The Revolution of Decentralized Credit Assessment

The emergence of decentralized finance has fundamentally transformed how we approach credit assessment and lending, moving from traditional centralized models that rely on institutional gatekeepers and credit bureaus to innovative on-chain reputation systems that leverage blockchain transparency and mathematical algorithms to evaluate creditworthiness. This paradigm shift represents one of the most significant developments in financial infrastructure since the advent of traditional credit scoring systems, offering unprecedented opportunities for financial inclusion while challenging conventional assumptions about risk assessment and borrower evaluation.

The traditional credit scoring system, dominated by institutions like FICO and major credit bureaus, has long been criticized for its opacity, geographical limitations, and exclusion of billions of people worldwide who lack formal banking relationships or sufficient credit history. These legacy systems rely heavily on historical financial data, employment records, and payment histories that may not accurately reflect an individual’s current financial capabilities or future creditworthiness, particularly in rapidly changing economic environments.

Decentralized finance introduces a revolutionary alternative through on-chain reputation systems that analyze blockchain transaction data to create comprehensive credit profiles without requiring traditional documentation or institutional intermediaries. These systems can evaluate borrower behavior in real-time, assess portfolio composition and management skills, analyze transaction patterns and frequency, and measure adherence to protocol rules and smart contract obligations, creating a more dynamic and inclusive approach to credit assessment.

The transparency inherent in blockchain technology enables lenders and borrowers to access the same information simultaneously, reducing information asymmetries that have historically plagued traditional lending markets. Every transaction, every protocol interaction, and every financial decision made by a wallet address becomes part of an immutable record that can be analyzed and scored using sophisticated algorithms that consider factors ranging from liquidity provision patterns on TradingView to governance token voting behavior across multiple protocols.

Historical Development and Evolution of On-Chain Credit Systems

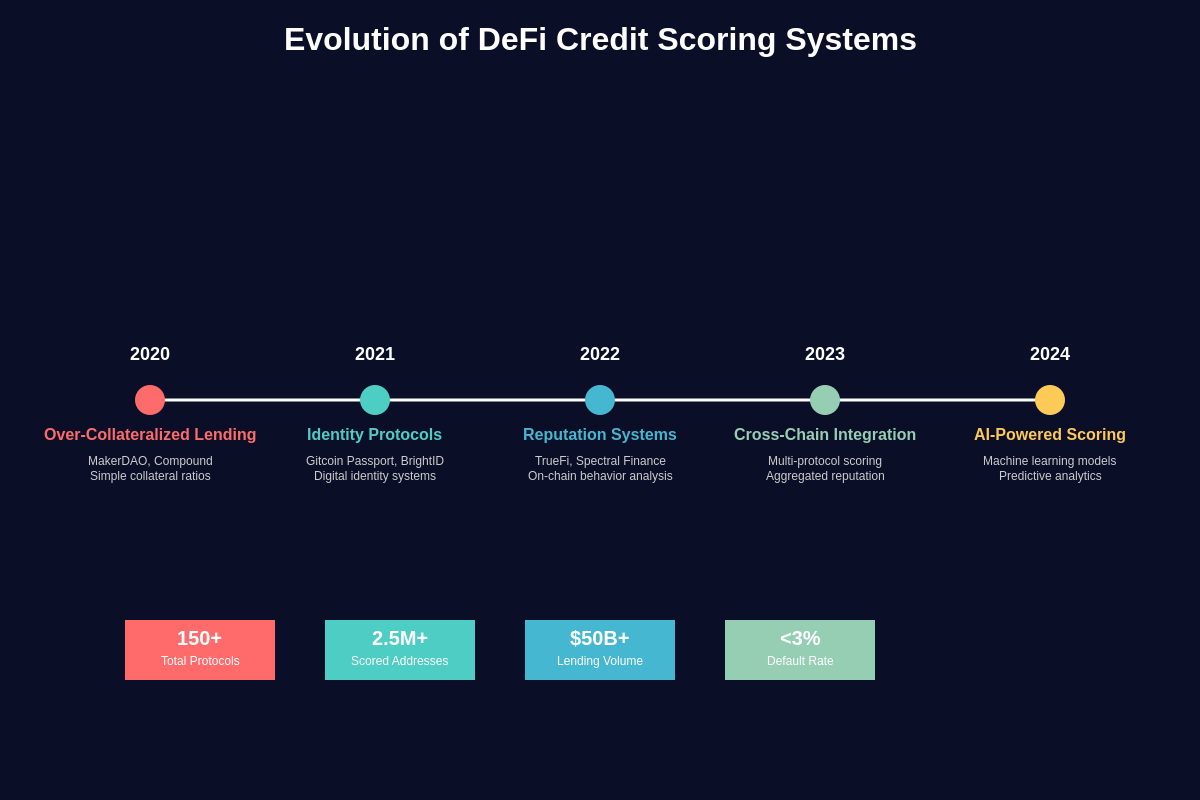

The evolution of on-chain credit scoring systems has been marked by rapid innovation and experimentation as the DeFi ecosystem has matured and expanded. Early implementations were relatively simple, focusing primarily on over-collateralization ratios and basic transaction history analysis, but have evolved into sophisticated multi-dimensional scoring systems that incorporate machine learning, behavioral analysis, and complex risk modeling techniques.

