The emergence of non-fungible tokens as collateral for cryptocurrency loans represents a revolutionary convergence of digital art markets and decentralized finance, creating entirely new financial instruments that allow collectors and investors to unlock liquidity from their digital assets without permanently selling them. This innovative lending model has transformed how individuals and institutions approach digital asset ownership while introducing complex challenges related to valuation, liquidation, and risk management that are fundamentally different from traditional collateral-based lending systems.

Understanding NFT Collateralization in DeFi

NFT-backed lending platforms operate on the principle that unique digital assets can serve as effective collateral for loans, similar to how traditional finance uses real estate, vehicles, or other valuable assets to secure credit facilities. However, the unique characteristics of NFTs including their indivisible nature, subjective valuation, and volatile pricing create unprecedented challenges that require innovative technological and financial solutions.

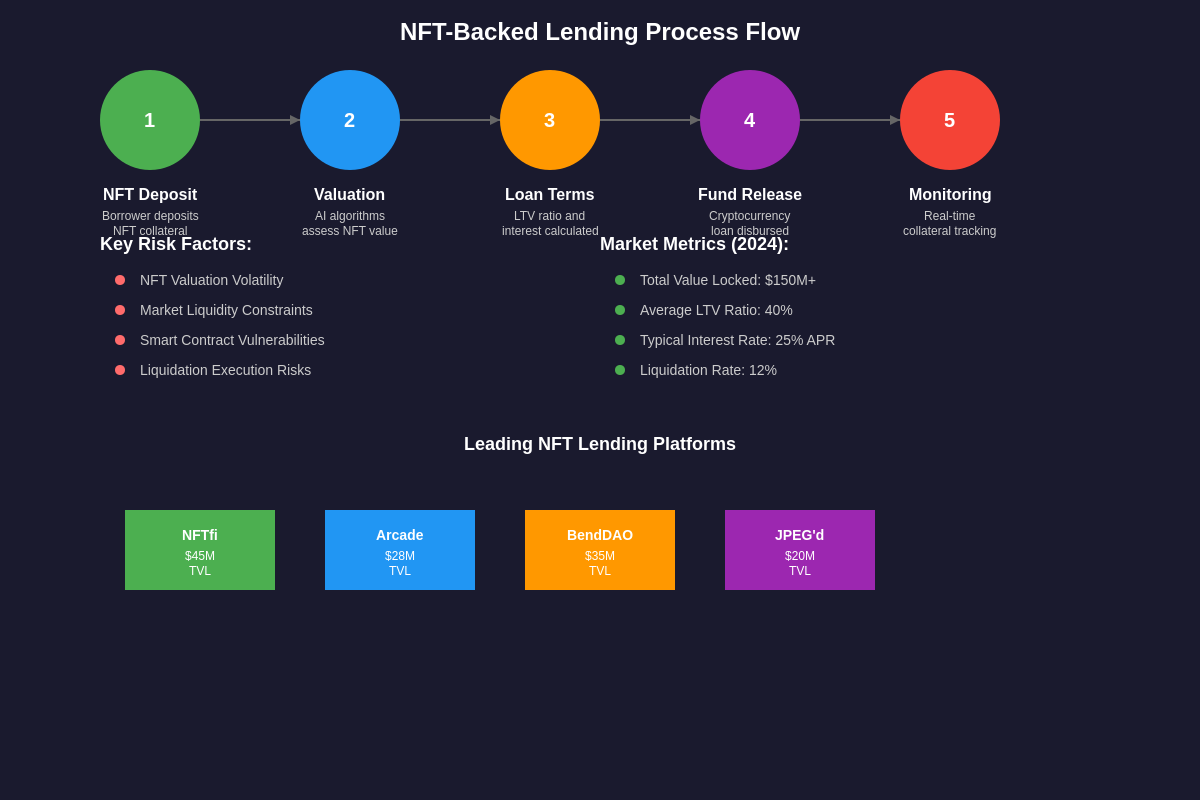

The fundamental mechanics of NFT collateralization involve borrowers depositing their digital assets into smart contracts that temporarily transfer custody to lending platforms while maintaining the borrower’s ultimate ownership rights. These smart contracts automatically enforce loan terms, manage collateral ratios, and execute liquidation procedures when necessary, creating a trustless system that operates without traditional financial intermediaries.

