The Revolution of Affordable DeFi Lending

Layer 2 scaling solutions have fundamentally transformed the decentralized finance landscape by making lending protocols accessible to users who were previously priced out by Ethereum mainnet’s prohibitive gas fees. The emergence of sophisticated lending platforms on Polygon and Arbitrum has created a new paradigm where borrowers and lenders can participate in yield farming, leveraged trading, and complex DeFi strategies without the burden of expensive transaction costs that once limited DeFi participation to large capital holders.

The revolution began as Ethereum’s transaction fees reached astronomical levels during periods of network congestion, with simple lending operations costing hundreds of dollars in gas fees during peak demand periods. This fee structure effectively excluded retail participants from DeFi lending protocols, creating a system that primarily served institutional users and whale investors who could absorb the high transaction costs. Layer 2 solutions emerged as the critical infrastructure needed to democratize DeFi lending by reducing transaction costs by up to 99% while maintaining the security guarantees of the underlying Ethereum blockchain.

The rapid growth of Layer 2 lending has attracted billions of dollars in total value locked across various protocols, with Polygon and Arbitrum leading the charge in terms of both adoption and innovation in the lending space. These networks have not only reduced costs but also enabled new types of lending products that were previously economically unfeasible on Ethereum mainnet, including micro-lending, frequent rebalancing strategies, and sophisticated automated yield farming protocols.

Understanding Layer 2 Scaling Technologies

Layer 2 scaling solutions represent a fundamental advancement in blockchain architecture that enables higher transaction throughput while maintaining the security and decentralization properties of the underlying Layer 1 blockchain. These solutions operate by processing transactions off the main Ethereum chain while periodically settling batches of transactions back to the mainnet, creating a system that combines the best aspects of both centralized efficiency and decentralized security.

Polygon utilizes a hybrid approach that combines Plasma chains, sidechains, and more recently, zero-knowledge rollups to achieve scalability while maintaining compatibility with Ethereum’s existing infrastructure. The Polygon network processes transactions using a modified proof-of-stake consensus mechanism that enables block times of approximately two seconds, dramatically reducing the time and cost associated with lending operations compared to Ethereum’s longer block times and auction-based fee structure.

