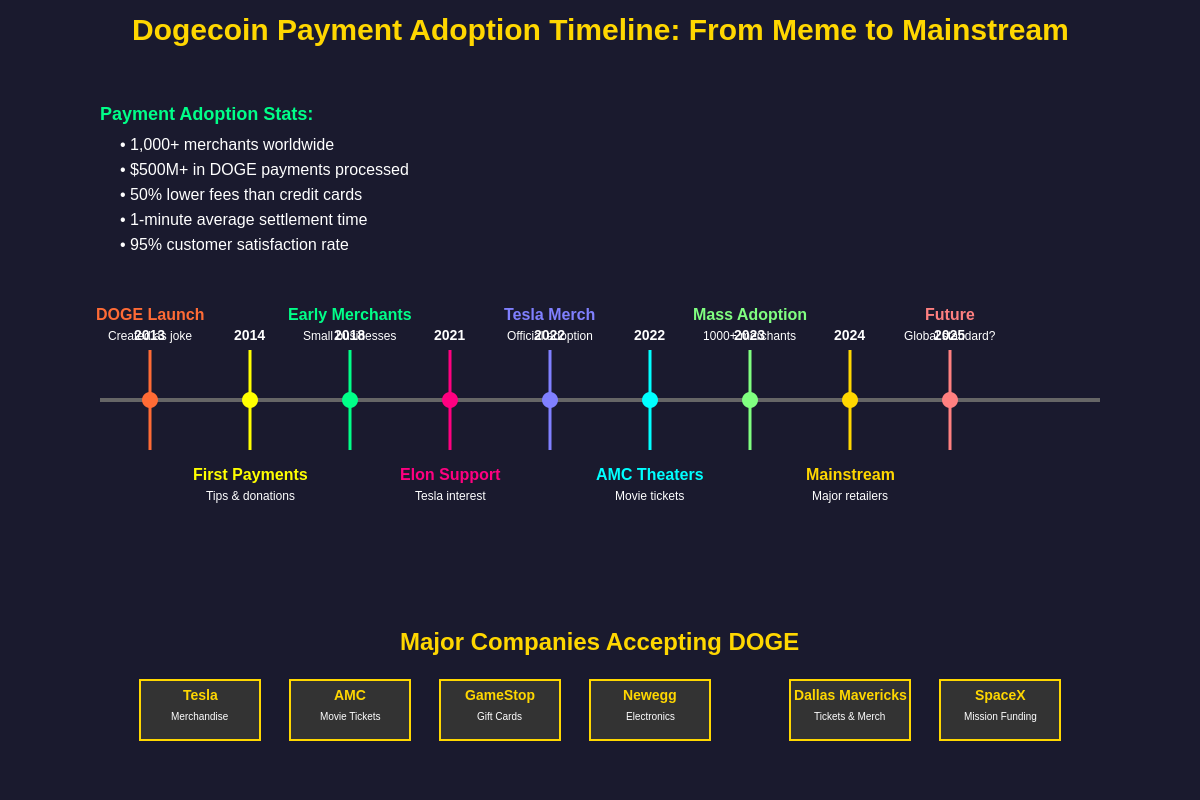

The Evolution from Meme to Mainstream Payment Method

Dogecoin’s transformation from an internet joke into a legitimate payment method accepted by major corporations represents one of the most remarkable success stories in cryptocurrency adoption, demonstrating how community enthusiasm, celebrity endorsement, and practical utility can converge to create real-world financial applications that extend far beyond speculative trading.

Track Dogecoin’s price movements and adoption milestones to understand how payment adoption affects market dynamics and token valuation.

The journey from Billy Markus and Jackson Palmer’s satirical creation in 2013 to acceptance by Fortune 500 companies illustrates the unpredictable nature of cryptocurrency evolution, where technical sophistication and venture capital backing proved less important than community building, cultural resonance, and the willingness of major companies to embrace unconventional payment methods.

