The Hidden Perils of DeFi Lending

Decentralized finance lending pools have emerged as one of the most popular yield-generating mechanisms in the cryptocurrency ecosystem, attracting billions of dollars in total value locked as users seek attractive returns on their digital assets. However, beneath the alluring promises of high annual percentage yields lies a complex web of risks that can devastate unprepared investors through mechanisms like impermanent loss and sudden liquidations. Understanding these risks is crucial for anyone considering participation in DeFi lending protocols, as the difference between profit and catastrophic loss often depends on comprehensive risk assessment and proper position management.

The sophistication of modern DeFi lending protocols has created new categories of financial risk that traditional finance practitioners may not fully comprehend, combining the volatility of cryptocurrency markets with the complexity of automated market-making algorithms and dynamic interest rate models. These protocols operate through smart contracts that execute predetermined rules without human intervention, creating both opportunities for efficiency gains and potential vulnerabilities that can be exploited by sophisticated actors or triggered by extreme market conditions.

Understanding Impermanent Loss Mechanics

Impermanent loss represents one of the most misunderstood yet financially devastating risks facing liquidity providers in automated market maker protocols, occurring when the relative prices of tokens in a liquidity pool change compared to their values at the time of initial deposit. This phenomenon affects anyone providing liquidity to trading pairs, particularly those participating in lending pools that incorporate AMM functionality or those staking LP tokens as collateral in lending protocols.

