Explore advanced financial analytics on TradingView

The Allure of Double-Digit Returns

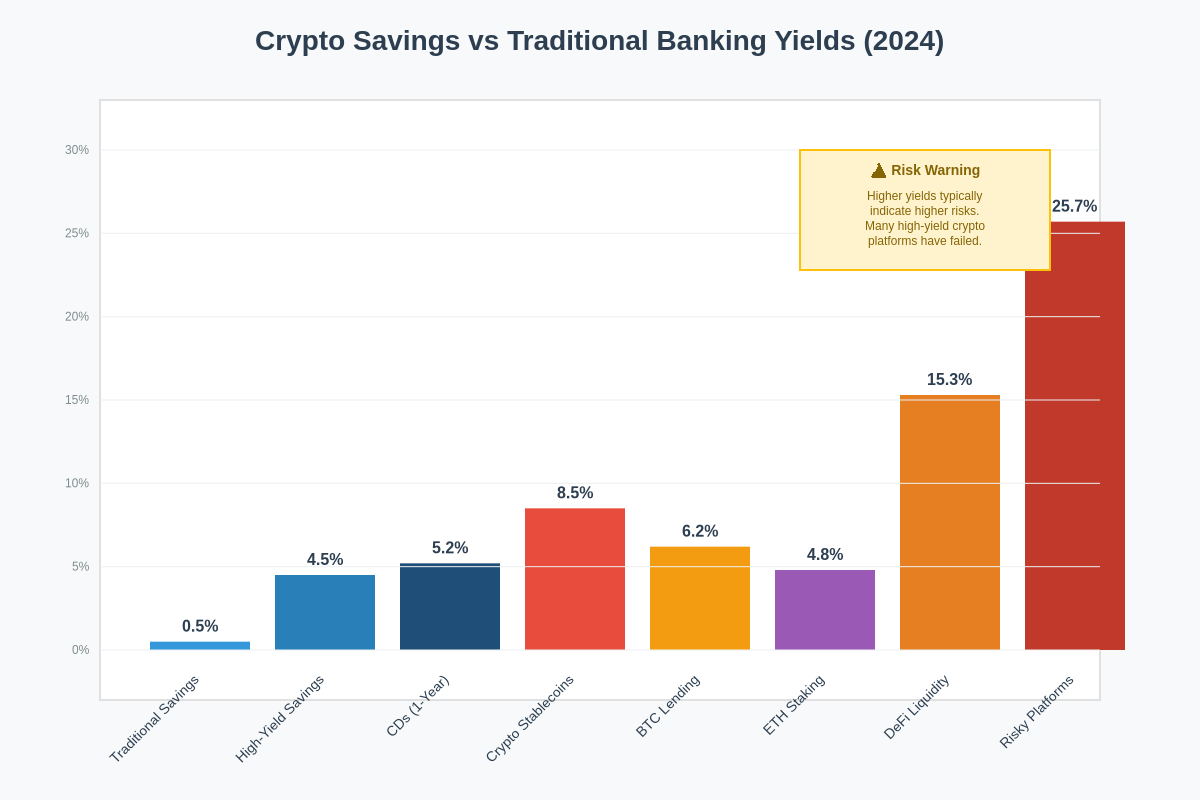

The cryptocurrency lending and savings market has exploded into a multi-billion dollar industry offering yields that traditional financial institutions simply cannot match, with some platforms promising annual percentage yields exceeding 20% on popular cryptocurrencies like Bitcoin and Ethereum. These astronomical returns have attracted millions of investors seeking alternatives to traditional savings accounts that offer minimal interest rates, often below the rate of inflation, making crypto savings accounts appear as attractive solutions for wealth preservation and growth.

The fundamental appeal of high-yield crypto savings accounts stems from their promise to generate passive income from cryptocurrency holdings without requiring active trading or deep technical knowledge of complex DeFi protocols. Users can simply deposit their digital assets and watch their balances grow through daily or weekly compound interest payments, creating an appealing proposition for both cryptocurrency veterans and newcomers seeking exposure to digital asset yields.

