TradingView Analysis Platform provides essential tools for cryptocurrency compliance monitoring and transaction analysis that support institutional KYC requirements.

The Regulatory Foundation of Crypto Banking KYC

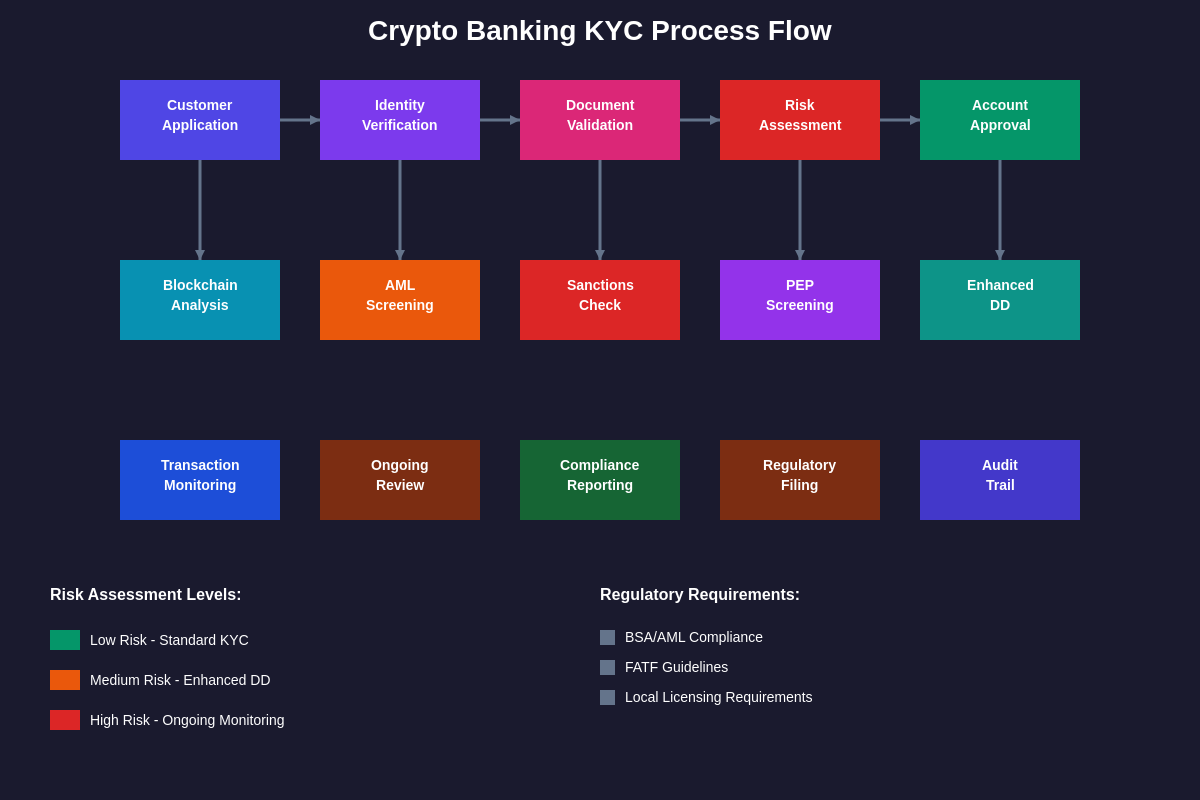

Know Your Customer requirements for centralized cryptocurrency banking institutions represent one of the most complex and rapidly evolving areas of financial regulation, as traditional banking compliance frameworks intersect with innovative blockchain technologies to create unprecedented challenges for both regulators and financial institutions. The fundamental principles of KYC in crypto banking extend far beyond simple identity verification to encompass comprehensive risk assessment, transaction monitoring, and ongoing due diligence that must account for the unique characteristics of digital assets and blockchain-based financial services.

The regulatory landscape governing KYC requirements for crypto banking varies significantly across jurisdictions, with different countries implementing vastly different approaches to digital asset compliance that reflect their broader regulatory philosophies and risk tolerance levels. In the United States, crypto banking institutions must comply with Bank Secrecy Act requirements, Anti-Money Laundering regulations enforced by FinCEN, and state-level money transmission licensing requirements that often include additional KYC obligations beyond federal minimums. European Union regulations under the Anti-Money Laundering Directive and Markets in Crypto-Assets Regulation establish comprehensive frameworks for crypto banking KYC that emphasize customer due diligence, beneficial ownership identification, and enhanced monitoring for high-risk transactions.

