Navigating the Complex Tax Landscape of Meme Coin Investments

The explosive growth of meme coin trading has created unprecedented challenges for both taxpayers and tax professionals attempting to navigate the complex regulatory landscape governing cryptocurrency taxation in the United States. As millions of retail investors have participated in speculative trading of tokens like Dogecoin, Shiba Inu, and Pepe Coin, the Internal Revenue Service has been forced to develop clearer guidance for how these highly volatile digital assets should be treated under existing tax law, creating new compliance requirements that many traders are unprepared to handle.

The intersection of meme coin speculation and tax compliance represents one of the most challenging areas of modern cryptocurrency taxation, where traditional investment tax principles must be applied to assets that may experience thousand-percent price movements within hours and generate thousands of individual transactions through automated trading systems and decentralized exchanges. Understanding how the IRS views meme coin trading activities is essential for investors seeking to maintain compliance while maximizing their after-tax returns from these highly speculative investments.

Current IRS guidance treats cryptocurrency transactions, including meme coin trades, as property transactions subject to capital gains and losses taxation, though the application of these rules to high-frequency speculative trading presents numerous practical challenges for both taxpayers and enforcement agencies. The tracking requirements for meme coin transactions demand sophisticated record-keeping systems that many retail investors lack, creating significant compliance risks for even well-intentioned taxpayers.

The tax implications of meme coin investing extend beyond simple buy-and-sell transactions to include complex scenarios involving decentralized finance protocols, liquidity mining, staking rewards, and cross-chain bridging activities that can trigger multiple taxable events within single investment strategies. These activities often generate tax liabilities that exceed the actual cash proceeds received by investors, creating substantial compliance challenges for those who fail to plan appropriately for their tax obligations.

