Start with TradingView to analyze cryptocurrency lending market trends and make informed decisions about centralized lending platforms that have shaped the cryptocurrency financial services landscape.

The Rise and Fall of Centralized Crypto Lending

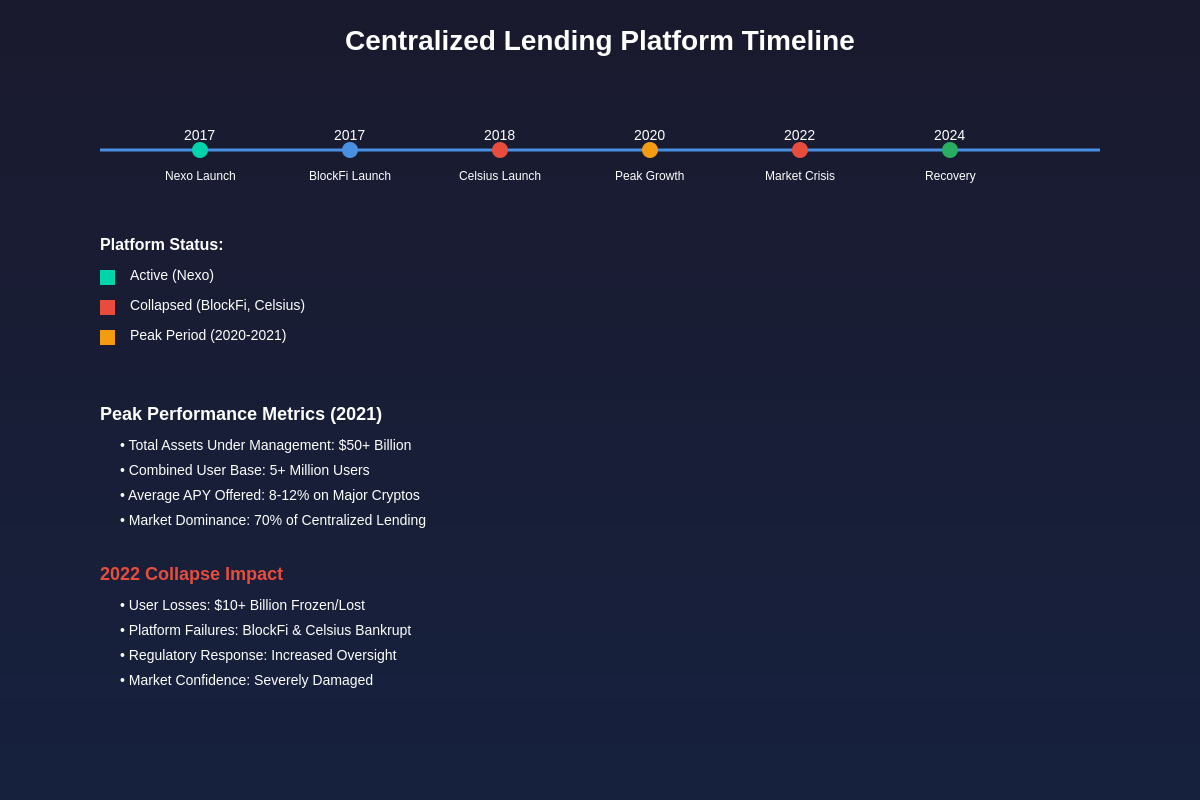

The centralized cryptocurrency lending sector experienced a meteoric rise and dramatic collapse between 2018 and 2022, with platforms like Nexo, BlockFi, and Celsius attracting billions of dollars in user deposits by promising attractive yields on cryptocurrency holdings while providing sophisticated financial services that bridged traditional finance and the emerging digital asset ecosystem. These platforms fundamentally changed how cryptocurrency holders approached passive income generation, offering yields that far exceeded traditional banking products while leveraging the unique properties of digital assets to create new financial products and services.

The business model employed by these centralized lending platforms relied on accepting user deposits of various cryptocurrencies, paying attractive interest rates to depositors, and then lending these assets to institutional borrowers, market makers, and other professional participants at higher rates to generate profit margins. This seemingly straightforward approach concealed significant complexities related to risk management, regulatory compliance, market volatility, and operational security that would ultimately lead to the downfall of several major platforms and fundamentally reshape the sector.

The collapse of major players in this space, particularly Celsius and BlockFi, sent shockwaves through the cryptocurrency industry and highlighted the risks associated with centralized custody models, unclear regulatory frameworks, and aggressive yield-seeking strategies that prioritized growth over sustainable risk management. Understanding the evolution, operations, and ultimate fate of these platforms provides crucial insights into the challenges and opportunities within cryptocurrency financial services while illustrating the importance of due diligence and risk assessment in the rapidly evolving digital asset landscape.