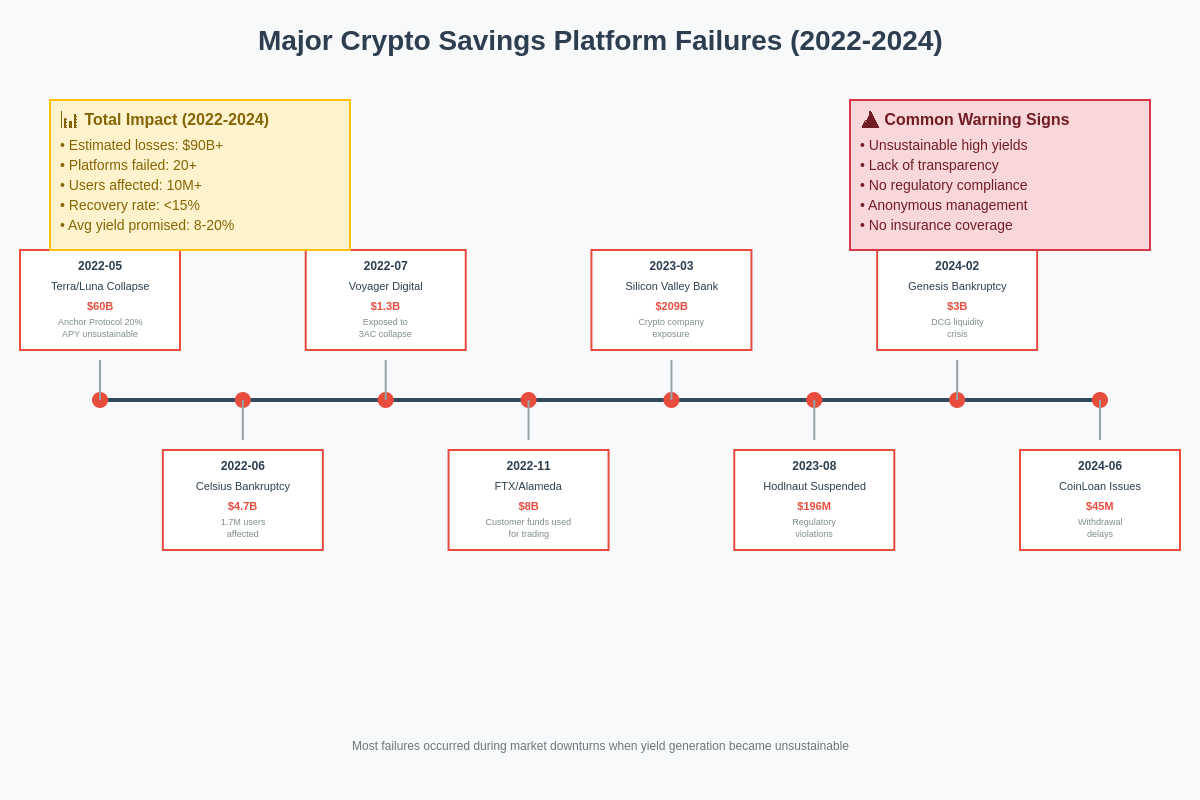

However, the sustainability and safety of these extraordinary returns remain subjects of intense debate among financial experts, regulators, and industry participants. The question of whether these yields represent genuine value creation or unsustainable financial engineering has become increasingly relevant as the market has matured and several high-profile platforms have collapsed, taking billions in user funds with them.

The traditional banking sector’s inability to offer competitive yields on deposits has created a significant opportunity gap that cryptocurrency platforms have rushed to fill. While traditional savings accounts in developed markets often offer less than 1% annual interest, crypto savings platforms routinely advertise yields of 8-15% on stablecoins and even higher rates on volatile cryptocurrencies, creating an apparent arbitrage opportunity that seems almost too good to be true.