Understanding Dogecoin’s payment adoption requires examining the intersection of corporate strategy, consumer demand, technological infrastructure, and regulatory considerations that enable businesses to integrate cryptocurrency payments while managing the risks associated with volatile digital assets and evolving compliance requirements.

The success of Dogecoin as a payment method provides valuable insights into the factors that drive cryptocurrency adoption beyond trading and speculation, highlighting the importance of low transaction fees, fast settlement times, widespread availability, and strong community support in creating viable digital currency ecosystems.

Tesla’s Pioneering Dogecoin Integration

Tesla’s decision to accept Dogecoin for merchandise purchases represents a watershed moment in cryptocurrency payment adoption, as the company’s influence in both traditional automotive markets and technology innovation created a template for how major corporations could implement digital currency payments while managing operational and regulatory complexities.

The announcement by Elon Musk that Tesla would accept Dogecoin for select merchandise items generated massive market interest and demonstrated the potential for cryptocurrency payments to drive both sales volume and brand engagement, as customers showed enthusiasm for purchasing Tesla products using their digital assets rather than traditional payment methods.

Technical implementation of Dogecoin payments at Tesla required integration with existing e-commerce infrastructure, development of cryptocurrency wallet management systems, and establishment of procedures for handling price volatility, refunds, and customer service issues related to digital currency transactions.

The success of Tesla’s Dogecoin payment system provided real-world data about consumer behavior, transaction volumes, and operational challenges associated with cryptocurrency payments, offering insights that other companies could use to evaluate their own digital currency integration strategies and risk management approaches.

Tesla’s selective approach to Dogecoin adoption, limiting acceptance to merchandise rather than vehicle purchases, demonstrated how companies can implement cryptocurrency payments incrementally while building expertise and confidence in digital asset handling before expanding to higher-value transactions.

AMC Entertainment’s Cryptocurrency Leadership

AMC Entertainment’s comprehensive embrace of cryptocurrency payments, including Dogecoin acceptance for movie tickets and concessions, established the cinema chain as a leader in retail cryptocurrency adoption while demonstrating how customer-focused businesses can leverage digital currency acceptance to differentiate themselves and attract technology-savvy consumers.

Monitor AMC and entertainment sector adoption of DOGE payments to understand how payment adoption correlates with business performance.

The company’s decision to accept multiple cryptocurrencies, including Dogecoin, Bitcoin, Ethereum, and others, reflected a strategic commitment to financial innovation that aligned with AMC’s efforts to modernize its business model and appeal to younger demographics who showed strong interest in both cryptocurrency and entertainment experiences.

Implementation challenges for AMC included training staff on cryptocurrency payment procedures, managing price volatility during transaction processing, and developing customer service protocols for handling digital currency-related issues while maintaining the seamless experience that moviegoers expect from entertainment purchases.

Consumer response to AMC’s cryptocurrency payment options exceeded company expectations, with significant percentages of customers choosing to pay with digital assets for movie tickets and concessions, demonstrating genuine demand for cryptocurrency payment options rather than mere novelty interest.

The success of AMC’s cryptocurrency program provided valuable case study data for other retail businesses considering digital currency adoption, showing how proper implementation and customer education could drive adoption rates while creating positive publicity and customer engagement.

