TradingView Pine Script Reference

Understanding FDIC Coverage in the Digital Asset Era

The Federal Deposit Insurance Corporation has provided critical deposit protection for American consumers since 1933, but the emergence of cryptocurrency and digital assets has created significant confusion about what protections actually extend to crypto-related activities. Many cryptocurrency users operate under fundamental misunderstandings about FDIC insurance coverage, believing their digital assets receive the same protections as traditional bank deposits when the reality is far more nuanced and limited than most realize.

The intersection of traditional banking regulation and cryptocurrency represents one of the most complex areas of financial consumer protection, with various crypto platforms making claims about FDIC insurance that range from technically accurate but misleading to outright false. Understanding the precise boundaries of FDIC protection in cryptocurrency contexts requires examining the specific legal frameworks governing deposit insurance, the operational structures of different crypto platforms, and the evolving regulatory landscape that continues to reshape how digital assets interact with traditional financial systems.

Contemporary cryptocurrency platforms employ diverse business models and custody arrangements that create dramatically different risk profiles for user funds, yet many platforms market themselves using language that suggests broader FDIC protection than actually exists. The distinction between what is protected, partially protected, or completely unprotected often depends on technical details that are not clearly communicated to users, creating a dangerous information gap that can lead to significant financial losses when platforms fail or experience security breaches.

