The Nexo Interest Rate Phenomenon

Nexo has emerged as one of the most prominent centralized finance platforms in the cryptocurrency space, attracting millions of users with its competitive interest rates on cryptocurrency deposits that often exceed traditional banking yields by significant margins. The platform’s promise of earning up to 12% annual percentage yield on various cryptocurrency holdings has positioned it as a major player in the rapidly expanding crypto lending market, but questions about the sustainability of these attractive rates have become increasingly relevant as market conditions evolve and regulatory scrutiny intensifies.

The company’s business model relies on generating revenue through cryptocurrency lending, trading, and various financial services while passing a portion of these returns to depositors in the form of interest payments. This approach has allowed Nexo to offer yields that are particularly attractive when compared to traditional banking products, especially in the current low interest rate environment where traditional savings accounts often provide less than 1% annual returns.

Understanding the mechanics behind Nexo’s interest rate structure requires examining the broader cryptocurrency lending ecosystem, the platform’s revenue generation strategies, the risks associated with centralized cryptocurrency lending, and the various factors that could impact the long-term sustainability of current yield levels. The analysis becomes particularly important as investors seek to evaluate whether Nexo’s interest rates represent a sustainable value proposition or a temporary market anomaly that could change as conditions evolve.

Historical Context and Market Evolution

The cryptocurrency lending market has experienced tremendous growth over the past several years, with platforms like Nexo capitalizing on the increasing demand for yield generation in an environment where traditional fixed-income investments have offered historically low returns. The emergence of centralized cryptocurrency lending platforms represented a significant evolution from early peer-to-peer lending models, providing users with more streamlined interfaces and supposedly more secure custody solutions.

Nexo’s founding in 2017 coincided with the broader institutionalization of the cryptocurrency market, as the company sought to bridge traditional financial services with emerging cryptocurrency opportunities. The platform’s initial focus on cryptocurrency-backed loans has since expanded to include interest-bearing accounts, trading services, and various other financial products designed to serve both retail and institutional cryptocurrency users.

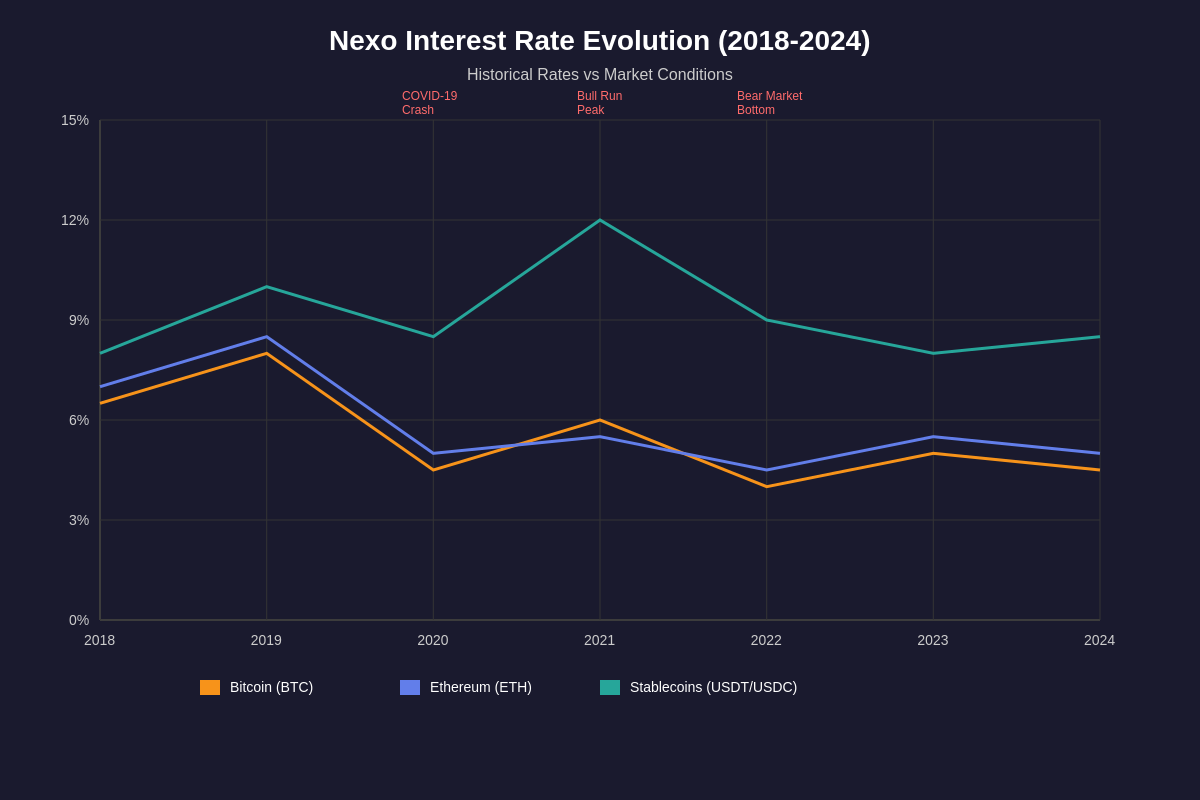

The historical performance of Nexo’s interest rates reveals significant variation based on market conditions, cryptocurrency prices, and competitive pressures within the lending space. During periods of high cryptocurrency volatility and strong market demand, the platform has been able to maintain relatively high interest rates, while market downturns have occasionally necessitated rate adjustments to ensure operational sustainability.