Loan-to-value ratios in NFT lending typically range from 20% to 60% of estimated NFT value, significantly lower than traditional asset-backed loans due to the heightened volatility and liquidity challenges associated with digital collectibles. These conservative ratios provide crucial protection for lenders while still offering meaningful liquidity access for borrowers who need capital without selling their prized digital assets.

The process begins with borrowers selecting qualified NFTs from their collections and submitting them to lending platforms for valuation assessment. Advanced pricing algorithms analyze historical sales data, collection floor prices, rarity metrics, and market trends to determine appropriate loan amounts, though this valuation process remains one of the most challenging aspects of NFT lending due to the subjective nature of digital art pricing.

Interest rates for NFT-backed loans vary significantly based on collection reputation, loan duration, and market conditions, typically ranging from 15% to 40% annually with shorter-term loans often commanding higher rates due to increased administrative overhead and market volatility risks. These rates reflect the experimental nature of NFT lending and the premium required to compensate for elevated risk levels compared to traditional collateral types.

Technological Infrastructure and Smart Contract Architecture

The technological foundation underlying NFT-backed lending relies heavily on sophisticated smart contract systems that must handle complex interactions between borrowers, lenders, and collateral assets while maintaining security, transparency, and efficient execution of loan terms. These systems represent significant advances in decentralized finance technology, incorporating multi-signature security, automated liquidation mechanisms, and real-time price monitoring capabilities.

Smart contract architecture for NFT lending typically involves multiple interconnected contracts including collateral vaults that securely hold deposited NFTs, pricing oracles that provide real-time valuation data, liquidation engines that execute automatic sales when necessary, and governance contracts that manage platform parameters and protocol upgrades. This modular approach allows for greater flexibility and security while enabling continuous improvement of lending protocols.

Pricing oracles represent one of the most critical components of NFT lending infrastructure, as accurate and timely valuation data is essential for maintaining appropriate collateral ratios and executing fair liquidation procedures. These systems aggregate data from multiple NFT marketplaces, analyze transaction patterns, and apply sophisticated algorithms to estimate current market values for diverse digital assets.

The integration with various NFT marketplaces and trading platforms creates complex technical challenges related to cross-platform compatibility, data standardization, and real-time synchronization of market information. Advanced lending platforms maintain connections to multiple data sources to ensure comprehensive market coverage and reduce the risk of pricing manipulation or data feed failures.

Automated liquidation systems must balance the need for timely execution with fair pricing for both borrowers and lenders, often incorporating grace periods, partial liquidation mechanisms, and sophisticated auction systems that maximize recovery values while minimizing market disruption. These systems represent significant technological achievements in automated asset management and risk mitigation.

Security considerations for NFT lending platforms include protection against smart contract vulnerabilities, oracle manipulation attacks, front-running exploits, and various forms of collateral fraud. Multi-layered security approaches incorporating formal verification, bug bounty programs, and continuous monitoring systems help protect against these diverse threat vectors.