Traditional FDIC Insurance Fundamentals

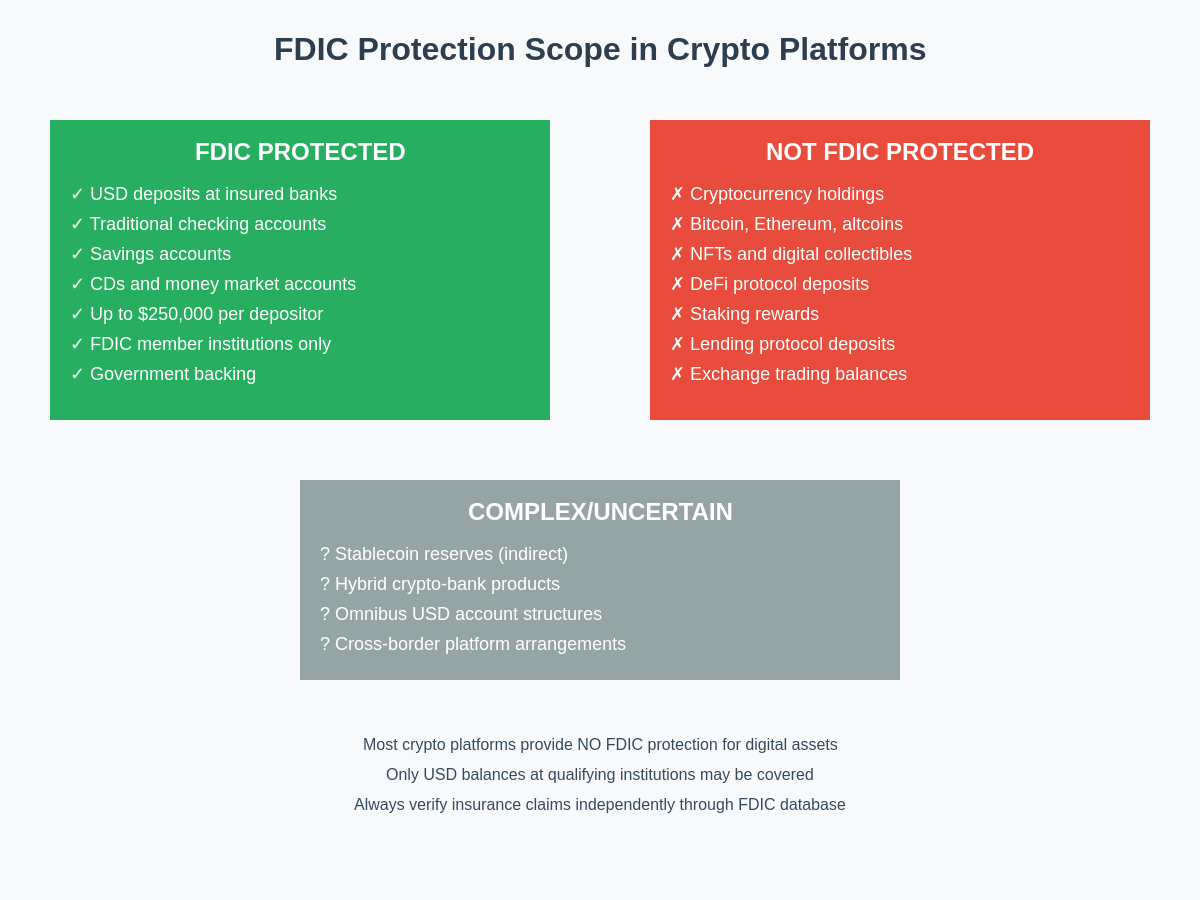

FDIC insurance operates under a comprehensive regulatory framework that provides up to $250,000 in protection per depositor, per insured bank, for each account ownership category, covering traditional deposit products including checking accounts, savings accounts, certificates of deposit, and money market accounts. This protection extends only to institutions that have obtained FDIC insurance and maintain compliance with federal banking regulations, creating a clearly defined universe of protected financial institutions and deposit products.

The FDIC’s deposit insurance fund draws resources from premiums paid by member banks and maintains the full faith and credit backing of the United States government, providing depositors with absolute confidence that covered deposits will be made whole even in the event of bank failure. This system has successfully protected millions of depositors through thousands of bank failures since its inception, creating the foundation of trust that enables the modern American banking system to operate effectively.

However, FDIC protection applies exclusively to deposits held at FDIC-insured institutions and does not extend to investment products, securities, cryptocurrencies, or other financial instruments even when these products are offered by FDIC-insured banks. The critical distinction lies in understanding that FDIC insurance covers deposits, not investments, and cryptocurrency holdings are generally classified as investments or digital assets rather than deposits under current regulatory frameworks.