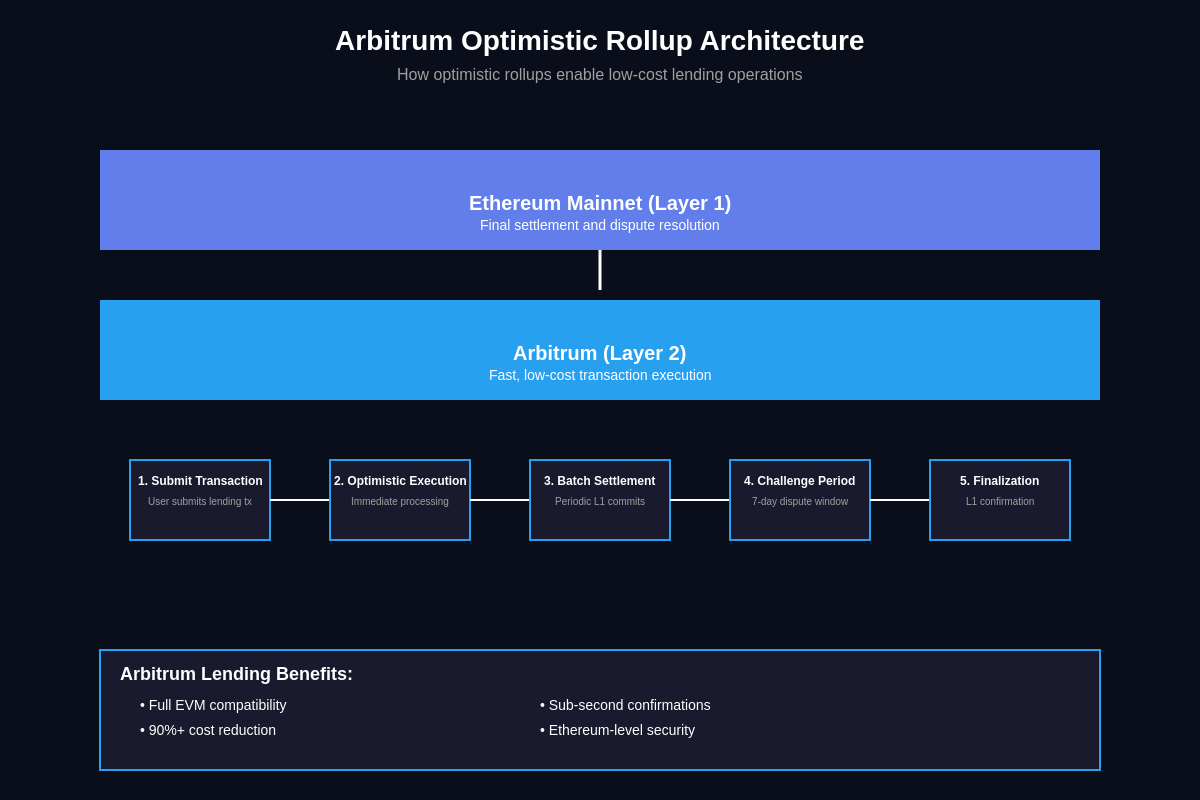

Arbitrum employs optimistic rollup technology that assumes transactions are valid by default while providing a challenge period during which invalid transactions can be disputed and reversed. This approach enables near-instant transaction finality for most operations while maintaining full compatibility with existing Ethereum smart contracts, allowing lending protocols to migrate to Arbitrum with minimal modifications to their existing codebase.

The technical implementation of these Layer 2 solutions involves complex cryptographic proofs and state management systems that ensure transaction integrity while achieving significant cost reductions. Zero-knowledge proofs, fraud proofs, and various cryptographic techniques work together to create systems where users can interact with lending protocols at a fraction of mainnet costs while maintaining the same level of security and decentralization that users expect from Ethereum-based protocols.