Understanding the Yield Generation Mechanisms

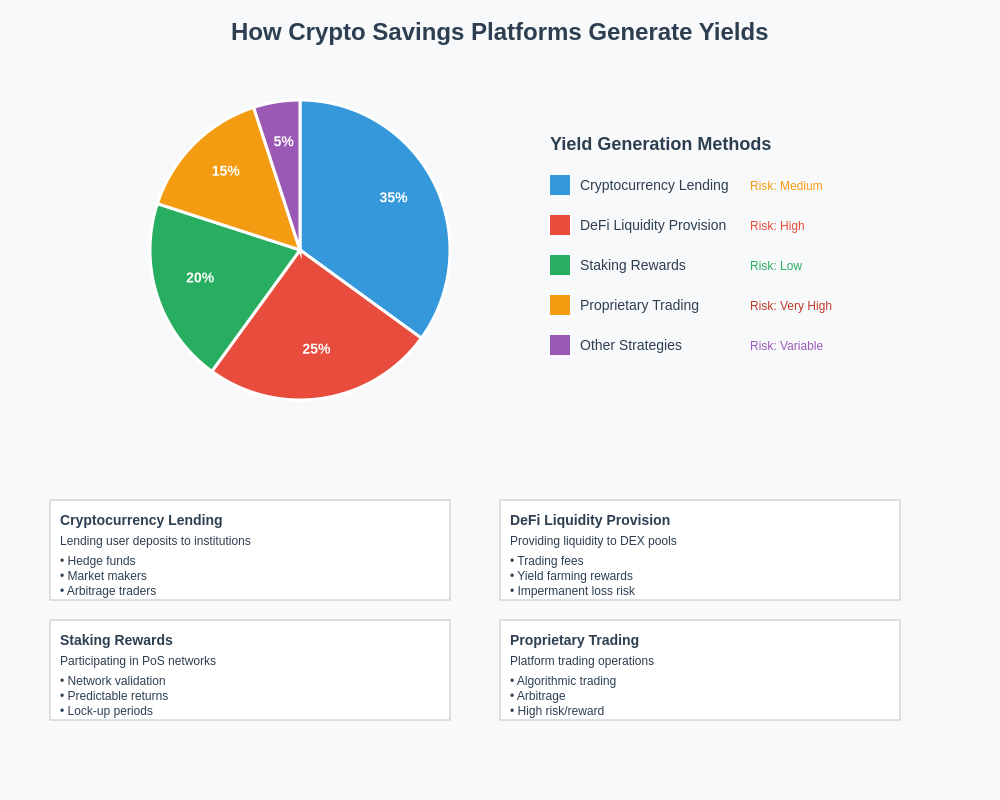

The mechanics behind high-yield crypto savings accounts vary significantly depending on the platform’s business model, risk tolerance, and underlying financial strategies employed to generate returns for depositors. Most platforms combine multiple yield generation strategies including cryptocurrency lending to institutional borrowers, liquidity provision to decentralized exchanges, staking rewards from proof-of-stake networks, and proprietary trading activities that aim to generate consistent profits from market inefficiencies.

Cryptocurrency lending represents one of the most straightforward yield generation mechanisms, where platforms lend user deposits to institutional borrowers, hedge funds, and market makers who require cryptocurrency for various trading strategies including arbitrage, market making, and derivatives trading. These borrowers typically pay premium interest rates for access to cryptocurrency liquidity, particularly during periods of high market volatility when demand for borrowing increases substantially.

Liquidity provision strategies involve deploying user funds as liquidity on decentralized exchanges and automated market makers, earning fees from trading activity while potentially benefiting from yield farming rewards offered by various DeFi protocols. These strategies can generate substantial returns during periods of high trading volume but also expose depositors to impermanent loss risks and smart contract vulnerabilities that may not be fully disclosed or understood by retail investors.

