Revolutionary Regulatory Framework Reshaping Crypto Lending

The European Union’s Markets in Crypto-Assets (MiCA) regulation represents a watershed moment for cryptocurrency lending platforms operating within the European Economic Area, fundamentally transforming how these innovative financial services must structure their operations, manage risk, and serve customers. As the world’s first comprehensive regulatory framework for digital assets, MiCA establishes unprecedented standards for crypto lending platforms that extend far beyond traditional financial services regulation while creating both opportunities and challenges for industry participants.

TradingView analysis shows that European crypto lending platforms have experienced significant volatility following MiCA’s implementation, with compliance costs and operational restructuring creating substantial market dynamics that affect both institutional and retail lending markets. The regulatory framework’s impact on lending yields, platform availability, and customer access has reverberated throughout the global cryptocurrency ecosystem, influencing how platforms worldwide approach regulatory compliance and risk management.

The implementation of MiCA regulations has created a complex landscape where crypto lending platforms must navigate intricate licensing requirements, capital adequacy standards, customer protection measures, and operational transparency obligations that significantly exceed previous regulatory expectations. These requirements have forced platforms to fundamentally reevaluate their business models, technological infrastructure, and risk management frameworks while adapting to a regulatory environment that prioritizes consumer protection and financial stability over innovation speed.

Traditional lending platforms that previously operated in regulatory grey areas now face explicit requirements for authorization, ongoing supervision, and compliance with detailed operational standards that mirror those applied to conventional financial institutions. This transformation has created both consolidation pressures and competitive advantages, with well-capitalized platforms potentially benefiting from reduced competition while smaller platforms struggle with compliance costs and regulatory complexity.

Historical Context of Crypto Lending Regulation

The development of cryptocurrency lending services emerged organically from the broader decentralized finance movement, initially operating without specific regulatory oversight as traditional financial authorities struggled to categorize and regulate these innovative products. Early crypto lending platforms capitalized on regulatory uncertainty to offer high-yield products that attracted significant capital from both institutional and retail investors seeking alternatives to traditional banking products with historically low interest rates.

The collapse of several high-profile crypto lending platforms during 2022, including Celsius Network, BlockFi, and Voyager Digital, exposed significant consumer protection gaps and highlighted the systemic risks associated with unregulated cryptocurrency lending services. These failures resulted in billions of dollars in investor losses and demonstrated the urgent need for comprehensive regulatory frameworks that could balance innovation with adequate consumer protection and financial stability safeguards.

European regulators responded to these market failures by accelerating the development of MiCA, recognizing that cryptocurrency lending services required specific regulatory treatment that addressed their unique characteristics while providing clarity for market participants. The regulation’s development process involved extensive consultation with industry stakeholders, financial authorities, and consumer protection organizations to create a framework that could accommodate innovation while preventing the type of catastrophic failures witnessed in unregulated markets.

The regulatory approach embodied in MiCA reflects lessons learned from traditional banking crises and recognizes that cryptocurrency lending platforms perform functions similar to traditional financial institutions despite their technological innovations. This recognition led to the development of regulatory requirements that focus on fundamental risk management principles while accommodating the unique operational characteristics of blockchain-based lending services.