Nexo: The European Pioneer in Crypto Lending

Nexo emerged as one of the earliest and most prominent centralized cryptocurrency lending platforms, founded in 2017 by the team behind Credissimo, a European fintech company with extensive experience in traditional lending markets. The platform positioned itself as a bridge between traditional finance and cryptocurrency markets, offering institutional-grade services with regulatory compliance as a core differentiator in a market that was largely unregulated and dominated by platforms operating in regulatory gray areas.

The company’s approach to cryptocurrency lending emphasized transparency, regulatory compliance, and risk management from its inception, obtaining various licenses and certifications across multiple jurisdictions including the European Union, where it operated under more stringent regulatory oversight than many of its competitors. Nexo’s business model centered on providing instant crypto-backed loans, earning interest on cryptocurrency deposits, and offering a proprietary token (NEXO) that provided various benefits and governance rights to holders while serving as a key component of the platform’s economic model.

Nexo’s lending services allowed users to borrow fiat currencies or stablecoins against cryptocurrency collateral without requiring traditional credit checks or lengthy approval processes, making it particularly attractive to cryptocurrency holders who wanted to access liquidity without selling their digital assets. The platform supported a wide range of collateral types including Bitcoin, Ethereum, and various altcoins, with loan-to-value ratios and interest rates determined by the type and amount of collateral provided as well as the user’s loyalty tier within the platform’s reward system.

The interest-earning component of Nexo’s service offering enabled users to deposit cryptocurrencies and earn competitive yields, with rates varying based on the specific cryptocurrency, deposit amount, and the user’s NEXO token holdings. The platform implemented a tiered system where users holding larger amounts of NEXO tokens received preferential interest rates, lower borrowing costs, and additional platform benefits, creating incentives for users to purchase and hold the platform’s native token while generating additional revenue streams for the company.

Nexo’s risk management approach included real-time portfolio monitoring, automated liquidation systems, and insurance coverage for digital assets held in custody, though the specific details and limitations of these protections were not always fully transparent to users. The platform claimed to employ institutional-grade security measures including multi-signature wallets, cold storage systems, and regular security audits, though the effectiveness of these measures was never tested by a major security breach during the platform’s operational period.

BlockFi: Institutional Backing Meets Retail Innovation

BlockFi launched in 2017 with significant institutional backing and a focus on bringing Wall Street-style cryptocurrency financial services to both retail and institutional clients, positioning itself as a more traditional and regulated approach to cryptocurrency lending compared to many of its competitors. The platform attracted substantial venture capital investment from prominent firms and established partnerships with major financial institutions, lending credibility to its operations and enabling rapid growth in user adoption and assets under management.

The company’s core business model revolved around accepting cryptocurrency deposits from users, paying competitive interest rates on these deposits, and then lending the assets to institutional borrowers including hedge funds, market makers, and other professional trading firms at higher rates to generate profit margins. BlockFi differentiated itself through its emphasis on transparency, regulatory compliance, and institutional-grade risk management practices, though these claims would later be called into question during the platform’s eventual collapse.

BlockFi’s interest account product allowed users to earn yields on various cryptocurrencies including Bitcoin, Ethereum, and stablecoins, with interest rates that were initially among the most competitive in the market. The platform implemented a tiered interest rate structure where rates decreased for larger deposit amounts, though users could maintain higher rates by holding a certain amount of the platform’s credit card rewards or meeting other criteria within the platform’s ecosystem.

The lending component of BlockFi’s service offering provided cryptocurrency-backed loans to users who wanted to access fiat currency liquidity without selling their digital assets, with loan terms and rates that were generally more favorable than traditional financial institutions but less attractive than some pure-play cryptocurrency lending platforms. The platform supported various cryptocurrencies as collateral and offered both USD and GUSD loans, with automated liquidation systems designed to protect the platform from collateral value declines.

BlockFi’s approach to risk management included partnerships with established custody providers, insurance coverage for digital assets, and sophisticated monitoring systems designed to track collateral values and trigger liquidations when necessary. However, the platform’s aggressive growth strategy and exposure to various market participants, including the failed hedge fund Three Arrows Capital, would ultimately contribute to its downfall when market conditions deteriorated and counterparty risks materialized.

The platform’s regulatory approach involved engaging with various jurisdictions and seeking appropriate licenses and registrations, though this process was complex and evolving as regulatory frameworks for cryptocurrency financial services were still being developed. BlockFi’s attempts to launch an IPO and operate as a more traditional financial services company were hampered by regulatory uncertainty and changing market conditions that ultimately made these ambitions impossible to achieve.

Celsius: Community-Driven Yield Generation

Celsius Network positioned itself as a community-driven alternative to traditional banking, founded by Alex Mashinsky with the mission of “unbanking” users by providing better financial services through cryptocurrency and blockchain technology. The platform’s marketing emphasized its commitment to sharing profits with users rather than enriching shareholders, though this populist messaging concealed significant operational and financial risks that would ultimately lead to the platform’s spectacular collapse.

