The Critical Need for DeFi Protection

The decentralized finance ecosystem has revolutionized how individuals interact with financial services, eliminating traditional intermediaries and providing unprecedented access to lending, borrowing, trading, and yield farming opportunities. However, this innovation comes with significant risks that traditional financial systems have spent decades learning to manage and mitigate. The absence of centralized oversight and the experimental nature of many DeFi protocols create unique vulnerabilities that can result in catastrophic losses for users who fail to adequately protect their digital assets.

Smart contract vulnerabilities represent one of the most significant threats in the DeFi space, with billions of dollars lost to exploits, bugs, and design flaws in protocol code. Unlike traditional financial systems where human oversight can halt suspicious transactions or reverse fraudulent activities, smart contracts execute automatically and irreversibly, making any flaws in their code potentially devastating for users. The complexity of modern DeFi protocols, which often interact with multiple other protocols and rely on intricate economic mechanisms, creates numerous attack surfaces that malicious actors continuously seek to exploit.

The rapid pace of DeFi innovation has led to a situation where new protocols are regularly launched with limited security audits or battle-testing, creating an environment where users must constantly evaluate the risk-reward tradeoffs of participating in experimental financial systems. Traditional financial institutions spend years developing and testing new products before public release, while DeFi protocols often launch with minimal testing and evolve rapidly based on community feedback and market conditions.

Market volatility presents another layer of risk for DeFi participants, as the cryptocurrency markets that underpin these systems can experience extreme price movements that liquidate positions, trigger cascade effects across interconnected protocols, and create scenarios where users lose more than their initial investments. The interconnected nature of DeFi means that problems in one protocol can quickly spread to others, creating systemic risks that individual users may struggle to anticipate or protect against.

Understanding DeFi Insurance Fundamentals

DeFi insurance represents a new paradigm for protecting digital assets that operates entirely on blockchain networks without relying on traditional insurance companies or centralized authorities. These systems use smart contracts, community governance, and cryptocurrency-based economic incentives to create protection mechanisms that can compensate users for losses resulting from smart contract failures, protocol exploits, and other covered risks.

The fundamental principle underlying DeFi insurance is the creation of risk pools funded by community contributions, where participants can purchase coverage for specific risks in exchange for premium payments denominated in cryptocurrency. These systems operate transparently on public blockchains, allowing anyone to verify the solvency of insurance pools, review claims processes, and participate in governance decisions that determine how the protocols evolve over time.

Coverage mechanisms in DeFi insurance typically focus on technical risks specific to blockchain-based financial systems, including smart contract bugs, governance attacks, oracle failures, and protocol-specific risks like impermanent loss in liquidity provision. Unlike traditional insurance that covers a broad range of risks including natural disasters, theft, and human error, DeFi insurance is specifically designed to address the unique technological and economic risks inherent in decentralized financial systems.

The claims process in DeFi insurance protocols is typically governed by community voting mechanisms where token holders review submitted claims and determine whether they meet the criteria for compensation. This decentralized approach to claims assessment eliminates the need for traditional insurance adjusters while creating new challenges around expertise, objectivity, and potential conflicts of interest among voting participants.

Risk assessment in DeFi insurance relies heavily on technical analysis of smart contract code, historical data about protocol performance, and community evaluation of development teams and security practices. This approach requires participants to develop technical expertise that goes far beyond what traditional insurance customers need, creating barriers to entry for less technically sophisticated users while potentially providing more accurate risk pricing for those who can effectively analyze the underlying technologies.