The first generation of DeFi lending protocols, including platforms like MakerDAO and Compound, initially relied on simple over-collateralization mechanisms that required borrowers to deposit assets worth significantly more than their borrowed amounts. While these systems eliminated the need for traditional credit checks, they also limited access to capital for users who lacked substantial cryptocurrency holdings, essentially replicating some of the exclusionary aspects of traditional finance within the DeFi ecosystem.

As the ecosystem matured, innovative protocols began developing more nuanced approaches to credit assessment that considered factors beyond simple collateral ratios. Projects like Aave introduced concepts like credit delegation and flash loans that demonstrated the potential for more sophisticated risk assessment mechanisms, while protocols like TrueFi began experimenting with uncollateralized lending based on reputation and on-chain behavior analysis.

The emergence of identity protocols and reputation systems marked a significant milestone in the development of DeFi credit infrastructure. Platforms like Gitcoin Passport, BrightID, and various soul-bound token implementations created ways to establish persistent digital identities that could accumulate reputation across multiple protocols and applications, laying the groundwork for more comprehensive credit scoring systems.

Cross-chain interoperability has further enhanced the sophistication of on-chain credit systems by enabling the aggregation of behavioral data from multiple blockchain networks. Modern credit scoring systems can now analyze user behavior across Ethereum, Polygon, Arbitrum, Optimism, and other networks to create comprehensive credit profiles that capture the full scope of a user’s DeFi activities and financial behavior.

Technical Infrastructure and Scoring Methodologies

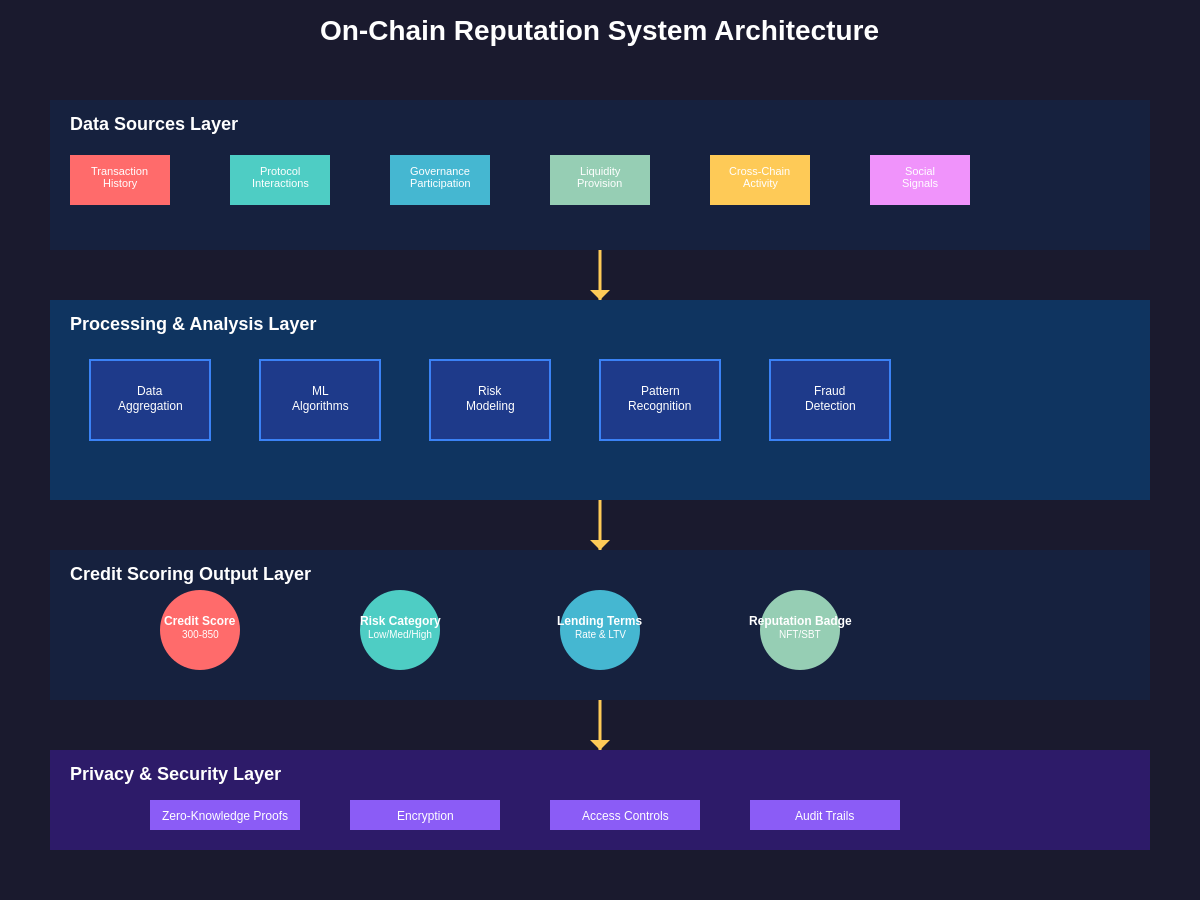

The technical infrastructure underlying on-chain credit scoring systems represents a sophisticated blend of blockchain data analysis, machine learning algorithms, and financial modeling techniques that work together to create comprehensive and dynamic credit assessments. These systems must process vast amounts of blockchain data in real-time while maintaining accuracy, fairness, and resistance to manipulation attempts.