The company’s approach to cryptocurrency lending was built around accepting user deposits of various digital assets, paying attractive interest rates to depositors, and using these funds for a variety of activities including lending to institutional borrowers, market making, staking, and trading activities designed to generate returns that could support the yields promised to users. Celsius differentiated itself through aggressive marketing, celebrity endorsements, and interest rates that were often higher than competitors, attracting billions of dollars in user deposits at the platform’s peak.

Celsius’s business model included several revenue streams beyond traditional lending, including participation in DeFi protocols, cryptocurrency mining operations, and various trading strategies that were designed to generate yields but also introduced additional risks and complexities that were not always fully disclosed to users. The platform’s native CEL token played a central role in its economic model, with token holders receiving preferential interest rates and other benefits while the platform used CEL tokens for various operational purposes including collateral management and loyalty rewards.

The platform’s approach to transparency was mixed, with regular community calls and updates from leadership providing some insights into operations while critical financial and risk management details remained opaque to users and regulators. Celsius claimed to employ sophisticated risk management practices and security measures, though subsequent revelations during the platform’s bankruptcy proceedings revealed significant gaps in risk controls and questionable decision-making that contributed to user losses.

Celsius’s regulatory strategy was less defined than some competitors, with the platform operating in various jurisdictions without clear regulatory approval while facing increasing scrutiny from authorities concerned about the platform’s business practices and financial stability. The platform’s rapid growth and aggressive yield strategies attracted regulatory attention that ultimately contributed to operational challenges and funding difficulties that preceded the platform’s collapse.

The social and community aspects of Celsius were central to its branding and user acquisition strategy, with the platform emphasizing its mission to disrupt traditional banking while building a loyal user base through social media engagement, community events, and marketing campaigns that positioned Celsius as a movement rather than simply a financial services provider. This community-driven approach helped drive rapid growth but also created additional reputational and legal risks when the platform’s financial difficulties became apparent.

Comparative Analysis of Platform Features

The three major centralized lending platforms each developed distinct approaches to cryptocurrency financial services, with significant differences in their product offerings, risk management practices, regulatory strategies, and business models that reflected their founders’ philosophies and target markets. Understanding these differences provides important insights into the evolution of the cryptocurrency lending sector and the factors that contributed to the success or failure of different platforms.

Nexo’s approach emphasized regulatory compliance and institutional-grade services, with a focus on European markets where regulatory frameworks were more developed and enforcement was more consistent. The platform’s product suite included both lending and borrowing services, with a sophisticated tiered system based on NEXO token holdings that incentivized users to invest in the platform’s ecosystem while providing preferential terms to larger users and token holders.

BlockFi positioned itself as a bridge between traditional finance and cryptocurrency markets, attracting institutional investment and partnerships while serving both retail and professional clients. The platform’s emphasis on transparency and regulatory compliance was supported by significant compliance investments and legal engagement, though these efforts were ultimately insufficient to navigate the complex and evolving regulatory landscape for cryptocurrency financial services.

Celsius differentiated itself through aggressive marketing, community engagement, and yield offerings that were often higher than competitors, attracting a large and loyal user base while generating significant media attention and brand recognition. However, the platform’s focus on growth and yield generation came at the expense of risk management and regulatory compliance, contributing to the operational and financial challenges that led to its collapse.