Market Dynamics and Collection Analysis

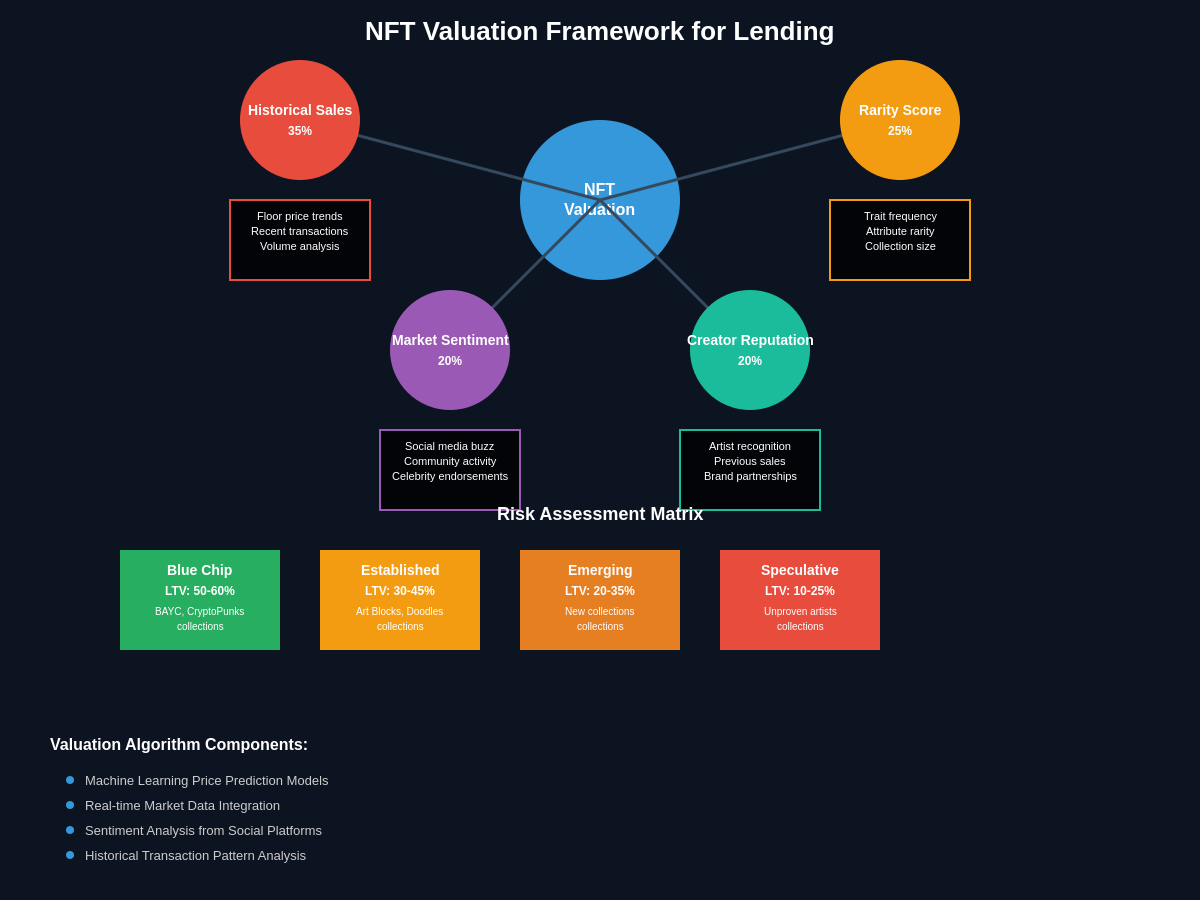

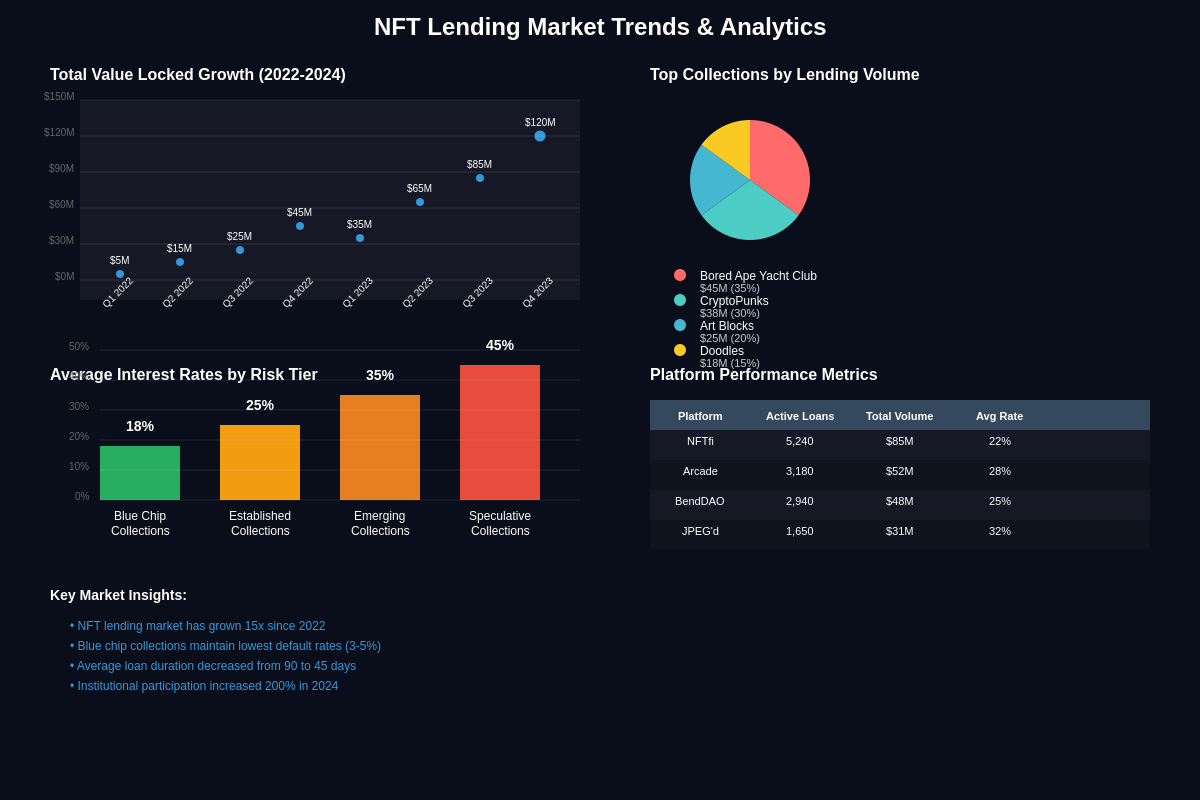

The NFT lending market has evolved to accommodate diverse collection types with varying risk profiles, liquidity characteristics, and valuation methodologies that reflect the broader maturity and sophistication of digital art markets. Premium collections such as CryptoPunks, Bored Ape Yacht Club, and Art Blocks pieces typically command higher loan-to-value ratios and more favorable terms due to their established market presence and relatively predictable pricing patterns.

Collection analysis for lending purposes involves comprehensive evaluation of historical trading volumes, price stability, community engagement, creator reputation, and long-term value potential that extends far beyond simple floor price calculations. Advanced lending platforms employ machine learning algorithms and market analysis tools to assess collection risk profiles and determine appropriate lending parameters for different asset categories.

The emergence of fractionalized NFT lending represents an innovative approach to increasing liquidity and accessibility by allowing multiple lenders to participate in funding larger loans secured by high-value digital assets. This model distributes risk across multiple participants while enabling larger loan amounts for premium NFT collateral that might otherwise exceed individual lender risk tolerances.

Seasonal market dynamics significantly impact NFT lending operations, with demand for loans often increasing during market downturns when collectors need liquidity but prefer not to sell at depressed prices. Conversely, bull market periods typically see reduced lending demand as rising asset values provide natural liquidity through sales while increasing the opportunity cost of locking assets as collateral.

The role of celebrity and institutional involvement in NFT collections has created new categories of lending risk and opportunity, with high-profile endorsements potentially driving rapid value appreciation while also introducing volatility related to public relations events and celebrity behavior. Lending platforms must carefully evaluate these external factors when assessing collection suitability for collateralization.

Geographic and regulatory considerations affect NFT lending markets differently across jurisdictions, with some regions embracing digital asset innovation while others impose restrictions that limit platform operations and user access. These regulatory variations create complex compliance challenges for lending platforms seeking to operate across multiple markets while maintaining consistent service quality.