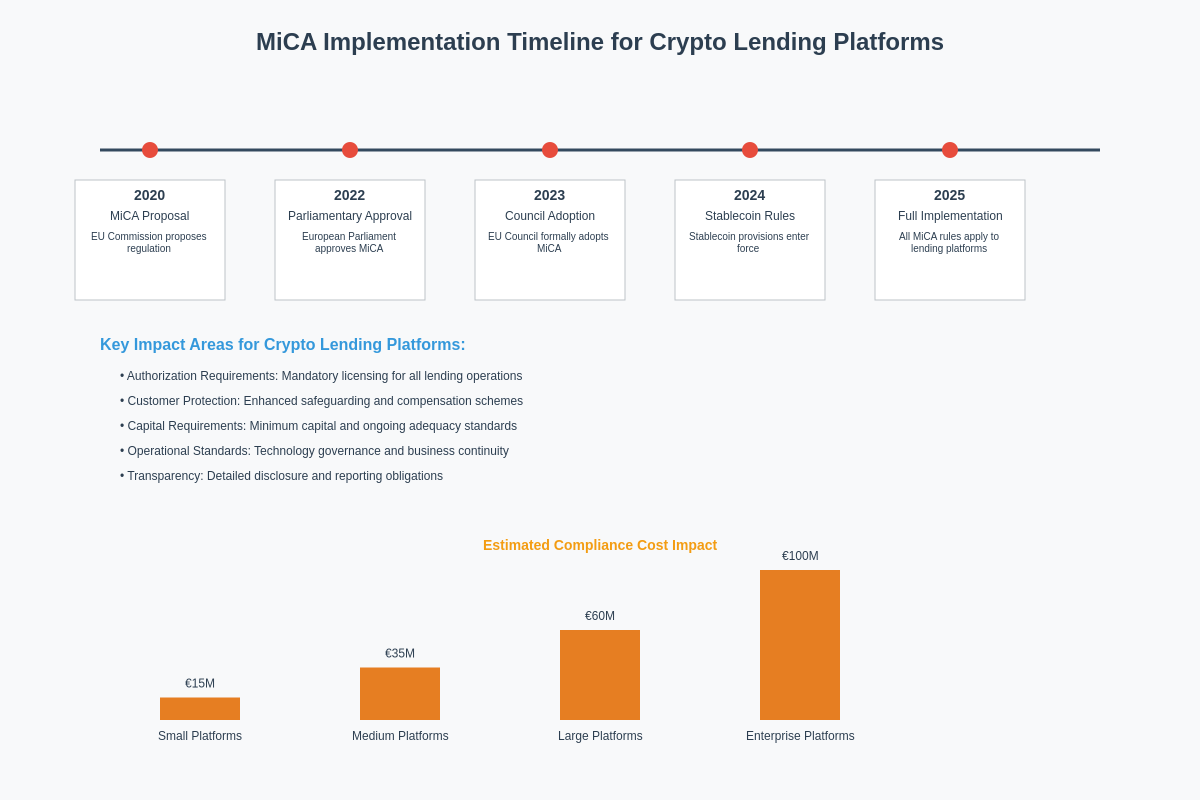

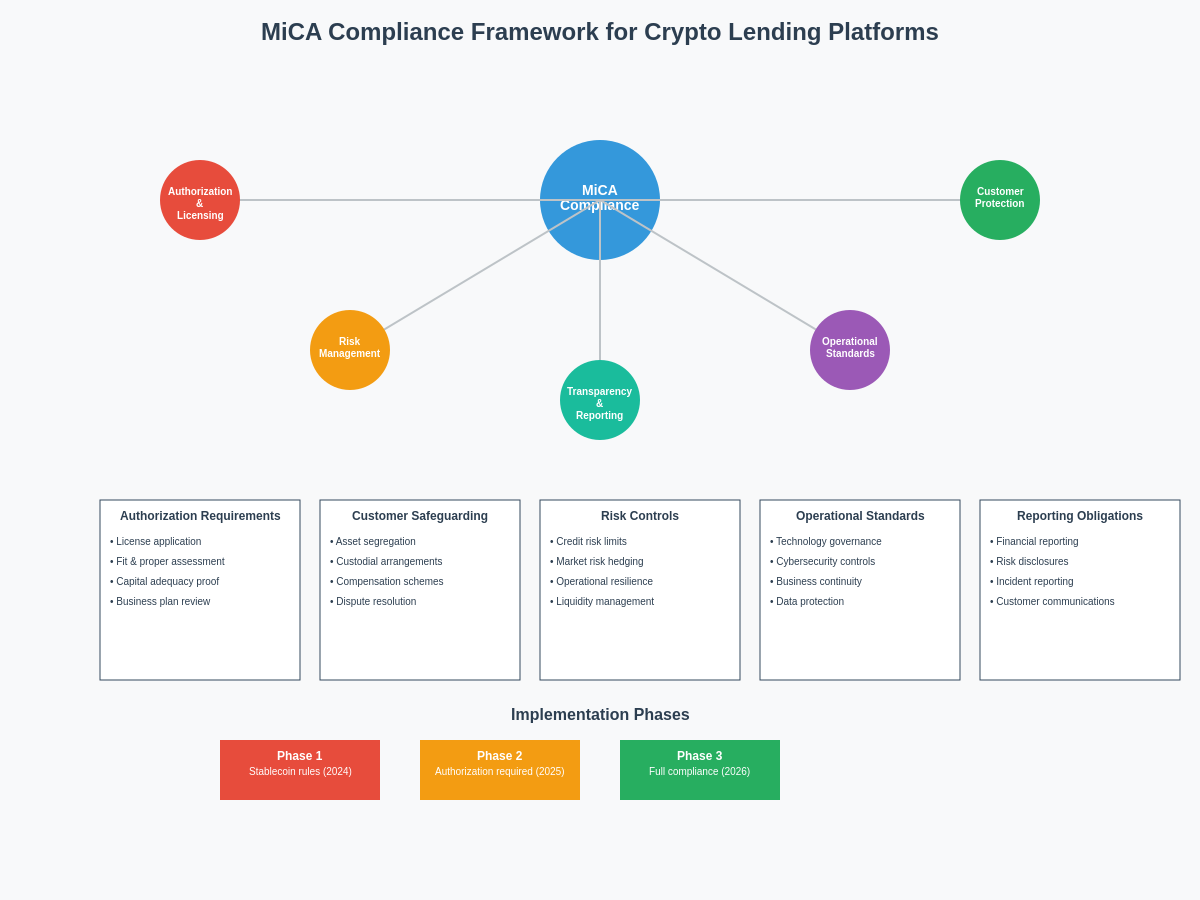

Core MiCA Requirements for Lending Platforms

MiCA establishes comprehensive authorization requirements for crypto lending platforms that must obtain specific licenses to operate within the European Union, with different categories of authorization depending on the types of services offered and the scale of operations. These licensing requirements involve detailed assessments of platform management, operational systems, risk controls, and financial resources that mirror the stringent standards applied to traditional banking institutions.

Capital adequacy requirements under MiCA mandate that crypto lending platforms maintain sufficient financial resources to absorb potential losses while continuing operations during stressed market conditions. These requirements include minimum capital thresholds, ongoing capital monitoring, and stress testing procedures that ensure platforms can meet their obligations to customers even during periods of significant market volatility or operational disruption.

Customer asset segregation represents one of the most significant operational changes required by MiCA, mandating that lending platforms maintain clear separation between customer funds and platform operational assets. This segregation requirement extends to both cryptocurrency holdings and traditional currency deposits, with specific custodial arrangements and third-party oversight mechanisms designed to protect customer assets from platform insolvency or operational failures.

Transparency and disclosure obligations under MiCA require crypto lending platforms to provide detailed information about their operations, risk factors, financial condition, and lending terms to both customers and regulatory authorities. These disclosure requirements include regular financial reporting, risk assessments, and customer communications that enable informed decision-making while providing regulators with comprehensive oversight capabilities.

The operational resilience requirements embedded in MiCA mandate that crypto lending platforms implement robust technological systems, cybersecurity measures, and business continuity procedures that can withstand various types of operational disruption. These requirements encompass technology governance, data protection, incident response procedures, and recovery planning that ensure continued service provision even during significant operational challenges.

Licensing and Authorization Framework

The MiCA licensing framework establishes multiple tiers of authorization for crypto lending platforms based on the scope and scale of their operations, with different requirements for platforms offering simple lending services versus those providing complex structured products or institutional services. This tiered approach recognizes the diversity of crypto lending business models while ensuring that regulatory requirements are proportionate to the risks and complexity associated with different types of operations.