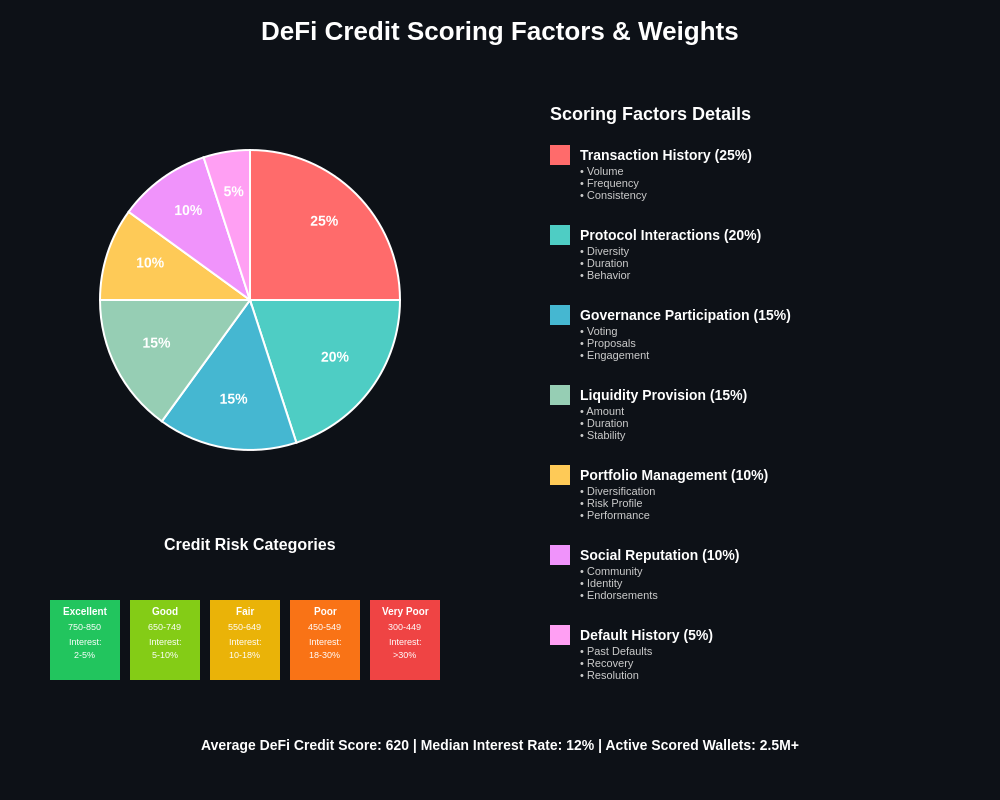

Data aggregation forms the foundation of on-chain credit scoring, with systems collecting and analyzing information from multiple sources including transaction histories, protocol interactions, governance participation, liquidity provision patterns, and cross-protocol behavior. Advanced scoring systems can process millions of transactions and interactions to identify patterns and behaviors that correlate with creditworthiness and default risk.

Machine learning algorithms play a crucial role in identifying subtle patterns and relationships within blockchain data that might not be apparent through traditional analysis methods. These algorithms can detect complex behavioral patterns, identify potential fraud or manipulation attempts, and continuously adapt their scoring models based on new data and changing market conditions. Natural language processing techniques are increasingly being used to analyze governance proposal participation and community engagement as additional indicators of user commitment and reliability.

Risk modeling in DeFi credit systems must account for the unique characteristics of cryptocurrency markets, including high volatility, correlation risks, and the potential for smart contract failures or protocol exploits. Sophisticated models incorporate factors such as portfolio diversification metrics available through TradingView analysis, liquidity risk assessments, and exposure to various DeFi protocols to create comprehensive risk profiles for individual borrowers.

Real-time updating capabilities distinguish on-chain credit systems from traditional credit bureaus, which typically update information monthly or quarterly. Blockchain-based systems can monitor borrower behavior continuously and adjust credit scores in real-time based on new transactions, changing market conditions, or evolving risk factors, enabling more dynamic and responsive lending decisions.

Privacy-preserving techniques are increasingly important in on-chain credit systems, with technologies like zero-knowledge proofs enabling the verification of creditworthiness without revealing sensitive personal or financial information. These techniques allow users to prove their creditworthiness while maintaining privacy and preventing potential discrimination or targeting based on financial status.

Major Protocols and Platforms

The landscape of DeFi credit scoring and reputation systems includes numerous innovative platforms, each taking unique approaches to solving the challenges of decentralized credit assessment. These platforms range from comprehensive credit scoring services to specialized reputation systems focused on specific aspects of DeFi behavior and interaction patterns.