The technical implementation of KYC requirements in crypto banking environments presents unique challenges that traditional banking institutions rarely encounter, including the need to verify identities across multiple blockchain networks, monitor transactions that may involve privacy coins or mixing services, and maintain compliance while supporting innovative financial products like decentralized finance integrations. These challenges require crypto banking institutions to develop sophisticated compliance systems that can adapt to rapidly changing regulatory requirements while maintaining operational efficiency and customer satisfaction.

Traditional banking KYC frameworks rely heavily on established identity verification systems, credit reporting agencies, and standardized financial documentation that may not translate directly to cryptocurrency environments where customers may prefer privacy-preserving technologies or operate across multiple jurisdictions with different documentation standards. Crypto banking institutions must therefore develop hybrid approaches that combine traditional identity verification methods with blockchain-specific compliance tools and risk assessment frameworks designed specifically for digital asset transactions.

Identity Verification and Customer Onboarding

The customer onboarding process for centralized crypto banking institutions involves multiple layers of identity verification that must satisfy both traditional banking requirements and cryptocurrency-specific regulatory obligations while providing a user experience that meets customer expectations for digital financial services. Primary identity verification typically requires government-issued identification documents, proof of address, and biometric verification through secure digital channels that can authenticate customers without requiring in-person visits to physical banking locations.

Enhanced due diligence requirements for crypto banking customers often exceed those required for traditional banking relationships, reflecting regulatory concerns about the potential for digital assets to facilitate money laundering, terrorist financing, and other illicit activities. These enhanced requirements may include detailed source of funds documentation, employment verification, investment experience questionnaires, and ongoing monitoring of customer transactions that exceeds the typical surveillance applied to conventional banking relationships.

The technological infrastructure supporting crypto banking KYC processes must integrate with multiple data sources including government databases, sanctions lists, politically exposed person databases, and blockchain analytics platforms that can provide real-time transaction monitoring and risk assessment capabilities. Advanced cryptocurrency analysis tools enable institutions to perform comprehensive due diligence on customer wallet addresses and transaction histories before establishing banking relationships.

Cross-border customer verification presents particular challenges for crypto banking institutions that may serve customers across multiple jurisdictions with different identification requirements, privacy laws, and data protection regulations. These institutions must develop compliance frameworks that can accommodate varying documentation standards while maintaining consistent risk assessment processes and ensuring compliance with all applicable regulatory requirements in each jurisdiction where they operate.

Institutional customer onboarding for crypto banking services requires additional layers of verification including corporate documentation, beneficial ownership identification, board resolutions authorizing cryptocurrency activities, and compliance certifications that demonstrate the institution’s ability to meet regulatory requirements for digital asset custody and trading. These requirements reflect the increased regulatory scrutiny applied to institutional cryptocurrency activities and the potential for large-scale transactions to pose systemic risks to financial stability.