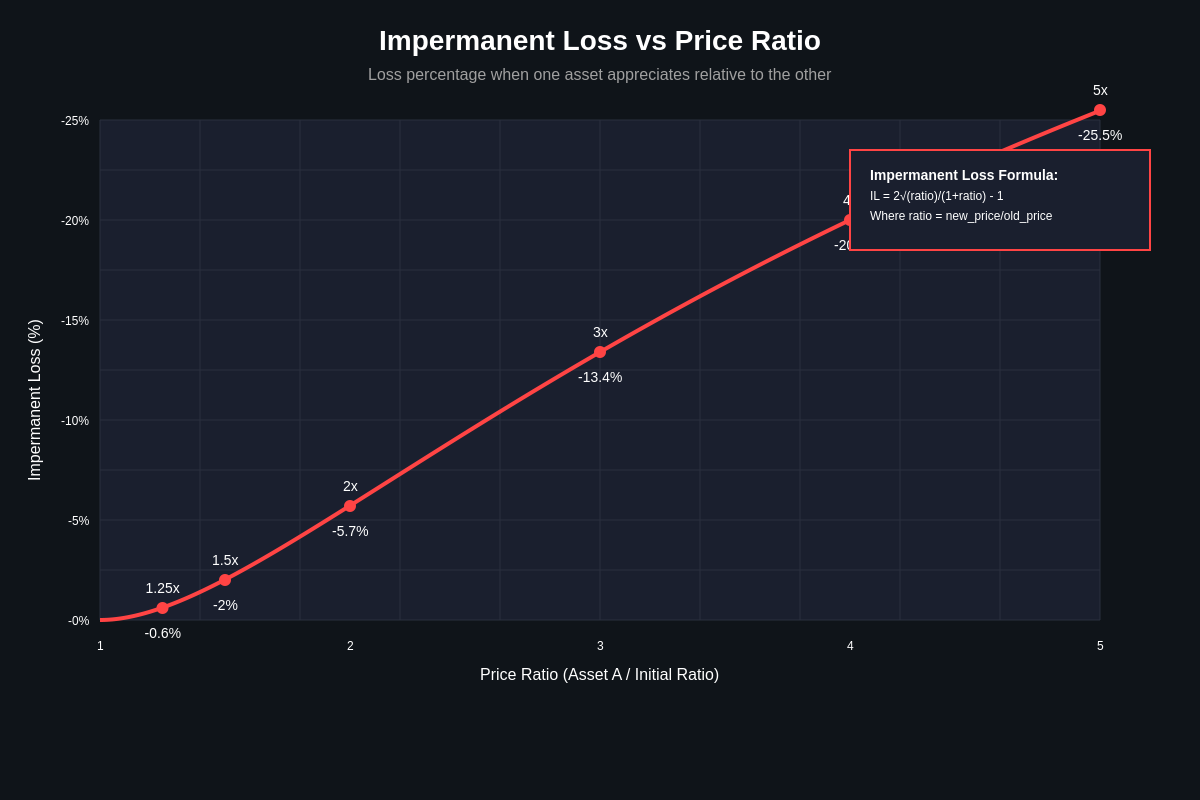

The mathematical foundation of impermanent loss stems from the constant product formula used by most AMM protocols, which maintains the relationship x * y = k, where x and y represent the quantities of two tokens in a pool and k represents a constant. When token prices diverge from their initial ratio, arbitrageurs rebalance the pool by trading the undervalued token for the overvalued one, effectively forcing liquidity providers to sell their appreciating assets and accumulate depreciating ones at unfavorable rates.

Consider a scenario where a liquidity provider deposits equal values of ETH and USDC into a lending pool when ETH trades at $2000. If ETH subsequently appreciates to $3000, the automated rebalancing mechanism will gradually sell ETH for USDC to maintain the constant product relationship, resulting in the liquidity provider holding fewer ETH tokens than they would have retained by simply holding their original assets. The magnitude of impermanent loss increases exponentially with price divergence, reaching approximately 5.7% when one asset doubles in value and exceeding 20% when price ratios reach 4:1.

The term “impermanent” proves misleading in practice, as losses become permanent when liquidity providers withdraw their positions at unfavorable price ratios. Many retail investors misunderstand this mechanism, assuming that losses will automatically reverse if prices return to their original levels, failing to account for the continuous rebalancing that occurs throughout the price movement cycle and the trading fees lost during volatile periods.

Complex multi-asset pools introduce additional layers of impermanent loss risk, as price movements in any component token can trigger rebalancing across the entire pool structure. Advanced protocols may implement strategies to mitigate impermanent loss through dynamic fee structures, concentrated liquidity mechanisms, or novel algorithmic approaches, but these solutions often introduce their own complexity and additional risk vectors that participants must carefully evaluate.