Small-scale crypto lending platforms benefit from simplified authorization procedures under MiCA’s proportionality principle, though they must still meet core requirements related to customer protection, operational resilience, and financial soundness. These simplified procedures reduce regulatory burden for platforms with limited operations while maintaining essential safeguards that protect customers and financial stability.

Large-scale institutional crypto lending platforms face comprehensive authorization requirements that include detailed assessments of governance arrangements, risk management systems, internal controls, and senior management fitness and propriety. These assessments involve extensive documentation, on-site inspections, and ongoing supervisory engagement that ensures platforms meet the highest standards of operational excellence and customer protection.

Cross-border licensing arrangements under MiCA enable authorized crypto lending platforms to provide services throughout the European Union based on a single authorization, creating significant economies of scale for platforms that can meet the regulatory requirements. This passport approach encourages the development of pan-European crypto lending services while ensuring consistent regulatory standards across all member states.

The authorization process includes specific requirements for platform ownership structures, ensuring that beneficial owners and significant shareholders meet fitness and propriety standards while providing transparency about platform control and governance arrangements. These ownership requirements prevent inappropriate persons from controlling crypto lending platforms while enabling regulatory authorities to assess the suitability of platform ownership structures.

Customer Protection and Asset Safeguarding

MiCA’s customer protection framework for crypto lending platforms encompasses comprehensive requirements for customer asset safeguarding, dispute resolution, complaint handling, and compensation arrangements that provide multiple layers of protection for platform users. These protections recognize the unique risks associated with cryptocurrency lending while ensuring that customers receive protections comparable to those available in traditional financial services.

Asset safeguarding requirements mandate that crypto lending platforms implement qualified custodial arrangements for customer cryptocurrencies and traditional currencies, with specific requirements for custodian selection, monitoring, and oversight. These arrangements must include segregation of customer assets from platform assets, regular reconciliation procedures, and independent verification of asset holdings that protect customers from platform insolvency or operational failures.

Customer communication requirements under MiCA mandate clear and comprehensive disclosure of lending terms, risks, and potential outcomes that enable customers to make informed decisions about crypto lending products. These communication requirements include standardized risk warnings, clear explanations of lending mechanisms, and ongoing updates about platform performance and market conditions that affect customer investments.