Risk Assessment and Customer Classification

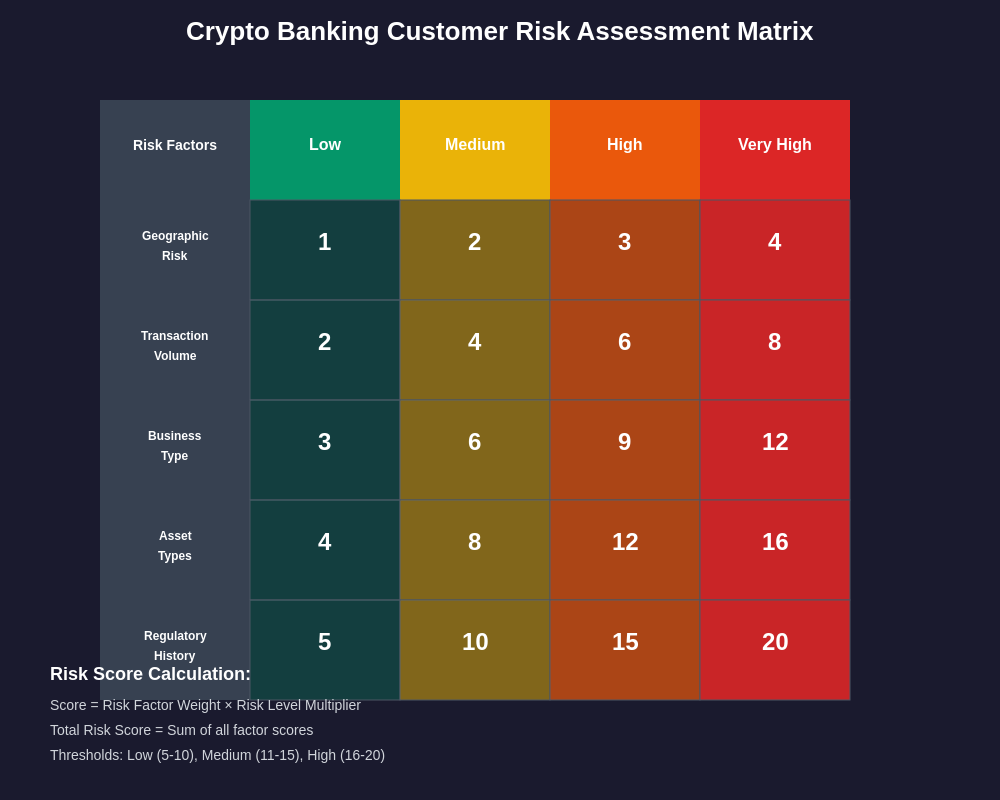

The risk assessment frameworks employed by centralized crypto banking institutions must account for factors that are largely irrelevant to traditional banking relationships while maintaining consistency with established anti-money laundering and know your customer regulatory requirements. Customer risk profiles in crypto banking environments must consider transaction patterns across multiple blockchain networks, exposure to high-risk jurisdictions through decentralized protocols, and the potential for customers to engage in activities that may not be clearly defined under existing regulatory frameworks.

Geographic risk assessment for crypto banking customers involves complex considerations that extend beyond simple country-of-residence classifications to include analysis of blockchain transaction patterns, exposure to jurisdictions with weak anti-money laundering frameworks, and potential connections to sanctioned entities through decentralized finance protocols or peer-to-peer trading platforms. These assessments require sophisticated analytics capabilities that can trace cryptocurrency movements across multiple blockchain networks and identify potential compliance risks that may not be apparent from traditional banking information.

Transaction volume and frequency analysis for crypto banking customers must account for the highly volatile nature of cryptocurrency markets, the potential for legitimate customers to engage in high-frequency trading strategies, and the challenges of distinguishing between legitimate arbitrage activities and potential money laundering schemes. Risk assessment frameworks must be calibrated to avoid excessive false positives that could disrupt legitimate customer activities while maintaining effective detection capabilities for genuinely suspicious transactions.

The classification of cryptocurrency assets for risk assessment purposes requires ongoing evaluation as new digital assets are developed and existing assets evolve in response to technological innovations and market dynamics. Different cryptocurrency assets present varying levels of privacy, regulatory compliance, and potential illicit use that must be reflected in customer risk profiles and transaction monitoring systems. Privacy-focused cryptocurrencies, for example, may warrant enhanced scrutiny regardless of other customer risk factors due to their potential to obscure transaction details that are essential for effective compliance monitoring.

Customer business model analysis for institutional crypto banking relationships requires deep understanding of cryptocurrency markets, blockchain technologies, and digital asset business operations that may not be familiar to traditional banking compliance personnel. Risk assessment frameworks must account for the legitimate business needs of cryptocurrency exchanges, mining operations, DeFi protocols, and other digital asset businesses while identifying potential compliance risks that may not be apparent to personnel without specialized cryptocurrency expertise.

Ongoing Monitoring and Transaction Surveillance

Continuous transaction monitoring for crypto banking customers requires real-time analysis of blockchain activity that extends far beyond the account-based monitoring systems used in traditional banking environments. Effective surveillance systems must track customer wallet addresses across multiple blockchain networks, identify connections to high-risk addresses or services, and detect patterns that may indicate money laundering, sanctions evasion, or other illicit activities while accounting for the legitimate complexity of modern cryptocurrency transaction flows.

The technical implementation of crypto banking transaction monitoring systems requires integration with multiple blockchain analytics platforms, sanctions screening services, and risk assessment tools that can provide comprehensive coverage of customer activities across the rapidly expanding universe of cryptocurrency networks and protocols. These systems must be capable of processing large volumes of transaction data in real-time while maintaining low false positive rates that avoid disrupting legitimate customer activities through excessive compliance investigations.

