrated DeFi protocols must balance security and privacy requirements with usability concerns, ensuring that identity verification processes are streamlined and accessible while maintaining the trustless and permissionless characteristics that make DeFi attractive to users. Interface design should guide users through identity verification and credit assessment processes without overwhelming them with technical complexity.

Economic Models and Incentives

The economic sustainability of decentralized identity systems for crypto credit scoring depends on creating aligned incentives for all participants including identity credential issuers, verification services, data providers, lending protocols, and end users. Token-based incentive systems can reward participants for maintaining accurate identity data, providing reliable verification services, and contributing to the overall health of the credit scoring ecosystem.

Data monetization models must balance the value created by identity and credit data with user privacy rights and control over personal information. Users should be able to benefit financially from the value their data creates while maintaining control over how it is used and shared, potentially through revenue-sharing mechanisms or tokenized data rights.

Credit scoring algorithm development and maintenance requires ongoing investment in research, development, and infrastructure, which may be supported through transaction fees, subscription models, or token-based governance and funding mechanisms. Open-source development models can reduce costs and increase transparency while requiring sustainable funding mechanisms to ensure continued innovation and maintenance.

Risk-sharing mechanisms between lenders, identity verification services, and credit scoring providers can help distribute the costs and risks associated with loan defaults while providing appropriate incentives for accurate risk assessment and responsible lending practices. These mechanisms might include insurance pools, mutual guarantee systems, or profit-sharing arrangements based on loan performance.

Network effects and platform adoption strategies are crucial for the success of decentralized identity systems, as the value of these systems increases with the number of participating platforms and users. Early adopter incentives, partnership programs, and cross-platform compatibility initiatives can help build the critical mass necessary for sustainable ecosystem growth.

Technical Challenges and Limitations

Scalability remains a significant challenge for decentralized identity systems that must process large volumes of identity verifications, credential updates, and credit score calculations while maintaining acceptable performance levels. Layer 2 scaling solutions, sidechains, and off-chain computation systems may be necessary to achieve the throughput required for mainstream adoption of decentralized credit scoring.

Interoperability between different blockchain networks and identity standards creates technical complexity that must be managed through standardization efforts, bridge technologies, and cross-chain communication protocols. The lack of universal standards for decentralized identity can fragment the ecosystem and reduce the network effects that make these systems valuable to users.

Data quality and verification challenges arise when aggregating information from multiple sources with varying levels of reliability and accuracy. Consensus mechanisms and reputation systems for data sources can help ensure data quality, but these systems themselves introduce additional complexity and potential points of failure.

Key management and recovery procedures for decentralized identity systems must balance security with usability, ensuring that users can maintain control over their identity credentials while providing mechanisms for recovery in case of key loss or compromise. Social recovery, multi-signature schemes, and hardware security modules can provide enhanced security but may increase system complexity and user friction.

Oracle systems that provide off-chain data to decentralized identity and credit scoring systems face the traditional oracle problem of ensuring data accuracy and preventing manipulation. Decentralized oracle networks, multiple data source aggregation, and cryptographic verification mechanisms can help address these challenges but may increase system costs and complexity.

Market Adoption and User Behavior

User adoption of decentralized identity systems for crypto credit scoring depends on providing clear value propositions including improved access to credit, better interest rates, enhanced privacy protection, and portability of credit history across platforms. Educational initiatives and user experience improvements are essential for overcoming the learning curve associated with these new systems.

Institutional adoption by cryptocurrency lending platforms, traditional financial institutions exploring blockchain technology, and regulatory bodies influences the overall market development and legitimacy of decentralized identity systems. Pilot programs, regulatory sandboxes, and industry partnerships can help establish proof of concept and build confidence in these emerging technologies.

Market dynamics between competing decentralized identity solutions create pressure for standardization and interoperability while driving innovation in privacy protection, user experience, and technical capabilities. Platform competition can benefit users through improved services and lower costs, but fragmentation can reduce network effects and slow adoption.

User behavior patterns in cryptocurrency markets, including privacy preferences, platform loyalty, and risk tolerance, influence the design and adoption of decentralized identity systems. Understanding these patterns is essential for developing systems that meet user needs while achieving sustainable business models.