Risk Assessment and Valuation Methodologies

Accurate valuation of NFT collateral represents perhaps the most complex challenge facing the digital asset lending industry, requiring sophisticated methodologies that account for artistic merit, historical significance, rarity factors, and market sentiment while managing the inherent subjectivity and volatility associated with digital collectibles. Traditional asset valuation approaches often prove inadequate for NFTs due to their unique characteristics and the rapidly evolving nature of digital art markets.

Automated valuation models for NFTs typically incorporate multiple data points including recent sales within the same collection, overall collection performance metrics, rarity scoring based on trait analysis, and broader market trends that affect digital asset pricing. However, these quantitative approaches must be balanced with qualitative assessments that consider artistic value, cultural significance, and community sentiment factors that significantly influence NFT pricing but resist easy quantification.

The challenge of analyzing NFT market trends and pricing patterns requires sophisticated data analysis capabilities that can process information from multiple marketplaces, social media platforms, and community forums to develop comprehensive market intelligence. Advanced platforms employ natural language processing and sentiment analysis to incorporate community feedback and social signals into their valuation models.

Risk stratification systems classify NFTs into different categories based on collection maturity, artist reputation, historical price stability, and liquidity characteristics that help lenders make informed decisions about appropriate loan terms and collateral requirements. These systems must continuously evolve as new collections emerge and market dynamics shift in response to technological innovations and cultural trends.

The development of standardized risk metrics for NFT lending has become increasingly important as the industry matures and institutional participants seek consistent frameworks for evaluating digital asset collateral. Industry initiatives aimed at creating common risk assessment standards help improve market efficiency while enabling better comparison of lending opportunities across different platforms and collection types.