Staking-based yield generation leverages proof-of-stake networks where cryptocurrency holders can earn rewards for participating in network security and validation processes. Platforms aggregate user deposits to meet staking minimums and share the resulting rewards, though this approach typically generates more modest yields compared to lending and liquidity provision strategies, often in the range of 4-12% annually depending on the specific network and staking parameters.

Proprietary trading strategies employed by some platforms involve using user deposits as capital for algorithmic trading, arbitrage operations, and market making activities conducted by professional trading teams. While these strategies can potentially generate substantial returns, they also introduce significant counterparty risks and require users to trust platform operators with complex trading decisions that may not always be profitable or properly risk-managed.

The complexity and interconnectedness of these yield generation mechanisms create opacity that makes it difficult for users to fully understand the risks associated with their deposits. Many platforms provide limited disclosure about their specific strategies, risk management practices, and the potential for losses, leaving users to make decisions based on advertised yields rather than comprehensive risk assessments.

Risk Assessment and Red Flags

The evaluation of risk in high-yield crypto savings accounts requires careful analysis of multiple factors including platform transparency, regulatory compliance, insurance coverage, liquidity provisions, and the sustainability of advertised yields under various market conditions. Many platforms that offer extraordinarily high yields often exhibit characteristics that should raise concerns among sophisticated investors, yet these warning signs are frequently overlooked by users focused primarily on potential returns.

Lack of transparency regarding yield generation strategies represents one of the most significant red flags in the crypto savings industry, with many platforms providing vague descriptions of their investment activities while promising specific return rates. Legitimate financial institutions typically provide detailed explanations of their investment strategies, risk management practices, and fee structures, whereas problematic crypto platforms often rely on marketing language and testimonials rather than substantive financial disclosure.

Unsustainable yield rates that significantly exceed what can be reasonably generated through legitimate financial activities should be viewed with extreme skepticism, particularly when platforms cannot provide clear explanations for how such returns are achieved consistently over time. Basic financial principles suggest that risk-free returns significantly above government bond yields require either substantial risk-taking or unsustainable business models that may eventually collapse.

Regulatory compliance issues plague many crypto savings platforms, with some operating in jurisdictions with minimal oversight while serving customers in regions with strict financial regulations. The lack of proper licensing, registration, and regulatory supervision creates significant risks for users, as these platforms may not be subject to the same consumer protections, capital requirements, and operational standards that govern traditional financial institutions.

Insurance coverage limitations represent another critical risk factor, as many crypto platforms either lack insurance entirely or provide coverage that is insufficient to protect all user deposits in the event of security breaches, operational failures, or business collapse. Even platforms that advertise insurance coverage often have policies with significant exclusions and limitations that may not provide the comprehensive protection that users expect.

Liquidity constraints can become problematic during periods of market stress when large numbers of users attempt to withdraw funds simultaneously, potentially creating liquidity crises that prevent platforms from meeting withdrawal requests. Some platforms have implemented withdrawal limits, processing delays, and other restrictions that can trap user funds during critical market periods when access to capital is most important.

The concentration of counterparty risk in crypto savings platforms creates systemic vulnerabilities that can result in total loss of user funds if platform operators engage in fraudulent activities, make poor investment decisions, or experience operational failures. Unlike traditional banking where deposits are typically insured by government agencies, crypto savings accounts often provide no meaningful recourse for users when platforms fail.

Regulatory Landscape and Compliance Issues

The regulatory environment surrounding crypto savings accounts remains fragmented and evolving, with different jurisdictions taking varying approaches to oversight and consumer protection in the digital asset lending space. This regulatory uncertainty creates significant challenges for both platform operators and users, as changing rules and enforcement actions can dramatically impact platform operations and user access to funds.

United States regulatory agencies including the Securities and Exchange Commission, Commodity Futures Trading Commission, and state banking regulators have taken increasingly aggressive enforcement actions against crypto lending platforms, arguing that many yield-bearing products constitute unregistered securities offerings that violate federal and state laws. These enforcement actions have resulted in significant fines, operational restrictions, and in some cases, complete shutdown of platform operations.