Polygon’s DeFi Lending Ecosystem

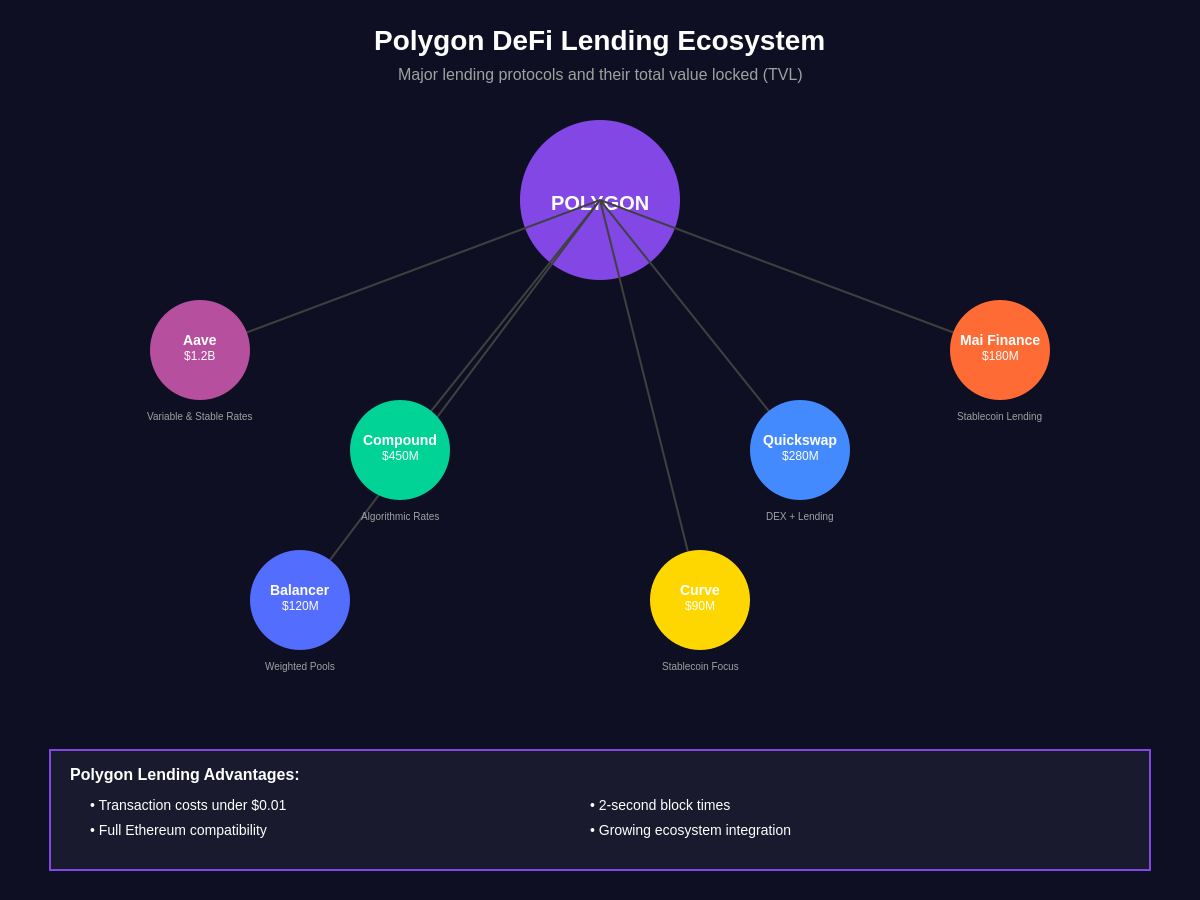

The Polygon network has emerged as one of the most vibrant ecosystems for DeFi lending, hosting a diverse array of protocols that cater to different user needs and risk profiles. Major lending platforms like Aave, Compound, and various native protocols have established significant presence on Polygon, creating a competitive environment that benefits users through improved rates, innovative features, and reduced barriers to entry.

Aave’s deployment on Polygon represents one of the most successful cross-chain lending implementations, offering users access to the same sophisticated lending features available on mainnet but at dramatically reduced costs. The protocol’s variable and stable rate borrowing options, flash loans, and collateral management features operate seamlessly on Polygon, enabling users to execute complex DeFi strategies that would be prohibitively expensive on Ethereum mainnet. The lower transaction costs have enabled new use cases such as frequent position rebalancing, small-scale yield farming, and automated liquidation protection strategies.

Native Polygon lending protocols have also flourished by taking advantage of the network’s unique characteristics and close integration with the broader Polygon ecosystem. These protocols often offer enhanced features such as cross-chain collateral management, integration with Polygon’s native staking mechanisms, and novel tokenomics that reward long-term protocol participation. The competitive landscape has driven innovation in areas such as dynamic interest rate models, automated yield optimization, and sophisticated risk management systems.

The integration between different Polygon DeFi protocols creates a synergistic ecosystem where lending platforms can leverage liquidity from decentralized exchanges, yield farming protocols, and other DeFi primitives. This interconnectedness enables users to build complex financial strategies that combine lending, trading, liquidity provision, and yield farming in ways that would be economically unfeasible on higher-cost networks. The resulting ecosystem effect has attracted significant liquidity and user adoption, creating a self-reinforcing cycle of growth and innovation.

Arbitrum’s Optimistic Approach to Lending

Arbitrum’s optimistic rollup architecture provides a unique environment for DeFi lending that combines the familiar experience of Ethereum mainnet with significantly reduced transaction costs and faster confirmation times. The network’s full EVM compatibility means that existing Ethereum lending protocols can deploy on Arbitrum with minimal modifications, creating a seamless transition path for users and developers while maintaining access to the same tools and interfaces they’re familiar with.

The optimistic rollup model employed by Arbitrum creates interesting dynamics for lending protocols, particularly in terms of withdrawal times and liquidity management. While most transactions achieve near-instant finality, withdrawals to Ethereum mainnet are subject to a challenge period that can affect certain lending strategies and arbitrage opportunities. However, the development of native bridge protocols and fast withdrawal services has largely mitigated these concerns, creating a user experience that rivals traditional centralized finance in terms of speed and convenience.

Major lending platforms on Arbitrum have taken advantage of the network’s characteristics to offer enhanced services and improved user experiences. Compound’s deployment on Arbitrum has enabled more frequent compound interest calculations and automated position management, while Aave has implemented advanced features such as debt tokenization and cross-chain collateral management that leverage Arbitrum’s technical capabilities.

The Arbitrum ecosystem has also seen the emergence of innovative lending protocols that take advantage of the network’s unique characteristics to offer new types of financial products. These include protocols focused on leveraged yield farming, automated market making with borrowed capital, and sophisticated derivatives trading that requires frequent position adjustments. The lower transaction costs have enabled these protocols to implement features such as automatic liquidation protection, dynamic collateral rebalancing, and complex multi-asset lending strategies.