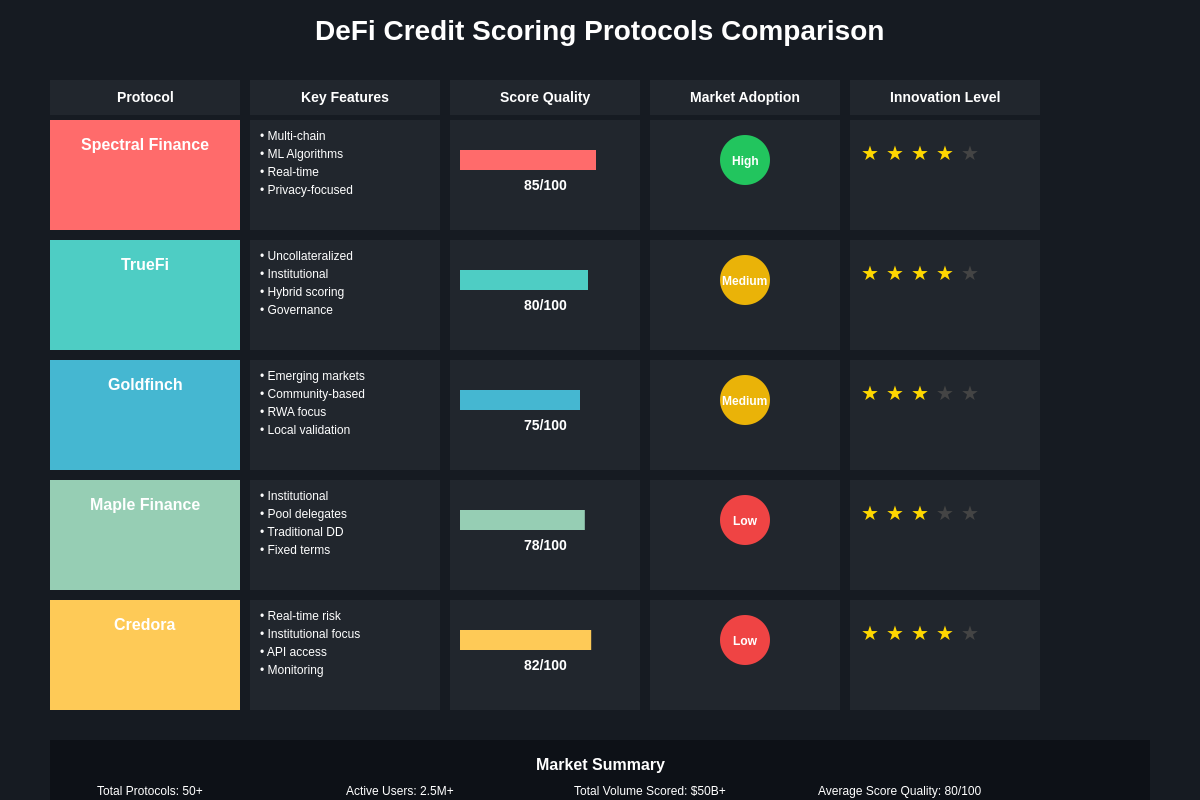

Spectral Finance has emerged as one of the leading platforms in the on-chain credit scoring space, developing sophisticated algorithms that analyze wallet behavior across multiple dimensions to create comprehensive credit scores. Their system evaluates factors including transaction frequency and consistency, portfolio composition and diversification, protocol interaction patterns, and governance participation to generate scores that reflect both financial capacity and behavioral reliability.

TrueFi represents another significant innovation in uncollateralized DeFi lending, utilizing a combination of on-chain reputation systems and off-chain due diligence to enable lending without traditional collateral requirements. Their approach incorporates both quantitative on-chain analysis and qualitative assessment of borrower credentials and business models, creating a hybrid system that bridges traditional finance and DeFi methodologies.

Goldfinch has developed a unique approach to DeFi credit that combines on-chain reputation with real-world asset backing and community-based risk assessment. Their system enables lending to borrowers in emerging markets by incorporating local knowledge and community validation alongside traditional on-chain behavioral analysis, demonstrating how reputation systems can be adapted for different geographical and economic contexts.

Maple Finance focuses on institutional DeFi lending with sophisticated credit assessment mechanisms that combine on-chain behavior analysis with traditional institutional due diligence processes. Their platform demonstrates how on-chain reputation systems can be integrated with existing financial infrastructure to serve professional investors and institutional borrowers while maintaining the transparency and efficiency benefits of blockchain technology.

Credora has developed specialized credit scoring systems focused on institutional cryptocurrency trading and lending activities. Their platform provides real-time risk monitoring and credit assessment services that enable more sophisticated lending relationships between institutional participants in the cryptocurrency markets, showcasing how on-chain reputation systems can evolve to serve professional market participants.

The Ethereum Name Service (ENS) and similar domain systems have become important components of DeFi reputation, with premium domain ownership and long-term registration patterns serving as signals of user commitment and financial capacity. Many credit scoring systems now incorporate ENS ownership and registration history as factors in their assessment algorithms.

Privacy Considerations and Identity Management

Privacy represents one of the most critical challenges in developing effective on-chain credit scoring systems, as these platforms must balance the need for comprehensive behavioral analysis with users’ rights to financial privacy and protection from potential discrimination or targeting. The public nature of blockchain transactions creates both opportunities and risks for credit assessment systems that must be carefully managed through technological and governance mechanisms.