Major DeFi Insurance Protocols and Platforms

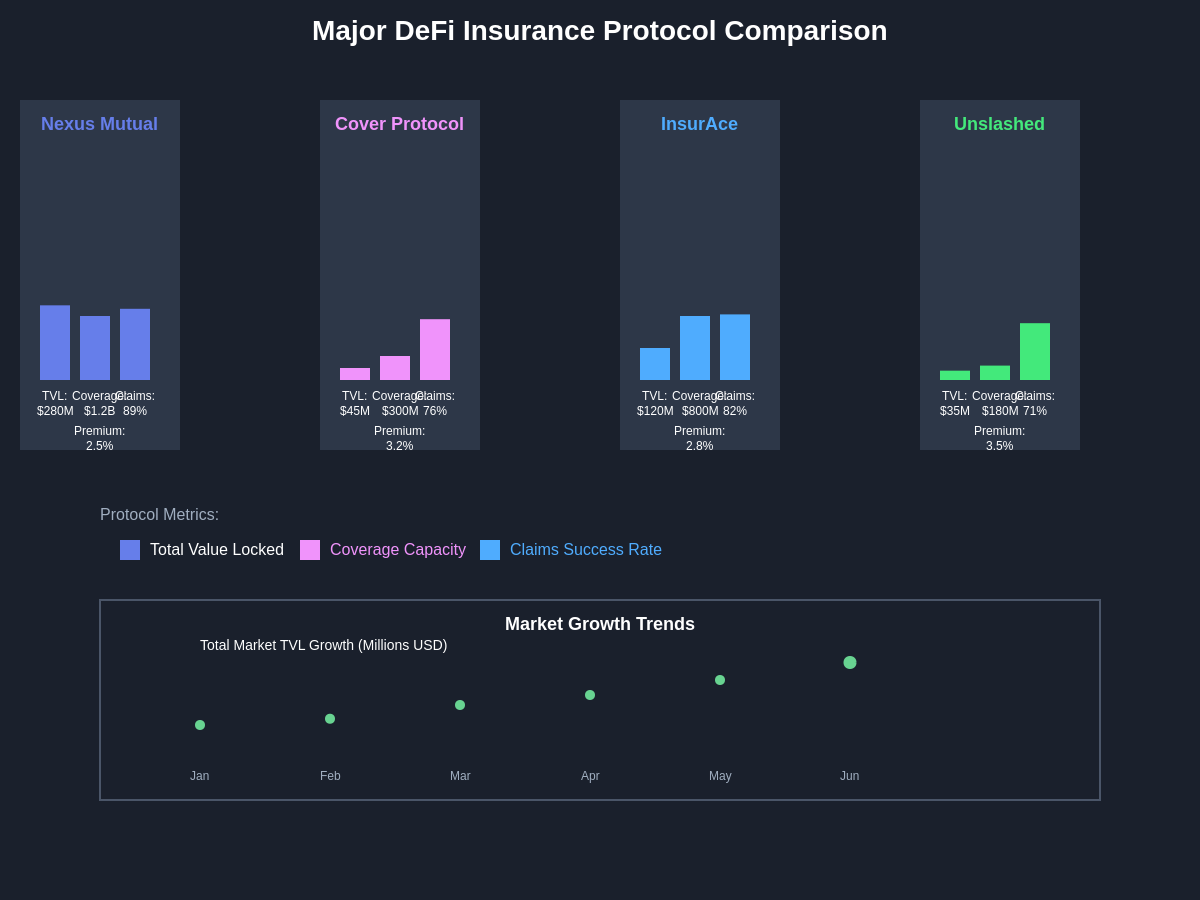

Nexus Mutual stands as one of the pioneering protocols in the DeFi insurance space, operating as a discretionary mutual where members pool funds to provide coverage against smart contract failures and other technical risks. The protocol uses a unique membership structure where users must hold NXM tokens to participate, creating alignment between coverage providers and recipients while enabling community governance of coverage decisions and risk assessment processes.

The platform’s approach to risk assessment involves detailed technical analysis of smart contract code, evaluation of development team credentials, and ongoing monitoring of protocol performance to adjust coverage terms and pricing. Members who stake NXM tokens to provide coverage for specific protocols receive rewards based on the premiums collected, while also bearing the risk of potential claims that could reduce their staked amounts.

Cover Protocol represents another significant player in the DeFi insurance ecosystem, operating through a peer-to-peer marketplace model where coverage providers can offer protection for specific protocols and coverage seekers can purchase the protection that best meets their needs. This marketplace approach allows for more dynamic pricing based on supply and demand while enabling specialization among coverage providers who may focus on particular types of risks or protocols.

The protocol’s use of fungible coverage tokens creates a secondary market for insurance positions, allowing coverage providers to exit their positions before expiration and enabling more sophisticated trading strategies around insurance coverage. This innovation addresses one of the traditional limitations of insurance products by providing liquidity to coverage providers who might otherwise be locked into positions for extended periods.

InsurAce represents a more recent entrant that focuses on providing comprehensive coverage across multiple blockchain networks and DeFi protocols while emphasizing user experience and accessibility for less technical users. The platform offers simplified coverage options that bundle multiple types of protection, making it easier for average users to obtain appropriate coverage without needing to understand the technical details of specific risk types.

The protocol’s multi-chain approach recognizes that modern DeFi users often interact with protocols across multiple blockchain networks, creating complex risk profiles that single-chain insurance solutions may not adequately address. By providing unified coverage across different networks, InsurAce simplifies the insurance process for users while creating economies of scale that can reduce overall premium costs.