Fundamental Tax Treatment of Cryptocurrency Speculation

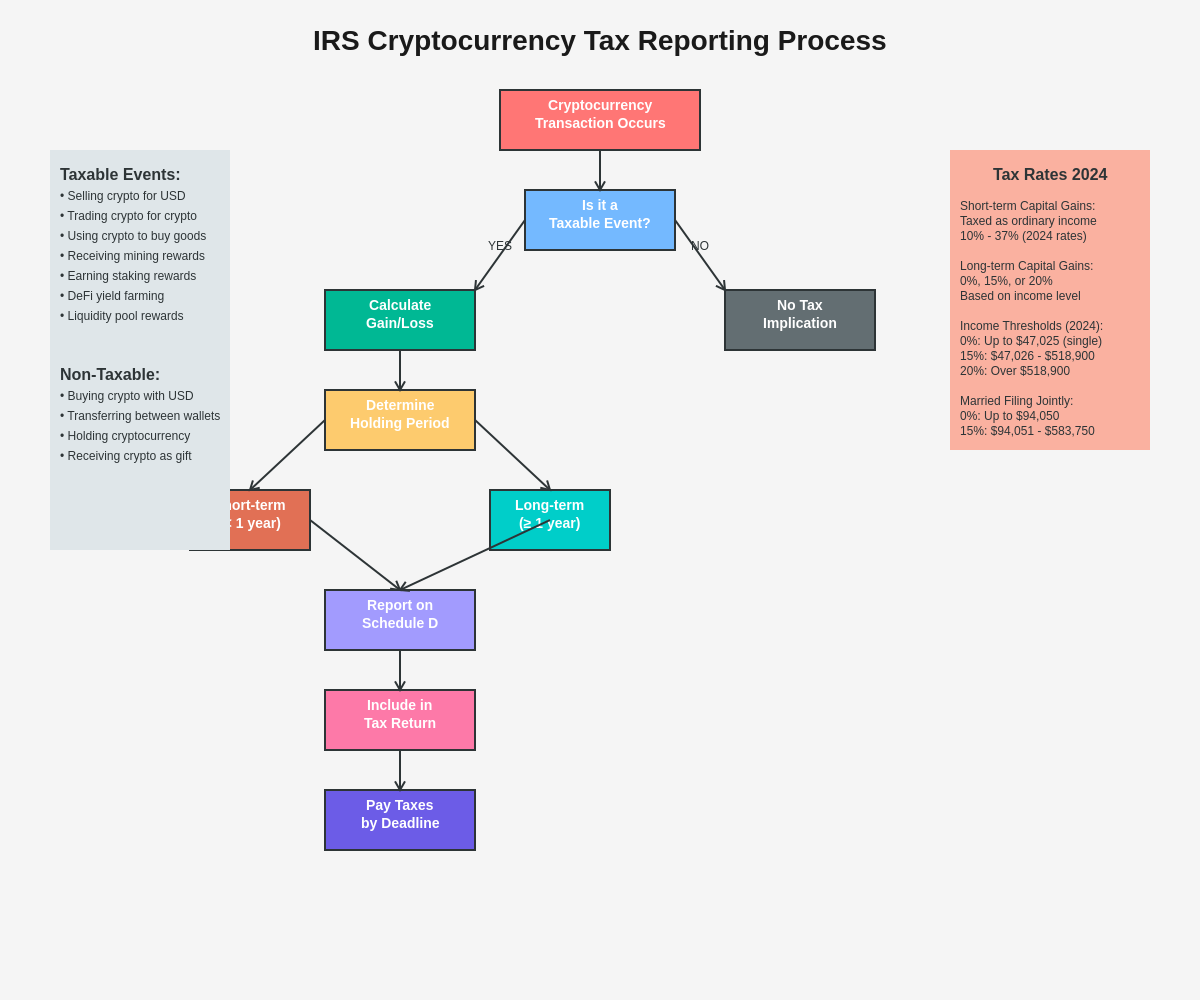

The Internal Revenue Service has established that all cryptocurrency transactions, regardless of the underlying asset’s utility or speculative nature, are treated as property transactions for federal tax purposes, meaning that every trade between different cryptocurrencies or conversion to fiat currency potentially creates a taxable event that must be reported on annual tax returns. This fundamental principle applies equally to established cryptocurrencies like Bitcoin and speculative meme coins, though the practical application of these rules becomes significantly more complex when dealing with highly volatile assets that may be traded frequently.

Property treatment means that meme coin investors must calculate capital gains or losses for each transaction using the difference between the asset’s cost basis and fair market value at the time of disposal, requiring detailed record-keeping of purchase prices, transaction dates, and fair market values that can be challenging to maintain during periods of intense trading activity. The complexity increases dramatically for investors who engage in frequent trading or participate in automated trading strategies that may generate hundreds or thousands of transactions annually.