Threshold monitoring for crypto banking transactions must account for the extreme volatility of cryptocurrency markets that can cause routine transactions to cross traditional monetary thresholds during periods of rapid price appreciation or depreciation. Compliance systems must implement dynamic thresholds that adjust for market conditions while maintaining effective detection capabilities for genuinely suspicious activities that may attempt to exploit market volatility to evade detection.

Pattern recognition algorithms for crypto banking surveillance must be trained to identify cryptocurrency-specific money laundering techniques including layering through decentralized exchanges, structuring through multiple wallet addresses, and integration through legitimate cryptocurrency businesses. These algorithms must be continuously updated to account for evolving criminal methodologies while avoiding excessive false positives that could undermine customer relationships and operational efficiency.

Cross-platform monitoring capabilities are essential for effective crypto banking surveillance as customers may maintain activities across multiple cryptocurrency exchanges, DeFi protocols, and blockchain networks that could collectively indicate suspicious activity patterns even if individual transactions appear routine. Comprehensive market analysis tools provide essential insights for monitoring complex cryptocurrency transaction patterns and identifying potential compliance risks.

Regulatory Compliance Across Jurisdictions

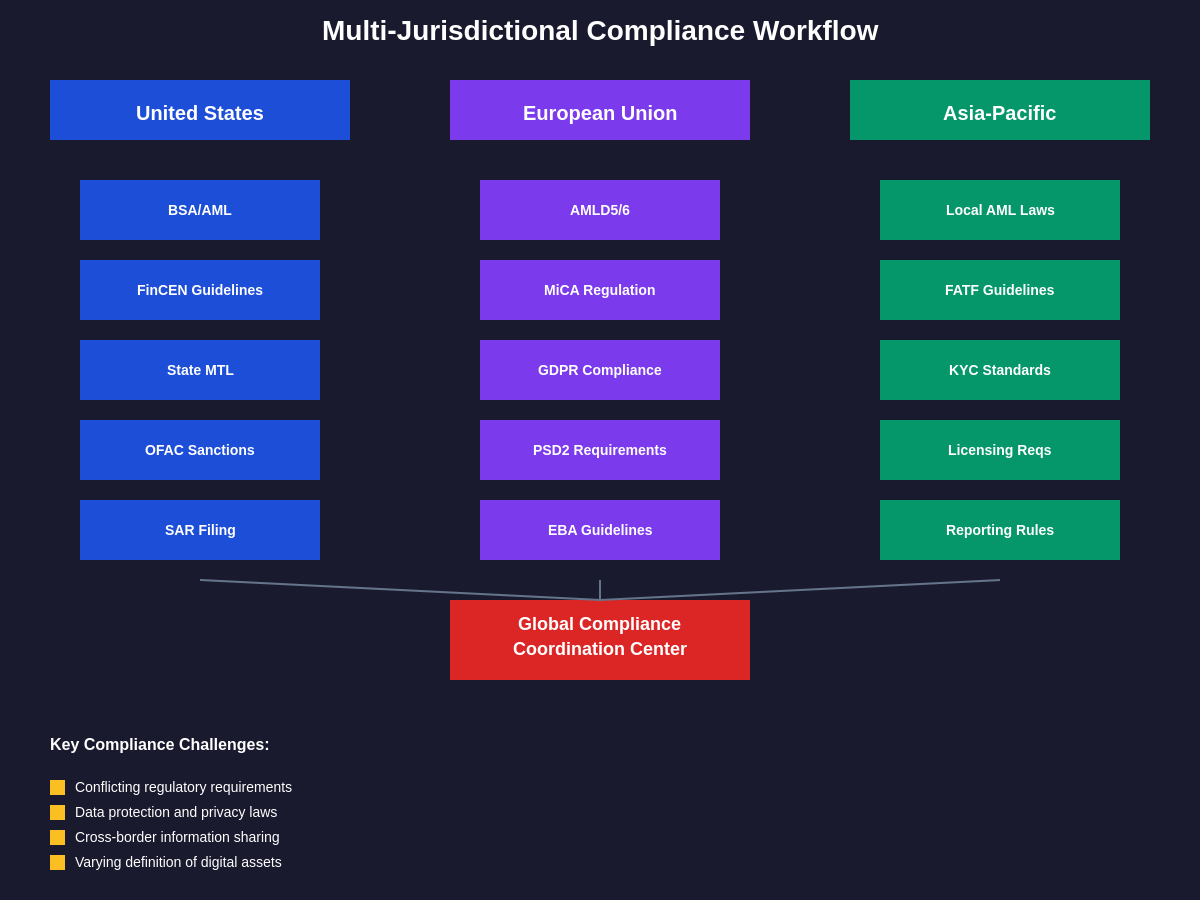

The multi-jurisdictional nature of cryptocurrency operations creates complex compliance challenges for centralized crypto banking institutions that must navigate varying regulatory requirements across different countries while maintaining consistent global compliance standards. These challenges are compounded by the rapid evolution of cryptocurrency regulations and the lack of international coordination on digital asset compliance standards that could provide clearer guidance for global crypto banking operations.