Zero-knowledge proof systems offer promising solutions for privacy-preserving credit scoring by enabling users to prove their creditworthiness without revealing specific transaction details or sensitive financial information. These systems can verify that a user meets certain criteria or thresholds without disclosing the underlying data, enabling credit assessment while protecting individual privacy and preventing potential misuse of financial information.

Selective disclosure mechanisms allow users to control which aspects of their financial history are shared with potential lenders or credit scoring systems, enabling more granular privacy controls while still providing sufficient information for accurate credit assessment. These systems can enable users to prove specific qualifications or experiences without revealing their complete financial history.

Identity fragmentation represents both a challenge and an opportunity in DeFi credit systems, as users often maintain multiple wallet addresses for different purposes or security reasons. Advanced reputation systems must develop mechanisms for linking related addresses while respecting users’ desires for privacy and security, potentially using techniques like cryptographic proofs or voluntary identity linkage.

The emergence of soul-bound tokens and non-transferable reputation credentials offers new approaches to identity management in DeFi credit systems. These technologies can create persistent reputation records that cannot be easily manipulated or transferred, while still allowing users to maintain privacy and control over their personal information and financial data.

Regulatory compliance requirements in various jurisdictions add additional complexity to privacy management in on-chain credit systems, as platforms must balance privacy protection with potential know-your-customer (KYC) and anti-money laundering (AML) requirements. The development of privacy-preserving compliance solutions will be crucial for the continued growth and adoption of DeFi credit systems.

Risk Assessment and Default Prediction Models

The development of effective risk assessment and default prediction models for DeFi lending represents a complex challenge that requires understanding both traditional financial risk factors and the unique characteristics of decentralized finance ecosystems. These models must account for cryptocurrency market volatility, smart contract risks, regulatory uncertainties, and behavioral patterns that may differ significantly from traditional borrowing contexts.

Traditional credit risk models rely heavily on historical payment data and employment stability, factors that may not be directly applicable or available in DeFi contexts. On-chain risk models must instead focus on cryptocurrency-specific indicators such as portfolio volatility, exposure to various DeFi protocols, transaction pattern analysis, and correlation with broader cryptocurrency market movements to assess borrower risk profiles.

Behavioral analysis plays a crucial role in DeFi risk assessment, with models analyzing patterns such as liquidity provision consistency, governance participation levels, reaction to market volatility, and adherence to protocol rules and community standards. These behavioral indicators can provide insights into borrower reliability and decision-making capabilities that may be predictive of future default risk.

Machine learning techniques are particularly valuable in DeFi risk modeling due to the complexity and multidimensional nature of on-chain data. Advanced models can identify subtle patterns and correlations within blockchain data that might not be apparent through traditional statistical analysis, continuously improving their predictive accuracy as they process more historical data and observe actual default outcomes.

Market risk modeling in DeFi must account for the high correlation between different cryptocurrency assets and the potential for rapid market downturns that can affect multiple borrowers simultaneously. Sophisticated models incorporate real-time market analysis tools from TradingView and other platforms to assess current market conditions and adjust risk assessments accordingly.

Stress testing and scenario analysis are essential components of DeFi risk models, given the relatively short history of cryptocurrency markets and the potential for unprecedented events or market conditions. These models must consider scenarios including extreme market volatility, protocol failures, regulatory changes, and other systemic risks that could affect borrower ability to repay loans.

Regulatory Landscape and Compliance Challenges

The regulatory environment surrounding DeFi credit scoring and on-chain reputation systems remains complex and rapidly evolving, with different jurisdictions taking varying approaches to the oversight and regulation of decentralized finance activities. These regulatory uncertainties create significant challenges for developers and operators of credit scoring systems while also creating opportunities for innovation in compliance technology and privacy-preserving verification methods.

Traditional financial regulations, including fair lending laws, data protection requirements, and consumer protection statutes, may apply to DeFi credit systems depending on their structure and operation. The challenge lies in adapting these regulations, which were designed for centralized financial institutions, to decentralized systems that may not have traditional corporate structures or centralized control mechanisms.

Data protection regulations such as the General Data Protection Regulation (GDPR) in Europe and similar laws in other jurisdictions create particular challenges for blockchain-based credit systems, given the immutable nature of blockchain data and the global, decentralized nature of these systems. Compliance solutions must balance regulatory requirements with the technical realities of blockchain technology and the privacy expectations of users.

Anti-discrimination laws present another area of regulatory complexity, as credit scoring algorithms must be designed to avoid unfair discrimination based on protected characteristics while still providing accurate risk assessments. The challenge is particularly acute in on-chain systems where certain behavioral patterns might correlate with protected characteristics, requiring careful algorithm design and ongoing monitoring to ensure compliance.

The emergence of regulatory sandboxes and innovation hubs in various jurisdictions provides opportunities for DeFi credit platforms to work with regulators to develop appropriate oversight frameworks while continuing to innovate and serve users. These collaborative approaches may help establish clearer regulatory guidelines while preserving the benefits of decentralized finance innovation.

International coordination and regulatory harmonization efforts are becoming increasingly important as DeFi protocols operate across multiple jurisdictions simultaneously. The development of common standards and frameworks for DeFi regulation could help reduce compliance complexity while ensuring appropriate consumer protection and systemic risk management.