The competitive landscape for cryptocurrency lending has intensified significantly since Nexo’s launch, with numerous platforms offering similar services and competing primarily on interest rates, security features, and user experience. This competition has created both opportunities and challenges for platforms like Nexo, as they must balance attractive rates with operational sustainability while managing various risks associated with cryptocurrency lending operations.

Market evolution has also been influenced by regulatory developments in various jurisdictions, with increasing scrutiny of cryptocurrency lending platforms creating uncertainty about future operating conditions and potentially affecting the sustainability of current business models. The regulatory environment continues to evolve rapidly, with different jurisdictions taking varying approaches to cryptocurrency lending platform oversight and consumer protection requirements.

Nexo’s Business Model and Revenue Sources

Monitor Nexo Token Performance

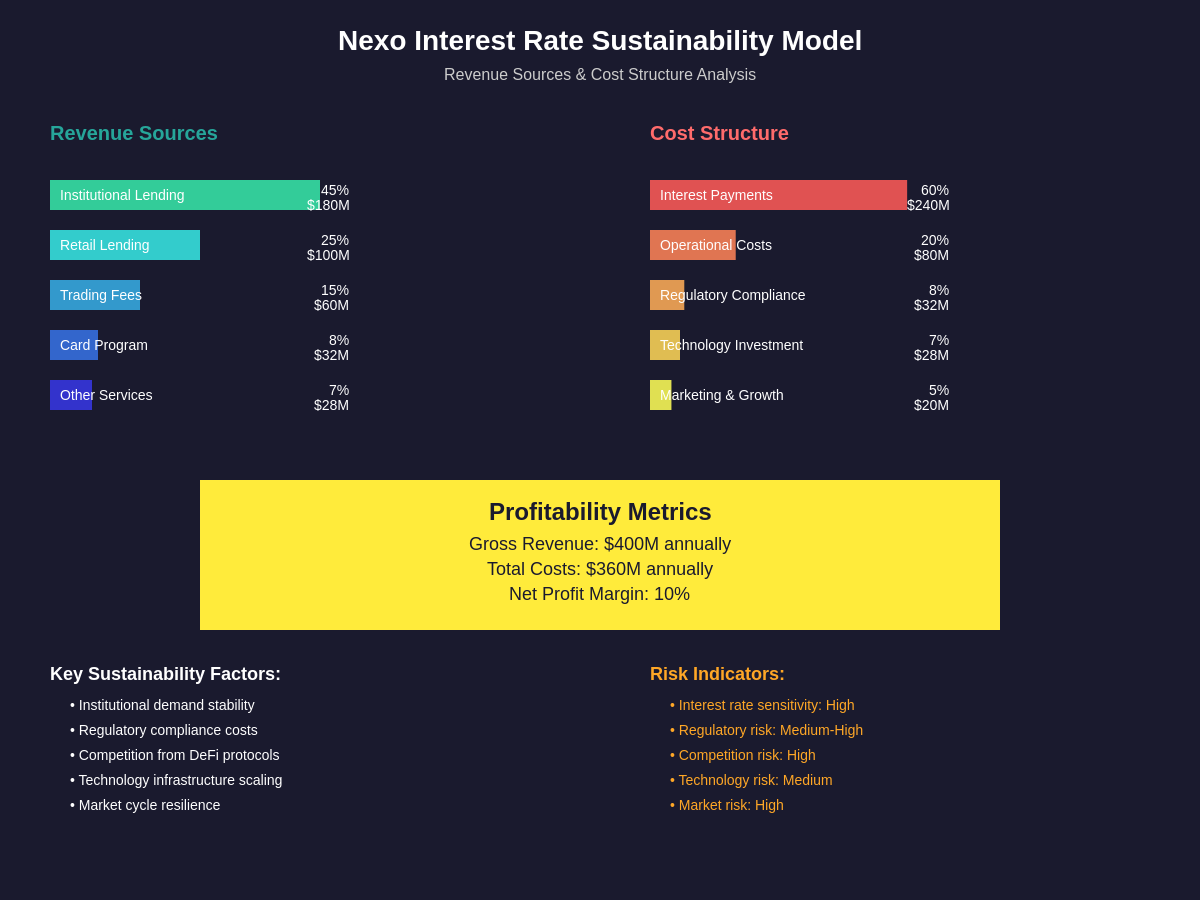

The foundation of Nexo’s ability to offer competitive interest rates lies in its diversified revenue generation model, which encompasses several key areas including institutional lending, retail lending, trading fees, and various financial services. The platform generates revenue by lending user deposits to institutional borrowers at rates higher than those paid to depositors, capturing the spread as profit while managing the associated risks.

Institutional lending represents a major component of Nexo’s revenue model, with the platform serving hedge funds, trading firms, and other institutional clients who require access to cryptocurrency liquidity for various purposes including arbitrage, market making, and proprietary trading strategies. These institutional borrowers are typically willing to pay premium rates for reliable access to cryptocurrency liquidity, especially during periods of high market volatility when traditional funding sources may be less available.