United States regulatory requirements for crypto banking institutions include compliance with federal anti-money laundering regulations, state money transmission licensing requirements, sanctions compliance obligations, and emerging regulations specific to cryptocurrency custody and trading activities. The fragmented nature of US cryptocurrency regulation, with oversight distributed across multiple federal agencies and varying state requirements, creates particular challenges for institutions seeking to provide comprehensive crypto banking services to US customers.

European Union regulatory frameworks for crypto banking are increasingly comprehensive, with the Markets in Crypto-Assets Regulation establishing detailed requirements for cryptocurrency service providers including enhanced KYC obligations, operational resilience requirements, and consumer protection measures. The implementation of MiCA across EU member states is creating more consistent regulatory requirements for crypto banking institutions operating in European markets while potentially influencing global regulatory standards through the Brussels Effect.

Asian regulatory approaches to crypto banking vary dramatically across the region, with some jurisdictions like Singapore and Hong Kong implementing comprehensive licensing frameworks for cryptocurrency businesses while others maintain more restrictive approaches that limit crypto banking activities. These varying approaches create challenges for institutions seeking to provide regional crypto banking services while requiring specialized compliance expertise for each jurisdiction.

Emerging market regulations for crypto banking often reflect broader financial inclusion objectives and may include provisions for simplified KYC requirements for smaller transactions or rural customers. However, these simplified requirements must be balanced against international compliance standards and correspondent banking relationships that may require enhanced due diligence regardless of local regulatory minimums.