Liquidation Mechanisms and Threshold Management

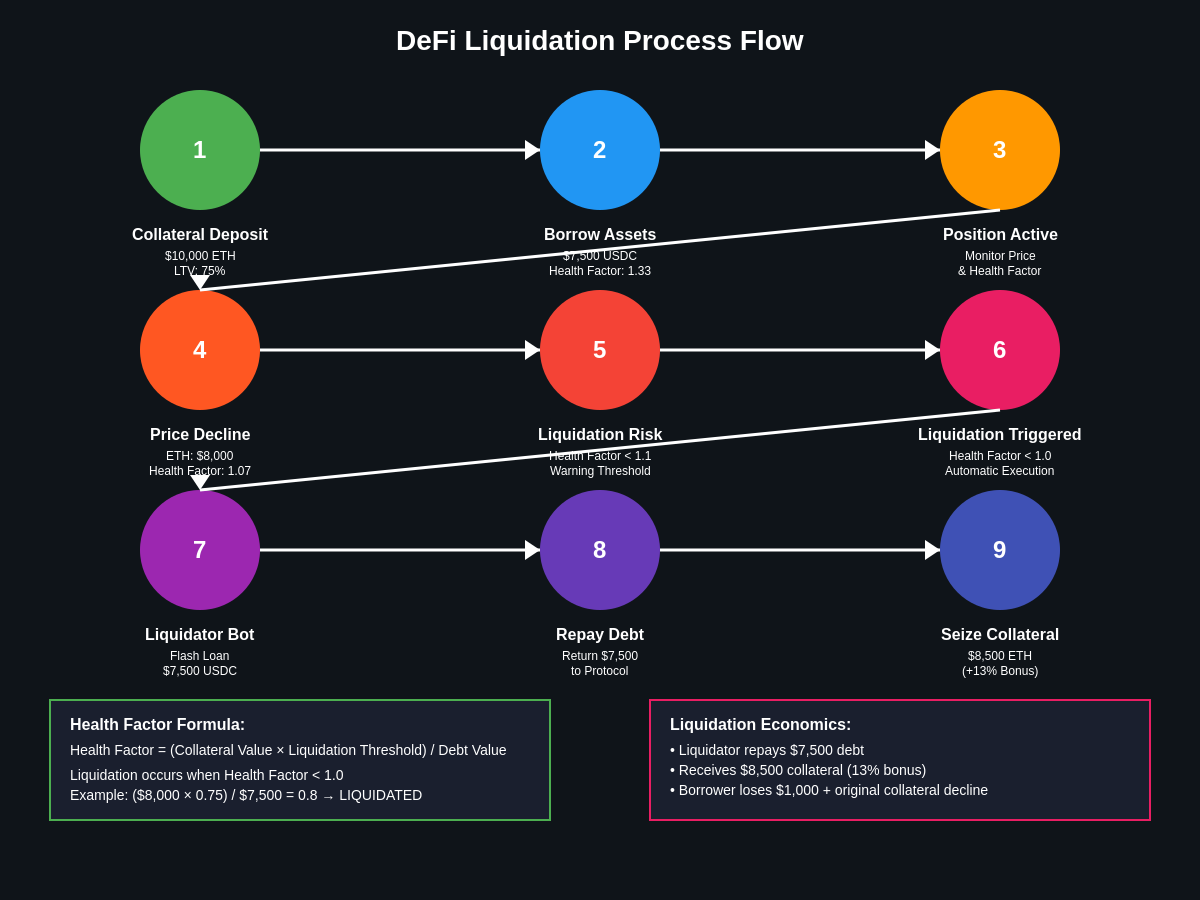

Liquidation represents the most immediate and catastrophic risk facing borrowers in DeFi lending protocols, occurring when the value of posted collateral falls below the minimum threshold required to maintain a loan position. Unlike traditional finance where liquidation processes may involve lengthy legal procedures and opportunities for borrower intervention, DeFi liquidations execute automatically through smart contracts within minutes or even seconds of threshold breaches, providing no opportunity for borrowers to add additional collateral or negotiate alternative arrangements.

The liquidation threshold, typically expressed as a loan-to-value ratio, varies significantly across different protocols and collateral types, with more volatile assets generally requiring higher collateralization ratios to account for their increased price risk. For example, major protocols may require borrowers to maintain collateralization ratios of 150% or higher for volatile cryptocurrency collateral, meaning that a $10,000 loan requires at least $15,000 in collateral value at all times.

Price feed mechanisms play a critical role in liquidation timing, with most protocols relying on oracle systems that aggregate price data from multiple sources to determine when liquidation thresholds are breached. However, oracle delays, manipulation attempts, or extreme market volatility can create situations where liquidation prices become stale or inaccurate, potentially triggering premature liquidations or allowing positions to become undercollateralized before liquidation mechanisms activate.

The liquidation process typically involves selling collateral assets at discounted prices to incentivize liquidators to execute the transactions quickly, with discounts ranging from 5% to 15% depending on the protocol and market conditions. This discount structure means that borrowers not only lose their collateral but also suffer additional losses beyond the threshold breach, creating a penalty mechanism that can quickly escalate losses during volatile market conditions.

Flash loan liquidations have introduced additional complexity to the liquidation landscape, allowing sophisticated actors to execute liquidations without requiring their own capital by borrowing the necessary funds within a single transaction block. While this mechanism improves capital efficiency and liquidation speed, it can also lead to rapid cascade liquidations during extreme market stress, as automated systems compete to liquidate positions with minimal human oversight or intervention.

Multiple position management across different protocols creates compound liquidation risks that many users fail to properly assess, as correlated price movements can trigger simultaneous liquidations across multiple platforms, amplifying losses and reducing diversification benefits. Borrowers maintaining positions on multiple protocols must carefully monitor their aggregate exposure and ensure that liquidation events on one platform do not create cascading effects that compromise their other positions.