Retail lending services, including cryptocurrency-backed loans and credit lines, provide another significant revenue stream for the platform. Individual users can borrow against their cryptocurrency holdings at competitive rates, while Nexo earns interest on these loans that typically exceeds the rates paid to depositors. The collateralized nature of these loans helps manage credit risk, though cryptocurrency volatility can create challenges in maintaining appropriate loan-to-value ratios.

Trading and exchange services generate additional revenue through fees charged on various trading activities, including spot trading, derivatives, and various advanced trading features. The platform’s integrated approach allows users to seamlessly move between different services, potentially increasing overall revenue per user while providing a more comprehensive financial services experience.

The Nexo token ecosystem plays an important role in the platform’s business model, with token holders receiving various benefits including higher interest rates, reduced loan rates, and fee discounts. This token-centric approach helps create user loyalty while potentially reducing the platform’s operational costs through various incentive mechanisms. However, the token’s price volatility can impact the effectiveness of these incentives and the overall economics of the business model.

Revenue diversification extends to various other services including card programs, advanced trading features, and institutional custody solutions. This diversified approach helps reduce dependence on any single revenue source while providing multiple avenues for growth, though it also increases operational complexity and regulatory requirements across different jurisdictions.

Interest Rate Structure and Tier System

Nexo’s interest rate structure employs a sophisticated tiering system that takes into account multiple factors including the type of cryptocurrency deposited, the user’s loyalty tier based on Nexo token holdings, the amount deposited, and the chosen interest payment method. This complex structure is designed to optimize user engagement while managing the platform’s cost structure and risk exposure across different types of assets and user segments.

The base interest rates vary significantly across different cryptocurrencies, with established assets like Bitcoin and Ethereum typically offering lower rates compared to smaller altcoins or stablecoins. This differentiation reflects the varying levels of demand for different cryptocurrencies in lending markets, as well as the different risk profiles associated with each asset. Stablecoins often command higher interest rates due to their lower volatility and high demand from institutional borrowers.

The loyalty tier system creates significant rate differentials based on users’ Nexo token holdings, with higher-tier users receiving substantially better rates on their deposits. This system incentivizes users to hold Nexo tokens while providing the platform with a mechanism to reward its most committed users. However, the requirement to hold a volatile token to maximize yields introduces additional risk considerations for users seeking stable returns.

Flexible versus fixed-term deposits offer different rate structures, with longer-term commitments typically providing higher yields in exchange for reduced liquidity. This structure helps Nexo manage its own liquidity requirements while providing users with options that match their risk tolerance and liquidity needs. The platform’s ability to offer higher rates on fixed-term deposits depends on its confidence in being able to profitably deploy these funds over the commitment period.

Geographic restrictions and regulatory requirements have led to different rate structures in various jurisdictions, with some locations receiving different terms based on local regulatory compliance requirements. These geographical differences can create complexity for users and may impact the platform’s ability to maintain consistent global rates as regulatory environments continue to evolve.

The dynamic nature of Nexo’s interest rate structure means that rates can change based on market conditions, demand for specific cryptocurrencies, and the platform’s own operational requirements. While this flexibility allows the platform to respond to changing market conditions, it also creates uncertainty for users who may see their returns fluctuate over time without direct control over these changes.

Risk Assessment and Sustainability Factors

The sustainability of Nexo’s interest rates depends on a complex interplay of factors including market demand for cryptocurrency loans, the platform’s operational efficiency, regulatory compliance costs, and the broader competitive landscape within the cryptocurrency lending sector. Understanding these factors is crucial for evaluating whether current rate levels represent a sustainable long-term proposition or a temporary market condition.

Market demand for cryptocurrency lending fluctuates based on numerous factors including overall market sentiment, arbitrage opportunities, institutional adoption, and the availability of alternative funding sources. During periods of high market volatility and strong institutional interest, demand for cryptocurrency loans typically increases, supporting higher interest rates. Conversely, market downturns or reduced institutional activity can pressure rates downward as demand decreases.

Operational risk factors include the platform’s ability to effectively manage credit risk, maintain adequate liquidity, and operate efficiently at scale. Nexo’s centralized model creates concentration risks that could impact sustainability if the platform experiences operational difficulties, security breaches, or significant loan defaults. The platform’s risk management systems and operational procedures play a crucial role in maintaining the stability required to support consistent interest payments.

Regulatory risk represents one of the most significant factors affecting long-term sustainability, as changing regulatory requirements could impact the platform’s operating model, increase compliance costs, or restrict certain types of activities. The evolving regulatory landscape in key jurisdictions could force changes to the business model that might affect the ability to maintain current interest rate levels.

Competitive pressure from other cryptocurrency lending platforms, traditional financial institutions entering the cryptocurrency space, and decentralized finance protocols offering similar services could impact Nexo’s ability to maintain its current market position and pricing power. Increased competition typically puts downward pressure on interest rates as platforms compete for market share.