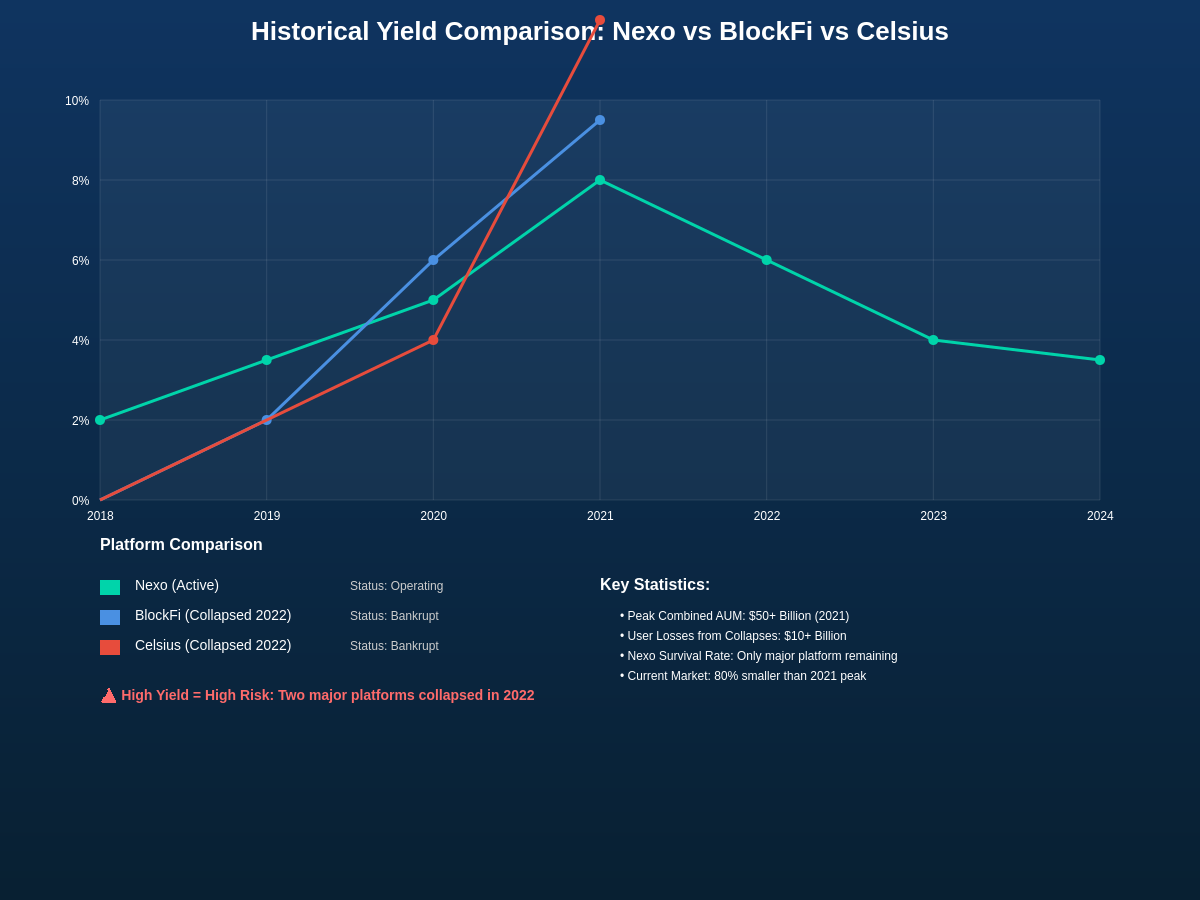

Interest rate offerings across the three platforms varied significantly based on the specific cryptocurrency, deposit amounts, loyalty tier, and market conditions, with each platform implementing different strategies for managing the balance between attractive user yields and sustainable business operations. TradingView’s comprehensive market data provides valuable insights into the yield curves and market dynamics that influenced these platforms’ pricing strategies and risk management decisions.

The lending components of each platform also differed in terms of supported collateral types, loan-to-value ratios, interest rates, and liquidation procedures, reflecting different approaches to credit risk management and target market preferences. These differences were important factors in user decision-making and contributed to the competitive dynamics within the centralized cryptocurrency lending sector.