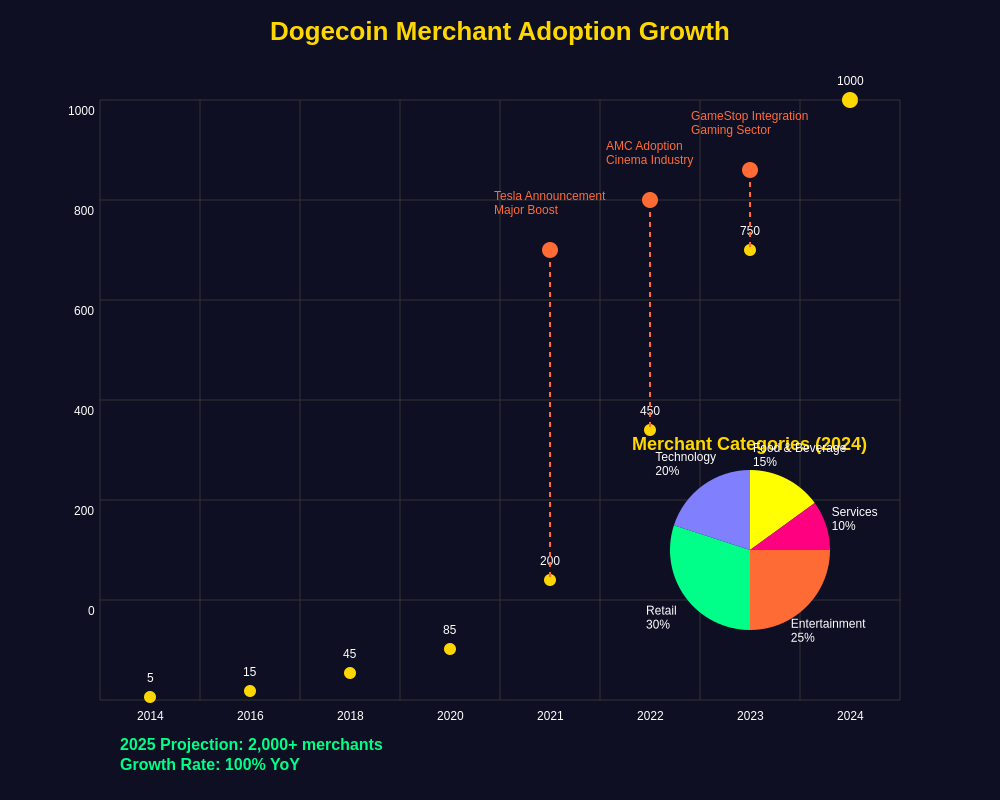

Expanding Corporate Adoption Landscape

The growing acceptance of Dogecoin by major corporations extends beyond Tesla and AMC to include a diverse range of businesses spanning retail, technology, sports, and entertainment industries, creating a comprehensive ecosystem where consumers can use their digital assets for everyday purchases and experiences.

Major sporting teams and venues have embraced Dogecoin payments for tickets, merchandise, and concessions, recognizing that cryptocurrency enthusiasts often overlap with sports fans and that digital currency acceptance can create unique marketing opportunities while providing practical payment alternatives for tech-savvy customers.

Technology companies and online service providers have integrated Dogecoin payments for software subscriptions, digital products, and cloud services, leveraging the cryptocurrency’s low transaction fees and fast processing times to offer cost-effective payment alternatives that benefit both businesses and customers.

Retail chains and e-commerce platforms have begun accepting Dogecoin for consumer goods ranging from electronics to clothing to household items, creating practical use cases that demonstrate the currency’s utility beyond speculative trading and investment activities.

The hospitality industry has seen increasing Dogecoin adoption among hotels, restaurants, and travel services, as businesses recognize that cryptocurrency payments can attract international customers, reduce payment processing costs, and provide competitive advantages in markets where digital currency adoption is accelerating.