The establishment of compensation schemes for crypto lending platform failures represents a significant innovation in customer protection, with requirements for platforms to participate in compensation arrangements that provide limited protection for customer losses resulting from platform insolvency or operational failures. While these schemes may not provide full compensation for all losses, they represent important safety nets for smaller investors who might otherwise have no recourse following platform failures.

Dispute resolution mechanisms under MiCA require crypto lending platforms to establish accessible and effective procedures for handling customer complaints and disputes, with requirements for independent dispute resolution services that provide fair and timely resolution of customer concerns. These mechanisms include both internal complaint handling procedures and access to external alternative dispute resolution services that provide customers with multiple avenues for addressing problems with platform services.

Risk Management and Compliance Obligations

The risk management framework established by MiCA for crypto lending platforms requires comprehensive identification, assessment, monitoring, and mitigation of various risk categories including credit risk, market risk, operational risk, liquidity risk, and compliance risk. These requirements mandate that platforms implement sophisticated risk management systems that can handle the unique characteristics of cryptocurrency markets while meeting traditional financial services risk management standards.

Credit risk management for crypto lending platforms involves detailed assessment of borrower creditworthiness, collateral valuation, and portfolio diversification that accounts for the volatility and correlation characteristics of cryptocurrency assets. These requirements include stress testing procedures, concentration limits, and provisioning requirements that ensure platforms can absorb potential losses from borrower defaults while maintaining operational continuity.

Market risk management requirements address the significant volatility associated with cryptocurrency markets, mandating that platforms implement comprehensive hedging strategies, position limits, and value-at-risk monitoring that protect both platform solvency and customer interests. These requirements recognize the unique market dynamics of cryptocurrency assets while ensuring that platforms maintain adequate capital buffers to absorb market-related losses.

Operational risk management encompasses cybersecurity requirements, system resilience standards, and business continuity planning that address the technological complexity and security challenges associated with cryptocurrency lending operations. These requirements include regular security assessments, incident response procedures, and recovery planning that ensure platforms can continue operating even during significant operational disruptions.

Liquidity risk management requirements mandate that crypto lending platforms maintain sufficient liquid resources to meet customer withdrawal demands and operational obligations even during stressed market conditions. These requirements include liquidity monitoring, stress testing, and contingency funding arrangements that ensure platforms can honor their commitments to customers regardless of market conditions.

Anti-money laundering and compliance obligations under MiCA require crypto lending platforms to implement comprehensive customer due diligence, transaction monitoring, and suspicious activity reporting procedures that meet or exceed traditional banking standards. These requirements recognize the potential use of cryptocurrency lending services for illicit purposes while ensuring that platforms contribute to broader financial crime prevention efforts.

Operational and Technical Standards

MiCA establishes detailed operational and technical standards for crypto lending platforms that encompass system architecture, data management, cybersecurity, and business continuity requirements designed to ensure reliable and secure service provision. These standards recognize the technological complexity of cryptocurrency operations while establishing minimum requirements for operational excellence that protect both customers and financial stability.

System architecture requirements mandate that crypto lending platforms implement robust, scalable, and secure technological infrastructure capable of handling peak transaction volumes while maintaining data integrity and customer privacy. These requirements include specific standards for system design, testing, change management, and performance monitoring that ensure platforms can provide reliable services even during periods of high demand or market stress.

Data management and privacy requirements under MiCA establish comprehensive standards for customer data collection, storage, processing, and protection that exceed general data protection regulation requirements while addressing the specific characteristics of cryptocurrency transactions. These requirements include data minimization principles, encryption standards, access controls, and breach notification procedures that protect customer privacy while enabling necessary regulatory reporting and oversight.

Cybersecurity standards for crypto lending platforms encompass comprehensive requirements for threat assessment, security controls, incident response, and recovery procedures that address the elevated cybersecurity risks associated with cryptocurrency operations. These standards include regular security testing, vulnerability assessments, and security awareness training that ensure platforms maintain effective defenses against evolving cyber threats.

Business continuity and disaster recovery requirements mandate that crypto lending platforms implement comprehensive procedures for maintaining operations during various types of disruption, including natural disasters, cyber attacks, and key personnel unavailability. These requirements include backup systems, alternative operating procedures, and recovery testing that ensure platforms can restore normal operations quickly following significant disruptions.

Technology governance requirements establish standards for platform oversight of technological systems, including board-level responsibility for technology strategy, risk management, and performance monitoring. These governance requirements ensure that platform management maintains appropriate oversight of technological operations while implementing effective controls and accountability mechanisms that support reliable service provision.