Advantages and Limitations of On-Chain Credit Systems

On-chain credit scoring systems offer numerous advantages over traditional credit assessment methods, including enhanced transparency, global accessibility, real-time updating, and resistance to institutional bias. However, these systems also face significant limitations and challenges that must be addressed for widespread adoption and effectiveness in serving diverse user populations and use cases.

The transparency of blockchain technology represents one of the most significant advantages of on-chain credit systems, enabling borrowers and lenders to access the same information and verify the accuracy of credit assessments independently. This transparency can help build trust and confidence in the credit assessment process while reducing the information advantages that traditional financial institutions have historically maintained over individual borrowers.

Global accessibility is another major advantage, as on-chain credit systems can potentially serve users worldwide without requiring relationships with local financial institutions or compliance with numerous different national credit reporting systems. This accessibility could significantly expand access to credit for underserved populations, particularly in developing countries where traditional credit infrastructure may be limited or unreliable.

Real-time data processing and score updating enable more dynamic and responsive credit assessment compared to traditional systems that may update information monthly or quarterly. This capability allows lenders to make more informed decisions based on current borrower behavior and market conditions, potentially reducing default risk and enabling more efficient capital allocation.

However, on-chain credit systems also face significant limitations, including limited transaction history for many users, vulnerability to manipulation through wash trading or artificial transaction generation, and potential privacy concerns related to the public nature of blockchain data. The relatively short history of DeFi protocols also limits the availability of long-term behavioral data that traditional credit systems rely upon for accurate risk assessment.

Technical challenges include scalability limitations, cross-chain data integration complexity, and the need for sophisticated algorithms to distinguish between legitimate behavior and manipulation attempts. These technical hurdles require ongoing innovation and development to create robust and reliable credit scoring systems that can serve large user populations effectively.

The volatility and correlation risks inherent in cryptocurrency markets create additional challenges for credit assessment, as traditional risk models may not adequately account for the unique characteristics of digital asset portfolios and the potential for rapid value changes that can affect borrower financial positions.

Use Cases and Applications Across DeFi Protocols

On-chain credit scoring systems have found applications across a wide range of DeFi protocols and use cases, from traditional lending and borrowing platforms to more innovative applications including insurance, derivatives trading, and governance participation. These diverse applications demonstrate the versatility and potential of reputation-based systems in creating more efficient and inclusive financial infrastructure.

Lending protocols represent the most obvious application for on-chain credit scoring, with platforms using reputation systems to enable undercollateralized or uncollateralized lending based on borrower behavior and history. These applications can significantly improve capital efficiency compared to traditional over-collateralized DeFi lending while still maintaining acceptable risk levels for lenders.

Insurance protocols are increasingly incorporating reputation systems to assess claim validity and prevent fraud, using on-chain behavior analysis to evaluate the credibility of insurance claims and the reliability of insurance providers. These applications can help reduce insurance premiums and improve the efficiency of decentralized insurance markets by better aligning risk pricing with actual risk levels.

Governance systems benefit from reputation scoring by enabling more informed voting and proposal evaluation, with reputation scores helping to identify participants who have demonstrated commitment to protocol success and community welfare. These applications can improve governance outcomes by highlighting the input of experienced and committed community members while reducing the influence of potential bad actors.

Trading and derivatives platforms can use credit scoring to enable more sophisticated trading strategies including margin trading, options writing, and other activities that require assessment of counterparty risk. Advanced trading platforms integrated with TradingView can leverage reputation data to provide more personalized trading experiences and risk management tools for their users.

Cross-protocol applications are emerging that aggregate reputation data from multiple DeFi protocols to create comprehensive user profiles that can be used across the entire ecosystem. These applications can help users build portable reputation that follows them across different platforms and protocols, creating incentives for consistent good behavior and long-term ecosystem participation.

Future Developments and Technological Innovations

The future of on-chain credit scoring and reputation systems promises significant technological innovations and developments that could further enhance the accuracy, privacy, and utility of these systems. These advances will likely focus on improving data analysis capabilities, enhancing privacy protection, and expanding the scope and sophistication of credit assessment methodologies.

Artificial intelligence and machine learning technologies are expected to play increasingly important roles in on-chain credit scoring, with advanced algorithms capable of identifying complex patterns and relationships within blockchain data that current systems may miss. These technologies could enable more accurate prediction of default risk and more sophisticated behavioral analysis while adapting to changing market conditions and user behavior patterns.

Cross-chain data integration and analysis will become increasingly sophisticated as interoperability protocols mature and enable seamless data sharing between different blockchain networks. Future credit scoring systems may be able to analyze user behavior across dozens of different blockchain networks and protocols to create truly comprehensive reputation profiles.

Privacy-preserving technologies including advanced zero-knowledge proof systems, homomorphic encryption, and secure multi-party computation will likely enable more sophisticated privacy protection while still allowing for comprehensive credit assessment. These technologies could resolve many of the current tensions between privacy protection and effective credit scoring.