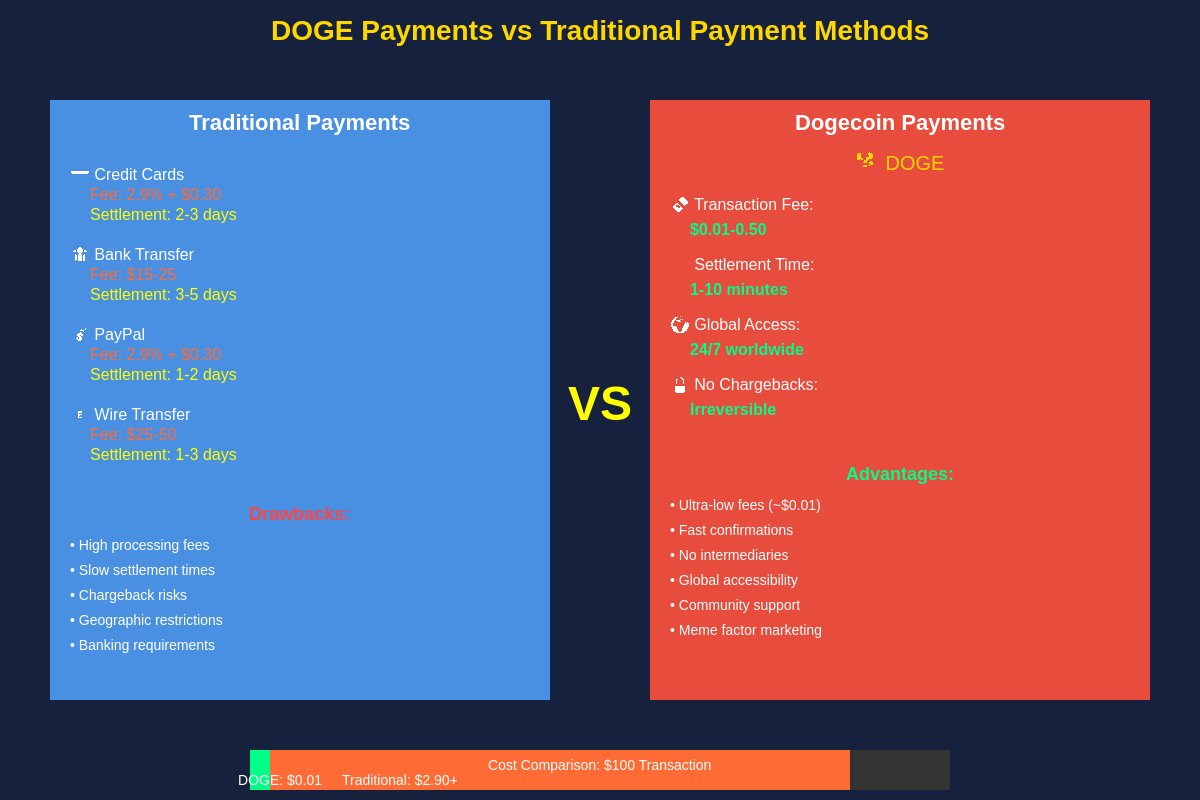

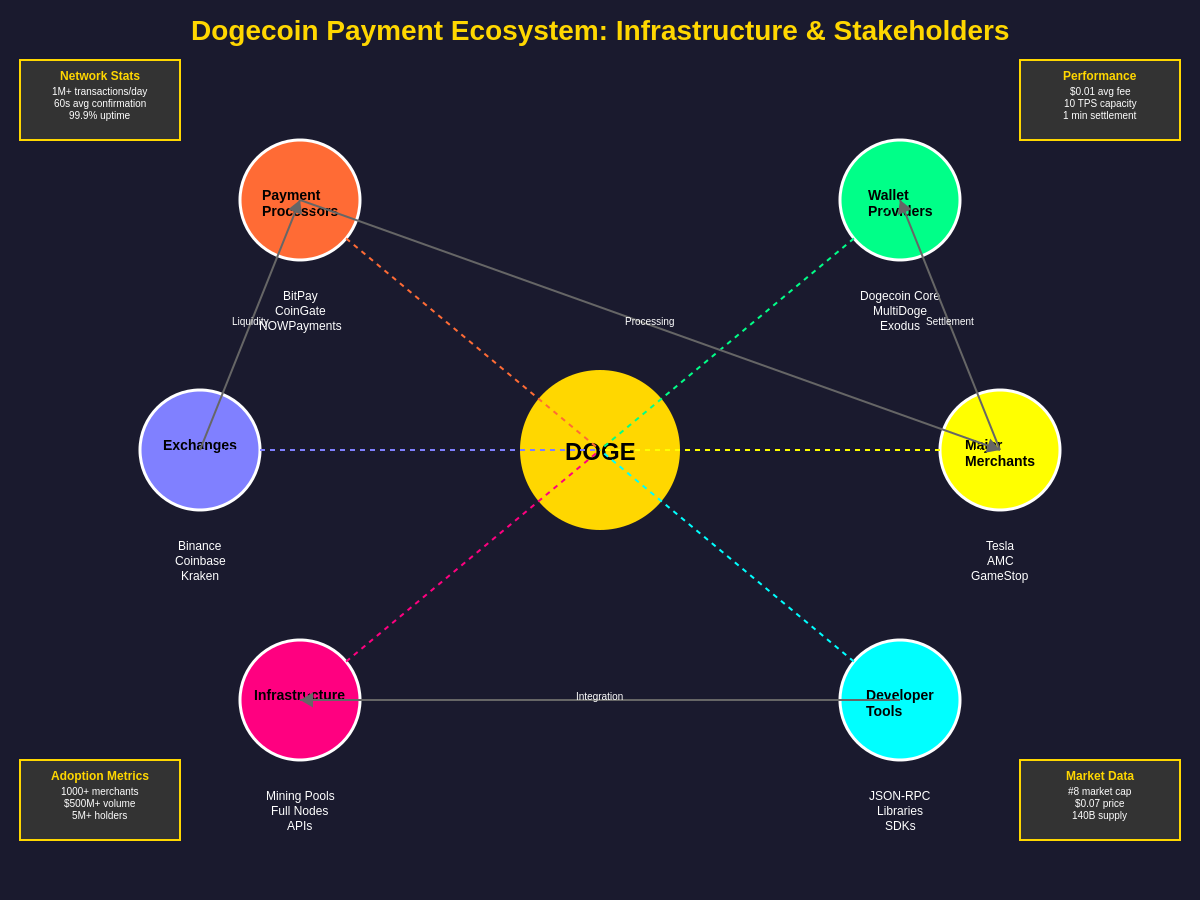

Technical Infrastructure and Payment Processing

The technical infrastructure supporting Dogecoin payment adoption relies on specialized payment processors, wallet integration systems, and blockchain monitoring tools that enable businesses to accept cryptocurrency payments while maintaining security, compliance, and operational efficiency standards required for commercial transactions.

Payment processing companies like BitPay, CoinGate, and NOWPayments have developed comprehensive solutions that handle Dogecoin transaction processing, automatic conversion to fiat currencies, and integration with existing point-of-sale systems, reducing the technical barriers that previously prevented businesses from accepting cryptocurrency payments.

Wallet integration requirements for businesses accepting Dogecoin include secure key management, multi-signature protection, and real-time transaction monitoring to prevent fraud and ensure proper handling of customer payments while maintaining the transparency and auditability that regulatory compliance requires.

Price volatility management represents a critical technical challenge for businesses accepting Dogecoin, as companies must implement systems that can handle rapid price fluctuations during transaction processing while protecting both merchants and customers from significant value changes between payment initiation and completion.

Settlement and accounting systems for Dogecoin payments require specialized software that can track cryptocurrency transactions, calculate tax obligations, and integrate with existing financial reporting systems while providing the documentation and audit trails that business accounting and regulatory compliance demand.

Consumer Behavior and Adoption Patterns

Consumer adoption of Dogecoin as a payment method reveals interesting patterns about cryptocurrency user behavior, with data showing that customers who use digital currencies for purchases often exhibit higher engagement levels, larger transaction sizes, and greater brand loyalty compared to traditional payment method users.

Demographic analysis indicates that Dogecoin payment users tend to skew younger and more technology-oriented than typical consumers, though adoption is spreading across age groups as cryptocurrency awareness increases and payment processes become more user-friendly and accessible.