The classification debate surrounding crypto savings products centers on whether these offerings constitute securities, commodities, banking products, or entirely new financial instruments that require novel regulatory frameworks. This classification uncertainty creates compliance challenges for platforms and investment risks for users who may find their access to funds restricted by regulatory actions.

European Union regulations under the Markets in Crypto-Assets framework are establishing comprehensive rules for crypto service providers including specific requirements for custody, operational resilience, and consumer protection that may significantly impact how crypto savings platforms operate within EU jurisdictions. These regulations aim to provide greater consumer protection while maintaining innovation in the digital asset space.

Asian markets have adopted diverse regulatory approaches ranging from comprehensive bans on cryptocurrency activities to detailed licensing regimes that permit crypto savings platforms to operate under strict supervision. The fragmented nature of global crypto regulation creates arbitrage opportunities for platforms to jurisdiction shop while potentially exposing users to regulatory risks.

Compliance costs associated with meeting evolving regulatory requirements can significantly impact platform profitability and their ability to maintain high yield rates, as resources must be allocated to legal compliance, reporting, and operational changes rather than yield generation activities. These costs may ultimately be passed on to users through reduced yields or increased fees.

The potential for retrospective regulation represents an ongoing risk for crypto savings platforms and their users, as regulatory agencies may apply new rules to existing activities or determine that previously permitted activities were actually violations of existing laws. This regulatory overhang creates uncertainty that may impact platform operations and user confidence in the long-term viability of crypto savings products.

Platform Analysis and Due Diligence

Conducting comprehensive due diligence on crypto savings platforms requires evaluation of multiple factors including management team experience, operational transparency, financial stability, security practices, and regulatory compliance history. The decentralized and often pseudonymous nature of cryptocurrency markets makes traditional due diligence practices more challenging while simultaneously making thorough investigation more critical for user protection.

Management team backgrounds and track records provide important insights into platform credibility and operational competence, though many crypto platforms are operated by individuals with limited traditional financial services experience or regulatory compliance knowledge. Platforms with experienced management teams from traditional finance, proper licensing, and transparent operations generally present lower risks than those operated by anonymous teams or individuals with questionable backgrounds.

Financial stability assessment becomes particularly challenging in the crypto savings space due to limited financial disclosure requirements and the private nature of many platforms, making it difficult for users to evaluate whether platforms maintain adequate capital reserves, proper risk management practices, and sustainable business models. Some platforms provide limited financial information through audit reports or regulatory filings, though the quality and comprehensiveness of these disclosures varies significantly.

Security practices evaluation should include assessment of custody solutions, insurance coverage, operational security measures, and historical security incidents, though many platforms provide limited transparency about their security practices until after security breaches occur. Platforms that undergo regular security audits, maintain comprehensive insurance coverage, and provide detailed security disclosure generally demonstrate higher operational standards.

Technology infrastructure assessment involves evaluating platform reliability, scalability, and integration with underlying blockchain networks and DeFi protocols, as technical failures can result in user fund losses or extended periods where funds are inaccessible. Platforms with robust technical infrastructure, comprehensive backup systems, and experienced development teams generally provide more reliable service.

User experience and customer support quality can provide insights into platform operational competence and commitment to user satisfaction, though these factors should not be the primary determinants of platform selection. Effective customer support becomes particularly important during market stress periods when users may need assistance with withdrawals or account issues.

Community reputation and user feedback analysis can provide valuable insights into platform performance and potential issues, though online reviews and community discussions should be evaluated critically as they may be subject to manipulation or may not represent the full range of user experiences. Long-term users and industry experts often provide more reliable assessments than anonymous online reviews.