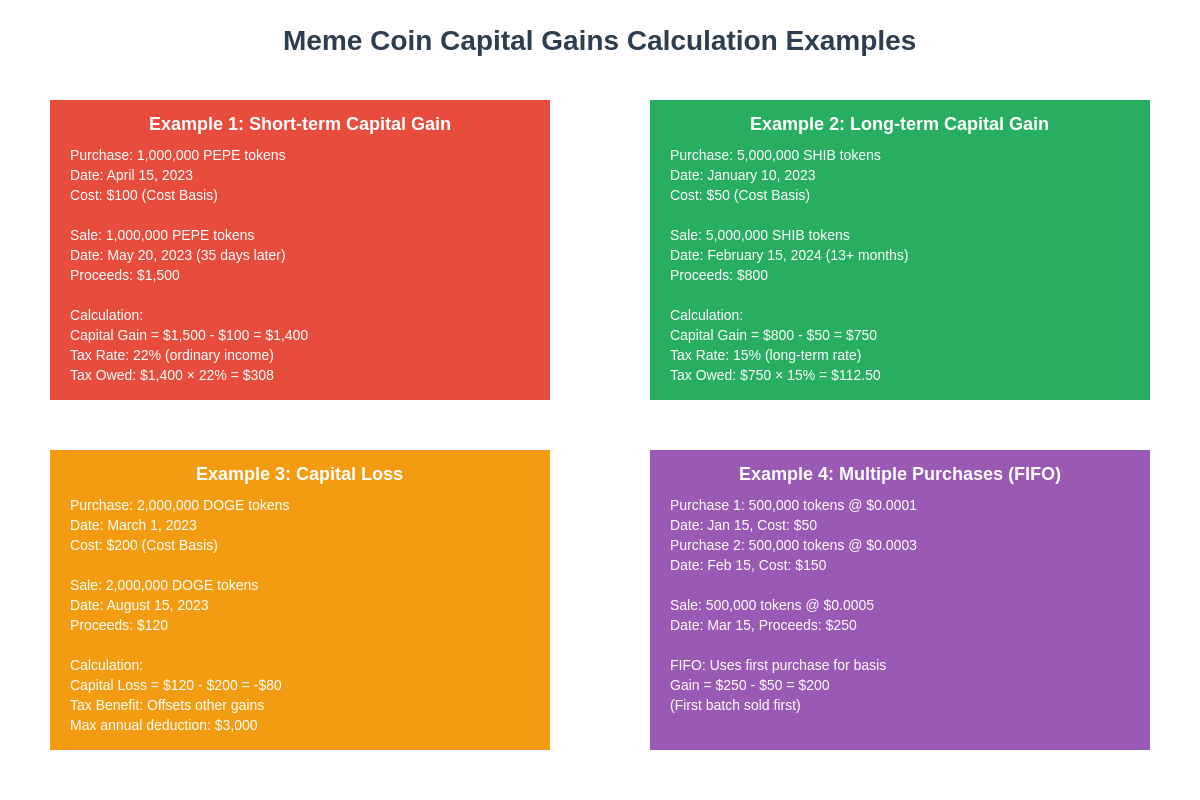

Short-term versus long-term capital gains distinctions apply to meme coin transactions based on holding periods, with assets held for less than one year subject to ordinary income tax rates while assets held for more than one year qualify for preferential long-term capital gains treatment. Given the volatile nature of meme coins and the tendency for investors to trade frequently in response to viral social media campaigns, most meme coin transactions likely qualify as short-term capital gains subject to higher tax rates.

The challenge of determining fair market value for meme coin transactions becomes particularly complex during periods of extreme volatility when prices may fluctuate dramatically between different exchanges or even within individual trading sessions. Taxpayers must establish reasonable methods for determining fair market value that can withstand IRS scrutiny while accurately reflecting the economic reality of their transactions.