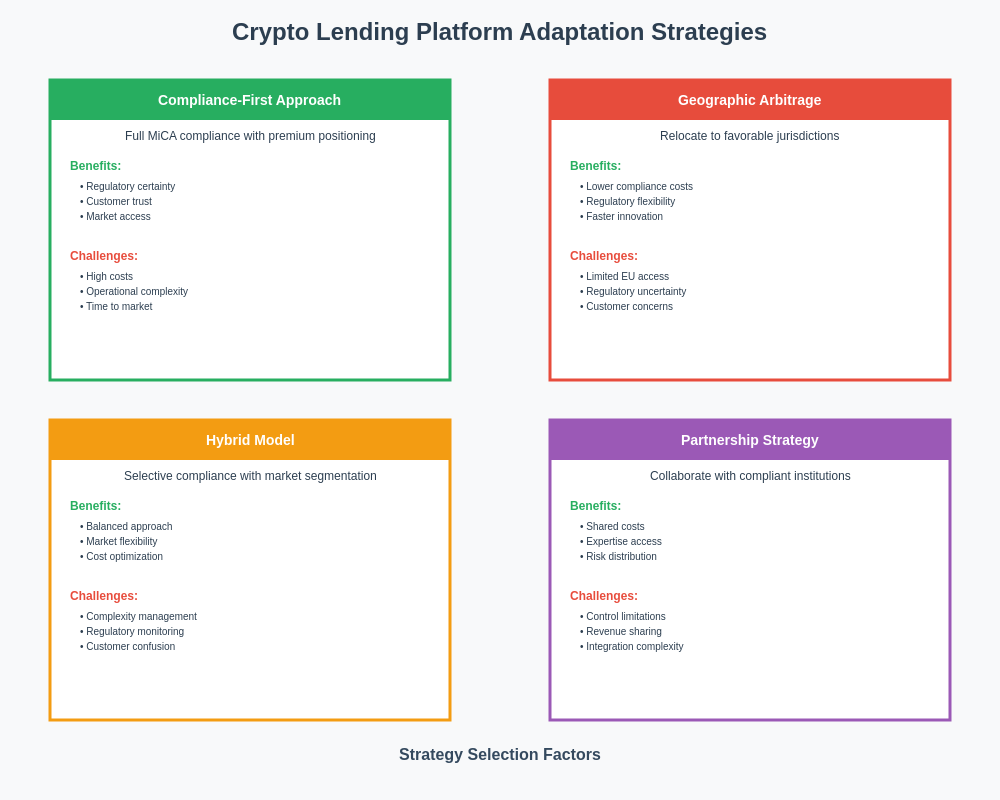

Market Impact and Platform Adaptation

The implementation of MiCA regulations has created significant market restructuring within the European crypto lending sector, with platforms pursuing various adaptation strategies including business model modifications, geographical repositioning, and strategic partnerships that enable continued operations within the new regulatory framework. These adaptations have created both consolidation pressures and competitive advantages that are reshaping the industry landscape in fundamental ways.