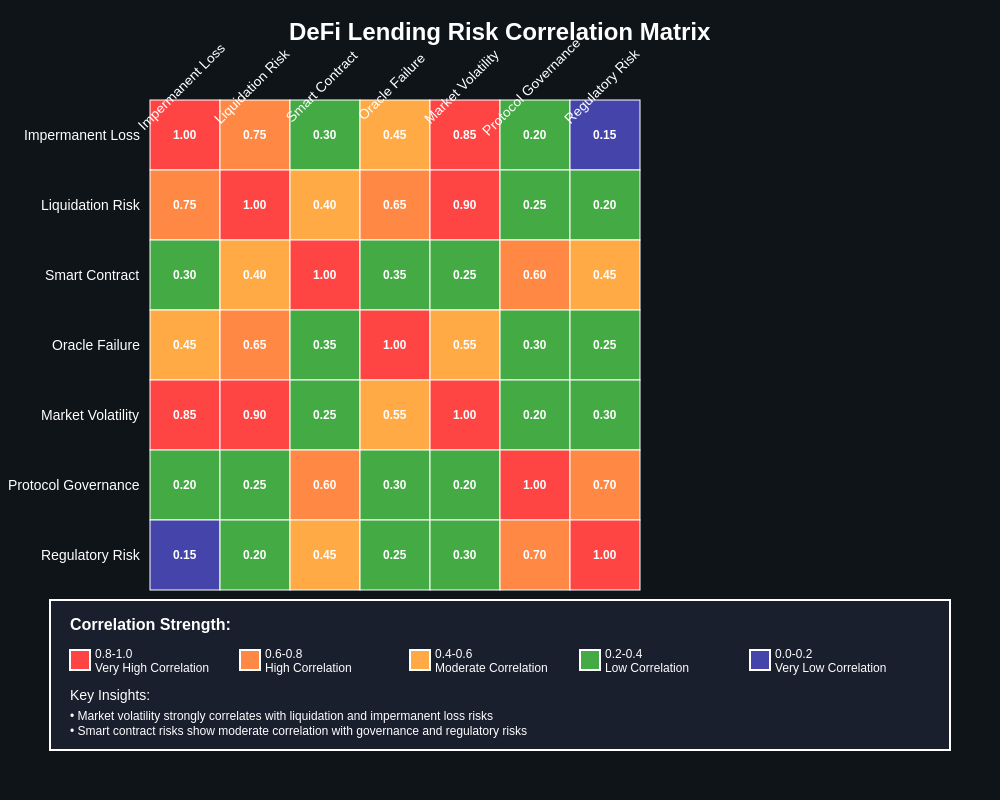

Market Volatility and Correlation Risks

The cryptocurrency market’s inherent volatility creates unique challenges for DeFi lending participants, as sudden price movements can rapidly transform profitable positions into catastrophic losses through various risk mechanisms. Unlike traditional financial markets that may experience volatility of 1-3% daily, cryptocurrency markets regularly witness price swings of 10-30% within hours, creating extreme stress on lending protocols and their participants.

Correlation risk represents a particularly insidious threat to diversification strategies within DeFi lending, as assets that appear uncorrelated during normal market conditions often exhibit high correlation during periods of extreme stress. The infamous market crashes of March 2020 and May 2022 demonstrated how even supposedly stable assets can experience significant price movements simultaneously, triggering liquidation cascades across multiple protocols and asset classes.

Algorithmic trading strategies and automated liquidation mechanisms can amplify volatility through feedback loops, where initial liquidations trigger further price declines that lead to additional liquidations in a self-reinforcing cycle. These dynamics are particularly pronounced in smaller market cap assets or during periods of reduced liquidity, when relatively small trading volumes can create disproportionate price impacts that trigger widespread liquidation events.

The interconnected nature of DeFi protocols means that volatility in one market segment can rapidly propagate throughout the ecosystem, as arbitrageurs and automated systems react to price discrepancies across different platforms. For example, a sudden decline in ETH price may simultaneously affect collateral values in lending protocols, trigger rebalancing in AMM pools, and create opportunities for liquidation bots across multiple platforms, creating complex risk interactions that individual users may struggle to anticipate or manage effectively.

Cross-chain lending protocols introduce additional volatility considerations, as participants must account for risks associated with bridge mechanisms, cross-chain arbitrage opportunities, and potential disconnections between different blockchain networks during periods of network congestion or technical difficulties. These factors can create temporary price divergences that may trigger liquidations based on stale or inaccurate price information, while making it difficult for users to take corrective action due to technical constraints.