Record-Keeping Requirements and Documentation Standards

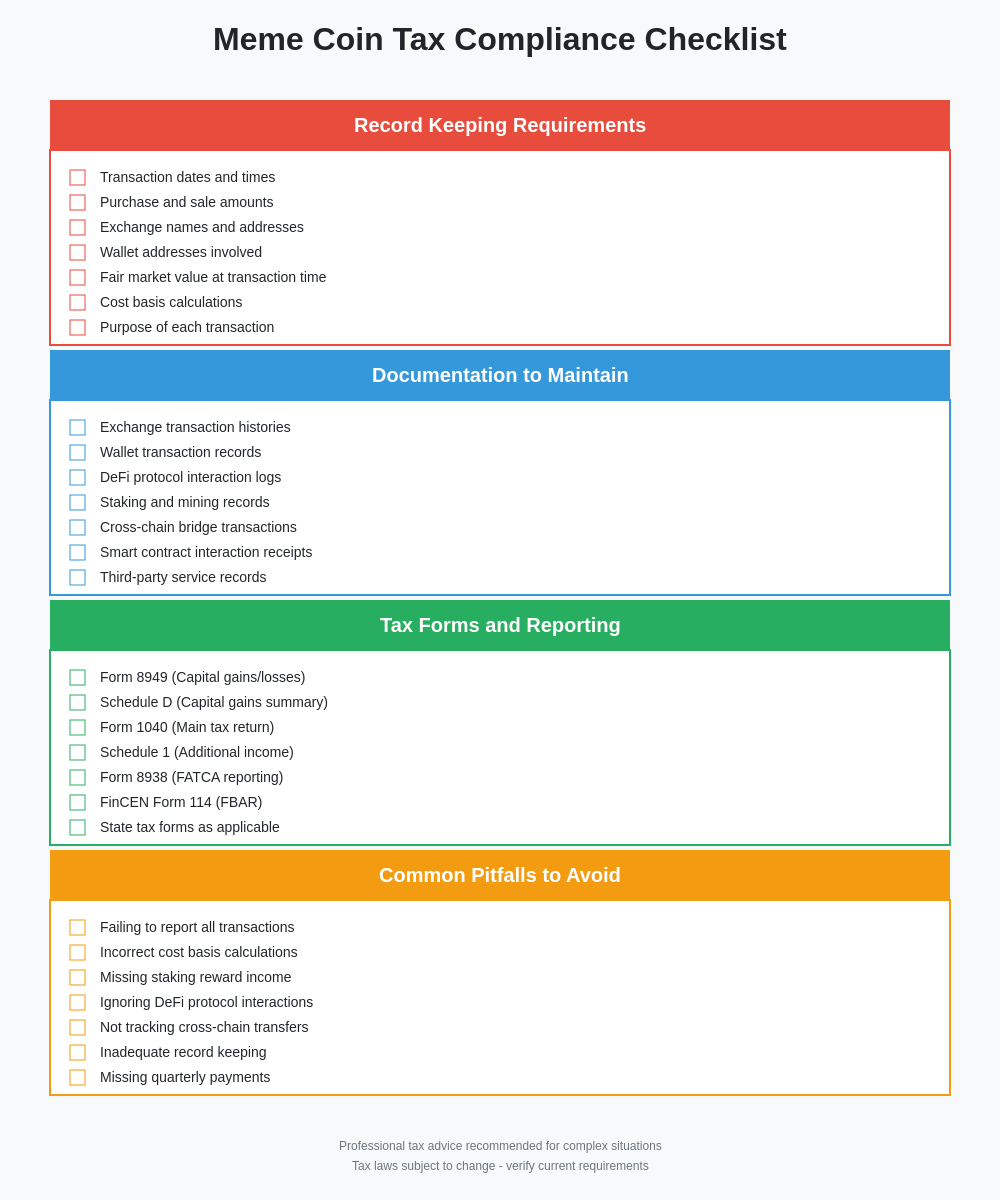

Maintaining adequate records for meme coin tax compliance requires sophisticated tracking systems that capture transaction details, cost basis calculations, and fair market value determinations for potentially thousands of individual trades across multiple exchanges and wallet addresses. The IRS expects taxpayers to maintain detailed records that include transaction dates, amounts, counterparties, fair market values, and the business purpose of each transaction, though these requirements can be overwhelming for casual investors who may not realize the complexity of their tax obligations.

Automated record-keeping solutions have emerged to help meme coin traders manage their compliance obligations, though these systems face challenges in accurately tracking transactions across decentralized exchanges, cross-chain bridges, and complex DeFi protocols that may not generate traditional transaction records. The accuracy of automated systems depends heavily on complete data feeds and proper configuration, making manual review and verification essential for ensuring compliance.

Exchange reporting requirements vary significantly across different trading platforms, with some exchanges providing comprehensive tax reporting while others offer minimal transaction history that may be insufficient for accurate tax preparation. Investors who trade across multiple platforms must aggregate data from various sources while ensuring that all transactions are properly captured and classified for tax purposes.

The documentation of meme coin mining or staking activities requires additional record-keeping for income recognition at the time rewards are received, followed by capital gains tracking when those rewards are subsequently sold or exchanged. These activities can generate complex tax scenarios where the same underlying assets create both ordinary income and capital gains tax obligations at different times.

Calculating Cost Basis in High-Volume Trading Scenarios

Determining accurate cost basis for meme coin investments becomes increasingly complex as trading volume and frequency increase, particularly for investors who may purchase the same token multiple times at different prices while maintaining ongoing positions that are periodically reduced through partial sales. The IRS requires taxpayers to use specific identification methods, first-in-first-out (FIFO), or other consistent methodologies for determining which specific tokens are being sold in each transaction.

Specific identification methods allow investors to choose which particular tokens they are selling, potentially optimizing their tax outcomes by selecting tokens with higher or lower cost basis depending on their overall tax strategy and the desire to realize gains or losses in particular tax years. However, this method requires detailed record-keeping that tracks individual token purchases and clearly identifies which specific tokens are being disposed of in each transaction.

FIFO methodology assumes that the first tokens purchased are the first tokens sold, creating a systematic approach that simplifies record-keeping but may not provide optimal tax outcomes during periods of volatile pricing. This method can be particularly disadvantageous for meme coin investors during bull markets where early purchases at low prices are automatically assigned to sales, potentially maximizing taxable gains.

Average cost basis methods, while permitted for mutual fund investments, are generally not available for cryptocurrency transactions, requiring meme coin investors to maintain lot-level tracking that can become extremely complex for high-frequency traders. The inability to use average cost methods means that investors cannot simplify their record-keeping through portfolio-level calculations that might be available for traditional securities.