Economic Sustainability and Market Dynamics

The economic sustainability of high-yield crypto savings accounts depends on complex market dynamics including cryptocurrency lending demand, DeFi yield opportunities, staking rewards, and overall market conditions that can change rapidly and unpredictably. Understanding these underlying economic factors is essential for evaluating whether advertised yields represent sustainable long-term returns or temporary market anomalies.

Cryptocurrency lending markets experience significant volatility in demand and pricing based on factors including market volatility, institutional trading activity, regulatory developments, and overall cryptocurrency adoption trends. During periods of high market volatility, institutional demand for cryptocurrency borrowing typically increases, driving up lending rates and enabling platforms to offer higher yields to depositors.

DeFi yield opportunities fluctuate based on protocol adoption, governance decisions, token incentive programs, and overall decentralized finance ecosystem development, creating variability in the yields available to platforms that deploy user funds in these protocols. Many DeFi yield opportunities are subsidized by token rewards that may not be sustainable long-term as protocols mature and reduce incentive programs.

Market cycles significantly impact the sustainability of crypto savings yields, with bull markets typically generating higher yields through increased trading activity and lending demand, while bear markets often result in reduced yields and increased risk of platform failures. The cyclical nature of cryptocurrency markets suggests that consistently high yields may not be maintainable across different market conditions.

Competition among crypto savings platforms has intensified as the market has matured, potentially leading to yield compression as platforms compete for user deposits while facing similar underlying yield generation opportunities. This competitive dynamic may pressure platforms to take increased risks or employ unsustainable business models to maintain competitive yield rates.

Traditional financial institution entry into cryptocurrency services may impact the competitive landscape for crypto savings platforms, as established banks and investment firms bring greater regulatory compliance, insurance coverage, and operational resources while potentially offering lower but more sustainable yields. The institutionalization of cryptocurrency services may ultimately lead to yield normalization and improved consumer protection.

Economic incentive alignment between platforms and users varies significantly based on platform business models, with some platforms aligning interests through equity-like arrangements or transparent fee structures, while others may have incentive structures that prioritize platform profits over user returns. Understanding these incentive alignments is crucial for evaluating long-term platform sustainability.

Insurance and Consumer Protection

The insurance landscape for crypto savings platforms presents significant challenges and limitations compared to traditional banking deposit insurance, with most platforms offering limited or no meaningful insurance coverage for user deposits while advertising insurance in ways that may mislead users about the actual protection provided. Understanding the reality of insurance coverage is essential for accurate risk assessment of crypto savings products.

FDIC deposit insurance and similar government-backed deposit protection schemes do not cover cryptocurrency deposits or crypto savings accounts, leaving users without the safety net that protects traditional bank deposits up to specified limits. This fundamental difference in consumer protection represents one of the most significant risks associated with crypto savings accounts compared to traditional savings products.

Private insurance policies obtained by crypto platforms typically cover only specific risks such as theft from hot wallets or security breaches, while excluding coverage for business failure, management fraud, lending losses, or market-related losses that could result in total loss of user funds. These exclusions mean that insurance coverage may not provide protection against the most likely scenarios that could result in user losses.

Custodial insurance arrangements vary significantly among platforms, with some maintaining comprehensive coverage for assets under custody while others provide minimal or no custodial insurance, creating significant differences in user protection levels. Users should carefully review insurance disclosure documents rather than relying on marketing claims about insurance coverage.

Regulatory insurance requirements for crypto savings platforms are minimal or non-existent in most jurisdictions, contrasting sharply with traditional banking where comprehensive deposit insurance and capital requirements provide multiple layers of consumer protection. This regulatory gap creates significant consumer protection concerns for crypto savings account users.

Self-insurance approaches employed by some platforms involve maintaining capital reserves to cover potential losses, though the adequacy and availability of these reserves may not be independently verified or regulated, leaving users to trust platform representations about their financial strength and loss coverage capabilities.