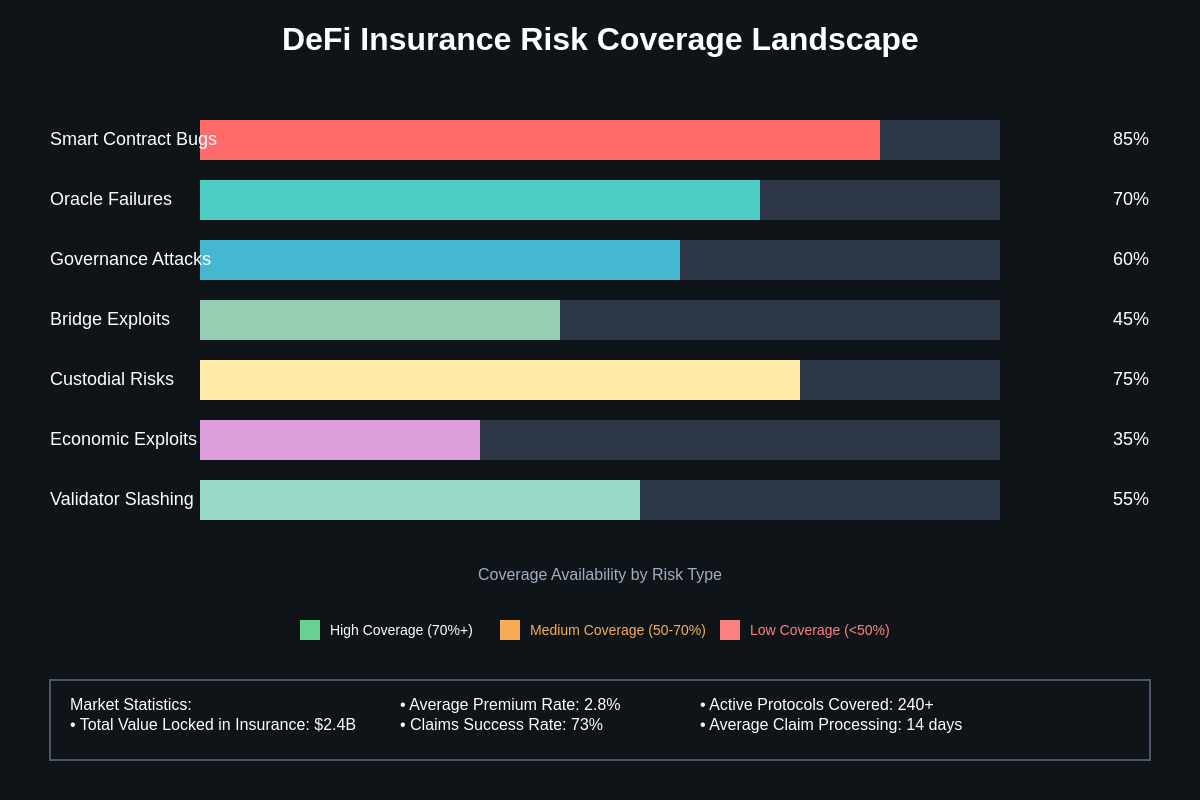

Risk Types and Coverage Options

Smart contract risk represents the most fundamental type of coverage offered by DeFi insurance protocols, protecting users against losses resulting from bugs, exploits, or design flaws in protocol code that result in permanent loss of funds. This coverage typically excludes losses resulting from user error, market volatility, or intentional actions by protocol developers, focusing specifically on technical failures that prevent users from withdrawing their legitimately deposited assets.

The complexity of determining smart contract risk coverage lies in the difficulty of distinguishing between legitimate technical failures and intended protocol behavior that users may not have fully understood. Modern DeFi protocols often implement complex economic mechanisms that can result in user losses under certain market conditions, creating gray areas where it may be unclear whether a loss represents a covered technical failure or an uncovered economic risk.

Oracle failure coverage addresses risks associated with external data feeds that many DeFi protocols rely on for price information, market data, and other external inputs crucial to their operation. When oracles provide incorrect information, either due to technical failures or manipulation, the resulting losses can be substantial as protocols make decisions based on false data that triggers liquidations, enables arbitrage opportunities, or causes other unintended consequences.

The challenge in oracle risk coverage lies in determining when oracle behavior represents a failure versus normal market volatility or temporary data inconsistencies that sophisticated users should expect and plan for. Different oracle systems have varying degrees of reliability and different approaches to handling edge cases, making it difficult to create standardized coverage terms that apply across different protocols and oracle providers.

Governance attack coverage protects against losses resulting from malicious actions by protocol governance participants who use their voting power to make changes that benefit themselves at the expense of other users. These attacks can be particularly devastating because they may be technically legitimate according to protocol governance rules while still representing a fundamental betrayal of user expectations about how the protocol will operate.

The assessment of governance attack claims requires careful analysis of the intent behind governance decisions, the process by which they were implemented, and the impact on different user groups. This type of coverage raises complex questions about the nature of decentralized governance and the extent to which minority stakeholders should be protected against majority decisions that harm their interests.

Custodial risk coverage addresses situations where DeFi protocols interact with centralized entities or custodial services that may fail, be compromised, or act maliciously, resulting in user losses. While pure DeFi protocols avoid centralized dependencies, many practical DeFi applications include centralized components for user experience, regulatory compliance, or technical limitations, creating potential points of failure that insurance can address.

Technical Architecture and Smart Contract Security

The technical architecture underlying DeFi insurance protocols must balance multiple competing requirements including security, transparency, efficiency, and flexibility while operating in an environment where smart contract bugs can result in total loss of funds. These systems typically implement multi-layered security approaches that include formal verification of critical contract logic, extensive testing procedures, and gradual rollout strategies that limit exposure during initial deployment phases.

Risk pool management represents one of the most critical technical challenges for DeFi insurance protocols, as these systems must maintain sufficient liquidity to pay claims while providing reasonable returns to coverage providers and avoiding the concentration risks that could result in system-wide failures. Advanced protocols implement sophisticated algorithms for risk pool allocation, coverage pricing, and reserves management that adapt to changing market conditions and claim experience.