Wash Sale Rules and Their Application to Cryptocurrency Trading

The application of wash sale rules to cryptocurrency trading represents one of the most uncertain areas of meme coin taxation, with significant implications for investors who engage in tax-loss harvesting strategies or who may inadvertently trigger wash sale treatment through their trading patterns. Traditional wash sale rules prohibit taxpayers from claiming tax losses on securities sales when substantially identical securities are purchased within 30 days before or after the sale, though the application of these rules to cryptocurrency remains unclear.

Current IRS guidance does not explicitly extend wash sale rules to cryptocurrency transactions, creating a potential advantage for crypto investors who can engage in tax-loss harvesting strategies that would be prohibited for traditional securities investors. However, this regulatory gap may be temporary, and investors should be prepared for potential future changes that could eliminate this advantage and possibly apply retroactively to previous tax years.

The determination of what constitutes “substantially identical” cryptocurrency becomes particularly complex for meme coins that may share similar names, technology, or cultural associations but represent legally distinct assets. For example, the relationship between various Dogecoin-inspired tokens or different versions of Pepe-themed coins could potentially trigger wash sale treatment if future regulations expand these rules to cryptocurrency.

Strategic tax planning around potential wash sale rule application requires careful consideration of trading patterns and timing, particularly for investors who maintain ongoing positions in similar meme coins or who may be tempted to repurchase recently sold positions during market downturns. The volatility patterns visible in meme coin price data often create opportunities for tax-loss harvesting that may not be available in traditional markets.