Technology risk factors include the platform’s dependence on various blockchain networks, smart contracts, and third-party services that could experience technical difficulties or security vulnerabilities. While Nexo operates as a centralized platform, it still depends on decentralized blockchain infrastructure and various technological systems that could impact operations and sustainability.

Cryptocurrency market volatility affects sustainability through multiple channels including the value of collateral backing loans, the demand for different types of cryptocurrency services, and the overall health of the cryptocurrency ecosystem. Extreme market movements could create liquidity challenges or credit losses that might impact the platform’s ability to maintain current interest rate levels.

Comparative Analysis with Traditional and DeFi Alternatives

Nexo’s interest rates must be evaluated within the broader context of alternative investment options available to cryptocurrency holders, including traditional financial products, decentralized finance protocols, and other centralized cryptocurrency lending platforms. This comparative analysis reveals important insights about the value proposition and sustainability of Nexo’s offerings relative to available alternatives.

Traditional banking products typically offer significantly lower interest rates on deposits, with most savings accounts and certificates of deposit providing annual yields well below Nexo’s cryptocurrency interest rates. However, traditional products offer different risk profiles including government deposit insurance, regulatory oversight, and currency stability that may be attractive to certain investors despite lower returns.

Decentralized finance protocols often provide competitive or higher yields compared to centralized platforms like Nexo, but with different risk characteristics including smart contract risk, liquidity risk, and the technical complexity required to participate effectively. DeFi yields can be highly volatile and may require active management to optimize returns, while also exposing users to various technical and economic risks that may not be immediately apparent.

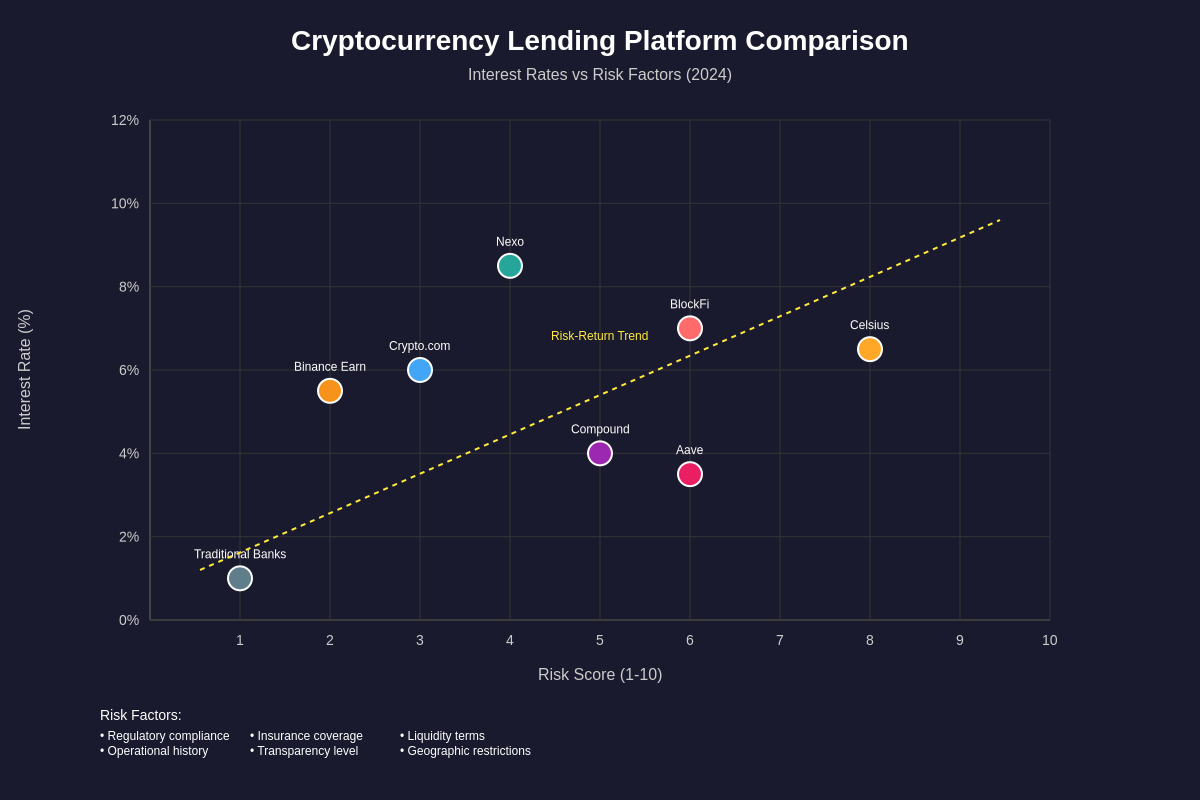

Other centralized cryptocurrency lending platforms offer varying rate structures and terms that compete directly with Nexo’s offerings. Platforms like Celsius, BlockFi, and others have experienced different trajectories in terms of rate sustainability, regulatory compliance, and operational stability, providing important case studies for evaluating the broader sustainability of the centralized lending model.

The risk-adjusted return comparison becomes particularly important when considering factors such as counterparty risk, regulatory protection, liquidity terms, and operational transparency. While Nexo may offer attractive nominal returns, users must consider whether these returns adequately compensate for the various risks associated with centralized cryptocurrency lending compared to alternatives.