Risk Management and Security Approaches

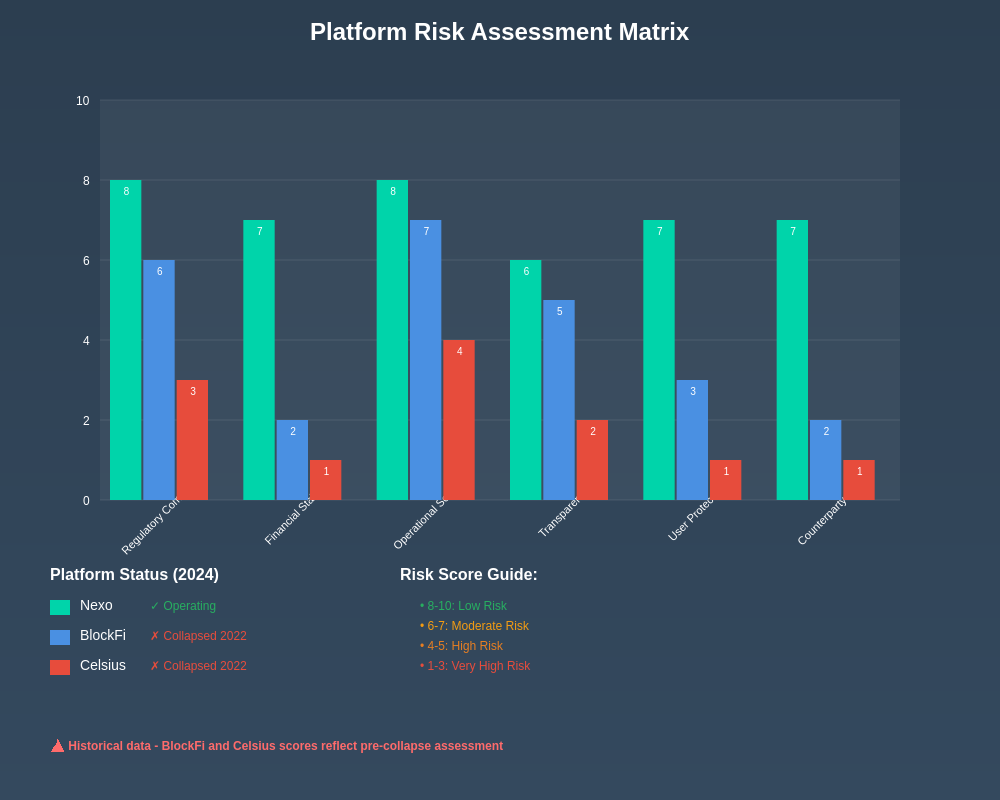

Risk management practices varied significantly among the three major centralized lending platforms, with each implementing different strategies for managing credit risk, market risk, operational risk, and regulatory risk that reflected their business models, target markets, and risk tolerances. Understanding these approaches provides crucial insights into the factors that contributed to platform success or failure during various market conditions and stress events.

Nexo’s risk management approach emphasized diversification across multiple asset types, borrower categories, and geographic regions, with sophisticated monitoring systems designed to track collateral values, borrower creditworthiness, and market conditions in real-time. The platform implemented automated liquidation systems, insurance coverage, and reserve fund mechanisms designed to protect user deposits while maintaining operational stability during market volatility.

BlockFi employed institutional-grade risk management practices including comprehensive due diligence procedures for borrowers, sophisticated collateral management systems, and regular stress testing designed to evaluate the platform’s resilience under various market scenarios. However, the platform’s exposure to major market participants like Three Arrows Capital created concentration risks that were not adequately hedged or disclosed, contributing to significant losses when these counterparties failed.

Celsius’s approach to risk management was less transparent and ultimately less effective, with the platform engaging in various high-risk activities including illiquid investments, complex trading strategies, and exposure to volatile DeFi protocols that generated additional risks while potentially providing higher returns. The platform’s risk management failures became apparent during market stress events when liquidity constraints and asset-liability mismatches created operational difficulties that ultimately led to user withdrawals being suspended.

Security practices across the three platforms included various combinations of cold storage systems, multi-signature wallets, insurance coverage, and monitoring systems designed to protect user funds from theft, hacking, and operational errors. However, the effectiveness of these security measures was often difficult for users to evaluate, and the platforms’ custody practices were not always as transparent as users might have preferred.

The platforms’ approaches to regulatory risk management varied significantly, with Nexo emphasizing compliance with European regulations, BlockFi attempting to engage constructively with U.S. regulators, and Celsius adopting a more aggressive approach that prioritized growth over regulatory compliance. These different strategies had significant implications for the platforms’ operational sustainability and legal exposure as regulatory scrutiny increased.

The Collapse of Celsius and BlockFi

The collapse of Celsius Network and BlockFi in 2022 represented one of the most significant failures in cryptocurrency financial services history, wiping out billions of dollars in user funds and fundamentally reshaping the centralized lending landscape. These failures highlighted the risks associated with centralized custody models, aggressive growth strategies, and inadequate risk management practices while demonstrating the importance of regulatory oversight and transparency in cryptocurrency financial services.

Celsius’s collapse began with liquidity constraints and user withdrawal restrictions in June 2022, followed by bankruptcy filing and revelations about the platform’s financial condition that shocked users and industry observers. Investigation into the platform’s operations revealed significant asset-liability mismatches, exposure to failed investments including Terra/Luna ecosystem projects, and questionable lending practices that prioritized yield generation over risk management.

The platform’s exposure to various DeFi protocols, illiquid investments, and high-risk trading strategies created vulnerabilities that became apparent when market conditions deteriorated and user withdrawal demand increased. Celsius’s inability to meet withdrawal requests revealed that the platform had been operating with insufficient liquidity reserves and had made investments that could not be easily liquidated to meet user demands.

BlockFi’s collapse followed a different trajectory but ultimately resulted in similar outcomes for users, with the platform filing for bankruptcy in November 2022 after experiencing significant losses from exposure to FTX and Alameda Research as well as other market participants who failed during the broader cryptocurrency market crisis. The platform’s institutional backing and regulatory engagement were insufficient to prevent collapse when counterparty risks materialized and market conditions deteriorated.

The bankruptcy proceedings for both platforms revealed significant details about their operations, risk management practices, and financial conditions that had not been transparent to users during the platforms’ operational periods. These revelations highlighted the importance of transparency, regulatory oversight, and independent auditing in cryptocurrency financial services while demonstrating the risks associated with centralized custody models.

Recovery prospects for users of both platforms remain uncertain, with bankruptcy proceedings ongoing and recovery amounts likely to be significantly less than the full value of user deposits. The legal and financial complexities associated with cryptocurrency bankruptcy proceedings have created additional challenges for users seeking to recover their funds while highlighting the importance of regulatory frameworks that provide appropriate protections for cryptocurrency financial services users.