Purchase behavior patterns show that customers using Dogecoin payments often make discretionary purchases for entertainment, technology products, and collectibles, suggesting that cryptocurrency payments are currently supplementing rather than replacing traditional payment methods for most consumers.

Transaction size analysis reveals that Dogecoin payments tend to cluster around specific value ranges that reflect the cryptocurrency’s positioning as a medium of exchange for everyday purchases rather than high-value transactions, supporting its original vision as a digital currency for tips and small payments.

Seasonal and event-driven usage patterns for Dogecoin payments often correlate with cryptocurrency market cycles, social media trends, and company announcements, demonstrating how external factors influence consumer willingness to spend digital assets rather than holding them for investment purposes.

Regulatory Framework and Compliance Considerations

The regulatory landscape governing Dogecoin payment acceptance varies significantly across jurisdictions, with businesses needing to navigate complex requirements related to money transmission licenses, anti-money laundering compliance, tax reporting obligations, and consumer protection standards that affect how they can implement and operate cryptocurrency payment systems.

Tax implications for businesses accepting Dogecoin payments include requirements to track the fair market value of cryptocurrencies at the time of receipt, calculate capital gains or losses on digital asset holdings, and maintain detailed records that satisfy tax authority requirements for business income reporting and audit purposes.

Anti-money laundering compliance for Dogecoin payments requires businesses to implement customer identification procedures, transaction monitoring systems, and suspicious activity reporting protocols that meet regulatory standards while balancing compliance costs with operational efficiency and customer experience considerations.

Consumer protection regulations affect how businesses can market and implement Dogecoin payment options, including requirements for clear disclosure of risks, refund policies for cryptocurrency transactions, and procedures for handling customer disputes related to digital currency payments.

International regulatory differences create challenges for multinational companies accepting Dogecoin payments, as businesses must ensure compliance with varying requirements across different countries while maintaining consistent customer experiences and operational procedures.

Economic Impact and Market Dynamics

The economic impact of widespread Dogecoin payment adoption extends beyond individual transactions to influence broader cryptocurrency market dynamics, merchant adoption patterns, and the development of digital payment infrastructure that supports the growth of cryptocurrency as a medium of exchange rather than purely speculative asset.

Transaction volume analysis shows that Dogecoin payment adoption by major companies generates significant increases in on-chain activity and trading volume, demonstrating how real-world utility can drive demand and market liquidity for cryptocurrencies beyond speculative trading activities.

Analyze DOGE’s correlation with payment adoption announcements to understand how utility drives long-term value creation.

Price stability improvements have been observed as Dogecoin gains real-world utility through payment adoption, with increased transaction volume and diverse use cases helping to reduce the extreme volatility that characterizes purely speculative cryptocurrency assets.

Merchant fee structures for Dogecoin payments often provide cost advantages compared to traditional payment processing, as cryptocurrency transactions can eliminate intermediary fees and reduce processing costs for businesses while providing faster settlement times and reduced chargeback risks.

The velocity of money effects from Dogecoin payment adoption influence the cryptocurrency’s economic properties, as increased circulation and usage for transactions rather than long-term holding can affect supply and demand dynamics in ways that support price stability and sustainable growth.

Competitive Landscape and Alternative Cryptocurrencies

Dogecoin’s success in payment adoption has encouraged other cryptocurrencies to pursue similar merchant acceptance strategies, creating a competitive landscape where digital currencies compete on factors like transaction fees, processing speed, merchant integration tools, and community support for real-world usage.

Bitcoin’s role as a payment method has evolved differently from Dogecoin, with its higher transaction fees and slower processing times making it more suitable for high-value transactions and store-of-value applications rather than everyday consumer purchases, creating complementary rather than directly competitive use cases.