Cross-platform migration and data portability features enable users to maintain their identity and credit history when switching between different DeFi platforms or cryptocurrency services. These features are essential for preventing vendor lock-in and maintaining user control over identity data, but they require technical coordination between different service providers.

Future Technological Developments

Artificial intelligence and machine learning integration with decentralized identity systems will enable more sophisticated credit scoring algorithms that can analyze complex patterns in on-chain behavior, market conditions, and borrower characteristics. Privacy-preserving machine learning techniques including federated learning and homomorphic encryption can enable advanced analytics while maintaining data privacy.

Quantum-resistant cryptography development is essential for ensuring the long-term security of decentralized identity systems as quantum computing capabilities advance. Migration to post-quantum cryptographic standards will require careful planning and coordination across the entire ecosystem to prevent disruption of existing identity credentials and verification systems.

Internet of Things integration could expand decentralized identity systems beyond financial applications to include identity verification for smart contracts, supply chain management, and autonomous system interactions. IoT devices could serve as additional data sources for identity verification and behavioral analysis while introducing new security and privacy challenges.

Biometric integration with decentralized identity systems could provide stronger identity verification while raising additional privacy concerns that must be addressed through advanced cryptographic techniques and careful system design. Biometric data must be protected against theft and misuse while remaining useful for identity verification purposes.

Regulatory technology solutions that automate compliance with various regulatory requirements could reduce the burden on decentralized identity system operators while ensuring consistent adherence to applicable laws and regulations. These solutions could include automated reporting, risk assessment, and audit trail generation capabilities.

Case Studies and Implementation Examples

Several blockchain projects and DeFi platforms have begun implementing decentralized identity solutions for credit scoring with varying approaches and levels of success. Analysis of these early implementations provides valuable insights into the practical challenges and opportunities associated with deploying these systems at scale.

Self-sovereign identity initiatives from organizations like the Sovrin Foundation, Microsoft ION, and various government digital identity programs demonstrate different approaches to implementing decentralized identity infrastructure that could support crypto credit scoring applications. These initiatives provide technical foundations and regulatory precedents that can inform cryptocurrency-specific implementations.

Credit scoring experiments in emerging markets where traditional credit infrastructure is limited show the potential for decentralized identity systems to enable financial inclusion and expand access to credit. These implementations often face unique challenges related to technology access, regulatory frameworks, and user education that provide lessons for broader adoption efforts.

Partnership programs between traditional financial institutions and blockchain identity providers explore hybrid approaches that combine centralized and decentralized identity systems to provide comprehensive credit scoring capabilities. These partnerships demonstrate potential paths for mainstream adoption while highlighting integration challenges and regulatory considerations.

Academic research and development projects provide theoretical foundations and experimental results that inform the design and implementation of production decentralized identity systems. Peer-reviewed research helps establish best practices and identify potential vulnerabilities or limitations that should be addressed in system design.

Risk Management and Mitigation Strategies

Credit risk assessment in decentralized identity systems requires new approaches that account for the unique characteristics of cryptocurrency markets including high volatility, regulatory uncertainty, and the pseudonymous nature of blockchain transactions. Advanced risk models must incorporate these factors while providing accurate assessments of borrower creditworthiness.

Technical risk management includes protection against smart contract vulnerabilities, oracle manipulation, private key compromise, and various attack vectors specific to blockchain systems. Regular security audits, bug bounty programs, and formal verification techniques can help identify and address potential vulnerabilities before they can be exploited.

Operational risk considerations include the reliability of decentralized infrastructure, the availability of verification services, and the potential for system disruptions that could affect users’ ability to access credit or update their identity credentials. Redundancy, fail-safe mechanisms, and incident response procedures are essential for maintaining system reliability.

Regulatory risk management requires ongoing monitoring of changing legal requirements and proactive adaptation of system design and operations to maintain compliance. Legal expertise and regulatory engagement are essential for navigating the complex and evolving regulatory landscape affecting decentralized identity and credit systems.

Counterparty risk in decentralized systems includes the reliability of identity credential issuers, the accuracy of data providers, and the financial stability of lending platforms that rely on decentralized identity systems. Due diligence processes and risk assessment frameworks can help users and platforms evaluate and manage these risks.