Cryptocurrency Platform Structures and Insurance Claims

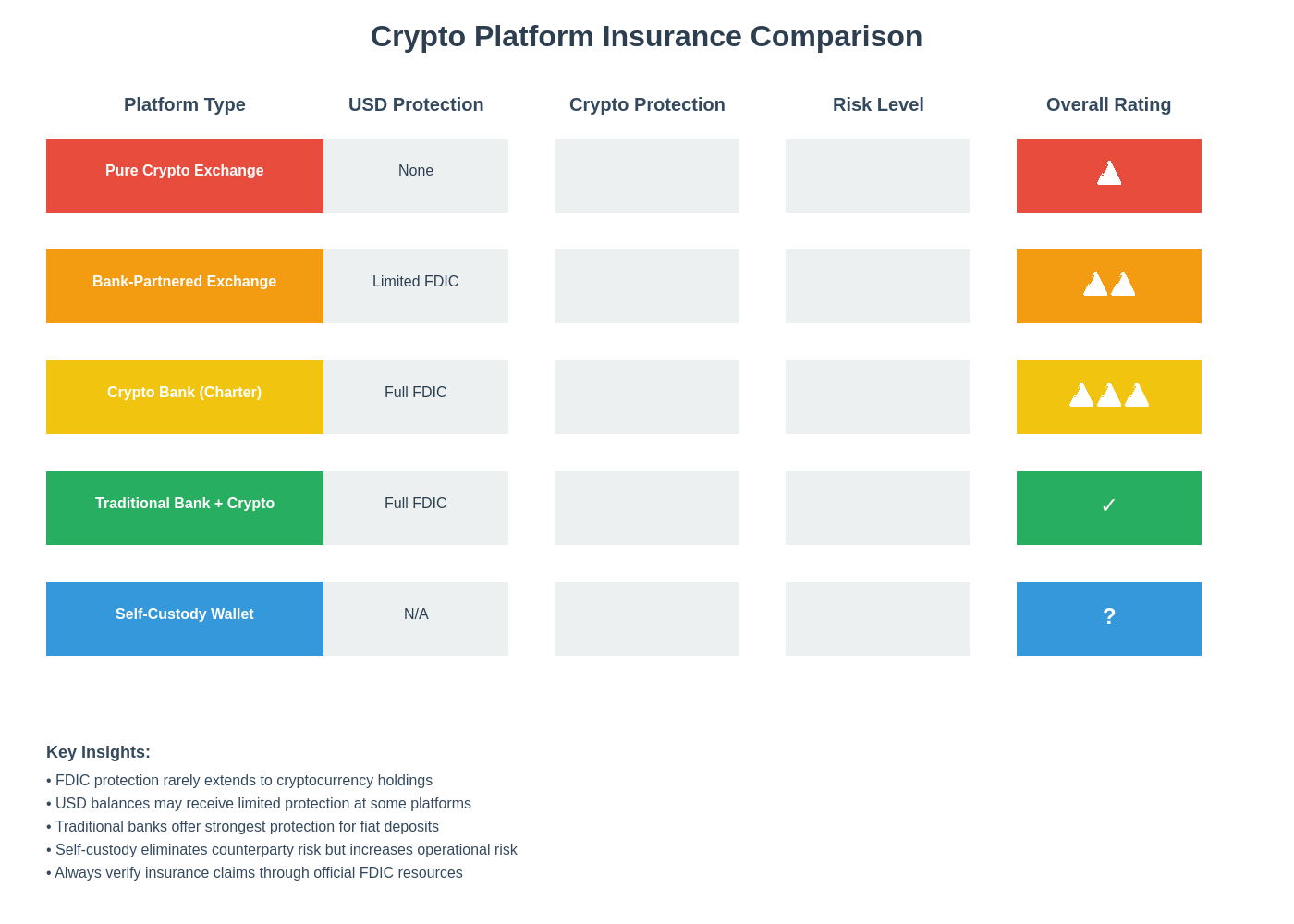

Cryptocurrency exchanges and platforms employ various business models that create different relationships between users and their funds, with some structures potentially qualifying for limited FDIC protection while others provide no traditional deposit insurance coverage whatsoever. Pure cryptocurrency exchanges that operate without banking partnerships typically provide no FDIC protection for user cryptocurrency holdings, as these platforms function more like brokerage services than traditional banks and cryptocurrency holdings are not considered deposits under federal banking law.

Some cryptocurrency platforms have established relationships with FDIC-insured banks to provide limited protection for US dollar deposits held on behalf of users, but this protection typically applies only to fiat currency balances and not to cryptocurrency holdings themselves. These arrangements often involve the platform maintaining omnibus accounts at FDIC-insured banks, where user dollar deposits are pooled together and theoretically protected up to applicable FDIC limits, though the practical implementation of such protection can be complex during platform failures.

Cryptocurrency platforms that obtain banking charters or partner with chartered banks may offer more comprehensive FDIC protection for certain products, but even these arrangements typically distinguish between traditional deposit products and cryptocurrency holdings. The marketing language used by these platforms often emphasizes their FDIC insurance status without clearly delineating which products and services actually receive deposit insurance protection, creating consumer confusion about the scope of coverage.

Understanding the specific legal structure of any cryptocurrency platform is essential for determining what protections actually apply to user funds, as seemingly similar platforms may offer dramatically different levels of FDIC coverage based on their regulatory status, banking partnerships, and operational models. The complexity of these arrangements means that users cannot rely on general assumptions about FDIC protection and must carefully review the specific terms and conditions governing their accounts.