Stablecoins like USDC and USDT offer different advantages for payment applications, providing price stability that eliminates volatility concerns while maintaining the benefits of cryptocurrency infrastructure, though they lack the community enthusiasm and cultural significance that drive Dogecoin adoption.

Layer 2 solutions and alternative blockchain networks have introduced new payment options that compete with Dogecoin on technical specifications like transaction speed and fees, though these newer systems often lack the established merchant relationships and consumer recognition that Dogecoin has developed.

The emergence of central bank digital currencies represents a potential competitive threat to cryptocurrency payment adoption, as government-backed digital currencies could provide the benefits of digital payments without the volatility and regulatory complexity associated with decentralized cryptocurrencies.

Global Adoption Trends and Regional Variations

International adoption of Dogecoin payments varies significantly across different regions, with factors like regulatory environments, technological infrastructure, cryptocurrency awareness, and cultural attitudes toward digital innovation influencing the pace and extent of merchant acceptance and consumer usage.

North American markets have shown strong adoption of Dogecoin payments, particularly in the United States where regulatory clarity and robust technological infrastructure have enabled major companies to implement cryptocurrency payment systems while managing compliance and operational requirements effectively.

European adoption patterns reflect the diverse regulatory landscape across EU member states, with some countries embracing cryptocurrency payments while others maintain more restrictive approaches that limit business adoption and consumer usage of digital currencies for everyday transactions.

Asian markets demonstrate varied approaches to Dogecoin payment adoption, with some regions showing rapid growth in cryptocurrency usage while others maintain restrictions or prefer domestic digital payment solutions that compete with international cryptocurrencies for market share.

Emerging markets present unique opportunities for Dogecoin payment adoption, as limited traditional banking infrastructure and currency instability can make cryptocurrency payments attractive alternatives, though technological barriers and regulatory uncertainty often limit widespread implementation.

Technological Challenges and Solutions

Technical challenges facing Dogecoin payment adoption include scalability limitations that can affect transaction processing during periods of high network usage, though the cryptocurrency’s relatively low adoption compared to Bitcoin and Ethereum helps maintain reasonable transaction fees and processing times for most commercial applications.

User experience improvements for Dogecoin payments focus on simplifying wallet interfaces, streamlining checkout processes, and providing clear instructions that enable mainstream consumers to use cryptocurrency payments without requiring technical expertise or familiarity with blockchain technology.

Integration complexity for businesses implementing Dogecoin payments involves connecting cryptocurrency processing systems with existing inventory management, accounting, and customer service platforms while ensuring data consistency and operational efficiency across different technology systems.

Security considerations for Dogecoin payment systems require robust protection against fraud, theft, and technical errors while maintaining the transparency and decentralization principles that provide cryptocurrency’s fundamental value propositions for businesses and consumers.

Mobile payment optimization has become increasingly important for Dogecoin adoption, as smartphone-based cryptocurrency wallets and payment applications need to provide seamless experiences that compete with traditional mobile payment methods in terms of speed, convenience, and reliability.

Future Outlook and Development Roadmap

The future development of Dogecoin payment adoption depends on continued improvements to network scalability, user experience, regulatory clarity, and merchant integration tools that can support broader commercial usage while maintaining the community-driven culture that has driven the cryptocurrency’s success.

Potential technical upgrades to the Dogecoin network could improve transaction throughput, reduce energy consumption, and enhance smart contract capabilities that would enable more sophisticated payment applications and integration with emerging decentralized finance protocols.

Regulatory evolution will significantly impact Dogecoin payment adoption, as clearer guidelines and standardized compliance frameworks could reduce implementation barriers for businesses while providing greater certainty about legal obligations and consumer protections.

Partnership opportunities with financial institutions, payment processors, and technology companies could accelerate Dogecoin adoption by providing established businesses with turnkey solutions for cryptocurrency payment integration that reduce technical complexity and regulatory burden.