Stress testing and scenario analysis help lending platforms understand potential losses under various market conditions including severe price declines, liquidity crises, and broader cryptocurrency market volatility that can significantly impact NFT values. These analytical approaches enable more informed risk management decisions and help platforms maintain appropriate capital reserves for potential losses.

Legal and Regulatory Framework Evolution

The regulatory landscape for NFT-backed lending continues to evolve as authorities worldwide grapple with how to classify and oversee these innovative financial instruments that combine elements of securities law, banking regulation, and intellectual property rights in unprecedented ways. Current regulatory uncertainty creates challenges for both lending platforms and users while highlighting the need for clear legal frameworks that balance innovation with consumer protection.

Jurisdictional variations in NFT and cryptocurrency regulation create complex compliance challenges for lending platforms that must navigate different legal requirements across multiple markets while maintaining consistent service offerings. Some regions have embraced digital asset innovation with favorable regulatory frameworks, while others have imposed restrictions that limit platform operations and user access to NFT lending services.

The classification of NFTs for regulatory purposes remains contentious, with different authorities treating them as securities, commodities, or unique digital property depending on their characteristics and use cases. This regulatory ambiguity affects how NFT lending is supervised and what compliance requirements apply to platforms operating in different jurisdictions.

Consumer protection considerations for NFT lending include ensuring fair pricing transparency, adequate risk disclosure, and appropriate dispute resolution mechanisms that protect borrowers from predatory lending practices while maintaining the efficiency benefits of automated smart contract systems. Regulatory authorities are increasingly focused on these consumer protection aspects as NFT lending becomes more mainstream.

The intersection of traditional banking regulations with DeFi lending protocols creates additional complexity for platforms that must comply with anti-money laundering requirements, know-your-customer procedures, and various reporting obligations while maintaining the decentralized and pseudonymous characteristics that make blockchain-based lending attractive to users.

International coordination efforts aim to develop harmonized approaches to digital asset regulation that could provide greater clarity for NFT lending platforms while reducing compliance costs and enabling more efficient cross-border operations. These initiatives reflect growing recognition of the global nature of digital asset markets and the need for coordinated regulatory responses.

Platform Architecture and User Experience Design

Leading NFT lending platforms have invested heavily in creating intuitive user interfaces that simplify the complex process of collateralizing digital assets while providing comprehensive information about loan terms, risks, and market conditions. These platforms must balance sophisticated functionality with accessibility to serve both experienced DeFi users and newcomers to blockchain-based lending.

The integration of wallet connectivity, collection browsing, and loan management tools requires seamless coordination between multiple blockchain networks, marketplace APIs, and user interface components that create unified experiences despite the underlying technical complexity. Advanced platforms provide single-dashboard access to all lending activities while maintaining security through non-custodial wallet integration.

Mobile accessibility has become increasingly important as NFT collecting and trading migrate to mobile platforms, requiring lending interfaces that function effectively on smaller screens while maintaining full functionality for complex financial transactions. Progressive web applications and dedicated mobile apps help platforms reach broader audiences while providing convenient access to lending services.

Customer support systems for NFT lending must address both technical issues related to blockchain transactions and financial questions about loan terms, collateral management, and market risks. Educational resources, comprehensive documentation, and responsive support teams help users navigate the complexities of NFT-backed lending while building confidence in platform reliability.

The implementation of notification systems that alert users to important events such as approaching liquidation thresholds, interest payment due dates, and market changes affecting their collateral helps prevent unwanted liquidations while keeping borrowers informed about their loan status. These systems must balance informativeness with user preferences to avoid notification fatigue.

Community features including user forums, educational content, and social trading elements help create engaged user bases while providing platforms for knowledge sharing and peer support that enhance overall user experience. These community aspects become particularly valuable in complex financial products where user education and support networks significantly impact success rates.

Economic Impact and Market Development

The NFT lending market has experienced remarkable growth since its inception, with total value locked in NFT lending protocols reaching hundreds of millions of dollars as collectors and investors increasingly recognize the value of unlocking liquidity from their digital asset holdings without permanently selling them. This growth reflects both the maturation of NFT markets and the sophistication of DeFi lending infrastructure.

The broader economic impact of NFT lending extends beyond direct lending volume to include increased NFT market liquidity, enhanced price discovery mechanisms, and new investment strategies that treat digital collectibles as productive assets rather than purely speculative holdings. These developments contribute to the overall maturation and institutionalization of digital asset markets.