Stablecoins and FDIC Protection Complexities

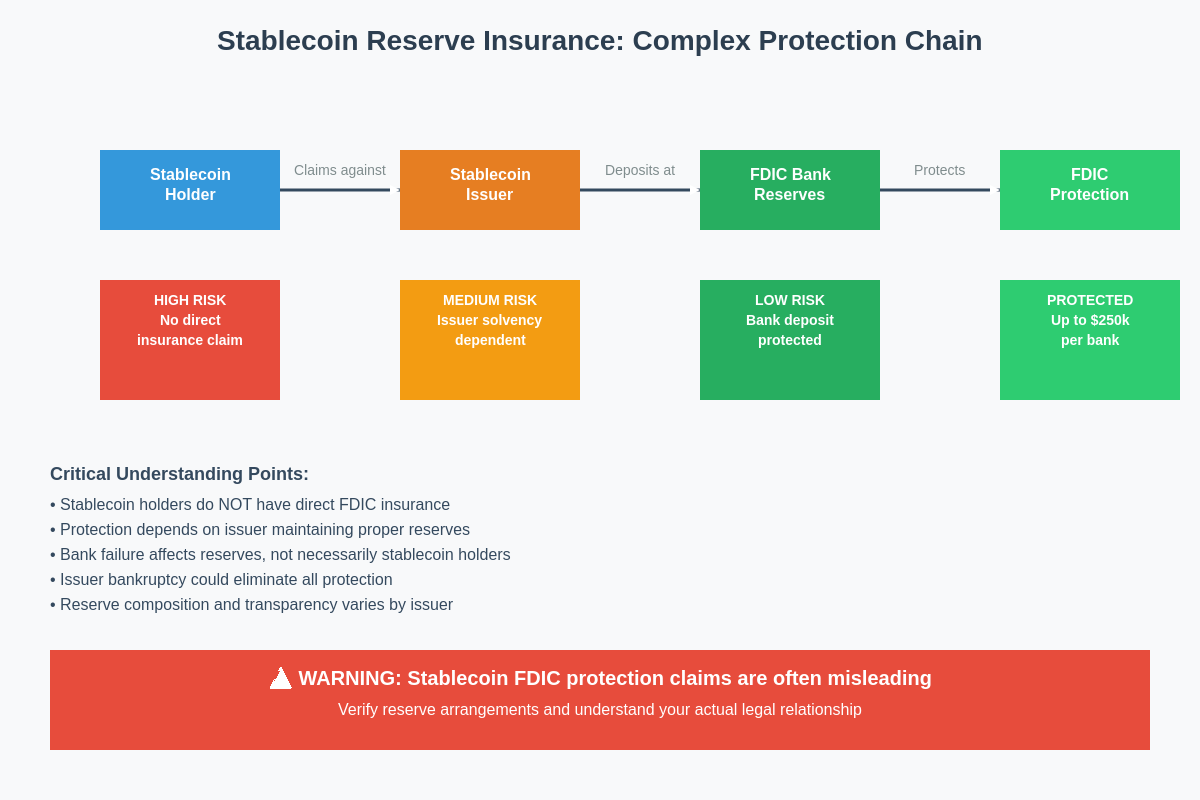

Stablecoins represent a particularly complex area of FDIC insurance discussion, with various stablecoin issuers claiming different levels of protection for the fiat currency reserves backing their digital tokens. Some stablecoin issuers maintain reserves at FDIC-insured banks and claim that these reserves provide indirect protection for stablecoin holders, but the legal relationship between stablecoin ownership and deposit insurance protection remains legally unclear and largely untested in practice.

The critical distinction lies in understanding that stablecoin holders typically do not have direct deposit relationships with FDIC-insured banks but rather hold claims against stablecoin issuers who may or may not maintain reserves at insured institutions. This indirect relationship creates significant uncertainty about whether FDIC protection would actually extend to stablecoin holders in the event of either bank failure or stablecoin issuer failure, as the insurance covers the issuer’s deposits but not necessarily the claims of individual stablecoin holders.

Different stablecoin issuers employ varying reserve management strategies, with some maintaining full US dollar reserves at FDIC-insured banks while others use combinations of cash, treasury securities, and other assets that may or may not qualify for FDIC protection. The transparency and verifiability of these reserve arrangements varies significantly across different stablecoin projects, creating additional uncertainty about the actual level of protection available to users.

TradingView USDT Price Chart analysis shows that stablecoin market confidence often reflects these underlying reserve and insurance uncertainties, with different stablecoins trading at varying premiums or discounts based on perceived stability and regulatory compliance of their underlying reserve structures.

The regulatory landscape surrounding stablecoin reserve requirements continues to evolve, with various federal and state agencies proposing different frameworks for ensuring adequate backing and consumer protection. These evolving regulations may eventually provide clearer guidance on FDIC protection for stablecoin holders, but current legal frameworks leave significant uncertainty about the scope and applicability of deposit insurance in stablecoin contexts.

Crypto Banking and Hybrid Models

The emergence of cryptocurrency-focused banks and hybrid financial institutions has created new categories of FDIC protection that combine traditional banking services with cryptocurrency capabilities, offering some products with full FDIC insurance while excluding cryptocurrency holdings from deposit insurance coverage. These institutions typically obtain traditional banking charters and FDIC insurance, then offer both conventional deposit products and cryptocurrency-related services under the same institutional umbrella.

Crypto banks generally provide standard FDIC protection for traditional deposit accounts, including checking and savings accounts denominated in US dollars, while maintaining separate non-insured services for cryptocurrency custody, trading, and related activities. The institutional separation between insured deposit services and uninsured cryptocurrency services creates operational complexity but allows these institutions to offer the benefits of FDIC protection for conventional banking needs while serving cryptocurrency users.

Some hybrid platforms offer innovative products that attempt to bridge traditional banking and cryptocurrency, such as accounts that automatically convert cryptocurrency deposits to US dollars for FDIC protection or services that provide cryptocurrency exposure while maintaining underlying fiat currency deposits. These products create complex risk profiles that require careful analysis to understand what protections actually apply to different components of user holdings.

The regulatory oversight of crypto banks involves multiple agencies including the FDIC, Office of the Comptroller of the Currency, and various state banking regulators, creating a complex compliance environment that can affect the scope and reliability of consumer protections. Users of crypto banking services must understand not only the FDIC insurance status of their specific accounts but also the regulatory standing of the institution itself.