Yield farming opportunities in decentralized finance often provide higher potential returns but with significantly higher complexity, risk, and time requirements. These alternatives may appeal to more sophisticated users while highlighting the value proposition that platforms like Nexo provide in terms of simplified access to cryptocurrency yields.

The evolution of interest rates across different platforms and protocols provides insights into market trends and sustainability factors that affect the entire cryptocurrency lending ecosystem. Historical data shows that rates have generally declined from the early days of cryptocurrency lending as markets have matured and competition has increased.

Regulatory Environment and Compliance Challenges

Track Regulatory Impact on Crypto

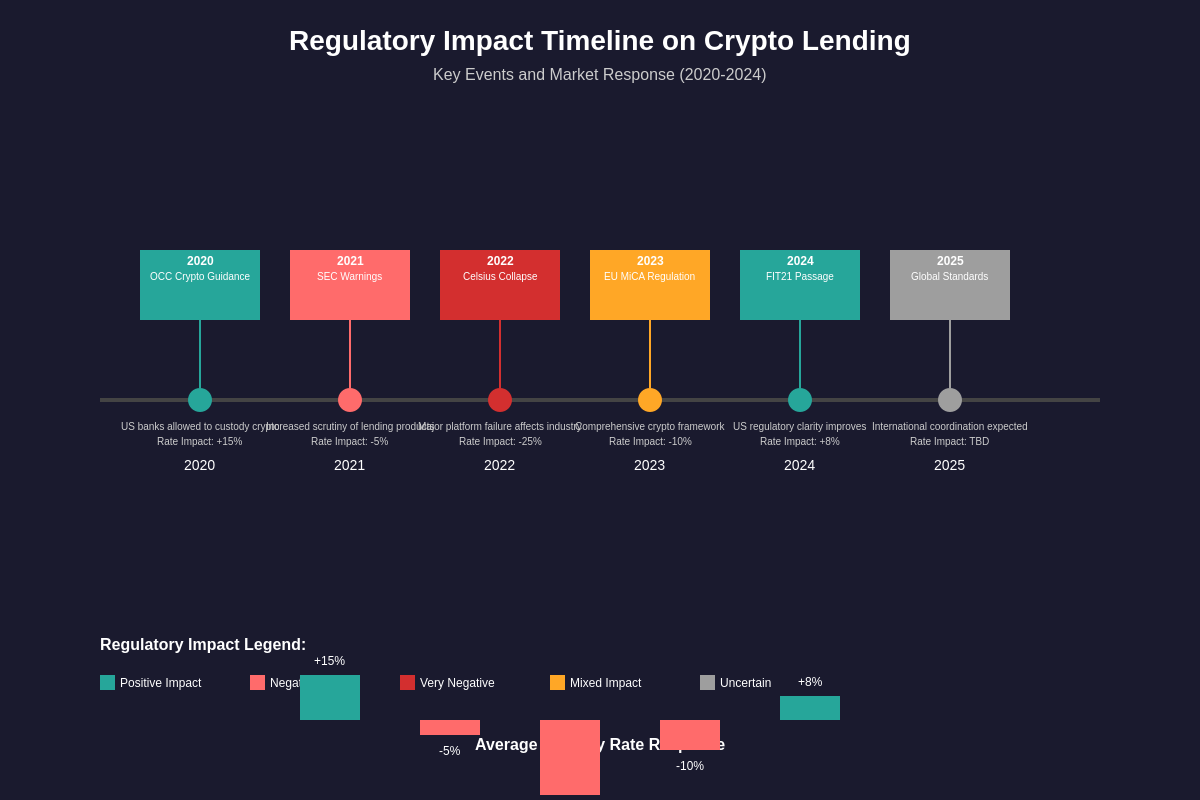

The regulatory landscape surrounding cryptocurrency lending platforms like Nexo continues to evolve rapidly across different jurisdictions, creating both challenges and opportunities that directly impact the sustainability of current interest rate levels. Understanding these regulatory dynamics is essential for evaluating the long-term viability of Nexo’s business model and its ability to maintain competitive yields.

Securities regulations represent one of the most significant challenges facing cryptocurrency lending platforms, as regulators in various jurisdictions have raised questions about whether interest-bearing cryptocurrency accounts should be classified as securities offerings subject to registration and disclosure requirements. The outcome of these regulatory determinations could significantly impact operating costs and business model flexibility.

Consumer protection regulations are becoming increasingly relevant as cryptocurrency lending platforms serve growing numbers of retail users who may not fully understand the risks associated with these products. Regulatory requirements for disclosure, risk warnings, and consumer protections could increase operational costs and potentially impact the economics of offering high interest rates to retail customers.

Anti-money laundering and know-your-customer requirements continue to evolve, with increasing emphasis on transaction monitoring, source of funds verification, and reporting obligations. Compliance with these requirements creates ongoing operational costs that must be factored into the sustainability of current rate structures, particularly as requirements become more stringent over time.