The use of oracles in DeFi insurance creates both opportunities and vulnerabilities, as these systems often need external data to verify claims, assess risks, and trigger automated payouts. However, the same oracle dependencies that enable automated insurance operations also create potential attack vectors where malicious actors might manipulate data feeds to trigger false claims or prevent legitimate claims from being processed.

Governance mechanisms in DeFi insurance protocols must be carefully designed to prevent capture by malicious actors while ensuring that legitimate claims are processed efficiently and fairly. Many protocols implement multi-stage governance processes with different voting mechanisms for different types of decisions, time delays that allow community review of proposed changes, and emergency procedures that can halt operations if critical vulnerabilities are discovered.

Interoperability with other DeFi protocols creates additional technical complexity as insurance systems must integrate with the ever-evolving landscape of decentralized financial services while maintaining security and reliability. This requires careful API design, robust error handling, and contingency plans for situations where integrated protocols undergo breaking changes or cease operations entirely.

Economic Models and Tokenomics

The economic sustainability of DeFi insurance protocols depends on carefully balanced tokenomics that align incentives among coverage providers, coverage purchasers, and protocol governance participants while generating sufficient revenue to cover operational costs and maintain adequate reserves for claim payments. These systems must navigate the challenge of providing competitive coverage pricing while maintaining the financial stability necessary to honor long-term commitments to policyholders.

Premium pricing in DeFi insurance typically uses algorithmic models that consider factors including protocol risk assessments, historical claim data, current market conditions, and supply-demand dynamics in coverage markets. However, the limited historical data available for many DeFi protocols creates challenges in risk pricing that traditional insurance companies do not face, leading to pricing models that may be inaccurate during market stress periods or as protocols evolve.

Token incentive structures play crucial roles in encouraging participation in DeFi insurance ecosystems, with many protocols offering governance tokens to coverage providers, claims assessors, and long-term participants. These incentive systems must be carefully calibrated to avoid creating perverse incentives where participants benefit from protocol failures or where short-term rewards encourage excessive risk-taking that threatens long-term sustainability.

Reserve management strategies in DeFi insurance must account for the volatility of cryptocurrency assets that typically comprise protocol reserves, implementing mechanisms to maintain adequate coverage ratios even during significant market downturns. Some protocols implement multi-asset reserve strategies that reduce correlation risks, while others focus on stablecoin reserves that provide more predictable value but may offer lower long-term returns.

The integration of yield farming and other DeFi strategies with insurance protocol reserves creates opportunities to enhance returns for coverage providers while also introducing additional risks that must be carefully managed. Advanced protocols implement sophisticated yield strategies that can adapt to market conditions while maintaining the liquidity necessary to process claims promptly when they arise.

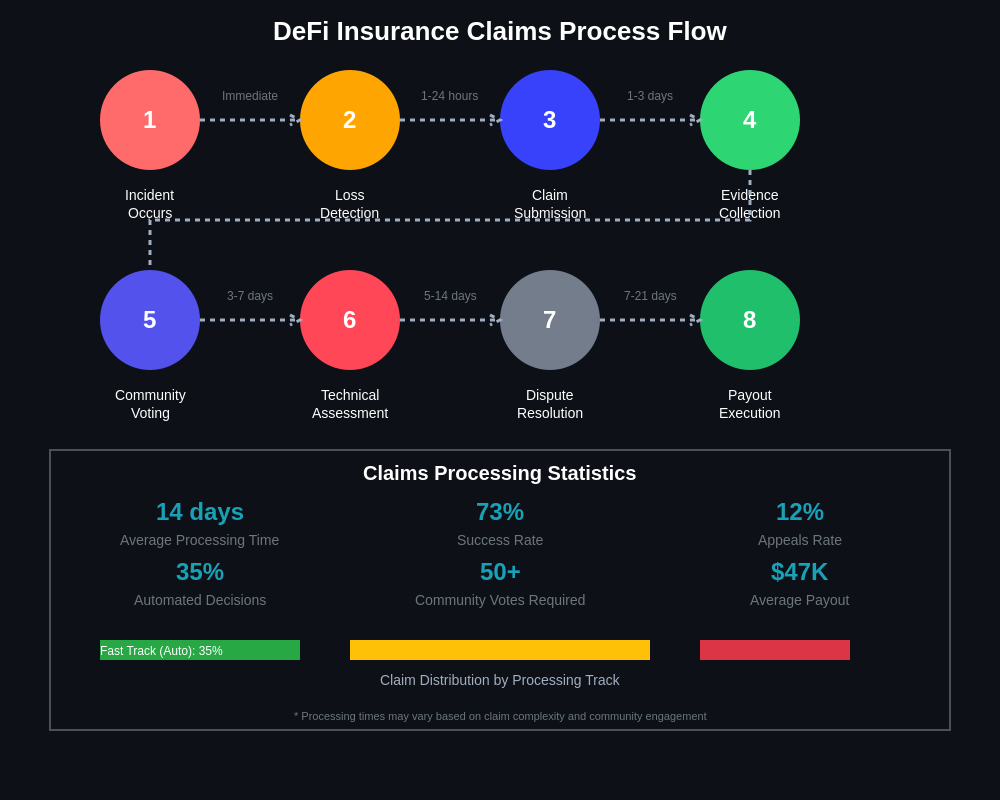

Claims Assessment and Dispute Resolution

The claims assessment process in DeFi insurance represents one of the most challenging aspects of these systems, as community-based evaluation mechanisms must accurately determine the validity of technical claims while avoiding the conflicts of interest and expertise limitations that can undermine decentralized decision-making processes. Effective claims assessment requires participants to have deep technical knowledge of blockchain systems, smart contract architecture, and the specific protocols being evaluated.