Partnership models between cryptocurrency platforms and traditional banks create additional complexity, as the structure of these relationships determines whether and how FDIC protection applies to user funds. Some partnerships involve direct custody arrangements where user funds are held at FDIC-insured banks, while others involve more complex arrangements that may not provide direct deposit insurance protection despite involving insured institutions.

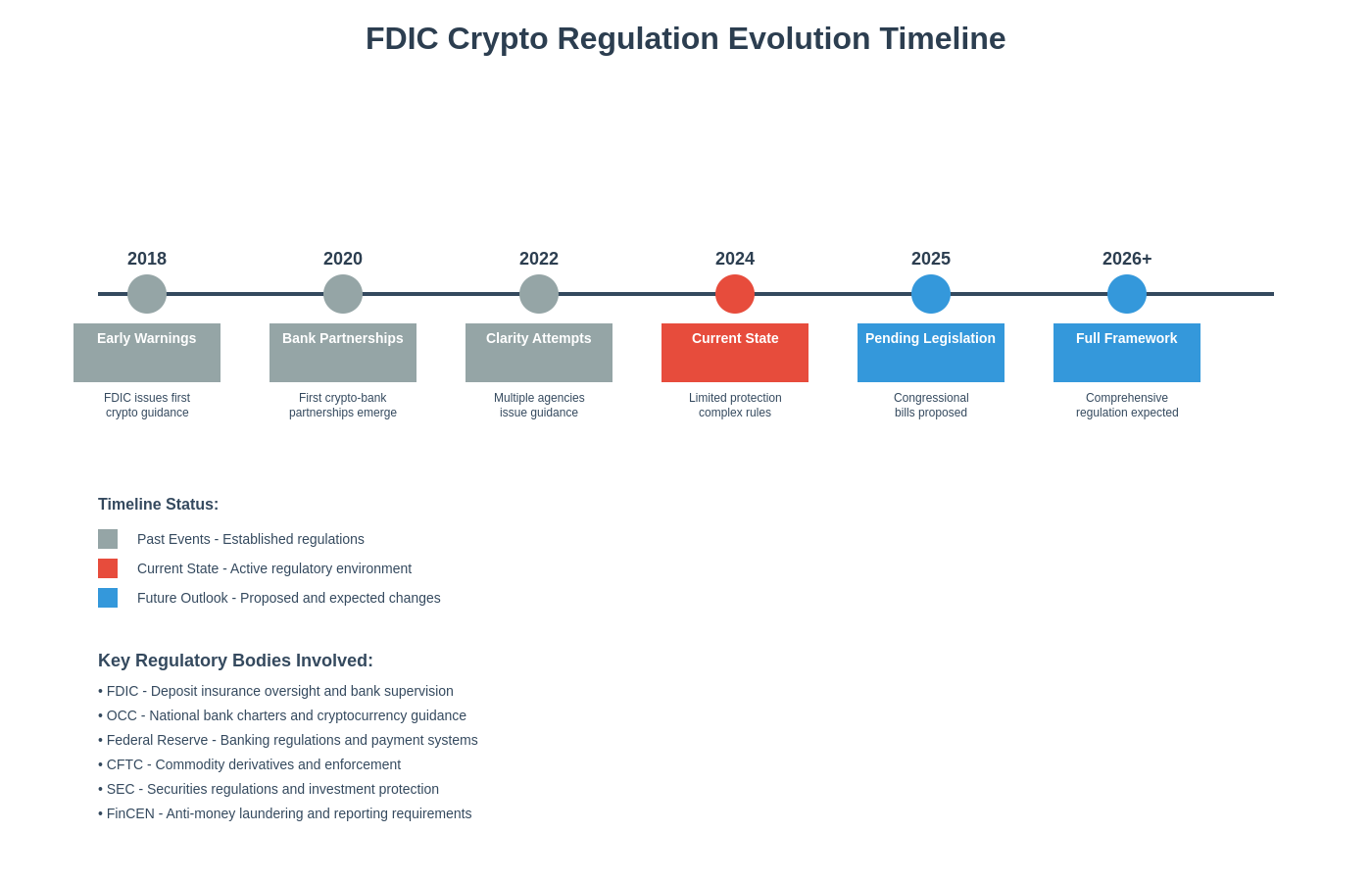

Regulatory Evolution and Future Protection Frameworks

The regulatory landscape governing FDIC protection for cryptocurrency-related activities continues to evolve rapidly, with various federal agencies developing new frameworks for digital asset oversight that may significantly change the scope of deposit insurance protection available to cryptocurrency users. The FDIC itself has issued guidance and policy statements regarding bank involvement in cryptocurrency activities, generally taking a cautious approach that emphasizes the risks associated with digital assets while acknowledging the potential for limited involvement under appropriate risk management frameworks.