Nexo’s Survival and Adaptation Strategy

Unlike its major competitors, Nexo managed to survive the 2022 cryptocurrency market crisis and platform collapses, though not without significant challenges and adaptations that fundamentally changed the platform’s operations and risk profile. The platform’s survival provides important insights into the factors that contributed to stability during market stress while highlighting the ongoing challenges facing centralized cryptocurrency lending platforms.

Nexo’s approach to managing the crisis included reducing risk exposure, increasing transparency, enhancing compliance procedures, and adapting product offerings to reflect changed market conditions and regulatory requirements. The platform implemented various measures designed to reassure users about the safety of their funds while demonstrating financial stability and operational continuity during a period of significant industry turbulence.

The platform’s regulatory compliance efforts, which had been a differentiating factor throughout its operation, became even more important during the crisis as users and regulators demanded greater transparency and accountability from cryptocurrency financial services providers. Nexo’s proactive engagement with regulators and emphasis on compliance provided advantages over competitors who had been less focused on regulatory requirements.

However, Nexo’s survival came at the cost of reduced yields, more conservative lending practices, and increased operational complexity as the platform adapted to changed market conditions and regulatory requirements. The platform’s users experienced lower returns compared to the pre-crisis period, reflecting the more challenging environment for cryptocurrency lending and the platform’s focus on stability over aggressive growth.

The lessons learned from Nexo’s survival strategy include the importance of conservative risk management, regulatory compliance, diversification, and transparency in building sustainable cryptocurrency financial services businesses. These factors proved crucial during market stress events and provide a template for other platforms seeking to build resilient operations in the evolving cryptocurrency financial services landscape.

Advanced portfolio analysis tools on TradingView can help investors evaluate the risk-adjusted returns and volatility characteristics of different cryptocurrency lending strategies, providing valuable insights for making informed decisions about centralized lending platform participation.