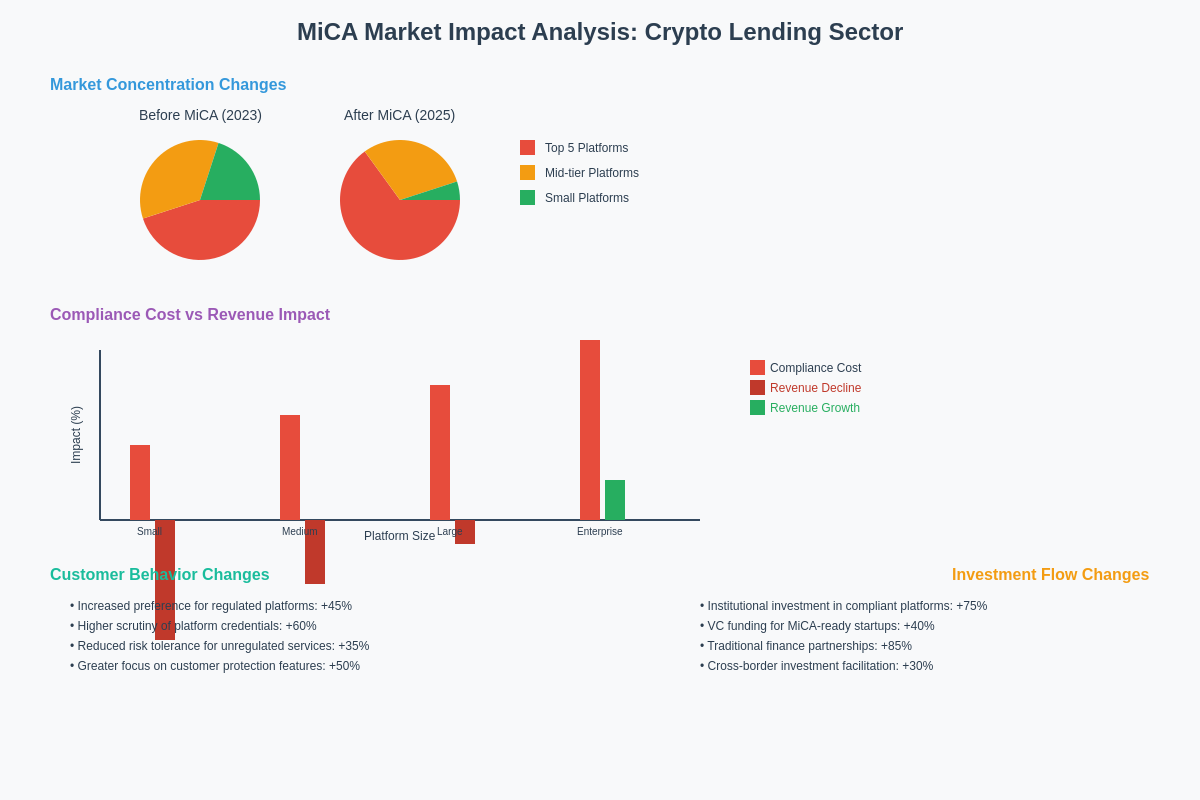

Compliance costs associated with MiCA implementation have created significant barriers to entry for new crypto lending platforms while imposing substantial ongoing operational expenses on existing platforms. TradingView data indicates that these costs have contributed to market consolidation, with smaller platforms either exiting the market or merging with larger competitors that can better absorb regulatory compliance expenses.

Geographic arbitrage has emerged as a significant strategic consideration for crypto lending platforms, with some providers relocating operations to jurisdictions with more favorable regulatory environments while others have chosen to embrace MiCA compliance as a competitive advantage in the European market. This geographic restructuring has created complex operational challenges related to customer service, regulatory compliance, and business continuity that require sophisticated management approaches.

Product innovation within MiCA-compliant crypto lending platforms has focused on developing new service offerings that meet regulatory requirements while providing competitive returns and customer value. These innovations include structured products, institutional services, and hybrid traditional-digital asset offerings that leverage regulatory compliance as a foundation for expanding market reach and customer trust.

The emergence of regulatory technology solutions specifically designed for crypto lending platform compliance has created new opportunities for specialized service providers while reducing the burden on individual platforms to develop comprehensive compliance capabilities internally. These RegTech solutions encompass automated reporting, risk monitoring, customer onboarding, and regulatory change management that enable platforms to maintain compliance more efficiently and effectively.

Customer behavior changes following MiCA implementation have included increased focus on platform regulatory status, greater scrutiny of terms and conditions, and heightened awareness of customer protection arrangements that influence platform selection decisions. These behavioral changes have created competitive advantages for compliant platforms while pressuring non-compliant providers to either achieve compliance or exit European markets.

Cross-Border Implications and Global Standards

MiCA’s extraterritorial effects extend beyond European Union borders through requirements that affect crypto lending platforms serving European customers regardless of their operational location, creating global compliance challenges that require sophisticated legal and operational responses. These extraterritorial provisions have established de facto global standards for crypto lending platform operations that influence regulatory development in other jurisdictions.

The interaction between MiCA requirements and existing national regulatory frameworks in EU member states has created complex compliance environments where crypto lending platforms must navigate multiple overlapping regulatory requirements. This regulatory complexity has required platforms to develop sophisticated compliance management systems while working with multiple regulatory authorities to ensure comprehensive compliance with all applicable requirements.

International cooperation mechanisms established under MiCA enable European regulators to share information and coordinate oversight activities with regulatory authorities in other jurisdictions, creating enhanced supervisory capabilities that extend beyond traditional territorial boundaries. These cooperation mechanisms have implications for crypto lending platforms with global operations that must consider cross-border regulatory coordination in their compliance planning and risk management strategies.

The influence of MiCA on regulatory development in other major jurisdictions has been significant, with regulators in the United States, United Kingdom, Asia-Pacific region, and other markets incorporating elements of the European approach into their own regulatory frameworks. This regulatory convergence has created opportunities for platforms that achieve MiCA compliance to more easily expand into other markets while establishing global best practices for crypto lending platform operations.

Regulatory arbitrage opportunities and challenges created by differences between MiCA and other jurisdictional approaches have influenced platform strategic planning and operational structuring decisions. These considerations include choice of operational jurisdiction, customer segmentation strategies, and service offering designs that optimize regulatory compliance costs while maximizing market access and competitive positioning.

Economic Impact Assessment

The economic implications of MiCA implementation on crypto lending platforms encompass direct compliance costs, operational restructuring expenses, and broader market effects that influence platform profitability, customer pricing, and competitive dynamics. Initial assessments suggest that compliance costs represent a significant proportion of platform operational expenses, particularly for smaller providers that lack economies of scale in regulatory compliance.