Evidence standards for DeFi insurance claims typically require detailed technical documentation including transaction hashes, block numbers, contract addresses, and technical analysis explaining how the claimed loss occurred. This creates a higher barrier for claim submission compared to traditional insurance but enables more objective evaluation of claims based on immutable blockchain data rather than potentially subjective witness accounts or damage assessments.

Expert evaluation mechanisms in many DeFi insurance protocols attempt to address the technical complexity of claims assessment by incorporating input from security researchers, smart contract auditors, and protocol developers who have the expertise necessary to evaluate complex technical claims. However, the limited pool of qualified experts and potential conflicts of interest create challenges in maintaining objectivity and preventing manipulation of the claims process.

Appeal and dispute resolution procedures in DeFi insurance must balance the need for finality in claims decisions with the recognition that complex technical assessments may sometimes reach incorrect conclusions. Many protocols implement multi-stage appeals processes with escalating levels of review, though the decentralized nature of these systems limits the options for final dispute resolution compared to traditional legal systems.

The time requirements for thorough claims assessment often conflict with user expectations for rapid claim resolution, as proper evaluation of complex smart contract failures may require extensive technical analysis, community debate, and multiple rounds of voting. This creates tension between the desire for quick payouts and the need for accurate evaluation that protects the protocol from fraudulent or mistaken claims.

Regulatory Considerations and Compliance Challenges

The regulatory landscape for DeFi insurance remains largely undefined in most jurisdictions, creating uncertainty for both protocol developers and users about the legal status of these systems and the obligations they may create for various participants. Traditional insurance regulation is built around centralized entities with clear ownership structures and geographic locations, concepts that do not map cleanly onto decentralized protocols governed by distributed communities.

Licensing requirements for insurance activities vary significantly across jurisdictions, with some regions requiring formal licenses for any entity offering insurance-like products while others focus on the specific activities and relationships involved rather than the technological implementation. DeFi insurance protocols must navigate these requirements while maintaining their decentralized characteristics, often resulting in complex legal structures that attempt to separate protocol development from insurance provision.

Consumer protection regulations in many jurisdictions include specific requirements for insurance products including disclosure standards, claims processing procedures, and financial stability requirements that may be difficult for decentralized protocols to satisfy using their current governance and operational models. These requirements may force DeFi insurance protocols to implement more centralized structures or formal legal entities that can comply with traditional regulatory frameworks.

The global nature of DeFi insurance creates additional complexity as users from different jurisdictions may participate in the same protocols while being subject to different regulatory requirements. This creates challenges for protocol developers who must consider multiple regulatory frameworks simultaneously while maintaining the borderless accessibility that represents one of the key advantages of decentralized systems.

Tax implications of DeFi insurance participation can be complex for users, as premium payments, claim receipts, and token rewards may all have different tax treatments depending on the jurisdiction and the specific nature of the transactions involved. The pseudonymous nature of many DeFi interactions creates additional complexity for users attempting to comply with tax obligations while participating in these systems.