Cost Comparison and Economic Benefits

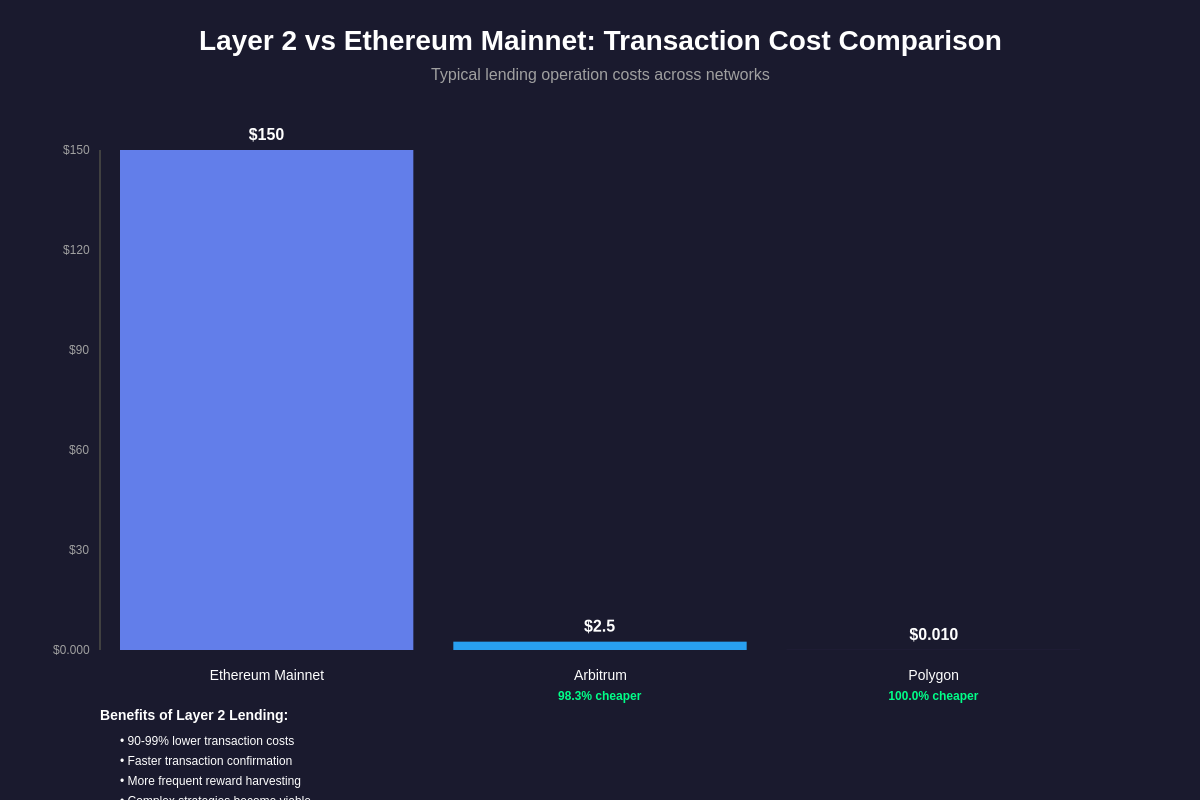

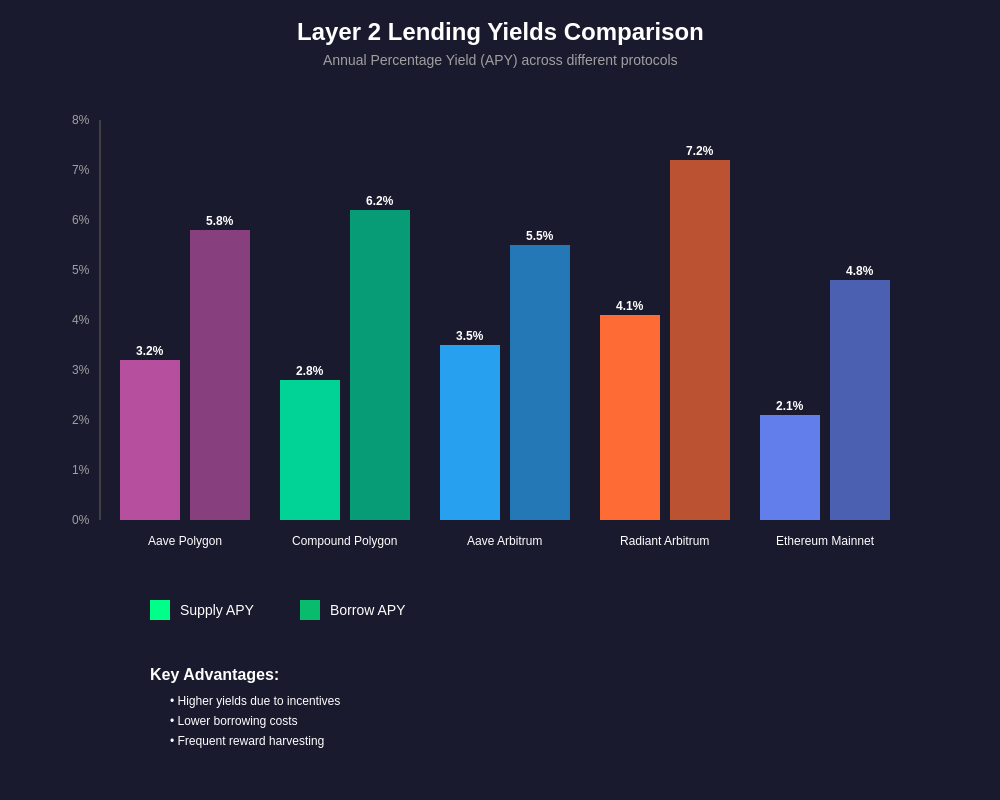

The economic advantages of Layer 2 lending become apparent when comparing transaction costs across different networks and protocols. On Ethereum mainnet, a simple lending operation such as supplying collateral and borrowing against it can cost anywhere from $50 to $500 in gas fees during periods of network congestion, making small-scale lending operations economically unviable for most users. In contrast, the same operations on Polygon typically cost less than $0.01, while Arbitrum transactions generally range from $0.50 to $5, representing cost reductions of 90-99% compared to mainnet.

These dramatic cost reductions have profound implications for lending strategies and user behavior. On mainnet, users are incentivized to make large, infrequent transactions to amortize gas costs across larger position sizes, limiting the flexibility and responsiveness of their DeFi strategies. Layer 2 networks enable users to make frequent small adjustments to their positions, respond quickly to market opportunities, and implement sophisticated automated strategies that would be prohibitively expensive on mainnet.

The economic benefits extend beyond simple transaction cost savings to include improvements in capital efficiency and yield optimization. Lower transaction costs enable users to harvest rewards more frequently, rebalance positions in response to changing market conditions, and implement complex strategies such as leveraged yield farming and automated arbitrage that require frequent interactions with multiple protocols. These capabilities can significantly improve the risk-adjusted returns available to DeFi users while reducing the minimum capital requirements for effective participation.

The compound effect of reduced transaction costs creates a virtuous cycle where increased user activity leads to greater protocol revenues, higher yields for participants, and continued innovation in lending products and services. This dynamic has contributed to the rapid growth of Layer 2 lending ecosystems and their ability to compete with traditional centralized finance products in terms of both cost and functionality.

Interest Rate Mechanisms and Yield Opportunities