Technology Infrastructure and Compliance Systems

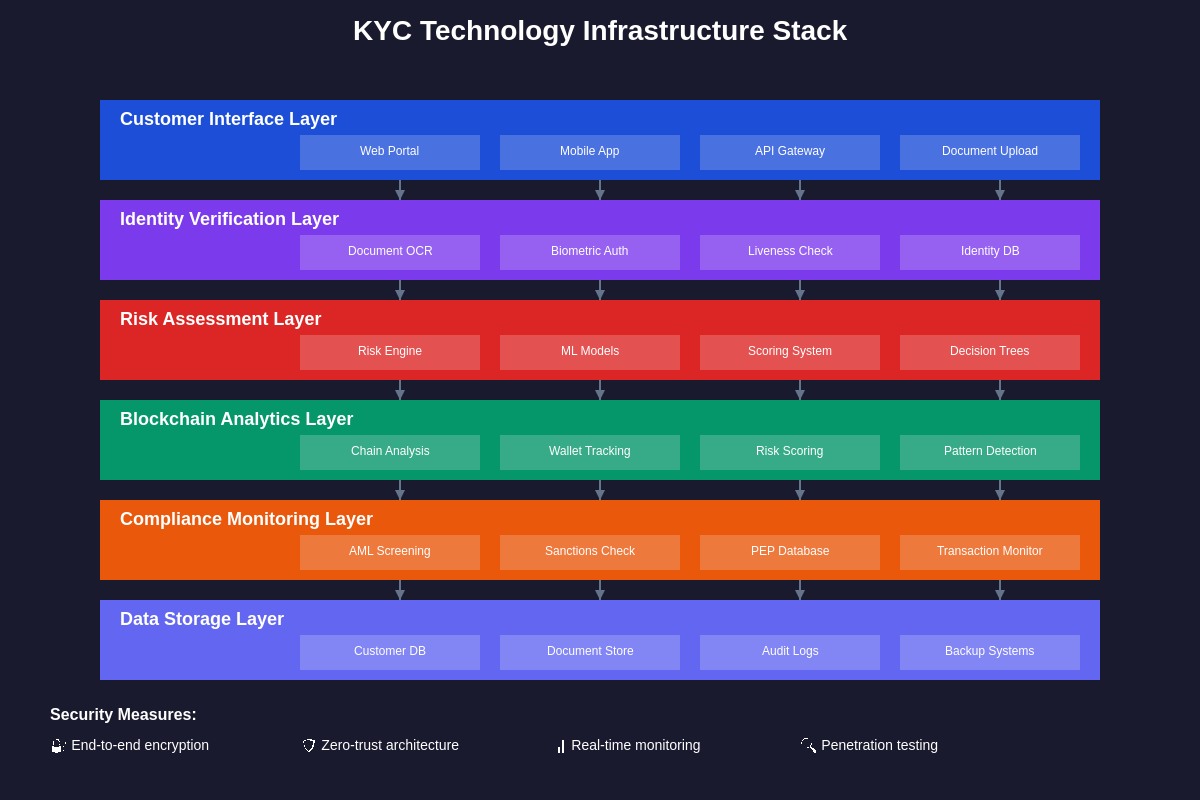

The technological infrastructure supporting KYC compliance for crypto banking institutions must integrate traditional banking compliance systems with specialized blockchain analytics tools, cryptocurrency-specific risk assessment platforms, and real-time monitoring capabilities that can provide comprehensive oversight of customer activities across multiple digital asset networks. This integration requires sophisticated data management systems that can process and analyze large volumes of blockchain transaction data while maintaining the security and reliability standards required for banking operations.

Identity verification technology for crypto banking must combine traditional document verification systems with blockchain-based identity solutions, biometric authentication methods, and advanced fraud detection capabilities that can identify synthetic identities and other sophisticated fraud schemes that may be more prevalent in cryptocurrency environments. These systems must be capable of verifying identities across multiple jurisdictions while complying with local privacy and data protection requirements that may limit the collection and use of personal information.

Blockchain analytics platforms serve as essential infrastructure for crypto banking compliance, providing capabilities to trace cryptocurrency transactions across multiple networks, identify high-risk addresses and services, and detect patterns that may indicate money laundering or other illicit activities. Leading platforms in this space offer real-time monitoring capabilities, comprehensive coverage of major cryptocurrency networks, and integration capabilities that allow seamless incorporation into existing compliance workflows.

Data management and storage systems for crypto banking compliance must accommodate the unique characteristics of blockchain data including immutable transaction records, pseudonymous addressing systems, and the potential for large volumes of transaction metadata that may be relevant for compliance analysis. These systems must provide long-term storage capabilities for compliance records while ensuring data security and privacy protection in accordance with applicable regulations.

Artificial intelligence and machine learning technologies are increasingly important for crypto banking compliance, providing capabilities to identify complex transaction patterns, detect emerging money laundering techniques, and reduce false positive rates in transaction monitoring systems. However, the implementation of AI-based compliance systems must account for regulatory requirements for explainable decision-making and the potential for algorithmic bias that could result in unfair treatment of certain customer segments.

Institutional Customer Requirements

Institutional customers for crypto banking services face enhanced KYC requirements that reflect the increased regulatory scrutiny applied to large-scale cryptocurrency activities and the potential for institutional transactions to pose systemic risks to financial stability. These requirements typically include comprehensive corporate documentation, beneficial ownership identification for complex corporate structures, board resolutions specifically authorizing cryptocurrency activities, and ongoing compliance certifications that demonstrate the institution’s ability to meet regulatory requirements for digital asset operations.

Corporate structure verification for institutional crypto banking customers requires detailed analysis of ownership structures that may span multiple jurisdictions and include complex arrangements designed to optimize tax efficiency or regulatory compliance. This analysis must identify all beneficial owners who meet regulatory threshold requirements while understanding the business purposes of complex structures and ensuring compliance with sanctions and politically exposed person requirements across all relevant jurisdictions.

Regulatory compliance documentation for institutional crypto banking customers must demonstrate that the institution has appropriate policies, procedures, and controls for cryptocurrency activities including anti-money laundering compliance, sanctions screening, market conduct requirements, and operational risk management. This documentation must be regularly updated to reflect changes in the institution’s activities and applicable regulatory requirements.

Investment policy and risk management documentation for institutional crypto banking customers must demonstrate appropriate governance oversight of cryptocurrency activities including board-level approval of investment strategies, risk limits for digital asset exposures, and procedures for monitoring and controlling cryptocurrency-related risks. These requirements reflect regulatory concerns about the volatility and complexity of cryptocurrency markets and the potential for institutions to incur losses that could affect their financial stability.