Integration with real-world data sources could enhance the accuracy and completeness of on-chain credit systems by incorporating information from traditional financial systems, social media platforms, professional networks, and other data sources. However, such integration must be carefully managed to protect user privacy and prevent potential discrimination or bias.

Standardization efforts across the DeFi ecosystem may lead to common credit scoring standards and methodologies that enable better interoperability and portability of reputation data across different protocols and platforms. These standards could help create more efficient and user-friendly credit ecosystems while maintaining innovation and competition among different scoring providers.

Economic Impact and Market Implications

The development and adoption of sophisticated on-chain credit scoring systems has significant implications for the broader DeFi ecosystem and cryptocurrency markets, potentially affecting everything from lending interest rates to protocol adoption patterns and overall market efficiency. These economic impacts extend beyond individual protocols to influence the entire decentralized finance landscape and its relationship with traditional financial systems.

Capital efficiency improvements represent one of the most direct economic impacts of advanced credit scoring systems, as these technologies enable lending protocols to offer higher loan-to-value ratios and lower collateral requirements for borrowers with strong on-chain reputations. This improved efficiency can lead to lower borrowing costs and higher yields for lenders while expanding access to capital for creditworthy borrowers who may lack substantial cryptocurrency holdings.

Market segmentation based on credit scores could lead to more sophisticated and efficient pricing of lending services, with different interest rates and terms offered to borrowers based on their assessed risk levels. This segmentation could help attract more risk-averse institutional investors to DeFi lending while still serving higher-risk borrowers at appropriate risk-adjusted rates.

The emergence of reputation-based systems could accelerate institutional adoption of DeFi protocols by providing the risk assessment and due diligence tools that institutional investors require for regulatory compliance and internal risk management. Professional investors increasingly rely on sophisticated market analysis tools like those available on TradingView to make informed investment decisions, and similar analytical rigor applied to credit assessment could drive greater institutional participation.

Competition among credit scoring providers could lead to continuous innovation and improvement in scoring methodologies, potentially creating a dynamic ecosystem of reputation systems that compete on accuracy, privacy protection, and user experience. This competition could benefit users through better service quality and more choices in how their creditworthiness is assessed and presented to potential lenders.

The development of credit derivatives and insurance products based on on-chain reputation scores could create new markets and opportunities for risk management and speculation. These products could enable lenders to hedge their credit risk more effectively while creating new investment opportunities for sophisticated traders and institutional investors.

Integration with Traditional Financial Systems

The integration of on-chain credit scoring systems with traditional financial infrastructure represents both a significant opportunity and a complex challenge, as these systems must bridge the gap between decentralized, blockchain-based data and the established processes and requirements of traditional financial institutions. This integration could significantly expand the utility and adoption of on-chain reputation systems while creating new opportunities for financial inclusion and innovation.

Traditional banks and financial institutions are beginning to explore how on-chain reputation data might supplement or enhance their existing credit assessment processes, particularly for customers who are active in cryptocurrency markets or seeking loans secured by digital assets. This integration could provide more comprehensive risk assessment by incorporating data sources that traditional systems cannot access while maintaining compliance with existing regulatory requirements.

Credit reporting agencies are investigating how blockchain data and on-chain reputation scores might be incorporated into traditional credit reports, potentially creating hybrid scoring systems that combine the best aspects of both traditional and blockchain-based credit assessment. Such integration could help bridge the gap between DeFi and traditional finance while providing users with more comprehensive and accurate credit profiles.

Regulatory compliance requirements for traditional financial institutions create both challenges and opportunities for on-chain credit system integration, as these institutions must ensure that any blockchain-based data sources meet appropriate standards for accuracy, fairness, and privacy protection. The development of compliant integration methods could help accelerate adoption of on-chain reputation data in traditional finance.

Cross-system identity verification and data portability represent key technical challenges for integration, as traditional financial systems typically rely on different identity verification Methods and data formats than blockchain-based systems. The development of standardized protocols and interfaces could help facilitate smoother integration while protecting user privacy and maintaining data accuracy.

The potential for on-chain reputation systems to serve unbanked and underbanked populations could create significant opportunities for financial institutions seeking to expand their customer base and serve new markets. These systems could enable traditional lenders to assess the creditworthiness of individuals who lack traditional credit histories but have demonstrated financial responsibility through their on-chain behavior.

Case Studies and Real-World Implementations

Examining real-world implementations and case studies of on-chain credit scoring systems provides valuable insights into the practical challenges and successes of these technologies, demonstrating how theoretical concepts translate into working systems that serve actual users and create measurable value within the DeFi ecosystem.

TrueFi’s implementation of uncollateralized lending represents one of the most successful applications of on-chain reputation systems in practice, with the platform successfully facilitating millions of dollars in uncollateralized loans based on borrower reputation and on-chain behavior analysis. Their approach combines quantitative on-chain metrics with qualitative assessment of borrower credentials, creating a hybrid system that has achieved relatively low default rates while serving institutional and high-net-worth individual borrowers.

Spectral Finance has developed sophisticated machine learning algorithms that analyze wallet behavior across multiple dimensions to create comprehensive credit scores, with their system demonstrating the ability to identify patterns and behaviors that correlate with creditworthiness and default risk. Their platform has processed millions of wallet addresses and transactions to create one of the most comprehensive databases of on-chain credit information available in the DeFi ecosystem.