Stablecoin depegging events represent another category of volatility risk that can devastate lending pool participants, as assets assumed to maintain stable value relationships may experience sudden price movements that trigger unexpected liquidations or impermanent loss events. The USDC depegging incident following Silicon Valley Bank’s collapse and various Terra ecosystem failures demonstrate how supposedly stable assets can become sources of extreme volatility that propagate throughout DeFi lending markets.

Protocol-Specific Risk Factors

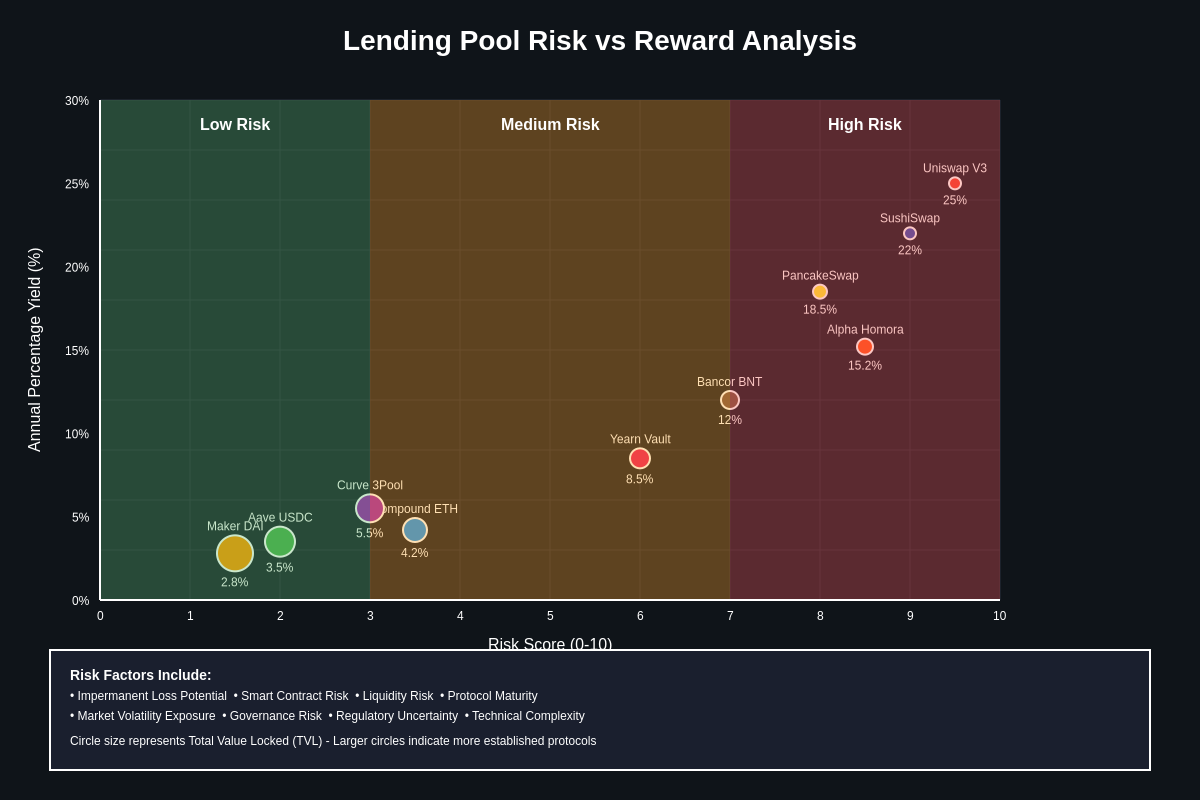

Different DeFi lending protocols implement varying risk management mechanisms, governance structures, and technical architectures that create unique risk profiles for participants. Understanding these protocol-specific factors is essential for making informed decisions about where to deploy capital and how to structure positions to minimize exposure to platform-specific risks.