Third-party service provider due diligence for institutional crypto banking customers must include comprehensive evaluation of cryptocurrency custody providers, trading platforms, and other service providers that may have access to institutional digital assets or transaction information. This due diligence must assess the regulatory compliance, operational security, and financial stability of service providers while ensuring appropriate contractual protections for institutional assets and information.

Cross-Border Compliance Challenges

Cross-border compliance for crypto banking institutions involves navigating complex regulatory frameworks that may conflict with each other or create gaps in compliance coverage that could expose institutions to regulatory violations. The global nature of cryptocurrency networks means that transactions may involve multiple jurisdictions even when customers and institutions are located in a single country, creating challenges for determining applicable regulatory requirements and ensuring comprehensive compliance coverage.

Correspondent banking relationships for crypto banking institutions require enhanced due diligence that accounts for the unique risks associated with digital asset activities while meeting the compliance requirements of correspondent banks that may have limited experience with cryptocurrency operations. These relationships are essential for providing traditional banking services to crypto banking customers but may be difficult to establish and maintain due to correspondent bank concerns about cryptocurrency-related risks.

Data protection and privacy compliance for cross-border crypto banking operations must account for varying requirements across jurisdictions including the European Union’s General Data Protection Regulation, California’s Consumer Privacy Act, and other data protection frameworks that may limit the collection, use, and transfer of customer information. These requirements can create challenges for maintaining comprehensive compliance monitoring while respecting customer privacy rights.

Sanctions compliance for cross-border crypto banking operations requires sophisticated systems that can identify sanctioned individuals and entities across multiple jurisdictions while accounting for the pseudonymous nature of cryptocurrency transactions and the potential for sanctions evasion through decentralized protocols. Professional trading platforms provide essential tools for monitoring compliance across global cryptocurrency markets.

Tax reporting and information sharing requirements for cross-border crypto banking operations are increasingly complex as jurisdictions implement new reporting requirements for cryptocurrency transactions and automatic exchange of information agreements that may include digital asset activities. Compliance with these requirements requires sophisticated systems for tracking customer transactions and generating reports that meet varying jurisdictional requirements.

Emerging Technologies and Future Compliance

The integration of emerging technologies into crypto banking compliance systems presents both opportunities and challenges for meeting regulatory requirements while maintaining operational efficiency and customer satisfaction. Artificial intelligence and machine learning technologies offer significant potential for improving the accuracy and efficiency of KYC processes while reducing compliance costs and false positive rates that can disrupt customer relationships.

Central Bank Digital Currencies represent a significant development for crypto banking compliance as these government-issued digital assets may be subject to different regulatory requirements than private cryptocurrencies while offering enhanced transaction transparency that could simplify compliance monitoring. However, the implementation of CBDCs may also create new compliance challenges including privacy protection requirements and cross-border payment monitoring obligations.

Decentralized identity solutions are emerging as potential alternatives to traditional identity verification systems, offering enhanced privacy protection and customer control over personal information while potentially reducing compliance costs for crypto banking institutions. However, the regulatory acceptance of decentralized identity systems remains uncertain and their implementation must account for existing KYC requirements and due diligence obligations.

Zero-knowledge proof technologies offer potential for enhancing privacy protection in crypto banking compliance systems while maintaining necessary transparency for regulatory oversight. These technologies could enable compliance verification without revealing sensitive customer information, but their implementation requires careful consideration of regulatory requirements and technical capabilities.

Quantum computing developments present both opportunities and threats for crypto banking compliance systems, potentially offering enhanced analytical capabilities for transaction monitoring while also threatening the security of existing cryptographic systems that protect customer information and transaction data. Compliance systems must be prepared to adapt to quantum computing developments while maintaining security and regulatory compliance.

The evolution of regulatory frameworks for crypto banking continues to accelerate as governments worldwide develop more comprehensive approaches to digital asset regulation. Future compliance systems must be designed with sufficient flexibility to adapt to changing regulatory requirements while maintaining consistent risk management and customer protection standards. The convergence of traditional banking and cryptocurrency technologies will likely result in more integrated compliance approaches that leverage the benefits of both systems while addressing their respective risks and challenges.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or regulatory advice. Cryptocurrency regulations vary by jurisdiction and are subject to frequent changes. Readers should consult with qualified legal and compliance professionals before implementing any KYC procedures or compliance systems for cryptocurrency banking operations. The regulatory landscape for digital assets continues to evolve rapidly, and compliance requirements may differ significantly across jurisdictions and institution types.