DeFi Protocol Interactions and Complex Tax Events

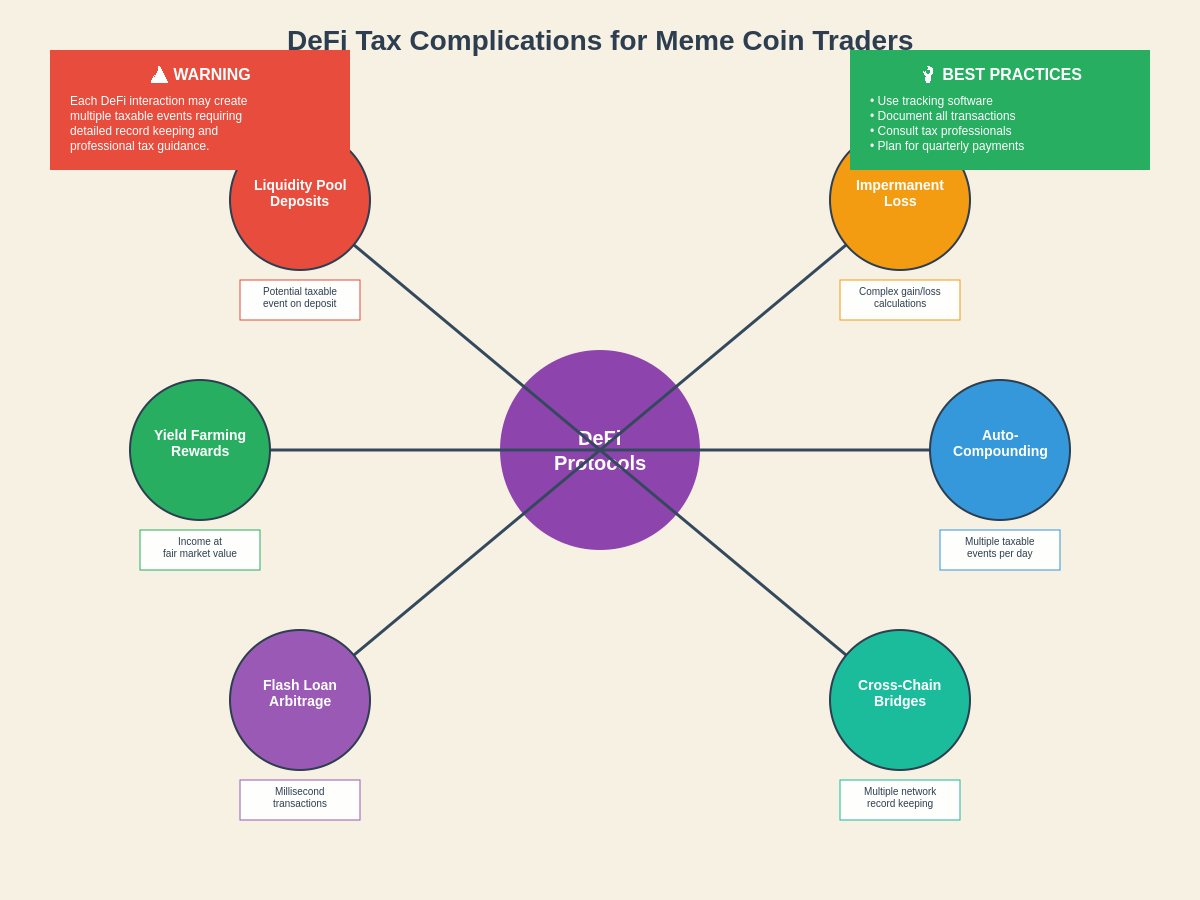

Participation in decentralized finance protocols using meme coins creates complex tax scenarios that often generate multiple taxable events within single investment strategies, requiring sophisticated analysis to properly classify income recognition, capital gains realization, and the tax treatment of various protocol rewards and incentives. These activities frequently involve token swaps, liquidity provision, yield farming, and governance participation that each carry distinct tax implications.

Liquidity provision to automated market makers (AMMs) using meme coins typically involves depositing tokens into liquidity pools in exchange for LP tokens that represent the investor’s share of the pool, creating potential taxable events at the time of deposit if the transaction is treated as a sale of the original tokens. The subsequent receipt of trading fees and protocol rewards may generate ordinary income that must be recognized at fair market value when received.

Yield farming strategies that involve staking meme coins or LP tokens to earn additional cryptocurrency rewards create ongoing income recognition requirements as rewards are distributed, followed by capital gains treatment when those rewards are subsequently sold or exchanged. The complexity increases when rewards are automatically compounded or when farming strategies involve multiple protocols with different reward structures.

Impermanent loss calculations for liquidity providers can create additional tax complexities when the relative value of paired tokens changes significantly, potentially creating taxable events that exceed the actual economic gains realized by the investor. These scenarios are particularly common with volatile meme coins that may experience dramatic price movements while paired with more stable assets.

Staking Rewards and Mining Income Classification

The tax treatment of meme coin staking rewards follows established IRS guidance for cryptocurrency mining income, requiring investors to recognize ordinary income at the fair market value of rewards when they are received, regardless of whether those rewards are immediately sold or retained for future appreciation. This income recognition creates immediate tax liabilities that may exceed the actual cash proceeds if rewards are not immediately liquidated to pay taxes.

Staking reward income must be reported at the fair market value of the tokens at the time they are received, creating valuation challenges for meme coins that may experience significant price volatility or have limited trading history on major exchanges. Taxpayers must establish reasonable methods for determining fair market value that can be consistently applied and documented for IRS review.

The subsequent sale or exchange of staking rewards creates additional capital gains or losses calculated from the fair market value established at the time the rewards were initially received as income. This double taxation effect means that staking rewards generate both ordinary income tax liability when received and potential capital gains tax when subsequently disposed of.

Delegation rewards from proof-of-stake networks and liquid staking protocols may create additional complexity where the timing of income recognition depends on when rewards become available to the staker rather than when they are actually claimed or withdrawn. These timing differences can create planning opportunities for managing tax liabilities across different tax years.

Cross-Chain Bridge Transactions and Multi-Network Activities

Cross-chain bridge transactions involving meme coins create complex tax scenarios where tokens are exchanged between different blockchain networks, potentially triggering taxable events that must be carefully analyzed to determine the appropriate tax treatment and timing of gain or loss recognition. These transactions often involve temporary holding periods and intermediate tokens that complicate traditional capital gains calculations.

The tax treatment of bridge transactions depends on whether the activity is classified as a simple transfer of the same asset between networks or as a taxable exchange of one asset for another, with significant implications for timing and amount of tax liability. The emerging consensus suggests that most bridge transactions should be treated as taxable events, though this area remains subject to ongoing clarification from tax authorities.