Banking regulations in various jurisdictions may impact cryptocurrency lending platforms as they increasingly compete with traditional banking products or seek to offer services that resemble traditional banking. The potential classification of certain cryptocurrency lending activities as banking services could subject platforms like Nexo to significantly more extensive regulatory oversight and capital requirements.

Tax implications and reporting requirements vary significantly across jurisdictions, creating compliance complexity for both platforms and users. Changes in tax treatment of cryptocurrency lending activities could impact user demand and the overall economics of the lending model, particularly if tax obligations reduce the after-tax returns available to users.

International coordination of cryptocurrency regulations continues to develop through various forums and organizations, potentially leading to more harmonized global standards that could affect how platforms like Nexo operate across multiple jurisdictions. While harmonization could reduce compliance complexity, it could also lead to more restrictive requirements if regulations converge toward the most stringent standards.

The regulatory response to high-profile failures in the cryptocurrency lending space has created increased scrutiny of business models and risk management practices across the industry. This heightened regulatory attention could lead to more prescriptive requirements regarding capital adequacy, risk management, and operational procedures that might impact profitability and sustainability.

Technology Infrastructure and Operational Considerations

The technological foundation underlying Nexo’s operations plays a crucial role in determining the sustainability of its interest rate offerings, as operational efficiency, security, and scalability directly impact the platform’s ability to generate revenue and manage costs effectively. Understanding these technological factors provides insights into the long-term viability of current rate structures.

Custody technology represents a fundamental component of Nexo’s operational infrastructure, requiring sophisticated solutions for securely storing user funds while maintaining the operational flexibility needed to generate returns through lending activities. The costs associated with implementing and maintaining institutional-grade custody solutions represent a significant operational expense that must be factored into rate sustainability calculations.

Smart contract integration and blockchain infrastructure costs continue to evolve as the platform interacts with various blockchain networks and decentralized protocols. Gas fees, network congestion, and the complexity of managing multi-chain operations create variable costs that can impact profitability and the ability to maintain consistent interest payments across different market conditions.

Risk management systems require ongoing investment in technology and personnel to effectively monitor credit risk, market risk, and operational risk across the platform’s various activities. The sophistication required for these systems increases as the platform scales and regulatory requirements become more complex, creating ongoing technology costs that affect overall profitability.

User interface and experience technology investments are necessary to remain competitive in an increasingly crowded market while also meeting evolving regulatory requirements for disclosure and user protection. The costs associated with maintaining and improving user-facing technology must be balanced against the need to maintain attractive interest rates.

Data security and compliance technology requirements continue to expand as regulatory expectations increase and cyber threats evolve. Investment in security infrastructure, monitoring systems, and compliance tools represents ongoing operational costs that impact the economics of the lending model and the sustainability of current rate offerings.

Scalability considerations become increasingly important as the platform grows, requiring technology investments that can support larger transaction volumes, more complex product offerings, and expanded geographic operations. The ability to achieve operational leverage through technology investments affects the platform’s long-term ability to maintain competitive rates while growing its business.

Third-party service dependencies create both opportunities and risks for operational efficiency and cost management. While outsourcing certain functions can reduce costs and improve efficiency, dependence on third-party providers also creates risks that could impact operations and the ability to maintain consistent service levels required for sustainable rate offerings.

Market Competition and Industry Trends

The competitive landscape for cryptocurrency lending continues to evolve rapidly, with new entrants, changing business models, and shifting user preferences creating both challenges and opportunities for established platforms like Nexo. Understanding these competitive dynamics is essential for evaluating the sustainability of current interest rate levels and the platform’s long-term market position.

Traditional financial institutions have begun entering the cryptocurrency space through various channels including custody services, trading platforms, and lending products. While these institutions typically offer lower yields, they bring significant advantages in terms of regulatory compliance, brand recognition, and integration with traditional financial services that could impact demand for specialized cryptocurrency lending platforms.

Decentralized finance protocols continue to innovate with new yield generation mechanisms, automated market makers, and governance tokens that can provide alternative sources of returns for cryptocurrency holders. The rapid pace of DeFi innovation creates ongoing competitive pressure as users have increasingly sophisticated alternatives for generating yields on their cryptocurrency holdings.

Emerging business models in the cryptocurrency lending space include hybrid approaches that combine centralized and decentralized elements, institutional-focused platforms that serve only qualified investors, and specialized platforms that focus on specific types of cryptocurrency assets or services. These new approaches could fragment the market and impact the pricing power of existing platforms.

Geographic expansion opportunities and challenges affect competitive positioning as platforms seek to serve users in new jurisdictions while complying with varying regulatory requirements. The ability to effectively expand internationally while maintaining operational efficiency and regulatory compliance could provide competitive advantages for some platforms while creating challenges for others.

Product innovation and feature differentiation have become increasingly important competitive factors as basic cryptocurrency lending becomes commoditized. Platforms that can successfully innovate with new products, features, or service models may be able to maintain premium pricing and sustainable rate structures even in an increasingly competitive environment.

Partnership strategies with other cryptocurrency companies, traditional financial institutions, and technology providers can create competitive advantages through expanded distribution, enhanced services, or operational efficiencies. The effectiveness of these partnerships in creating sustainable competitive moats affects long-term rate sustainability and market positioning.