Smart contract risk represents a fundamental concern for all DeFi lending protocols, as bugs, exploits, or design flaws in the underlying code can result in complete loss of deposited funds. Even protocols that have undergone extensive auditing may contain vulnerabilities that become apparent only under extreme market conditions or when faced with sophisticated attack vectors that auditors failed to anticipate during their reviews.

Governance risks emerge from the decentralized decision-making processes that control protocol parameters, upgrade procedures, and risk management policies. Token holders with significant voting power may implement changes that benefit their positions at the expense of other participants, while governance attacks involving the accumulation of voting tokens can allow malicious actors to manipulate protocol parameters for their own benefit.

Admin key risks persist in many DeFi protocols despite claims of decentralization, as development teams often retain privileged access to critical functions like parameter updates, emergency shutdowns, or contract upgrades. These centralized control mechanisms create single points of failure that can be exploited by malicious insiders or compromised by external attackers seeking to manipulate protocol behavior.

Liquidity risks vary significantly across different lending protocols based on their size, token support, and market maker participation. Smaller protocols may experience liquidity crunches during market stress that prevent users from withdrawing funds or closing positions when needed, while larger protocols may face different challenges related to systemic risk and regulatory scrutiny that could affect their long-term viability.

Oracle manipulation represents a sophisticated attack vector that can affect lending protocols by providing inaccurate price information that triggers inappropriate liquidations or allows borrowers to extract value from the protocol. While oracle systems have become more robust over time, they remain vulnerable to various manipulation techniques including flash loan attacks, market manipulation, and coordination attacks across multiple price feeds.

Integration risks arise when lending protocols connect with other DeFi services like DEXs, yield farming platforms, or cross-chain bridges, creating dependencies on external systems that may introduce additional failure modes. A compromise or failure in any integrated service can potentially cascade into the lending protocol, affecting user funds even if the lending protocol itself remains secure and functional.

Economic Impact and Market Dynamics

The rapid growth of DeFi lending has created new economic dynamics that influence both traditional and decentralized financial markets, with total value locked in lending protocols reaching hundreds of billions of dollars during peak periods. This massive capital allocation has profound implications for cryptocurrency market structure, interest rate dynamics, and the broader evolution of financial infrastructure.

Interest rate arbitrage opportunities between different lending protocols and traditional financial markets create complex economic relationships that affect pricing across the entire cryptocurrency ecosystem. Sophisticated traders exploit rate differentials through various strategies that can amplify volatility and create feedback loops between different market segments, while algorithmic borrowing and lending strategies automated by institutional participants add additional layers of complexity to market dynamics.

The emergence of yield farming and liquidity mining programs has fundamentally altered the risk-reward calculus for DeFi lending participants, as token rewards can potentially offset losses from impermanent loss or provide compensation for liquidation risks. However, these reward mechanisms often create their own risks related to token price volatility, reward sustainability, and the potential for sudden program changes that can dramatically affect position profitability.

Institutional participation in DeFi lending markets has grown significantly, bringing both increased liquidity and new types of market manipulation risks as large participants deploy sophisticated strategies that retail users may not fully understand or be able to compete against effectively. Professional market makers and hedge funds operating in DeFi lending markets can create adverse selection problems for retail participants while potentially destabilizing protocols through coordinated actions during market stress.

Regulatory uncertainty continues to create economic risks for DeFi lending participants, as changing compliance requirements or enforcement actions can rapidly affect protocol viability, token values, and user access to services. The potential for retrospective regulatory changes or enforcement actions creates ongoing uncertainty that affects long-term planning and risk assessment for both protocols and users.

Systemic risk concerns have emerged as DeFi lending protocols become increasingly interconnected with traditional financial systems and with each other, creating potential transmission mechanisms for financial contagion that could affect broader market stability. Central bank and regulatory studies of DeFi lending risks suggest that current market size may already be sufficient to create systemic concerns under certain stress scenarios.

Risk Mitigation Strategies and Best Practices

Successful participation in DeFi lending requires comprehensive risk management strategies that address multiple categories of potential losses while maintaining the flexibility to adapt to changing market conditions and protocol developments. Professional risk management in this space requires constant monitoring, diversification across multiple dimensions, and careful position sizing that accounts for extreme scenarios that traditional risk models may not adequately capture.