Layer 2 lending protocols have implemented sophisticated interest rate mechanisms that take advantage of reduced transaction costs to offer more responsive and efficient rate discovery. Traditional mainnet lending protocols often use relatively simple supply and demand curves to determine interest rates, with infrequent updates due to the high cost of rate adjustment transactions. Layer 2 protocols can implement more complex and responsive rate models that adjust more frequently to market conditions, creating more efficient capital allocation and better risk management.

Dynamic interest rate models on Layer 2 networks can incorporate real-time market data, cross-chain liquidity conditions, and sophisticated risk metrics to provide more accurate pricing of lending and borrowing costs. These models can adjust rates multiple times per day or even per hour, ensuring that interest rates accurately reflect current market conditions and risk levels. The ability to make frequent rate adjustments also enables protocols to implement more aggressive risk management strategies, quickly responding to changing market volatility or liquidity conditions.

The yield opportunities available on Layer 2 lending platforms often exceed those available on mainnet due to a combination of factors including lower operational costs, innovative tokenomics, and the ability to implement more complex yield generation strategies. Many Layer 2 protocols offer additional yield through governance token rewards, protocol fee sharing, and participation in broader ecosystem incentive programs that can significantly enhance the total return available to lenders and borrowers.

Automated yield farming strategies have become particularly popular on Layer 2 networks due to the reduced transaction costs associated with frequent position adjustments and reward harvesting. These strategies can automatically move funds between different lending protocols, optimize collateral ratios, and harvest rewards to maximize yield while managing risk. The economic feasibility of these strategies on Layer 2 networks has created new categories of DeFi products and services that were previously impossible due to high transaction costs.

Risk Management and Security Considerations

The migration of lending protocols to Layer 2 networks introduces new categories of risks that users and protocol developers must carefully consider and manage. While Layer 2 solutions inherit the security properties of the underlying Ethereum blockchain, they also introduce additional technical complexity and potential failure modes that can affect the safety of user funds and the reliability of lending operations.