Market consolidation trends may impact the competitive landscape as smaller platforms face pressure from regulatory compliance costs, operational challenges, or competitive pressures. Consolidation could benefit surviving platforms through reduced competition, but it could also attract additional regulatory scrutiny or create opportunities for new entrants.

User acquisition and retention costs continue to increase as competition intensifies and marketing channels become more expensive. The relationship between customer acquisition costs and long-term customer value affects the economics of maintaining high interest rates as customer acquisition tools versus sustainable business practices.

Economic Factors and Market Cycles

The broader economic environment and cryptocurrency market cycles play crucial roles in determining the sustainability of Nexo’s interest rate offerings, as these factors directly impact demand for cryptocurrency lending services, the cost of capital, and the overall health of the cryptocurrency ecosystem. Understanding these economic dynamics provides important context for evaluating long-term rate sustainability.

Macroeconomic factors including central bank monetary policy, inflation expectations, and traditional interest rates create the backdrop against which cryptocurrency lending rates are evaluated. Changes in traditional interest rates can affect the relative attractiveness of cryptocurrency yields while also impacting the cost of capital for cryptocurrency lending platforms.

Cryptocurrency market cycles have historically shown significant impact on lending demand and rate sustainability, with bull markets typically supporting higher rates through increased speculation, arbitrage opportunities, and institutional activity. Conversely, bear markets often lead to reduced demand for cryptocurrency loans and pressure on lending rates across the industry.

Institutional adoption trends affect lending demand through multiple channels including increased trading activity, hedging requirements, and the development of more sophisticated cryptocurrency investment strategies. The pace and scale of institutional adoption directly impacts the sustainability of premium rates charged to institutional borrowers.

Correlation between cryptocurrency and traditional asset markets has implications for diversification benefits and institutional demand for cryptocurrency lending services. As correlations increase, some of the diversification benefits of cryptocurrency investments may diminish, potentially affecting institutional demand for cryptocurrency lending services.

Global economic uncertainty and currency debasement concerns can drive demand for cryptocurrency assets and related services, potentially supporting higher lending rates. However, economic uncertainty can also lead to increased risk aversion and regulatory scrutiny that might negatively impact the cryptocurrency lending market.

Credit conditions in traditional markets affect the availability of alternative funding sources for institutional borrowers who might otherwise use cryptocurrency lending services. Tight credit conditions in traditional markets could increase demand for cryptocurrency lending, while loose credit conditions might reduce this demand.

Inflation dynamics and real interest rate considerations become important factors as users evaluate the attractiveness of cryptocurrency yields compared to alternatives. High inflation environments might make nominal cryptocurrency yields less attractive on a real basis, while deflationary environments could enhance their appeal.

Market liquidity conditions across different cryptocurrency markets affect the ability of lending platforms to deploy capital effectively and generate the returns necessary to support attractive interest rates. Reduced liquidity in cryptocurrency markets could impact both the demand for loans and the ability to manage risk effectively.

User Demographics and Behavioral Analysis

Understanding the user base that drives demand for Nexo’s interest-bearing products provides important insights into the sustainability of current rate structures and the potential for future growth or contraction. User behavior patterns, demographic characteristics, and evolving preferences all influence the platform’s ability to maintain competitive rates while building a sustainable business model.

Retail user segments display varying levels of sophistication, risk tolerance, and yield expectations that affect their sensitivity to interest rate changes and their likelihood of switching between platforms based on rate differentials. Understanding these behavioral patterns helps evaluate how rate changes might impact user retention and acquisition costs.

Geographic distribution of users creates different regulatory requirements, competitive pressures, and market dynamics that can affect rate sustainability. Users in different regions may have access to different alternative investment options and may face varying regulatory restrictions that influence their platform choices and rate sensitivity.

Age demographics and generational differences in cryptocurrency adoption and financial behavior affect long-term demand trends for cryptocurrency lending services. Younger users may be more comfortable with cryptocurrency-based financial services but may also be more sensitive to rate differences and more likely to switch platforms frequently.

Wealth distribution among users influences the average account size, the cost-effectiveness of different service levels, and the potential for cross-selling additional services. Understanding user wealth characteristics helps evaluate the sustainability of different rate tiers and service offerings.

Investment experience and sophistication levels among users affect their understanding of risks associated with cryptocurrency lending and their willingness to accept lower rates in exchange for perceived safety or convenience. More sophisticated users may be more sensitive to rate differentials while also being more aware of alternative options.

Platform loyalty and switching behavior patterns provide insights into user retention costs and the competitive advantages needed to maintain market share. High switching rates among users could pressure platforms to maintain unsustainably high rates to prevent customer defection.

Risk perception and tolerance levels among users influence their willingness to use cryptocurrency lending platforms and their sensitivity to changes in platform policies, rate structures, or market conditions. Understanding these risk perceptions helps evaluate the stability of the user base under different scenarios.

Usage patterns including deposit sizes, withdrawal frequency, and engagement with other platform services affect the operational costs and revenue opportunities associated with different user segments. These patterns influence the economics of serving different types of users and the sustainability of rate structures.