Integration with traditional finance remains limited but is beginning to emerge as institutional lenders explore opportunities to participate in NFT-backed lending markets through specialized funds and lending vehicles. This institutional participation could significantly increase available capital while bringing traditional risk management practices to digital asset lending.

The development of secondary markets for NFT-backed loans enables lenders to sell their loan positions to other investors, creating additional liquidity and risk distribution mechanisms that make NFT lending more attractive to a broader range of participants. These secondary markets represent important infrastructure developments that enhance overall market efficiency.

Cross-chain lending protocols are emerging that enable NFTs from different blockchain networks to be used as collateral for loans denominated in various cryptocurrencies, creating more flexible and efficient lending markets while reducing the friction associated with managing assets across multiple blockchain ecosystems.

The impact of broader cryptocurrency market cycles on NFT lending patterns creates interesting dynamics where lending demand often increases during market downturns as collectors seek liquidity without selling, while bull markets see reduced lending activity as rising asset values provide natural exit opportunities.

Liquidation Mechanisms and Asset Recovery

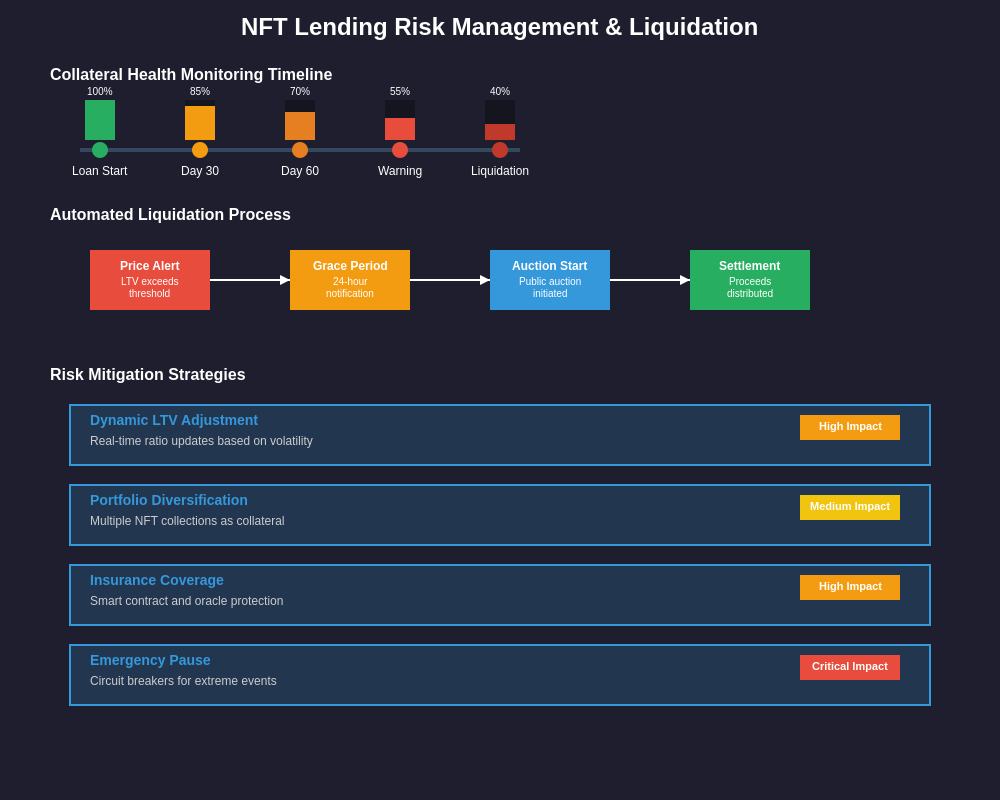

The liquidation process for NFT collateral presents unique challenges compared to traditional asset liquidation due to the illiquid nature of many digital collectibles and the subjective valuation that characterizes art markets. Effective liquidation mechanisms must balance the need for timely execution with fair pricing that protects both borrower and lender interests while maintaining market stability.

Auction-based liquidation systems have emerged as the preferred approach for most NFT lending platforms, providing transparent price discovery while enabling competitive bidding that can maximize recovery values. These systems typically incorporate reserve prices, bidding periods, and various auction formats designed to optimize outcomes for different types of NFT collateral.