Economic Impact and Market Opportunities

The potential economic impact of widespread adoption of decentralized identity for crypto credit scoring includes expanded access to credit for underserved populations, reduced costs for identity verification and credit assessment, and improved efficiency in capital allocation within cryptocurrency markets. These benefits could contribute to overall financial system efficiency and economic growth.

Market size estimates for decentralized identity and credit scoring systems consider the growing cryptocurrency lending market, the expanding DeFi ecosystem, and the potential for these systems to serve traditional financial markets through blockchain integration. Market research and adoption forecasts help inform investment and development decisions across the ecosystem.

Cost-benefit analysis of implementing decentralized identity systems must account for development costs, ongoing operational expenses, regulatory compliance costs, and the potential benefits including reduced fraud, improved risk assessment accuracy, and expanded market opportunities. These analyses help stakeholders evaluate the economic viability of different implementation approaches.

Competitive advantage considerations for early adopters of decentralized identity systems include first-mover benefits, network effect advantages, and the potential for differentiation in increasingly competitive cryptocurrency financial services markets. Strategic planning and market positioning are important considerations for platforms considering identity system integration.

Investment opportunities in decentralized identity infrastructure, credit scoring technology, and related services attract venture capital, strategic investment from financial institutions, and token-based funding mechanisms. Understanding investment trends and funding patterns helps identify promising projects and emerging market opportunities.

Privacy-Preserving Analytics and Insights

Advanced analytical capabilities that maintain user privacy while providing valuable insights for credit assessment represent a key technological frontier in decentralized identity systems. Techniques including differential privacy, secure multi-party computation, and homomorphic encryption enable sophisticated data analysis while protecting individual privacy.

Behavioral analytics based on on-chain transaction patterns can provide insights into borrower reliability, spending habits, and financial stability without requiring access to traditional financial data. These analytics must be designed to avoid discrimination and bias while providing accurate risk assessment capabilities.

Aggregate market insights derived from anonymized identity and credit data can help lending platforms, regulators, and researchers understand market trends, risk patterns, and the effectiveness of different credit assessment approaches. These insights can inform policy decisions and system improvements while protecting individual privacy.

Predictive modeling capabilities that use privacy-preserving techniques to forecast market conditions, default risks, and borrower behavior can help lending platforms optimize their risk management and pricing strategies. Machine learning models trained on encrypted or anonymized data can provide valuable predictions while maintaining data privacy.

Real-time monitoring and alerting systems that detect potential fraud, identity theft, or system manipulation without compromising user privacy are essential for maintaining system integrity and user trust. These systems must balance security needs with privacy protection while providing timely responses to potential threats.

Conclusion and Future Outlook

The development of decentralized identity systems for crypto credit scoring represents a significant evolution in how creditworthiness is assessed and managed in digital asset markets, offering the potential for more inclusive, privacy-preserving, and user-controlled financial reputation systems. While significant technical, regulatory, and adoption challenges remain, ongoing innovation and increasing market demand for these solutions suggest a promising future for this technology.

The success of decentralized identity for crypto credit scoring will depend on continued technological development, regulatory clarity, market adoption, and the ability to balance competing demands for privacy, security, transparency, and regulatory compliance. Collaboration between technology developers, financial institutions, regulators, and users will be essential for realizing the full potential of these systems.

As cryptocurrency markets continue to mature and integrate with traditional financial systems, decentralized identity solutions may become essential infrastructure for enabling efficient capital allocation, risk management, and financial inclusion. The lessons learned from early implementations and the ongoing evolution of blockchain technology will shape the future development and adoption of these transformative systems.

For traders and analysts seeking to understand the technical and market factors driving cryptocurrency credit and lending markets, comprehensive charting and analysis tools provide essential insights into price movements, volume patterns, and market sentiment that influence lending rates and credit availability across DeFi platforms.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency investments and DeFi lending involve significant risks, including the potential loss of principal. Decentralized identity systems are experimental technology with technical and regulatory uncertainties. Readers should conduct their own research and consult qualified professionals before making any financial decisions or participating in cryptocurrency lending markets. Past performance does not guarantee future results, and all investments in cryptocurrency and DeFi protocols carry inherent risks that may result in partial or total loss of funds.