Goldfinch’s focus on emerging market lending demonstrates how on-chain reputation systems can be adapted for different geographical and economic contexts, with their platform successfully facilitating loans to borrowers in countries where traditional credit infrastructure may be limited or unreliable. Their approach combines on-chain behavioral analysis with local knowledge and community validation to create effective credit assessment mechanisms for underserved markets.

The integration of reputation scoring into governance systems has been demonstrated by numerous protocols including Compound, Aave, and MakerDAO, where participation in governance activities and voting history are increasingly being used as indicators of community commitment and reliability. These implementations show how reputation systems can enhance democratic participation and decision-making within decentralized protocols.

Cross-protocol reputation aggregation has been successfully implemented by platforms like DegenScore and Gitcoin Passport, which collect and analyze user behavior across multiple protocols to create comprehensive reputation profiles. These implementations demonstrate the feasibility of creating portable reputation that follows users across the entire DeFi ecosystem while maintaining privacy and user control over personal data.

Challenges and Future Research Directions

The continued development and improvement of on-chain credit scoring systems faces numerous challenges that require ongoing research and innovation to address effectively. These challenges span technical, economic, social, and regulatory domains, requiring interdisciplinary approaches and collaboration between different stakeholders in the DeFi ecosystem.

Algorithm bias and fairness represent significant ongoing challenges, as credit scoring algorithms must be designed to avoid unfair discrimination while still providing accurate risk assessments. Research into algorithmic fairness and bias detection will be crucial for ensuring that on-chain credit systems serve all users equitably and comply with anti-discrimination laws and ethical standards.

Data quality and manipulation resistance require continuous research and development, as malicious actors may attempt to game credit scoring systems through wash trading, Sybil attacks, or other manipulation techniques. Advanced detection methods and robust algorithm design will be essential for maintaining the integrity and accuracy of reputation-based credit systems.

Privacy preservation while maintaining scoring accuracy presents an ongoing technical challenge that requires research into advanced cryptographic techniques and privacy-preserving computation methods. The development of practical solutions that protect user privacy without sacrificing the effectiveness of credit assessment will be crucial for widespread adoption.

Scalability and cross-chain integration challenges require research into efficient data processing and analysis techniques that can handle the growing volume of blockchain data while providing real-time credit scoring services. The development of scalable infrastructure and efficient algorithms will be essential for serving large user populations across multiple blockchain networks.

Regulatory compliance and legal framework development require ongoing collaboration between technologists, legal experts, and regulators to create appropriate oversight mechanisms that protect consumers while preserving innovation and the benefits of decentralized finance. Research into regulatory technology and compliance automation will be important for enabling compliant operations at scale.

The long-term sustainability and incentive alignment of reputation systems require economic research and modeling to ensure that these systems continue to function effectively as they scale and mature. Understanding the economic dynamics and incentive structures that drive user behavior and system performance will be crucial for designing sustainable and effective credit scoring ecosystems.

Conclusion and Future Outlook

On-chain credit scoring and reputation systems represent a transformative innovation in financial infrastructure that has the potential to democratize access to credit while creating more efficient and transparent lending markets. These systems leverage the unique properties of blockchain technology to create new approaches to credit assessment that can serve users worldwide without requiring traditional financial intermediaries or infrastructure.

The development of sophisticated on-chain credit scoring systems has already demonstrated significant progress in addressing the challenges of decentralized finance, with successful implementations showing that reputation-based lending can achieve acceptable risk levels while serving borrowers who might be excluded from traditional financial systems. The continued evolution of these systems promises even greater capabilities and applications as the underlying technology matures and adoption increases.

However, significant challenges remain in areas including privacy protection, algorithm fairness, regulatory compliance, and technical scalability. Addressing these challenges will require continued innovation, research, and collaboration between different stakeholders in the DeFi ecosystem, including developers, users, regulators, and traditional financial institutions.

The future of on-chain credit scoring systems appears bright, with numerous technological innovations and market developments pointing toward continued growth and improvement in these systems’ capabilities and adoption. The integration of artificial intelligence, privacy-preserving technologies, and cross-chain interoperability promises to create even more sophisticated and useful credit assessment tools.

As these systems continue to evolve and mature, they may fundamentally reshape how we think about credit assessment and financial inclusion, creating new opportunities for individuals and businesses worldwide to access capital and participate in the global financial system. The success of these systems will ultimately depend on their ability to balance innovation with responsibility, creating inclusive and fair access to credit while maintaining the security and reliability that users and regulators expect from financial infrastructure.

The journey toward fully mature and widely adopted on-chain credit scoring systems is still in its early stages, but the progress made to date suggests that these technologies will play an increasingly important role in the future of finance, both within the DeFi ecosystem and in the broader financial industry.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments and DeFi protocols involve significant risks, including the potential loss of principal. Past performance does not guarantee future results. Readers should conduct their own research and consult with qualified financial advisors before making investment decisions. The author and publisher are not responsible for any financial losses that may result from the use of information contained in this article. DeFi protocols and on-chain credit systems are experimental technologies that may contain bugs, vulnerabilities, or other risks that could result in financial losses.