Future Outlook and Sustainability Predictions

The long-term sustainability of Nexo’s interest rate structure depends on a complex interplay of technological development, regulatory evolution, market maturation, and competitive dynamics that will continue to evolve over the coming years. Analyzing these trends provides a framework for understanding the potential trajectory of cryptocurrency lending rates and the viability of current business models.

Technology advancements in areas such as automated risk management, blockchain efficiency, and decentralized finance integration could reduce operational costs and improve the efficiency of cryptocurrency lending platforms. These improvements might support sustainable rate structures by reducing the operational overhead required to generate and distribute yields to users.

Regulatory maturation is likely to bring both challenges and opportunities for cryptocurrency lending platforms, with increased compliance costs potentially pressuring rates downward while regulatory clarity could support institutional adoption and demand for lending services. The net impact of regulatory development will depend on the specific requirements implemented and their effect on operational costs versus market demand.

Market maturation trends suggest that cryptocurrency lending rates may converge toward levels that more closely resemble traditional financial markets as competition increases and the market becomes more efficient. This convergence could pressure current rate levels downward but might also support more stable and predictable rate structures.

Institutional adoption growth could provide sustainable demand for cryptocurrency lending services, particularly if institutional users develop more sophisticated hedging and trading strategies that require regular access to cryptocurrency liquidity. However, institutional users may also be more rate-sensitive and could pressure platforms to reduce margins.

Innovation in financial products and services could create new revenue opportunities for platforms like Nexo, potentially supporting rate sustainability through diversified income streams. New products might include more sophisticated lending products, derivatives, or integration with traditional financial services.

Economic cycle considerations suggest that cryptocurrency lending rates will likely continue to experience significant volatility based on broader market conditions, regulatory changes, and technological developments. Platforms that can adapt their rate structures to changing conditions while maintaining operational efficiency may be better positioned for long-term sustainability.

Competitive evolution will likely favor platforms that can effectively balance attractive rates with operational efficiency, regulatory compliance, and risk management. The long-term winners in the cryptocurrency lending space may be those that can build sustainable competitive advantages beyond simply offering the highest rates.

User education and market sophistication improvements could lead to more informed decision-making by cryptocurrency holders, potentially reducing the effectiveness of rate-based competition and favoring platforms that offer superior service, security, and transparency. This evolution could support more sustainable rate structures based on value rather than purely competitive rates.

Global economic trends including monetary policy changes, inflation dynamics, and traditional interest rate movements will continue to influence the relative attractiveness of cryptocurrency lending rates and the sustainability of current structures. Platforms will need to adapt to these changing conditions while maintaining competitive positioning.

The integration of cryptocurrency services with traditional financial systems could create new opportunities for sustainable revenue generation while also introducing new competitive pressures from established financial institutions. The success of this integration will significantly influence the long-term outlook for specialized cryptocurrency lending platforms.

Conclusion and Investment Considerations

The sustainability of Nexo’s interest rates represents a complex equation involving multiple dynamic factors that extend far beyond simple supply and demand mechanics in cryptocurrency lending markets. While the platform has demonstrated resilience and adaptability in navigating various market conditions since its inception, the long-term sustainability of current rate levels faces significant challenges from regulatory evolution, increasing competition, market maturation, and changing user expectations.

Current interest rates offered by Nexo appear to be supported by legitimate demand from institutional borrowers, efficient operational infrastructure, and a diversified revenue model that extends beyond simple lending spreads. However, the sustainability of these rates depends on the platform’s ability to maintain competitive advantages in an increasingly crowded market while adapting to evolving regulatory requirements and changing market conditions.

Investors considering Nexo’s interest-bearing products should carefully evaluate their risk tolerance, diversification objectives, and liquidity requirements while recognizing that past performance may not be indicative of future results. The centralized nature of the platform introduces counterparty risk that should be weighed against the attractive yield potential, particularly given the evolving regulatory landscape and the history of challenges faced by other cryptocurrency lending platforms.

The most prudent approach for potential users involves treating Nexo’s interest rates as one component of a diversified cryptocurrency and overall investment strategy rather than relying solely on these yields for investment returns. Understanding the various risk factors, competitive dynamics, and regulatory considerations discussed throughout this analysis provides the foundation for making informed decisions about participation in cryptocurrency lending platforms.

Long-term sustainability will likely depend on Nexo’s ability to successfully navigate the transition from a high-growth, high-rate environment to a more mature market characterized by increased regulation, competition, and user sophistication. Platforms that can build sustainable competitive advantages through superior technology, compliance capabilities, and customer service may be better positioned to maintain attractive rates even as overall market rates potentially decline.

The cryptocurrency lending market continues to evolve rapidly, and participants should remain informed about changes in platform policies, regulatory requirements, and market conditions that could affect the risk-return profile of their investments. Regular evaluation of alternative options and changing market dynamics will be essential for optimizing returns while managing risks in this dynamic environment.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risks including potential loss of principal. Interest rates on cryptocurrency lending platforms are subject to change and past performance does not guarantee future results. Readers should conduct their own research and consult with qualified financial advisors before making investment decisions. Cryptocurrency lending platforms operate in a rapidly evolving regulatory environment and face various operational risks that could impact returns and capital preservation.