Smart contract risk remains a primary concern for Layer 2 lending protocols, particularly given the relatively recent deployment of many protocols and the rapid pace of innovation in the space. The complexity of Layer 2 architectures can introduce subtle bugs or vulnerabilities that may not be apparent in traditional mainnet deployments. Additionally, the integration between Layer 2 protocols and cross-chain bridges creates additional attack surfaces that malicious actors may attempt to exploit.

Bridge risk represents a unique category of risk for Layer 2 lending protocols, as users must rely on various bridge mechanisms to move assets between Ethereum mainnet and Layer 2 networks. These bridges have historically been targets for significant attacks, and failures or exploits can affect the ability of users to access their funds or withdraw assets from lending protocols. Understanding the security model and operational procedures of relevant bridges is crucial for users participating in Layer 2 lending.

Liquidity risk on Layer 2 networks can be more pronounced than on mainnet due to the smaller overall market sizes and the potential for rapid capital flight during periods of market stress. While this risk is mitigated by the growing maturity and size of Layer 2 ecosystems, users should be aware that extreme market conditions could affect the ability to access liquidity or execute large transactions without significant market impact.

Cross-Chain Integration and Interoperability

The evolution of Layer 2 lending has been closely tied to advances in cross-chain infrastructure that enable seamless movement of assets and data between different blockchain networks. Modern Layer 2 lending protocols increasingly offer integrated cross-chain functionality that allows users to manage collateral and debt positions across multiple networks without the complexity and cost of manual bridge operations.

Cross-chain collateral management represents one of the most significant innovations in Layer 2 lending, enabling users to deposit collateral on one network while borrowing on another, or to use assets held on multiple chains as collateral for a single borrowing position. These capabilities require sophisticated infrastructure to track collateral values, manage liquidation procedures, and ensure the integrity of cross-chain positions, but they offer users unprecedented flexibility in managing their DeFi strategies.

Automated cross-chain yield optimization has emerged as a key feature of advanced Layer 2 lending platforms, with protocols automatically moving user funds between different chains and protocols to maximize yield while managing risk. These systems must navigate the complexity of different network characteristics, bridge delays, and transaction costs to provide users with optimal returns while maintaining appropriate risk management procedures.

The future of cross-chain lending integration points toward even more seamless experiences where users interact with unified interfaces that abstract away the complexity of managing positions across multiple networks. These developments will likely include advances in cross-chain messaging protocols, standardized security frameworks, and improved user experience design that makes cross-chain lending as simple and intuitive as traditional single-chain operations.

Regulatory Landscape and Compliance

The regulatory environment for Layer 2 lending protocols continues to evolve as regulators worldwide grapple with the implications of DeFi and scaling solutions. While many Layer 2 protocols operate in regulatory gray areas, the increasing mainstream adoption and institutional interest has prompted more serious consideration of compliance requirements and regulatory frameworks that may affect Layer 2 lending operations.

The decentralized nature of most Layer 2 lending protocols creates unique challenges for regulatory compliance, as traditional frameworks often assume centralized control and clear jurisdictional authority. However, some protocols have begun implementing optional compliance features such as geographic restrictions, know-your-customer procedures, and transaction monitoring systems that can help them operate within existing regulatory frameworks while maintaining their decentralized characteristics.

The treatment of governance tokens associated with Layer 2 lending protocols remains a particular area of regulatory uncertainty, with different jurisdictions taking varying approaches to the classification and regulation of these assets. Users participating in Layer 2 lending should be aware of their local regulatory requirements and the potential for changes in regulatory treatment that could affect their ability to participate in certain protocols or access specific features.

The development of regulatory clarity for Layer 2 lending protocols will likely influence the design and operation of future protocols, potentially leading to the emergence of different protocol variants optimized for different regulatory environments. This evolution may create a more complex landscape where users must navigate different compliance requirements and feature sets depending on their jurisdiction and the specific protocols they choose to use.

Market Impact and Institutional Adoption

The growth of Layer 2 lending has had a profound impact on the broader DeFi market, democratizing access to sophisticated financial products and creating new opportunities for both retail and institutional participants. The dramatic reduction in transaction costs has expanded the addressable market for DeFi lending to include users with smaller capital bases who were previously excluded by high gas fees, leading to significant growth in user adoption and total value locked.

Institutional adoption of Layer 2 lending has been driven by the improved cost structure and operational efficiency compared to mainnet protocols. Many institutional users require frequent position adjustments, complex hedging strategies, and automated risk management procedures that are economically feasible only on Layer 2 networks. The ability to implement sophisticated treasury management and yield generation strategies at scale has made Layer 2 lending an attractive option for institutions seeking to optimize their cryptocurrency holdings.