Wrapped token transactions that convert native blockchain tokens into ERC-20 compatible versions for use on Ethereum-based DeFi protocols may create taxable events despite the underlying economic similarity of the original and wrapped tokens. These transactions require careful analysis to determine whether gain or loss recognition is appropriate and to establish proper cost basis for the wrapped tokens.

Multi-network arbitrage strategies that exploit price differences for the same meme coin across different blockchain networks create complex tracking requirements where the same underlying asset may have different cost basis and holding period calculations depending on which network version is being traded. These strategies require sophisticated record-keeping to ensure accurate tax reporting across all networks and transactions.

State Tax Considerations and Multi-Jurisdictional Compliance

State tax treatment of meme coin investments varies significantly across different jurisdictions, with some states following federal guidance while others have developed their own cryptocurrency taxation rules that may create additional compliance requirements or planning opportunities for investors. Understanding state-specific requirements is essential for accurate tax planning and compliance, particularly for investors who may have tax obligations in multiple states.

States without personal income taxes generally do not impose additional tax obligations on cryptocurrency gains, creating potential advantages for investors who can establish residency in these jurisdictions before realizing significant meme coin profits. However, the determination of tax residency requires careful analysis of various factors including time spent in different states, location of business activities, and other connection factors.

State taxation of cryptocurrency mining and staking rewards may differ from federal treatment, with some states providing exemptions or preferential treatment for certain types of cryptocurrency income while others may impose additional taxes or reporting requirements. These differences create complexity for investors who participate in staking or mining activities while maintaining residency in states with active cryptocurrency tax regimes.

Multi-state compliance requirements for meme coin investors who trade while traveling or maintaining residences in multiple states can create complex apportionment issues where gains may be subject to taxation in multiple jurisdictions. Professional tax planning becomes essential for investors with significant holdings who may benefit from strategic residency planning or timing of major transactions.

Professional Trading Classification and Business Income Treatment

The classification of meme coin trading activities as investment or business income has significant implications for tax treatment, deduction availability, and overall tax liability, though the determination requires careful analysis of trading frequency, time commitment, and profit motive factors that may not be clear-cut for many investors. Professional trader status can provide advantages through enhanced deduction opportunities while also creating additional compliance requirements and potential audit risks.

Factors that support business income classification include full-time dedication to trading activities, substantial time commitment, significant transaction volume, and systematic trading strategies that demonstrate business-like operations rather than casual investment activity. However, the volatile nature of meme coin trading can make it difficult to demonstrate the consistent profit motive and business planning that typically support professional trader status.

Business expense deductions available to professional traders include home office expenses, computer equipment, trading software subscriptions, professional development, and travel expenses related to trading activities, though these deductions must be properly documented and directly related to the trading business. The availability of these deductions can significantly reduce the net tax impact of trading income.

Mark-to-market election allows qualifying traders to treat their trading inventory as sold at year-end, potentially simplifying the recognition of gains and losses while eliminating the need for detailed cost basis tracking throughout the year. However, this election requires careful consideration as it cannot be easily reversed and may not be advantageous in all circumstances.

International Tax Reporting and FBAR Requirements

Meme coin investments held on foreign exchanges or in foreign wallets may trigger international tax reporting requirements including Foreign Bank Account Report (FBAR) filings and Form 8938 reporting under the Foreign Account Tax Compliance Act (FATCA), creating additional compliance obligations that many investors may not realize apply to their cryptocurrency activities. These reporting requirements carry significant penalties for non-compliance and require careful analysis of the location and control of cryptocurrency assets.

FBAR reporting requirements apply to US persons who have financial interests in or signature authority over foreign financial accounts with aggregate maximum values exceeding $10,000 at any time during the calendar year. The application of these requirements to cryptocurrency held on foreign exchanges remains subject to ongoing interpretation, though conservative approaches suggest that accounts on foreign exchanges should be disclosed.

Form 8938 reporting under FATCA requires disclosure of specified foreign financial assets that exceed certain threshold amounts, with potential application to cryptocurrency held with foreign financial institutions or stored in foreign wallets. The determination of what constitutes a foreign financial institution for cryptocurrency purposes requires careful legal analysis that may benefit from professional guidance.

The intersection of international tax treaties and cryptocurrency taxation creates additional complexity for investors with international connections, potentially providing opportunities for reduced tax rates or elimination of double taxation while also creating additional compliance requirements and documentation obligations. These benefits typically require sophisticated planning and professional guidance to properly implement and maintain.