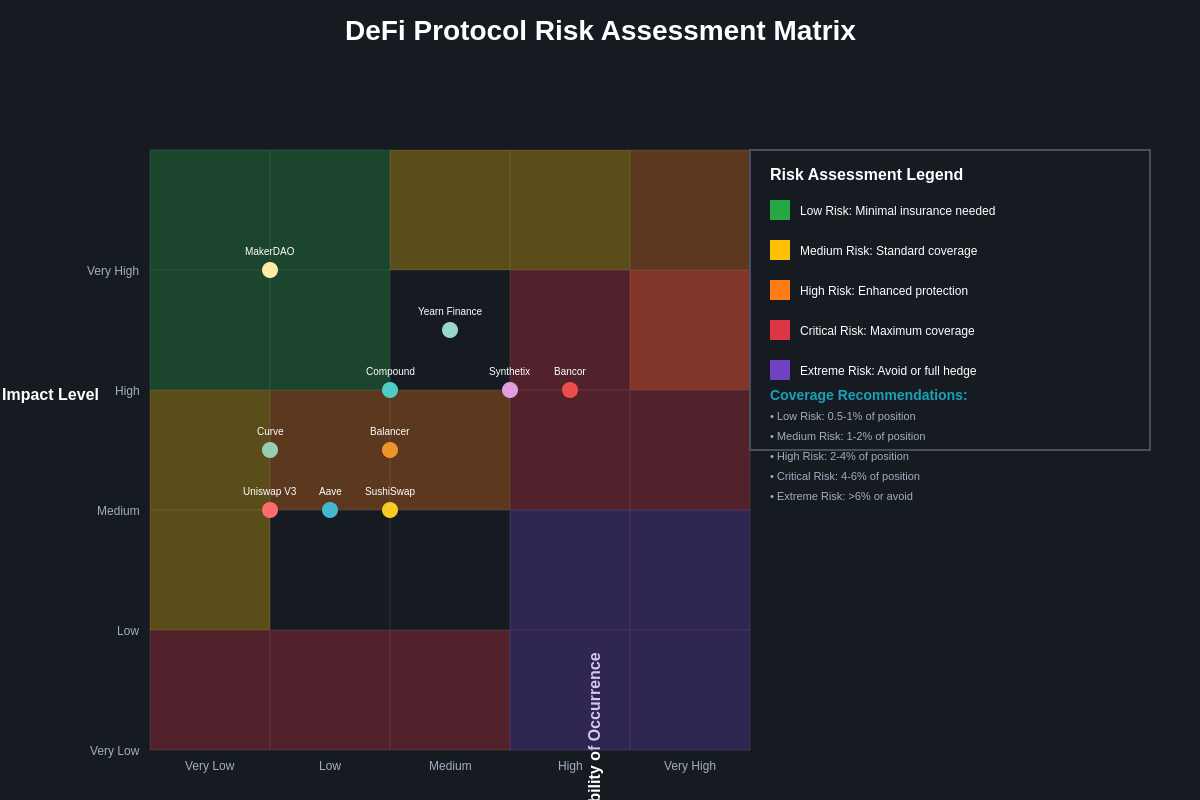

Risk Management Strategies for Users

Effective risk management in DeFi requires users to develop comprehensive strategies that go beyond simply purchasing insurance coverage to include careful protocol selection, position sizing, diversification, and ongoing monitoring of the rapidly evolving DeFi landscape. The interconnected nature of DeFi means that risks can propagate quickly across protocols, making it essential for users to understand the broader ecosystem dependencies of their positions.

Due diligence processes for DeFi protocol evaluation should include thorough review of smart contract audits, assessment of development team credentials and track records, analysis of governance structures and token distribution, evaluation of economic models and sustainability, and ongoing monitoring of protocol metrics and community health. However, the rapid pace of DeFi innovation means that even thorough due diligence may not identify all relevant risks or account for how protocols may evolve over time.

Portfolio diversification strategies in DeFi must account for the high correlation between different protocols during market stress periods, as many DeFi applications rely on similar underlying assets, oracle systems, or economic assumptions that can create cascading failures across seemingly independent protocols. Effective diversification may require spreading positions across different blockchain networks, different types of DeFi applications, and different risk profiles rather than simply using multiple protocols.

Position sizing in DeFi should reflect the experimental nature of many protocols and the potential for total loss in ways that traditional financial markets rarely experience. Many sophisticated DeFi users recommend limiting exposure to any single protocol to amounts that can be comfortably lost while maintaining sufficient diversification to capture the opportunities that successful protocols may provide over time.

Comprehensive Risk Analysis Tools

Ongoing monitoring requirements for DeFi positions include tracking protocol governance proposals that might affect risk profiles, monitoring for security vulnerabilities or exploits that might impact related protocols, staying informed about regulatory developments that might affect protocol operations, and maintaining awareness of market conditions that might trigger liquidations or other automated actions.

Traditional Insurance vs DeFi Insurance Comparison

The fundamental differences between traditional insurance and DeFi insurance reflect broader distinctions between centralized and decentralized financial systems, with each approach offering unique advantages and limitations that users must carefully consider when developing risk management strategies. Traditional insurance relies on established legal frameworks, regulatory oversight, and centralized decision-making processes that provide certainty and recourse but may also limit innovation and accessibility.

Underwriting processes in traditional insurance involve detailed risk assessment by professional underwriters who use historical data, actuarial models, and standardized risk categories to price policies and determine coverage terms. DeFi insurance typically uses algorithmic pricing models and community-based risk assessment that may be more transparent but also more volatile and potentially less accurate, particularly for novel risks that lack historical precedent.

Claims processing in traditional insurance involves professional claims adjusters who investigate losses, assess damages, and determine coverage eligibility based on established procedures and legal frameworks. DeFi insurance relies on community voting mechanisms that may be more democratic but also more technically demanding and potentially subject to manipulation or conflicts of interest among voting participants.

Regulatory protection for traditional insurance policyholders includes government-backed guarantee funds that protect against insurer insolvency, standardized disclosure requirements that ensure consumers understand their coverage, and formal dispute resolution procedures that provide recourse when claims are wrongly denied. DeFi insurance operates outside these protective frameworks, placing greater responsibility on users to understand and evaluate their coverage while providing fewer options for recourse when disputes arise.

Cost structures in traditional insurance include significant overhead for marketing, sales, claims processing, and regulatory compliance that may result in higher premiums but also provide professional services and regulatory protections that many consumers value. DeFi insurance can potentially offer lower costs by eliminating these overhead expenses while requiring users to take on additional responsibilities for risk assessment and claims evaluation.