Revenue model adjustments necessitated by MiCA compliance have included changes to fee structures, interest rate offerings, and service packaging that reflect increased operational costs while maintaining competitive positioning. These adjustments have created pricing pressures that affect customer acquisition and retention while influencing overall market dynamics and profitability levels across the industry.

Investment patterns in the European crypto lending sector have shifted significantly following MiCA implementation, with institutional investors showing increased interest in compliant platforms while expressing greater caution about providers that lack clear regulatory status. European cryptocurrency markets have reflected these investment pattern changes through modified valuations, funding availability, and strategic partnership opportunities that favor regulatory-compliant providers.

Employment and skills development within the crypto lending industry have been significantly affected by MiCA requirements, with increased demand for compliance professionals, risk management specialists, and regulatory technology experts. These employment effects have created both opportunities and challenges for platforms seeking to build necessary compliance capabilities while managing operational costs and maintaining competitive staffing levels.

The broader financial system impacts of MiCA-compliant crypto lending platforms include enhanced integration with traditional banking services, improved institutional acceptance, and reduced systemic risk concerns that facilitate greater mainstream adoption. These systemic benefits create long-term value for compliant platforms while contributing to overall financial system stability and consumer confidence in cryptocurrency services.

Innovation incentives and constraints created by MiCA implementation present complex trade-offs between regulatory compliance and technological advancement, with platforms needing to balance innovation speed with regulatory requirements. This balance has influenced product development priorities, technology investment decisions, and strategic partnerships that shape the future evolution of crypto lending services within the European market.

Enforcement and Supervisory Approach

The supervisory framework for MiCA compliance in crypto lending platforms involves coordination between European Securities and Markets Authority oversight and national competent authority supervision, creating a multi-layered regulatory structure that provides comprehensive coverage while avoiding supervisory gaps. This supervisory approach emphasizes ongoing monitoring, regular assessment, and proactive intervention that ensures sustained compliance with regulatory requirements.

Enforcement mechanisms available to supervisory authorities include administrative sanctions, operational restrictions, license suspension or revocation, and financial penalties that provide strong incentives for platform compliance with MiCA requirements. These enforcement tools are designed to be proportionate to violations while providing sufficient deterrent effects that maintain high standards of compliance across the industry.

Supervisory technology and data analytics capabilities deployed by regulatory authorities enable comprehensive monitoring of crypto lending platform operations, risk profiles, and customer outcomes that support effective oversight and early intervention. These technological capabilities include automated reporting analysis, transaction monitoring, and risk assessment tools that enhance supervisory effectiveness while reducing regulatory burden on compliant platforms.

International supervisory cooperation arrangements facilitate information sharing and coordinated enforcement actions that address the global nature of crypto lending platform operations while ensuring comprehensive regulatory coverage. These cooperation mechanisms include mutual recognition agreements, information sharing protocols, and joint investigation procedures that enhance the effectiveness of cross-border supervision and enforcement.

The development of supervisory best practices and guidance documents provides clarity for crypto lending platforms regarding regulatory expectations while establishing consistent supervisory approaches across different member states and regulatory authorities. These guidance documents address common compliance challenges, clarify regulatory requirements, and provide practical examples that support effective platform compliance efforts.

Stakeholder engagement processes embedded in the supervisory framework provide opportunities for crypto lending platforms to contribute to regulatory development while receiving guidance on compliance challenges and emerging issues. These engagement mechanisms include regular consultation procedures, industry working groups, and bilateral meetings that facilitate constructive dialogue between platforms and regulatory authorities.

Technology and Innovation Considerations

The intersection between MiCA compliance requirements and blockchain technology innovation creates both opportunities and constraints for crypto lending platforms seeking to develop new products and services while maintaining regulatory compliance. This intersection requires careful consideration of technological capabilities, regulatory requirements, and customer needs that influence platform development strategies and innovation priorities.

Smart contract governance and audit requirements under MiCA mandate that crypto lending platforms implement comprehensive oversight of automated systems and algorithmic processes that affect customer funds and platform operations. These requirements include code review procedures, security testing protocols, and ongoing monitoring systems that ensure smart contract reliability while maintaining regulatory compliance.

Decentralized finance integration challenges arise from the tension between MiCA’s emphasis on centralized accountability and oversight and the distributed nature of DeFi protocols that many crypto lending platforms utilize. These challenges require innovative approaches to regulatory compliance that maintain the benefits of decentralized systems while meeting centralized regulatory requirements for customer protection and operational oversight.