Legal recourse options for users of failed crypto savings platforms are often limited and complex, involving potentially lengthy and expensive legal proceedings with uncertain outcomes, particularly when platforms operate across multiple jurisdictions or become insolvent. The lack of standardized resolution procedures for failed crypto platforms contrasts unfavorably with established procedures for traditional bank failures.

Technology Risks and Smart Contract Vulnerabilities

The technological infrastructure underlying crypto savings platforms introduces unique risks that are not present in traditional financial services, including smart contract vulnerabilities, blockchain network risks, key management challenges, and integration complexities that can result in permanent loss of user funds through technical failures rather than fraudulent activities.

Smart contract risks represent a fundamental challenge for crypto savings platforms that integrate with DeFi protocols, as bugs, vulnerabilities, or unexpected interactions in smart contract code can result in loss of funds even when platform operators act with complete integrity and competence. The immutable nature of blockchain technology means that smart contract errors often cannot be reversed or corrected after they occur.

Blockchain network risks including network congestion, consensus failures, hard forks, and security vulnerabilities can impact platform operations and user fund accessibility, particularly for platforms that operate across multiple blockchain networks with different technical characteristics and risk profiles. Network-specific risks require platforms to maintain expertise across multiple technical domains.

Key management and custody challenges become particularly complex for crypto savings platforms that must manage large quantities of cryptocurrency across multiple networks while maintaining security, operational efficiency, and regulatory compliance. Technical failures in key management systems can result in permanent loss of funds with no possibility of recovery.

Oracle dependencies create additional technical risks for platforms that rely on external data feeds for pricing, liquidation, and risk management decisions, as oracle failures or manipulation can trigger incorrect platform actions that result in user losses. The centralized nature of many oracle systems creates single points of failure in otherwise decentralized systems.

Integration complexity increases as platforms connect with multiple DeFi protocols, blockchain networks, and external services, creating numerous potential failure points and making it difficult to predict how system failures might cascade across interconnected components. The rapid pace of development in the cryptocurrency space means that platform integrations must constantly evolve to maintain functionality.

Upgrade and governance risks arise when platforms depend on external protocols that may change their operations, fee structures, or functionality through governance processes that platform operators cannot control, potentially impacting yield generation capabilities or introducing new risks that were not present when user funds were originally deposited.

Alternative Investment Strategies

The search for yield in the cryptocurrency space extends beyond centralized crypto savings platforms to include various alternative strategies that may offer different risk-return profiles while providing users with greater control over their funds and investment decisions. Understanding these alternatives is essential for making informed decisions about cryptocurrency yield generation strategies.

Direct DeFi participation allows users to interact with decentralized finance protocols without intermediary platforms, providing transparency into yield generation mechanisms while requiring users to manage technical risks and complexity independently. This approach eliminates counterparty risks associated with centralized platforms while requiring greater technical sophistication and active management.

Staking-as-a-Service platforms provide alternatives to crypto savings accounts by focusing specifically on proof-of-stake network participation, often offering more transparent yield mechanisms and lower risks compared to complex multi-strategy platforms. These services typically provide more predictable returns based on network staking rewards rather than lending or trading activities.

Cryptocurrency index investing and dollar-cost averaging strategies provide alternative approaches to cryptocurrency exposure that focus on long-term appreciation rather than yield generation, potentially offering better risk-adjusted returns for users who are primarily seeking cryptocurrency exposure rather than income generation.

Traditional financial products with cryptocurrency exposure including exchange-traded funds, futures contracts, and regulated investment vehicles may provide safer alternatives for users seeking cryptocurrency exposure without the risks associated with unregulated crypto savings platforms. These products typically offer lower yields but provide greater regulatory protection and transparency.

Self-custody yield strategies enable users to maintain control of their cryptocurrency while participating in various yield generation activities including direct protocol participation, lending, and liquidity provision, though these approaches require significant technical knowledge and active management to implement safely and effectively.

Portfolio diversification across multiple yield strategies and platforms can help mitigate concentration risks while providing exposure to different yield generation mechanisms, though diversification may also increase complexity and monitoring requirements while potentially reducing overall returns through spreading across multiple platforms with different fee structures.