Portfolio diversification within DeFi lending should extend beyond simple asset diversification to include protocol diversification, strategy diversification, and temporal diversification that spreads risk across different time periods and market cycles. Concentration in any single protocol, asset class, or strategy can create catastrophic losses when adverse conditions affect that particular risk factor, while over-diversification can dilute returns and create management complexity that increases operational risks.

Position sizing and leverage management require careful consideration of extreme scenarios that may occur with higher probability in cryptocurrency markets than in traditional financial markets. Conservative position sizing that allows survival through multiple standard deviations of adverse price movement provides better long-term outcomes than aggressive leverage that maximizes returns during favorable conditions but creates unsustainable risks during market stress.

Monitoring and alert systems become essential tools for active risk management in DeFi lending, as the rapid pace of market movements and automated liquidation mechanisms provide minimal time for manual intervention once adverse conditions develop. Effective monitoring should track collateralization ratios, impermanent loss metrics, protocol health indicators, and market conditions across multiple timeframes and protocols simultaneously.

Hedging strategies can provide protection against various DeFi lending risks, though implementing effective hedges requires sophisticated understanding of correlation dynamics, options pricing, and the interactions between different hedging instruments and the underlying positions being protected. Simple hedging approaches may provide false confidence while failing to protect against the specific risk scenarios most likely to affect DeFi lending positions.

Exit strategy planning should account for the potential unavailability of normal exit mechanisms during periods of extreme market stress, when liquidation queues may be congested, withdrawal limits may be imposed, or technical issues may prevent normal protocol operation. Effective exit strategies require multiple contingency plans and may involve accepting suboptimal pricing in exchange for certainty of execution during crisis periods.

Regulatory Landscape and Compliance Considerations

The regulatory environment surrounding DeFi lending continues evolving rapidly as authorities worldwide grapple with how to classify, oversee, and potentially restrict decentralized lending activities. Understanding current regulatory risks and anticipating future developments is crucial for participants seeking to maintain compliant positions while navigating the complex intersection of traditional financial regulation and decentralized protocol innovation.

Securities law implications of DeFi lending participation vary significantly across jurisdictions, with many regulatory authorities still developing frameworks for determining whether lending tokens, governance tokens, or participation in lending protocols constitutes securities transactions subject to registration and compliance requirements. The potential for retrospective enforcement actions or changes in regulatory interpretation creates ongoing legal risks for protocol developers and users alike.

Tax implications of DeFi lending activities create complex compliance obligations that many participants may not fully understand or properly address, as traditional tax frameworks struggle to accommodate the novel characteristics of automated lending, yield farming rewards, and impermanent loss calculations. The lack of clear guidance from tax authorities in many jurisdictions creates uncertainty about proper reporting requirements and potential penalties for incorrect compliance approaches.

Anti-money laundering considerations apply to DeFi lending protocols in many jurisdictions, creating potential compliance obligations for protocol developers and possibly for users who facilitate transactions that violate AML requirements. The pseudonymous nature of many DeFi transactions and the global accessibility of lending protocols create particular challenges for implementing effective AML compliance while maintaining the decentralized characteristics that make these protocols attractive to users.

Cross-border regulatory arbitrage opportunities and risks emerge as different jurisdictions adopt varying approaches to DeFi regulation, creating potential benefits for users who can access favorable regulatory environments while also creating risks for those who inadvertently violate regulations in jurisdictions where they may be subject to enforcement actions.

International coordination efforts among regulatory authorities suggest that future DeFi regulation may become more harmonized across jurisdictions, potentially reducing regulatory arbitrage opportunities while creating more consistent compliance frameworks. However, the timeline and specific requirements for such coordination remain uncertain, creating ongoing regulatory risk for market participants.

Future Evolution and Emerging Technologies

The DeFi lending landscape continues evolving rapidly as developers implement new mechanisms to address current risk factors while potentially introducing new categories of risks that participants must understand and manage. Emerging technologies and protocol innovations promise to reshape the risk profile of decentralized lending while creating new opportunities for both profit and loss.