The timing of liquidation procedures significantly impacts recovery rates, with platforms implementing sophisticated monitoring systems that track collateral values in real-time and execute liquidation procedures when predetermined thresholds are reached. Grace periods and notification systems help borrowers avoid liquidation by providing opportunities to add additional collateral or repay loans before automatic liquidation occurs.

Partial liquidation mechanisms enable platforms to sell portions of NFT collections or fractionalized interests in high-value pieces to meet collateral requirements without completely liquidating borrower positions. These approaches help minimize the impact of temporary market volatility while providing more flexible risk management options.

The development of professional liquidation services specializing in NFT sales has improved recovery rates by leveraging specialized market knowledge, established buyer networks, and sophisticated marketing techniques that maximize sale prices for liquidated assets. These services represent important infrastructure developments that enhance the viability of NFT-backed lending.

Cross-platform liquidation capabilities enable lending platforms to sell NFT collateral across multiple marketplaces simultaneously, increasing exposure to potential buyers while reducing the impact of platform-specific liquidity constraints. This approach helps optimize sale prices while reducing liquidation timeframes.

Insurance and Risk Mitigation Strategies

The development of insurance products specifically designed for NFT lending represents a crucial infrastructure advancement that helps protect both lenders and borrowers against various risks including smart contract failures, oracle manipulation, and extreme market volatility that could result in significant losses beyond normal lending risks.

Parametric insurance models that automatically pay claims based on predetermined triggers such as extreme price movements or technical failures provide efficient protection mechanisms that align well with the automated nature of DeFi lending protocols. These insurance products help reduce the overall risk profile of NFT lending while providing predictable protection against specific loss scenarios.

The integration of insurance with lending platforms enables automatic coverage enrollment that protects users without requiring complex insurance purchasing decisions, while competitive insurance markets help reduce costs and improve coverage terms. This integration represents important progress toward making NFT lending safer and more accessible to mainstream users.

Risk pooling mechanisms that spread losses across multiple participants help reduce individual exposure while enabling more efficient capital allocation for insurance purposes. These shared risk models reflect successful approaches from traditional insurance markets while adapting to the unique characteristics of digital asset lending.

The development of specialized risk assessment tools for NFT insurance helps insurers price coverage appropriately while providing lending platforms with additional risk management capabilities that enhance overall system stability. These tools represent important technological advances that support the continued growth and maturation of NFT lending markets.

Regulatory developments affecting insurance for digital assets create both opportunities and challenges for coverage providers while highlighting the need for clear legal frameworks that support innovation while protecting consumers. The evolution of these regulatory frameworks will significantly impact the availability and cost of insurance for NFT lending participants.

Future Developments and Innovation Trends

The integration of artificial intelligence and machine learning technologies into NFT valuation and risk assessment systems promises to significantly improve the accuracy and efficiency of lending decisions while reducing the reliance on subjective judgment that currently characterizes much of the NFT lending process. These technological advances could enable more precise pricing models and better risk management capabilities.

The development of cross-chain NFT lending protocols that enable seamless collateralization of digital assets across different blockchain networks represents a significant opportunity to increase market efficiency while reducing the friction associated with managing multi-chain NFT portfolios. These protocols could dramatically expand the addressable market for NFT lending services.

Institutional adoption of NFT lending is expected to accelerate as traditional financial institutions develop comfort with digital asset custody and risk management while recognizing the potential returns available in this emerging market segment. This institutional participation could provide significant capital inflows while bringing professional risk management practices to NFT lending.

The emergence of programmable NFTs with embedded financial features could enable new forms of automated lending where smart contracts handle loan negotiations, collateral management, and liquidation procedures without requiring external platform intervention. These innovations could significantly reduce costs while improving efficiency for routine lending transactions.

Integration with metaverse platforms and virtual world economies could create new use cases for NFT-backed lending where digital assets serve as collateral for loans used to purchase virtual real estate, game items, or other metaverse assets. These applications could significantly expand the practical utility of NFT lending beyond pure financial speculation.

The development of regulatory sandboxes and clear legal frameworks for NFT lending could provide the certainty needed for broader institutional adoption while enabling platforms to operate more efficiently across multiple jurisdictions. These regulatory developments represent crucial infrastructure requirements for continued market growth and maturation.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. NFT-backed lending involves significant risks including total loss of collateral, and readers should conduct their own research and consult with qualified professionals before participating in any NFT lending activities. Cryptocurrency and NFT markets are highly volatile and regulatory frameworks continue to evolve.