Integration with Broader DeFi Ecosystem

The integration of insurance protocols with the broader DeFi ecosystem creates opportunities for more sophisticated risk management strategies while also introducing additional complexity and potential points of failure that users must carefully consider. Modern DeFi insurance protocols increasingly offer coverage that spans multiple protocols and blockchain networks, recognizing that users typically interact with numerous DeFi applications simultaneously.

Yield farming strategies that incorporate insurance coverage can provide enhanced risk-adjusted returns by protecting against smart contract failures while maintaining exposure to protocol rewards and token appreciation. However, the additional complexity of insured yield farming positions requires careful analysis of the relationship between insurance costs, potential yields, and the probability of covered losses occurring.

Cross-protocol composability enables the creation of sophisticated financial products that combine insurance coverage with lending, borrowing, trading, and other DeFi services in ways that traditional financial systems struggle to replicate. These composable insurance products can automatically adjust coverage based on user positions, provide dynamic pricing based on real-time risk assessment, and integrate with automated portfolio management strategies.

The emergence of insurance-focused DeFi protocols creates new opportunities for users to participate in insurance provision as an investment strategy, potentially earning returns by providing coverage for protocols they understand well while contributing to the overall security and sustainability of the DeFi ecosystem. However, this requires significant technical expertise and ongoing commitment to risk monitoring that may not be suitable for all users.

Interoperability challenges between different blockchain networks create additional complexity for DeFi insurance, as users increasingly operate across multiple chains while insurance coverage may be limited to specific networks or require separate policies for different chains. Cross-chain insurance solutions are beginning to emerge but remain technically complex and may introduce additional risks related to bridge security and cross-chain communication.

Emerging Technologies and Future Developments

Parametric insurance represents one of the most promising developments in DeFi insurance technology, enabling automatic claim payouts based on objective, measurable parameters rather than subjective damage assessments. These systems can potentially eliminate the need for complex claims evaluation processes while providing faster payouts and reduced administrative overhead, though they require careful parameter selection to ensure that payouts accurately reflect actual losses.

Zero-knowledge proof systems offer opportunities to enhance privacy protection for DeFi insurance participants while maintaining the transparency necessary for effective risk assessment and claims verification. These technologies could enable users to prove their eligibility for coverage or the validity of their claims without revealing sensitive information about their positions or trading strategies.

Artificial intelligence and machine learning applications in DeFi insurance could potentially improve risk assessment accuracy, automate routine claims processing, and detect fraudulent behavior more effectively than current community-based evaluation mechanisms. However, the implementation of AI systems in decentralized protocols raises questions about transparency, accountability, and the potential for algorithmic bias that must be carefully addressed.

Cross-chain bridge insurance represents an emerging coverage category that addresses the specific risks associated with moving assets between different blockchain networks, an increasingly common activity as the multi-chain DeFi ecosystem continues to develop. These specialized insurance products must account for the unique technical and economic risks associated with bridge protocols while providing coverage that scales with the growing cross-chain activity.

Prediction market integration with DeFi insurance could potentially improve risk pricing accuracy by leveraging collective intelligence about protocol risks, security vulnerabilities, and market conditions. These systems could provide more dynamic and responsive pricing than current algorithmic models while also creating new opportunities for sophisticated users to profit from superior risk assessment capabilities.

User Experience and Accessibility Improvements

The user experience challenges facing DeFi insurance adoption include complex technical concepts that average users struggle to understand, fragmented interfaces that require interaction with multiple protocols and platforms, high transaction costs that make small coverage amounts economically impractical, and limited educational resources that help users develop appropriate risk management strategies. Addressing these challenges is crucial for broader adoption of DeFi insurance among mainstream cryptocurrency users.

Simplified coverage products that bundle multiple types of protection into easy-to-understand packages could significantly improve accessibility for less technical users while maintaining the flexibility that sophisticated users require. These products might offer standardized coverage levels for common DeFi activities like yield farming, lending, or liquidity provision without requiring users to understand the technical details of specific risk types.

Mobile-first interfaces and improved user experience design could make DeFi insurance more accessible to users who are comfortable with traditional mobile financial apps but intimidated by the complex interfaces that characterize many current DeFi protocols. These improvements must balance simplicity with the transparency and control that represent key advantages of decentralized systems.

Educational initiatives and risk assessment tools could help users better understand the risks they face in DeFi participation and the coverage options available to address those risks. These tools might include risk calculators that help users determine appropriate coverage amounts, educational content that explains different types of DeFi risks in accessible language, and simulation tools that help users understand how insurance coverage would affect their positions under different scenarios.

Integration with popular DeFi wallets and interfaces could reduce the friction associated with purchasing and managing insurance coverage by embedding insurance options directly into the user interfaces where people already manage their DeFi positions. This approach could make insurance coverage as routine as any other DeFi transaction while providing appropriate warnings and education about the risks being covered.