The competitive dynamics between different Layer 2 networks have accelerated innovation and improvement in lending protocols, with each network seeking to attract users and liquidity through superior technology, lower costs, and innovative features. This competition has benefited users through improved protocols, better user experiences, and more competitive interest rates, while also driving the overall maturation of the Layer 2 ecosystem.

The success of Layer 2 lending has also influenced the development of traditional financial products and services, with some centralized platforms adopting similar fee structures and features to compete with decentralized alternatives. This convergence between decentralized and traditional finance represents a significant validation of the Layer 2 lending model and suggests continued growth and mainstream adoption.

Technical Innovation and Protocol Development

The technical development of Layer 2 lending protocols has pushed the boundaries of what’s possible in decentralized finance, with innovations in areas such as automated market making, dynamic risk assessment, and cross-chain integration. These advances have been enabled by the reduced transaction costs and increased throughput available on Layer 2 networks, which allow for more complex and computationally intensive protocol designs.

Advanced automation features have become a hallmark of Layer 2 lending protocols, with many platforms offering sophisticated bots and automated strategies that can manage user positions, harvest rewards, and optimize yields without manual intervention. These systems leverage the low transaction costs on Layer 2 networks to implement strategies that would be prohibitively expensive on mainnet, such as frequent rebalancing, automated liquidation protection, and dynamic collateral optimization.

The integration of oracle systems and external data feeds has become more sophisticated on Layer 2 networks, with protocols able to afford more frequent price updates and complex risk calculations. This enhanced data integration enables more accurate risk assessment, better liquidation procedures, and improved user protection during periods of market volatility. The ability to process more data more frequently has also enabled the development of new types of lending products that were previously impossible due to computational constraints.

Machine learning and artificial intelligence applications have begun to emerge in Layer 2 lending protocols, with some platforms experimenting with AI-driven risk assessment, automated yield optimization, and predictive analytics for market conditions. These applications are enabled by the lower costs and higher throughput of Layer 2 networks, which allow for more frequent data processing and model updates than would be feasible on more expensive networks.

User Experience and Interface Design

The user experience of Layer 2 lending platforms has evolved significantly from early DeFi protocols, with modern platforms offering sophisticated interfaces that rival traditional centralized finance applications in terms of usability and functionality. The reduced transaction costs on Layer 2 networks have enabled more responsive user interfaces with real-time updates, instant transaction confirmations, and seamless integration between different protocol features.

Mobile-first design has become increasingly important for Layer 2 lending platforms, with many protocols optimizing their interfaces for smartphone users who want to manage their DeFi positions on the go. The lower transaction costs make mobile interactions more practical, as users can make small adjustments and check their positions without worrying about prohibitive gas fees that would make mobile usage economically unviable.

Educational features and risk assessment tools have become standard components of modern Layer 2 lending interfaces, helping users understand the risks and opportunities associated with different lending strategies. These tools often include interactive tutorials, risk calculators, and simulation features that help users understand the potential outcomes of different actions before committing funds to specific strategies.

The integration of advanced analytics and portfolio management tools has transformed Layer 2 lending platforms into comprehensive financial management applications that can track performance across multiple protocols and networks. These tools provide users with detailed insights into their lending performance, risk exposure, and optimization opportunities, enabling more sophisticated and informed decision-making.

Future Developments and Innovation Trends

The future of Layer 2 lending points toward even greater integration, automation, and sophistication as the technology continues to mature and evolve. Emerging trends include the development of cross-chain native protocols that can operate seamlessly across multiple Layer 2 networks, advanced AI-driven yield optimization systems, and integration with traditional financial infrastructure to create hybrid decentralized-traditional finance products.

Zero-knowledge proof technology is expected to play an increasingly important role in Layer 2 lending, enabling enhanced privacy protection, more efficient cross-chain operations, and new types of lending products that require privacy preservation. The development of zkEVMs and other zero-knowledge scaling solutions may create new opportunities for lending protocols while addressing privacy and scalability concerns that limit current implementations.

The integration of real-world assets into Layer 2 lending protocols represents a significant opportunity for expansion beyond purely cryptocurrency-based lending. Projects are already exploring the tokenization of real estate, commodities, and other traditional assets that can be used as collateral in Layer 2 lending protocols, potentially creating enormous new markets and use cases for decentralized lending.

Institutional infrastructure development continues to advance, with the creation of specialized custody solutions, compliance frameworks, and risk management tools designed specifically for institutional participation in Layer 2 lending. These developments may accelerate institutional adoption and bring significantly more capital into Layer 2 lending ecosystems, creating new opportunities for innovation and growth.