Privacy-preserving technologies and their compatibility with MiCA transparency and reporting requirements create complex technical and regulatory challenges that require sophisticated solutions. These challenges include balancing customer privacy protection with regulatory reporting obligations while maintaining the security and efficiency benefits of privacy-preserving technologies in crypto lending operations.

Interoperability standards and cross-chain operations present additional complexity for MiCA-compliant crypto lending platforms that must ensure regulatory compliance across multiple blockchain networks and protocol implementations. These technical challenges require comprehensive risk assessment, operational controls, and monitoring capabilities that address the complexity of multi-chain operations while maintaining regulatory compliance.

The development of regulatory technology solutions specifically designed for crypto lending platform compliance has created new opportunities for innovation in compliance management, risk monitoring, and regulatory reporting. These RegTech innovations include automated compliance monitoring, real-time risk assessment, and standardized reporting tools that reduce compliance burden while enhancing regulatory effectiveness.

Future Regulatory Evolution

The ongoing development of MiCA implementation guidance and technical standards continues to shape the regulatory landscape for crypto lending platforms, with regular updates and clarifications that address emerging issues and market developments. This evolutionary approach to regulatory implementation requires platforms to maintain flexible compliance capabilities while adapting to changing regulatory expectations and market conditions.

Potential amendments and enhancements to MiCA that could affect crypto lending platforms include expanded scope of application, enhanced customer protection measures, and additional operational requirements that reflect lessons learned from initial implementation experience. These potential changes require platforms to monitor regulatory developments closely while maintaining adaptable compliance frameworks that can accommodate future regulatory evolution.

International regulatory coordination efforts aimed at establishing global standards for crypto lending platform regulation continue to influence the development of international best practices and harmonized approaches. These coordination efforts include bilateral agreements, multilateral cooperation frameworks, and international standard-setting initiatives that may influence future regulatory requirements for platforms with global operations.

The integration of environmental, social, and governance considerations into crypto lending platform regulation represents an emerging trend that could significantly impact future regulatory requirements. These ESG considerations include energy consumption disclosure, social impact assessment, and governance standard enhancement that reflect broader policy priorities related to sustainable finance and responsible business practices.

Technological advancement impacts on regulatory requirements include the potential need for updated standards related to quantum computing threats, artificial intelligence applications, and advanced cryptographic techniques that could affect crypto lending platform operations. These technological developments require ongoing regulatory assessment and potential framework updates that ensure continued effectiveness of customer protection and financial stability measures.

Market structure evolution and its regulatory implications encompass potential changes to crypto lending business models, competitive dynamics, and systemic importance that could necessitate adjustments to regulatory approaches and requirements. This market evolution requires ongoing monitoring and assessment by both platforms and regulatory authorities to ensure that regulatory frameworks remain appropriate and effective as markets continue to develop and mature.

Strategic Recommendations for Platforms

Successful adaptation to MiCA requirements necessitates comprehensive strategic planning that addresses regulatory compliance, operational efficiency, and competitive positioning within the evolving European crypto lending market. Platforms should prioritize early compliance achievement to capitalize on competitive advantages while building sustainable compliance capabilities that support long-term operational success.

Investment in regulatory technology and compliance infrastructure represents a critical success factor for crypto lending platforms operating under MiCA, with platforms needing to balance initial investment costs against long-term operational efficiency and regulatory effectiveness. These investments should focus on scalable solutions that can adapt to evolving regulatory requirements while providing comprehensive compliance management capabilities.

Human capital development strategies should emphasize building internal expertise in regulatory compliance, risk management, and customer protection that enables platforms to maintain high standards of regulatory compliance while supporting business growth and innovation objectives. These strategies include targeted recruitment, training programs, and knowledge management systems that build sustainable compliance capabilities.

Customer communication and education initiatives represent important opportunities for MiCA-compliant platforms to differentiate themselves in the market while building customer trust and loyalty through transparency and educational support. These initiatives should focus on clear explanation of regulatory protections, risk factors, and platform capabilities that enable customers to make informed decisions about crypto lending services.

Strategic partnerships and collaboration opportunities with traditional financial institutions, technology providers, and other crypto service providers can provide platforms with additional capabilities and resources that support MiCA compliance while expanding market reach and customer access. These partnerships should be structured to maintain regulatory compliance while providing mutual benefits that enhance competitive positioning.

Continuous monitoring and adaptation capabilities are essential for maintaining effective MiCA compliance as regulatory requirements evolve and market conditions change. Platforms should implement comprehensive monitoring systems that track regulatory developments, market trends, and operational performance indicators that inform strategic decision-making and risk management activities.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Cryptocurrency lending involves significant risks including potential loss of principal. Past performance does not guarantee future results. Always conduct thorough research and consult with qualified professionals before making financial decisions. Regulatory requirements may vary by jurisdiction and are subject to change.