Congressional consideration of cryptocurrency legislation includes various proposals for expanding or clarifying deposit insurance protection for digital assets, though the political and regulatory complexity of these issues makes the timeline and scope of any changes highly uncertain. Some proposals would extend FDIC-like protection to certain cryptocurrency activities, while others focus on creating separate regulatory frameworks that would operate alongside traditional deposit insurance without directly expanding FDIC coverage.

State-level regulatory developments also influence the landscape of cryptocurrency protection, with some states creating specialized charter types for cryptocurrency businesses that may include state-backed insurance or guarantee programs. These state-level initiatives operate independently of federal FDIC insurance but may provide alternative forms of consumer protection that serve similar functions for cryptocurrency users within specific jurisdictions.

The international regulatory environment affects US cryptocurrency protection frameworks, as global coordination on digital asset regulation influences domestic policy development and the competitive positioning of US-based cryptocurrency platforms. Regulatory developments in major jurisdictions like the European Union and United Kingdom create pressure for corresponding US developments that maintain the competitiveness of American cryptocurrency businesses while protecting consumers.

Industry self-regulatory initiatives and private insurance markets continue to develop alternative protection mechanisms that may supplement or compete with traditional FDIC insurance, including specialized cryptocurrency insurance products, industry guarantee funds, and enhanced custody practices designed to reduce the need for deposit insurance protection. These private sector developments may eventually create comprehensive protection frameworks that reduce reliance on traditional deposit insurance while providing equivalent or superior consumer protection.

Risk Assessment and Consumer Protection Strategies

Cryptocurrency users must develop sophisticated risk assessment capabilities to navigate the complex landscape of FDIC protection and alternative consumer protections, as the marketing claims made by various platforms often exceed the actual legal protections available to users. Effective risk assessment requires understanding the specific legal structure of each platform, the regulatory status of the institution, the custody arrangements for different types of assets, and the practical limitations of any insurance or protection claims.

Due diligence for cryptocurrency platform selection should include verification of FDIC insurance claims through direct consultation with FDIC databases and regulatory filings, as platforms sometimes make misleading claims about the scope or applicability of deposit insurance protection. The FDIC maintains public databases of insured institutions and regularly updates guidance on cryptocurrency-related activities, providing authoritative sources for verifying insurance claims and understanding regulatory restrictions.

Diversification strategies become particularly important in cryptocurrency contexts where FDIC protection may be limited or nonexistent, as concentrating large amounts of cryptocurrency holdings on any single platform creates significant counterparty risk regardless of insurance claims. Effective diversification may involve spreading holdings across multiple platforms, maintaining some funds in self-custody arrangements, and balancing cryptocurrency investments with traditional FDIC-insured deposits.

TradingView Bitcoin Analysis demonstrates the importance of understanding custody risks when evaluating cryptocurrency investments, as platform failures can result in total loss of funds regardless of the underlying performance of cryptocurrency assets themselves.

Consumer education initiatives from various sources including the FDIC, Consumer Financial Protection Bureau, and industry organizations provide ongoing guidance on cryptocurrency risks and protection strategies, though users must critically evaluate information sources and ensure they understand the current regulatory landscape rather than relying on outdated or incomplete guidance.

Legal recourse options for cryptocurrency users who experience losses due to platform failures or misleading insurance claims vary significantly based on the specific circumstances of each case, the jurisdiction involved, and the regulatory status of the platform. Understanding these legal options before problems arise can influence platform selection decisions and risk management strategies.

Insurance Alternatives and Private Protection Mechanisms

The limitations of FDIC protection in cryptocurrency contexts have sparked development of various alternative insurance and protection mechanisms, including specialized cryptocurrency insurance policies, self-insurance programs maintained by large platforms, and industry mutual insurance arrangements designed to provide coverage similar to FDIC protection for digital assets. These alternative mechanisms operate under different legal frameworks and provide varying levels of protection that may complement or substitute for traditional deposit insurance.