Layer 2 scaling solutions are fundamentally changing the economics of DeFi lending by reducing transaction costs and enabling more sophisticated risk management strategies that were previously economically unfeasible on layer 1 networks. However, layer 2 solutions also introduce new categories of risks related to bridge security, network connectivity, and the potential for temporary or permanent disconnection from layer 1 settlement mechanisms.

Cross-chain lending protocols represent a significant frontier for DeFi innovation, enabling users to access liquidity and lending opportunities across multiple blockchain networks while creating new categories of risks related to bridge mechanisms, cross-chain arbitrage, and the coordination of liquidation mechanisms across different networks with varying characteristics and capabilities.

Advanced risk management mechanisms like dynamic interest rates, automated position management, and AI-driven liquidation systems promise to reduce some traditional DeFi lending risks while potentially creating new forms of systemic risk as automated systems interact in complex ways during periods of market stress. The increasing sophistication of these systems may create advantages for technologically sophisticated participants while potentially disadvantaging retail users who cannot effectively monitor or respond to automated system behavior.

Integration with traditional finance through institutional custody solutions, regulated stablecoin issuers, and traditional financial institution participation in DeFi lending markets may reduce some risks while creating new ones related to regulatory compliance, counterparty risk, and the potential for traditional financial system disruptions to affect DeFi lending markets.

Zero-knowledge proof systems and privacy-focused lending protocols may address some current limitations of DeFi lending while creating new challenges related to regulatory compliance, risk assessment, and the potential for undetected system manipulation or abuse. These technologies represent a significant evolution in DeFi lending capabilities while requiring new frameworks for risk assessment and management.

The integration of real-world assets as collateral in DeFi lending protocols represents another frontier that may expand the utility and scale of decentralized lending while introducing traditional asset risks like title disputes, physical custody concerns, and valuation challenges that current DeFi risk models may not adequately address.

Conclusion and Strategic Recommendations

DeFi lending presents compelling opportunities for generating yield and accessing capital in novel ways, but successful participation requires comprehensive understanding of complex risk factors that can quickly transform profitable positions into significant losses. The combination of impermanent loss, liquidation risks, protocol-specific vulnerabilities, and rapidly evolving regulatory landscapes creates a challenging environment that demands sophisticated risk management approaches and conservative position sizing for most participants.

For retail investors considering DeFi lending participation, education and gradual exposure represent the most prudent approaches, beginning with small positions in established protocols while developing understanding of risk mechanisms and monitoring systems. The complexity of DeFi lending risks makes it unsuitable for participants who cannot dedicate significant time to understanding protocol mechanics, monitoring market conditions, and maintaining active risk management practices.

Institutional participants must develop sophisticated risk management frameworks that account for the unique characteristics of DeFi lending while ensuring compliance with applicable regulatory requirements and fiduciary obligations. The rapidly evolving nature of both technology and regulation in this space requires ongoing investment in research, monitoring, and risk management capabilities that may exceed those required for traditional financial market participation.

The future evolution of DeFi lending will likely involve continued innovations in risk management, regulatory clarification, and integration with traditional financial systems, creating both new opportunities and new risks for participants. Success in this environment will require adaptability, continuous learning, and risk management approaches that can evolve alongside technological and regulatory developments while maintaining protection against extreme scenarios that may occur with higher probability in decentralized financial systems than in traditional markets.

For more detailed analysis of DeFi protocols and risk management strategies, explore advanced trading tools and market data at TradingView’s comprehensive DeFi section, where professional traders monitor lending pool metrics and develop sophisticated risk management strategies for decentralized finance participation.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. DeFi lending involves significant risks including but not limited to impermanent loss, liquidation, smart contract vulnerabilities, and total loss of invested capital. Cryptocurrency markets are highly volatile and speculative. Past performance does not indicate future results. Readers should conduct their own research and consult with qualified financial advisors before making any investment decisions. The regulatory status of DeFi protocols varies by jurisdiction and may change rapidly. Participants in DeFi lending may be subject to tax obligations and regulatory requirements that vary by location and circumstances. The authors and publishers of this article do not guarantee the accuracy or completeness of any information presented and disclaim all liability for any losses or damages arising from the use of this information.