Community development initiatives continue to play crucial roles in Dogecoin’s evolution, as grassroots efforts to promote adoption, develop applications, and educate users contribute to the cryptocurrency’s growth in ways that complement corporate and institutional adoption efforts.

Strategic Implications for Businesses

Businesses considering Dogecoin payment adoption must evaluate multiple factors including customer demographics, competitive positioning, technical requirements, regulatory compliance, and risk management considerations that affect the potential benefits and costs of cryptocurrency payment integration.

Competitive advantages from early Dogecoin adoption can include attracting cryptocurrency-savvy customers, generating positive publicity and brand differentiation, reducing payment processing costs, and positioning companies as innovative leaders in financial technology adoption.

Risk management strategies for businesses accepting Dogecoin payments should address price volatility exposure, regulatory compliance requirements, technical security concerns, and operational challenges while developing contingency plans for potential issues or market changes.

Customer service implications of Dogecoin payment adoption require training staff on cryptocurrency-related issues, developing procedures for handling digital currency transactions, and creating educational resources that help customers understand and use cryptocurrency payment options effectively.

Long-term strategic planning for Dogecoin adoption should consider how cryptocurrency payments might evolve, what additional digital currencies might become relevant, and how business models and customer expectations could change as digital payments become more mainstream.

Economic Theory and Monetary Policy Implications

The adoption of Dogecoin as a payment method raises interesting questions about monetary policy, currency competition, and the role of decentralized digital currencies in modern economic systems where traditional central bank controls and commercial banking intermediation face alternatives from cryptocurrency networks.

Velocity of money considerations become relevant as Dogecoin transitions from speculative asset to medium of exchange, with payment adoption potentially increasing circulation and reducing hoarding behaviors that affect the cryptocurrency’s monetary properties and economic utility.

Network effects from increasing Dogecoin payment adoption create positive feedback loops where merchant acceptance encourages consumer usage, which in turn motivates additional businesses to accept the cryptocurrency, potentially leading to sustainable growth in real-world utility.

Monetary sovereignty implications arise as businesses and consumers gain alternatives to traditional payment systems, potentially reducing dependence on central bank policies and commercial banking infrastructure while creating new forms of financial autonomy and choice.

International trade applications for Dogecoin payments could reduce reliance on traditional banking systems for cross-border transactions, though regulatory complexity and exchange rate considerations currently limit widespread adoption for international commercial applications.

Conclusion: The Path to Mainstream Adoption

Dogecoin’s evolution from internet meme to accepted payment method by major corporations demonstrates the potential for cryptocurrency to achieve mainstream adoption through community building, celebrity endorsement, practical utility, and strategic business implementation rather than purely technical innovation or financial speculation.

The success of companies like Tesla and AMC in implementing Dogecoin payments provides templates for other businesses considering cryptocurrency adoption, showing how proper technical implementation, customer education, and risk management can create successful digital currency payment programs.

The growing ecosystem of Dogecoin payment acceptance creates network effects that could drive continued adoption as consumers become more comfortable using cryptocurrency for everyday purchases and businesses recognize competitive advantages from offering digital currency payment options.

Future development of Dogecoin payment adoption will likely depend on continued improvements in user experience, regulatory clarity, technical infrastructure, and business integration tools that make cryptocurrency payments as convenient and reliable as traditional payment methods.

Understanding Dogecoin’s payment adoption success requires recognizing the importance of community enthusiasm, cultural relevance, and practical utility in driving cryptocurrency adoption beyond speculative trading toward real-world applications that provide genuine value for businesses and consumers in the evolving digital economy.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments, including Dogecoin, carry substantial risk of loss and extreme volatility. Past performance does not guarantee future results. Businesses should carefully evaluate technical, regulatory, and financial risks before implementing cryptocurrency payment systems. Readers should conduct their own research and consult with qualified financial and legal advisors before making any business or investment decisions. The author and publisher are not responsible for any financial losses that may result from acting on the information provided in this article.