Regulatory Response and Industry Evolution

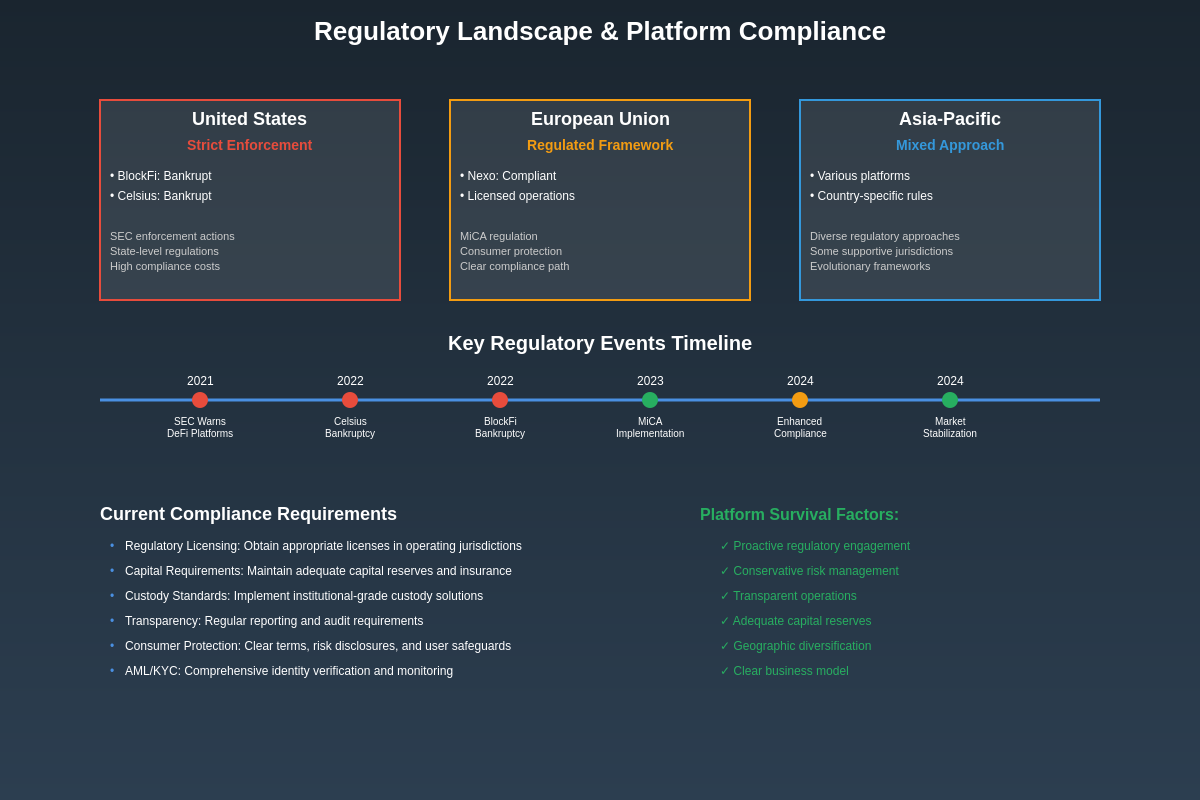

The collapse of major centralized cryptocurrency lending platforms prompted significant regulatory responses across multiple jurisdictions, with authorities implementing new requirements, enforcement actions, and guidance designed to address the risks highlighted by platform failures while providing greater protection for users of cryptocurrency financial services. These regulatory developments have fundamentally reshaped the industry landscape and created new compliance requirements for surviving and new platforms.

In the United States, regulatory authorities including the SEC, CFTC, and state regulators increased scrutiny of cryptocurrency lending platforms, implementing enforcement actions against various platforms while developing new guidance and requirements for cryptocurrency financial services providers. These regulatory actions have created greater clarity about compliance requirements while also increasing operational costs and complexity for platforms operating in U.S. markets.

European regulators, building on existing frameworks including the Markets in Crypto-Assets (MiCA) regulation, have implemented additional requirements for cryptocurrency financial services providers while emphasizing consumer protection, operational resilience, and financial stability. These regulatory developments have created both opportunities and challenges for platforms operating in European markets, with compliant platforms potentially benefiting from regulatory clarity while non-compliant platforms facing enforcement actions.

The global nature of cryptocurrency markets has created challenges for regulatory coordination, with different jurisdictions implementing different approaches to cryptocurrency lending platform oversight while attempting to address cross-border regulatory arbitrage and ensure appropriate user protections. This regulatory fragmentation has created compliance challenges for platforms serving global markets while highlighting the need for international coordination on cryptocurrency financial services regulation.

Industry evolution following the regulatory response has included consolidation of surviving platforms, increased focus on compliance and risk management, development of new business models that address regulatory requirements, and greater emphasis on transparency and user protection. These changes have created a more mature but also more complex operating environment for cryptocurrency lending platforms.

The long-term implications of regulatory responses include higher barriers to entry for new platforms, increased operational costs for existing platforms, greater user protections, and potentially reduced competition in some markets. These factors will likely influence the development of cryptocurrency financial services markets and the innovation potential within the sector.

Current Market Landscape and Alternatives

The centralized cryptocurrency lending landscape has been fundamentally transformed by the events of 2022, with surviving platforms operating under more stringent regulatory requirements and risk management practices while new entrants face higher barriers to entry and more complex compliance requirements. Understanding the current market structure provides important context for evaluating alternatives and making informed decisions about cryptocurrency financial services participation.

The reduction in the number of major centralized lending platforms has created opportunities for surviving platforms to gain market share while also highlighting the importance of platform selection criteria including financial stability, regulatory compliance, transparency, and risk management practices. Users now have fewer options but potentially greater clarity about the relative strengths and weaknesses of available platforms.

Alternative approaches to cryptocurrency yield generation have gained prominence following the centralized platform collapses, including decentralized finance (DeFi) protocols, staking services, and self-custody solutions that provide users with greater control over their assets while requiring additional technical knowledge and active risk management. These alternatives offer different risk-return profiles and operational requirements compared to centralized platforms.

Traditional financial institutions have also increased their cryptocurrency service offerings, providing regulated alternatives to specialized cryptocurrency platforms while leveraging existing compliance infrastructure and customer relationships. These institutional offerings typically provide lower yields but potentially greater regulatory protection and operational stability compared to specialized cryptocurrency platforms.

The market for cryptocurrency financial services continues to evolve rapidly, with new business models, regulatory frameworks, and technology solutions creating opportunities for innovation while addressing the risks highlighted by platform failures. This evolution includes development of hybrid custody models, enhanced transparency mechanisms, and improved risk management practices that attempt to address user concerns while maintaining operational efficiency.

Investment strategies for cryptocurrency holders now must account for the changed risk landscape, with greater emphasis on diversification, due diligence, and risk assessment when evaluating yield-generating opportunities. The concentration risk associated with centralized platforms has become more apparent, leading many users to diversify across multiple platforms and alternative approaches to reduce exposure to any single point of failure.

Future Outlook and Lessons Learned

The future of centralized cryptocurrency lending will likely be shaped by regulatory developments, technological innovations, and the lessons learned from the platform failures of 2022, with successful platforms needing to balance user demand for attractive yields with sustainable risk management practices and regulatory compliance requirements. The industry’s maturation process will likely continue to favor platforms with strong operational practices, regulatory compliance, and transparent risk management over those prioritizing rapid growth and aggressive yield strategies.