Commercial cryptocurrency insurance policies typically cover specific risks such as theft from hot or cold storage systems, employee fraud, and certain types of technical failures, but these policies often include significant exclusions and limitations that may not provide comprehensive protection equivalent to FDIC insurance. The cryptocurrency insurance market remains relatively immature compared to traditional deposit insurance, with limited competition among insurers and evolving policy terms that may change as the industry develops.

Platform-sponsored insurance and guarantee programs represent another category of protection mechanisms, where cryptocurrency platforms maintain insurance policies or reserve funds designed to protect user assets against various risks. These programs vary dramatically in their scope, funding levels, and legal enforceability, with some providing meaningful protection while others offer primarily marketing value without substantial financial backing.

Industry-wide initiatives such as mutual insurance arrangements and guarantee funds attempt to create collective protection mechanisms that spread risks across multiple platforms and participants, potentially providing more stable and comprehensive protection than individual platform insurance programs. These collective arrangements face significant coordination challenges and regulatory uncertainties that affect their viability and effectiveness.

Self-custody arrangements eliminate counterparty risks associated with platform failures but create different categories of risk related to private key management, technical security, and operational complexity. While self-custody provides complete control over cryptocurrency assets, it also places full responsibility for security and protection on individual users, making it unsuitable for many users who lack technical expertise or risk tolerance for self-managed security.

The evolution of decentralized finance protocols has created new categories of risk and protection mechanisms, including algorithmic insurance protocols, decentralized autonomous insurance organizations, and smart contract-based protection mechanisms that operate without traditional insurance companies or regulatory oversight. These innovative protection mechanisms offer potential advantages in terms of transparency and automation but also create new categories of technical and governance risks.

Platform Failure Case Studies and Lessons Learned

Historical cryptocurrency platform failures provide critical insights into the practical limitations of FDIC protection claims and the real-world consequences of inadequate consumer protection frameworks, with major collapses demonstrating how regulatory gaps and misleading marketing can result in massive consumer losses despite seemingly adequate protection mechanisms. The analysis of these failures reveals common patterns in how platforms misrepresent insurance coverage and how consumers can better protect themselves against similar risks.

The collapse of FTX represented one of the most significant cryptocurrency platform failures in history, highlighting how platforms with seemingly sophisticated risk management and regulatory compliance could still result in total loss of user funds despite various protection claims. The FTX case demonstrated that platform marketing claims about segregated customer funds and protection mechanisms may not reflect actual operational practices, and that regulatory gaps can leave consumers with limited recourse even when platforms appear to operate under appropriate oversight.

Celsius Network’s bankruptcy illustrated how cryptocurrency lending platforms can fail despite maintaining relationships with traditional financial institutions and making various claims about asset protection and insurance coverage. The Celsius case showed how complex platform structures can obscure actual risk levels and how traditional bankruptcy procedures may not provide adequate protection for cryptocurrency users who believed their assets were protected by various insurance or guarantee mechanisms.

The collapse of Silicon Valley Bank and its impact on cryptocurrency platforms demonstrated how traditional banking failures can cascade into cryptocurrency markets and affect platforms that claimed FDIC protection for certain activities. This case highlighted the importance of understanding the specific nature of bank relationships and how deposit insurance protection may not extend to all activities conducted by cryptocurrency platforms that maintain banking partnerships.

Smaller platform failures and exit scams provide additional lessons about due diligence and risk assessment, showing how platforms with limited regulatory oversight or questionable business models can disappear with user funds regardless of insurance claims or apparent legitimacy. These cases demonstrate the importance of verifying regulatory status and understanding the legal recourse available in different jurisdictions.

Recovery efforts following platform failures reveal the practical limitations of various protection mechanisms and the challenges users face in recovering funds even when some form of insurance or guarantee exists. The complexity of cryptocurrency recovery proceedings and the limited legal precedents in this area create significant uncertainty about outcomes even for users who believe they have adequate protection.

Regulatory Arbitrage and Cross-Border Implications

The global nature of cryptocurrency markets creates opportunities for regulatory arbitrage that can affect the applicability and effectiveness of FDIC protection and other consumer safeguards, as platforms may structure their operations across multiple jurisdictions to optimize regulatory treatment while potentially reducing consumer protections. Understanding these cross-border implications is essential for cryptocurrency users who may unknowingly be subject to foreign regulation or reduced protection when using platforms that appear to be domestic.

Offshore cryptocurrency platforms often market to US users while operating under foreign regulatory frameworks that may provide different levels of consumer protection than domestic alternatives, creating confusion about which regulatory protections actually apply to specific user relationships. The marketing practices of these platforms may emphasize aspects of their operations that suggest US regulatory compliance without clearly disclosing the limitations of foreign regulatory oversight or the reduced availability of US consumer protections.