Economic Impact and Market Analysis

The economic impact of DeFi insurance extends beyond direct protection for individual users to include broader effects on protocol adoption, risk pricing efficiency, and the overall stability of the decentralized finance ecosystem. Insurance availability can enable more conservative users to participate in DeFi activities they might otherwise avoid while providing protocols with additional credibility that can attract institutional participation and larger deposits.

Market pricing analysis for DeFi insurance reveals significant volatility and inconsistencies that reflect the nascent nature of these markets and the limited historical data available for risk assessment. Current market trends show that insurance premium costs can vary dramatically based on market conditions, recent exploit activity, and the specific protocols being covered, creating opportunities for sophisticated users while also creating barriers for price-sensitive participants.

The correlation between insurance costs and protocol adoption suggests that effective insurance markets could play a crucial role in the long-term growth and stability of the DeFi ecosystem by reducing the risk barriers that prevent many potential users from participating in decentralized financial services. However, the current high costs and limited availability of comprehensive coverage may be limiting this positive impact.

Institutional adoption of DeFi services increasingly depends on the availability of appropriate risk management tools including insurance coverage that meets institutional risk management standards and regulatory requirements. The development of more sophisticated DeFi insurance products could therefore play a crucial role in enabling the next phase of DeFi growth that includes significant institutional participation.

The systemic risk implications of DeFi insurance concentration must be carefully monitored as these markets develop, as the failure of major insurance protocols could have cascading effects across the broader DeFi ecosystem. Diversification of insurance provision and the development of multiple competing protocols will be important for maintaining system resilience as the market matures.

Challenges and Limitations

The technical complexity of accurately assessing smart contract risks represents one of the most significant challenges facing DeFi insurance protocols, as these assessments require deep expertise in blockchain technology, cryptographic systems, and economic mechanism design that few individuals possess. This expertise gap creates potential for systematic mispricing of risks and inadequate coverage for complex or novel protocols that could result in significant losses for both insurance providers and policyholders.

Liquidity constraints in DeFi insurance markets can result in situations where coverage is unavailable when it is most needed, particularly during market stress periods when exploit risks may be elevated and user demand for coverage increases. The procyclical nature of insurance demand and supply can exacerbate these constraints and potentially contribute to broader instability in the DeFi ecosystem during crisis periods.

Governance challenges in decentralized insurance protocols include the potential for capture by large token holders, conflicts of interest between insurance providers and policyholders, and the difficulty of making rapid decisions during crisis situations when traditional centralized insurance companies might need to act quickly to prevent further losses. These governance limitations could undermine the effectiveness of DeFi insurance in providing reliable protection when users need it most.

Regulatory uncertainty creates ongoing challenges for DeFi insurance protocols and their users, as unclear legal status makes it difficult to predict how these systems will be treated by authorities and whether participants might face unexpected legal obligations or restrictions. This uncertainty may limit institutional adoption and create compliance challenges for users in jurisdictions with strict financial services regulations.

The experimental nature of many DeFi protocols creates challenges for insurance coverage as traditional risk assessment methods may not be applicable to novel economic mechanisms, unproven technologies, and rapidly evolving systems. This creates potential for significant gaps between perceived and actual risks that could result in inadequate coverage or catastrophic losses for insurance providers.

Future Outlook and Predictions

The evolution of DeFi insurance toward more sophisticated risk assessment mechanisms will likely incorporate advanced analytics, machine learning, and real-time monitoring systems that can provide more accurate risk pricing and faster response to emerging threats. These developments could significantly improve the effectiveness of DeFi insurance while also making it more accessible to users who lack deep technical expertise in blockchain systems.

Integration between DeFi insurance and traditional insurance markets could create hybrid products that combine the accessibility and regulatory protection of traditional insurance with the transparency and innovation of decentralized systems. These hybrid approaches might enable broader adoption while addressing some of the regulatory and consumer protection concerns that currently limit institutional participation in DeFi insurance markets.

The development of standardized risk assessment frameworks and coverage terms across different DeFi insurance protocols could improve market efficiency and user understanding while enabling better comparison shopping and risk management strategies. However, standardization efforts must balance consistency with the flexibility to address novel risks and innovative protocol designs.

Scaling solutions for DeFi insurance must address the current high transaction costs and limited throughput that make small coverage amounts economically impractical while also maintaining the security and decentralization characteristics that represent key advantages of these systems. Layer 2 solutions and other scaling technologies could potentially enable broader adoption by reducing costs and improving user experience.

The maturation of DeFi insurance markets will likely result in increased specialization among coverage providers, with some focusing on specific types of risks or protocols while others develop expertise in particular aspects of risk assessment or claims processing. This specialization could improve overall market efficiency while also creating new opportunities for users to find coverage that precisely matches their risk profiles and preferences.

Disclaimer: This article is for educational and informational purposes only and should not be construed as financial, investment, or legal advice. DeFi insurance products are experimental and carry significant risks including total loss of funds. The regulatory status of DeFi insurance is uncertain in many jurisdictions. Always conduct thorough research and consider consulting with qualified professionals before participating in any DeFi activities or purchasing insurance coverage. Past performance does not guarantee future results, and all investments carry risk of loss.