Future Outlook and Industry Evolution

The future of crypto savings accounts will likely be shaped by regulatory developments, technological advances, institutional adoption, and market maturation processes that may fundamentally alter the risk-return characteristics of these products while potentially improving consumer protection and market stability.

Regulatory clarity development in major jurisdictions may provide greater consumer protection and operational stability for crypto savings platforms while potentially reducing yields as platforms invest in compliance infrastructure and operate under stricter capital and operational requirements. Clear regulatory frameworks may ultimately benefit the industry by increasing consumer confidence and enabling institutional participation.

Traditional financial institution integration into cryptocurrency services may normalize yields and improve consumer protection through established banking relationships, regulatory compliance, and deposit insurance coverage, though this institutionalization may also reduce the innovation and yield opportunities that have characterized the early cryptocurrency savings market.

Technological improvements including layer-2 scaling solutions, improved smart contract security practices, and better user interface design may reduce technical risks and improve user experience for crypto savings platforms while enabling new yield generation strategies and more efficient platform operations.

Central bank digital currency development may impact the competitive landscape for crypto savings platforms by providing government-backed digital currency alternatives that offer some benefits of cryptocurrency while maintaining traditional banking consumer protections and regulatory oversight.

Market maturation processes including improved price stability, reduced volatility, and increased institutional adoption may result in yield compression across cryptocurrency markets as risk premiums decline and market inefficiencies are reduced through increased participation and improved infrastructure.

Innovation in yield generation mechanisms including new DeFi protocols, cross-chain opportunities, and novel financial instruments may create new opportunities for crypto savings platforms while also introducing new risks that require careful evaluation and risk management practices.

Conclusion and Risk Management Recommendations

The evaluation of high-yield crypto savings accounts requires careful consideration of multiple risk factors including platform credibility, regulatory compliance, insurance coverage, technological risks, and economic sustainability, with users needing to balance potential returns against the significant risks associated with these largely unregulated financial products.

Due diligence practices should include thorough research of platform operators, regulatory status, insurance coverage, and yield generation mechanisms, with users avoiding platforms that lack transparency, regulatory compliance, or credible explanations for their advertised yields. The complexity and opacity of many crypto savings platforms make comprehensive due diligence challenging but essential for risk management.

Risk management strategies should include diversification across multiple platforms and strategies, limiting exposure to amounts that users can afford to lose completely, maintaining emergency funds in traditional savings accounts, and regularly monitoring platform developments and market conditions that may impact platform stability and yields.

Track cryptocurrency yields and market trends with professional tools

Regulatory development monitoring is essential as changing rules and enforcement actions can dramatically impact platform operations and user access to funds, with users needing to stay informed about regulatory developments in their jurisdictions and platform operating locations.

Conservative approach adoption may be appropriate for many users, with consideration of lower-yield but more transparent and regulated alternatives including traditional high-yield savings accounts, government bonds, and regulated cryptocurrency investment products that may offer better risk-adjusted returns than unregulated crypto savings platforms.

Exit strategy planning should include understanding withdrawal processes, potential limitations, and tax implications associated with crypto savings accounts, with users maintaining the ability to quickly exit positions if platform conditions deteriorate or market conditions change unfavorably.

The fundamental question of whether high-yield crypto savings accounts are “too good to be true” cannot be answered definitively, as individual platforms and market conditions vary significantly, though users should approach these products with healthy skepticism and comprehensive risk management practices given the numerous risks and uncertainties associated with this largely unregulated market sector.

Analyze crypto market fundamentals and technical indicators

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments and high-yield savings accounts involve significant risks including potential total loss of principal. Past performance does not guarantee future results. Always conduct thorough research and consider consulting with qualified financial advisors before making investment decisions. The regulatory status and consumer protections for cryptocurrency products vary by jurisdiction and may change without notice.