International banking relationships used by cryptocurrency platforms create additional complexity regarding FDIC protection, as platforms may maintain accounts at foreign banks or use correspondent banking relationships that affect the applicability of US deposit insurance. Users must understand not only the regulatory status of the cryptocurrency platform itself but also the jurisdiction and regulatory status of any banks or financial institutions involved in custody or payment processing activities.

The extraterritorial application of US financial regulations creates additional uncertainty about protection availability for US users of foreign cryptocurrency platforms, as some US regulatory protections may apply even to foreign platforms serving US customers while others may not extend beyond US borders. This complex legal landscape requires careful analysis of specific platform structures and user agreements to determine what protections actually apply.

Cross-border enforcement challenges affect the practical availability of consumer protections even when theoretical legal rights exist, as pursuing remedies against foreign platforms or recovering assets held in foreign jurisdictions can be complex, expensive, and uncertain. These enforcement limitations may make theoretical protections practically unavailable to many users, regardless of the formal legal framework governing their relationships with cryptocurrency platforms.

Emerging international coordination efforts on cryptocurrency regulation may eventually create more consistent protection frameworks across jurisdictions, but current international regulatory disparities create significant uncertainty and potential protection gaps for users of global cryptocurrency platforms. Users must navigate these international complexities as part of their overall risk assessment and platform selection processes.

Future Outlook and Emerging Protection Frameworks

The future landscape of FDIC protection for cryptocurrency activities will likely be shaped by ongoing regulatory development, technological innovation, and market evolution that could significantly expand or modify current protection frameworks while creating new categories of risk and consumer safeguard. Understanding emerging trends and potential regulatory changes can help cryptocurrency users anticipate future protection opportunities and adjust their risk management strategies accordingly.

Central bank digital currency development represents a significant potential change in the cryptocurrency protection landscape, as government-issued digital currencies could provide FDIC-equivalent protection for digital assets while competing with private cryptocurrency platforms and stablecoins. The design and implementation of any US central bank digital currency will likely influence broader regulatory approaches to cryptocurrency protection and may create new standards for consumer safeguards in digital asset contexts.

Congressional and regulatory agency consideration of comprehensive cryptocurrency legislation may eventually create specialized protection mechanisms for digital assets that operate alongside or integrate with traditional FDIC insurance frameworks, though the political complexity of cryptocurrency regulation makes the timeline and scope of such developments highly uncertain. Proposed legislation includes various approaches to consumer protection ranging from extending existing frameworks to creating entirely new regulatory structures.

Technological developments in cryptocurrency custody and security may reduce the need for traditional deposit insurance by creating more secure and reliable self-custody options, decentralized custody arrangements, and algorithmic protection mechanisms that provide equivalent security without relying on traditional financial institutions. These technological solutions could eventually create comprehensive protection frameworks that operate independently of traditional banking regulation.

TradingView Crypto Market Analysis indicates that market maturation and institutional adoption continue to drive demand for enhanced consumer protection mechanisms, potentially accelerating regulatory development and private sector innovation in cryptocurrency protection frameworks.

The competitive dynamics of the cryptocurrency industry will likely drive continued innovation in consumer protection mechanisms as platforms seek to differentiate themselves through enhanced security and protection offerings, potentially creating market-driven solutions that exceed regulatory minimums and provide comprehensive consumer safeguards even in the absence of traditional deposit insurance.

Industry consolidation and the emergence of systemically important cryptocurrency institutions may trigger enhanced regulatory oversight and protection requirements similar to those applied to traditional banks, potentially extending FDIC-like protections to major cryptocurrency platforms while creating new categories of regulatory compliance and consumer safeguards.

The integration of cryptocurrency services into traditional banking institutions will likely continue to expand the scope of FDIC protection available for certain cryptocurrency-related activities while maintaining clear distinctions between protected deposit products and unprotected investment activities. This integration may eventually create hybrid protection frameworks that combine traditional deposit insurance with specialized cryptocurrency safeguards.

TradingView Pine Script Reference

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Cryptocurrency investments carry significant risks, including potential total loss of principal. FDIC insurance coverage is complex and may not apply to cryptocurrency holdings. Readers should conduct their own research, verify all insurance claims independently, and consult with qualified financial and legal professionals before making investment decisions. The regulatory landscape for cryptocurrency is rapidly evolving, and current protections may change without notice. Past performance does not guarantee future results, and all investments involve risk of loss.