Audit Defense and IRS Examination Strategies

Meme coin tax positions face heightened audit risk due to the speculative nature of these investments, the complexity of transaction tracking, and the IRS’s increased focus on cryptocurrency compliance, making proactive audit defense preparation essential for investors with significant trading activity or unusual tax positions. Proper documentation and reasonable position support become critical for successfully defending tax treatment during IRS examination.

Documentation strategies for meme coin investments should include comprehensive transaction records, fair market value determinations with supporting data sources, written analysis of complex tax positions, and contemporaneous records of business purpose and investment strategy decisions. The volatile nature of meme coins makes real-time documentation particularly important as post-transaction reconstruction may be difficult or impossible.

Professional representation during IRS examination becomes particularly valuable for meme coin cases given the technical complexity of cryptocurrency taxation and the potential for significant tax adjustments that could result from adverse position changes. Tax professionals with cryptocurrency expertise can help navigate the examination process while protecting taxpayer rights and achieving reasonable resolutions.

Settlement strategies for meme coin tax disputes may include voluntary corrections through amended returns, participation in IRS voluntary disclosure programs, or negotiated settlements that resolve examination issues while minimizing penalties and interest charges. The complexity of tracking meme coin transactions often creates opportunities for reasonable settlement positions that acknowledge compliance challenges while demonstrating good faith efforts to determine correct tax treatment.

Planning Strategies for Future Tax Years

Effective tax planning for meme coin investments requires sophisticated strategies that account for the unique characteristics of these highly volatile assets while positioning investors to optimize their tax outcomes across multiple tax years through careful timing, loss harvesting, and income management techniques. The unpredictable nature of meme coin markets makes flexible planning approaches essential for adapting to changing circumstances.

Tax-loss harvesting strategies can be particularly effective for meme coin portfolios given the high volatility that frequently creates opportunities to realize losses for tax purposes while maintaining overall portfolio exposure to potential gains. However, these strategies require careful implementation to avoid potential wash sale issues and ensure that economic objectives remain aligned with tax optimization goals.

Charitable giving strategies using appreciated meme coins can provide significant tax advantages through elimination of capital gains tax on donated assets while providing income tax deductions for the fair market value of donated property. These strategies work particularly well for investors who have realized significant gains and wish to support charitable causes while optimizing their tax positions.

Retirement account strategies for meme coin investments may provide opportunities to defer or eliminate taxation on trading gains, though these strategies require careful consideration of prohibited transaction rules and the availability of cryptocurrency investment options within tax-advantaged accounts. Self-directed IRA structures may provide flexibility for cryptocurrency investments while maintaining tax-deferred status.

Emerging Regulatory Developments and Future Considerations

The rapidly evolving regulatory landscape for cryptocurrency taxation continues to create uncertainty for meme coin investors as the IRS develops new guidance, enforcement strategies, and reporting requirements that may significantly impact future tax planning and compliance obligations. Staying informed about regulatory developments becomes essential for maintaining compliance and optimizing tax strategies in this dynamic environment.

Proposed regulations addressing cryptocurrency taxation have included enhanced reporting requirements for exchanges, standardized cost basis reporting, and potential expansion of wash sale rules to digital assets, all of which could significantly impact the tax treatment of meme coin investments. These changes may require modifications to existing planning strategies and could affect the relative advantages of different investment approaches.

Legislative proposals for cryptocurrency taxation reform have included various approaches ranging from preferential treatment for certain types of digital asset transactions to enhanced penalties for non-compliance with reporting requirements. The ultimate direction of legislative reform remains uncertain, though the trend toward increased regulation and reporting seems likely to continue.

International coordination efforts for cryptocurrency taxation may result in standardized approaches across different jurisdictions, potentially affecting the benefits of multi-jurisdictional tax planning while creating new compliance requirements for investors with international connections. These developments require ongoing monitoring and may necessitate adjustments to existing international tax strategies.

Disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. Cryptocurrency taxation is complex and subject to changing regulations. Tax treatment may vary based on individual circumstances and jurisdiction. Readers should consult with qualified tax professionals before making decisions based on this information. The IRS requires reporting of all cryptocurrency transactions, and failure to comply with tax obligations may result in penalties and interest charges.