Key lessons from the centralized lending platform failures include the importance of transparency in risk management practices, the dangers of asset-liability mismatches, the risks associated with counterparty concentration, and the need for adequate liquidity reserves to meet user withdrawal demands during stress events. These lessons have influenced the development of new platforms and the operational changes implemented by surviving platforms.

The role of regulatory oversight in preventing future failures and protecting users has become more apparent, with appropriate regulatory frameworks potentially providing benefits for both platforms and users by establishing clear operational requirements, transparency standards, and user protection mechanisms. However, the development of effective regulatory frameworks remains challenging given the technical complexity of cryptocurrency financial services and the global nature of the markets.

Technological developments including improved custody solutions, enhanced transparency mechanisms, and better risk management tools may help address some of the challenges that contributed to platform failures while creating new opportunities for innovation in cryptocurrency financial services. These technological solutions could potentially reduce operational risks while improving user experience and regulatory compliance.

The evolution toward more sustainable business models in cryptocurrency financial services will likely continue, with successful platforms focusing on long-term viability rather than unsustainable growth strategies. This evolution may result in lower but more stable yields for users while providing greater operational security and regulatory compliance.

User education and awareness about the risks associated with cryptocurrency financial services have increased significantly following the platform failures, with users now more likely to evaluate platforms based on risk management practices, regulatory compliance, and financial stability rather than simply seeking the highest yields available. This increased sophistication among users may contribute to better outcomes and more sustainable platform operations in the future.

Investment Implications and Risk Assessment

The transformation of the centralized cryptocurrency lending landscape has significant implications for investors seeking to generate yield on cryptocurrency holdings, with traditional risk-return calculations now requiring greater emphasis on operational risk, regulatory risk, and platform sustainability in addition to market risk and yield potential. Investment decisions in this space now require more sophisticated due diligence and risk assessment practices.

Portfolio construction strategies for cryptocurrency holders must now account for the concentration risks associated with centralized platforms, potentially favoring diversification across multiple platforms, alternative yield generation methods, and self-custody solutions that reduce dependence on any single service provider. The optimal allocation strategy will depend on individual risk tolerance, technical expertise, and investment objectives.

Due diligence processes for evaluating centralized lending platforms should now include assessment of regulatory compliance status, financial stability indicators, risk management practices, transparency levels, and operational track record rather than focusing primarily on yield offerings. This enhanced due diligence may help investors avoid platforms with unsustainable business models or inadequate risk controls.

Risk management strategies for cryptocurrency lending participation should include position sizing appropriate to the investor’s overall portfolio, diversification across multiple platforms and approaches, regular monitoring of platform health and market conditions, and contingency planning for platform failures or market stress events. These strategies may help mitigate some of the risks associated with centralized platform participation while maintaining access to yield generation opportunities.

The integration of traditional finance and cryptocurrency markets continues to create new opportunities and risks for investors, with institutional adoption potentially providing new sources of yield while also introducing additional complexity and regulatory requirements. Understanding these developments and their implications for cryptocurrency financial services will be important for making informed investment decisions.

Long-term investment strategies in the cryptocurrency space may need to adapt to the changed landscape by incorporating lessons learned from platform failures while maintaining appropriate exposure to the innovation and growth potential of the sector. This balanced approach may help investors participate in the cryptocurrency market’s development while managing the risks associated with emerging financial services platforms.

Disclaimer

This article is for informational and educational purposes only and should not be construed as financial advice, investment recommendations, or professional guidance regarding cryptocurrency lending platforms, financial services, or investment strategies. The cryptocurrency and digital asset markets are highly volatile, speculative, and subject to significant risks including total loss of principal.

The centralized cryptocurrency lending platforms discussed in this article, including Nexo, BlockFi, and Celsius, carry substantial risks including platform failure, regulatory changes, market volatility, counterparty risk, and potential total loss of deposited funds. Past performance of these platforms does not guarantee future results, and the failure of major platforms like Celsius and BlockFi demonstrates that even well-established platforms can experience catastrophic failures resulting in user losses.

Cryptocurrency lending and yield generation strategies involve complex risks that may not be suitable for all investors, including but not limited to credit risk, market risk, operational risk, regulatory risk, and liquidity risk. Users should conduct thorough due diligence, understand the terms and risks associated with any platform or service, and consider consulting with qualified financial advisors before making investment decisions.

The regulatory landscape for cryptocurrency financial services is rapidly evolving and varies significantly across jurisdictions, with potential changes in regulations, enforcement actions, and legal requirements that could materially affect platform operations and user rights. Users should stay informed about regulatory developments in their jurisdictions and understand their legal protections and recourse options.

The authors and publishers of this content do not provide personalized investment advice and are not responsible for any financial losses, damages, or adverse consequences that may result from the use of this information. All investment decisions should be made based on individual circumstances, risk tolerance, and financial objectives after careful consideration of the risks involved.