Global Adoption and Market Penetration

The global adoption of Layer 2 lending has been facilitated by the improved accessibility and reduced barriers to entry compared to mainnet protocols. Users in regions with limited access to traditional financial services have been particularly drawn to Layer 2 lending platforms, which can provide sophisticated financial services without the need for traditional banking infrastructure or regulatory approval.

The cost advantages of Layer 2 lending have made these platforms particularly attractive in emerging markets where users may have smaller capital bases and be more sensitive to transaction costs. The ability to participate in global DeFi markets with minimal capital requirements has created new opportunities for wealth creation and financial inclusion in regions that have been underserved by traditional financial institutions.

Educational initiatives and community development efforts have played a crucial role in driving global adoption of Layer 2 lending, with many protocols investing in translated interfaces, local community support, and educational content designed to help users in different regions understand and safely participate in DeFi lending. These efforts have contributed to the global reach and diversity of Layer 2 lending ecosystems.

The development of local partnerships and integrations with regional financial service providers has further accelerated adoption in specific markets, creating on-ramps and off-ramps that make it easier for users to move between traditional finance and Layer 2 lending platforms. These integrations often include support for local payment methods, compliance with regional regulations, and customer support in local languages.

Risk Assessment and Portfolio Management

Sophisticated risk assessment tools have become essential components of Layer 2 lending platforms, enabling users to understand and manage the complex risks associated with multi-chain DeFi strategies. These tools often incorporate real-time market data, historical performance analytics, and advanced modeling techniques to provide users with comprehensive risk assessments for their lending positions.

Portfolio management features on Layer 2 lending platforms have evolved to include automated rebalancing, risk-based position sizing, and integration with external portfolio tracking tools. The low transaction costs on Layer 2 networks make it economically feasible to implement sophisticated portfolio management strategies that would be prohibitively expensive on mainnet, enabling more professional-grade investment management for retail users.

The development of standardized risk metrics and assessment frameworks has improved the comparability and transparency of different Layer 2 lending opportunities. These frameworks often include measures such as value at risk, maximum drawdown, Sharpe ratios, and other metrics borrowed from traditional finance that help users make informed decisions about their lending strategies.

Advanced users and institutions have access to sophisticated risk management tools that can implement complex hedging strategies, automated stop-losses, and dynamic position sizing based on market conditions. These tools leverage the programmable nature of DeFi protocols and the cost advantages of Layer 2 networks to provide institutional-grade risk management capabilities to a broader user base.

Economic Models and Tokenomics

The economic models underlying Layer 2 lending protocols have evolved to incorporate sophisticated tokenomics that align the interests of different stakeholders while providing sustainable revenue streams for protocol development and maintenance. Many protocols have implemented governance tokens that provide both utility within the platform and potential appreciation based on protocol success and adoption.

Revenue sharing mechanisms have become common features of Layer 2 lending protocols, with many platforms distributing a portion of protocol fees to token holders, liquidity providers, or active participants in governance. These mechanisms create additional yield opportunities for users while ensuring that protocol value accrues to stakeholders who contribute to the platform’s success and sustainability.

The design of incentive programs for Layer 2 lending protocols requires careful balancing of user acquisition, liquidity attraction, and long-term sustainability. Many protocols have experimented with different approaches including liquidity mining, yield farming rewards, and governance participation incentives to drive adoption while building sustainable economic models.

The interaction between different tokenomic systems across Layer 2 networks creates complex economic dynamics that can significantly affect user returns and protocol sustainability. Understanding these interactions and their potential implications is crucial for users seeking to optimize their participation in Layer 2 lending ecosystems while managing associated risks.

The future success of Layer 2 lending protocols will depend largely on their ability to maintain competitive yields and innovative features while building sustainable business models that can support continued development and expansion. The growing institutional interest in DeFi yields suggests that protocols with strong economic fundamentals and clear value propositions will continue to attract significant capital and user adoption, driving further innovation and growth in the Layer 2 lending space.

Disclaimer: This article is for educational and informational purposes only and should not be considered financial advice. Cryptocurrency and DeFi lending involve significant risks including smart contract vulnerabilities, market volatility, and potential loss of funds. Layer 2 networks introduce additional technical risks including bridge failures and scaling solution vulnerabilities. Users should conduct thorough research, understand the risks involved, and consider consulting with qualified financial advisors before participating in any DeFi lending protocols. Past performance does not guarantee future results, and all investments carry the risk of loss.