Revolutionary Transformation of Financial Services

The financial landscape stands on the precipice of a fundamental transformation as programmable money and smart loans emerge as the next evolutionary step in monetary systems. This paradigm shift represents more than technological innovation; it embodies a complete reimagining of how financial services operate, from interest rate determination to loan execution and risk management. Traditional banking systems, constrained by legacy infrastructure and manual processes, are giving way to autonomous financial protocols that can adjust parameters in real-time, execute complex financial instruments without human intervention, and optimize capital efficiency through algorithmic precision.

Advanced financial modeling and real-time market analysis have become essential tools for understanding these programmable financial systems, as they enable the sophisticated risk assessment and dynamic pricing mechanisms that make autonomous lending possible. The convergence of blockchain technology, artificial intelligence, and decentralized finance has created an environment where money itself becomes programmable, capable of executing predefined functions and adapting to changing market conditions without requiring traditional intermediaries.

The implications of programmable money extend far beyond simple automation of existing financial processes. These systems introduce entirely new categories of financial products, enable unprecedented levels of capital efficiency, and create opportunities for financial inclusion that were previously impossible under traditional banking models. Smart loans, powered by autonomous interest rate algorithms and real-time risk assessment, represent just the beginning of what becomes possible when money gains the ability to execute complex logic and respond dynamically to market conditions.

Historical Context and Evolution

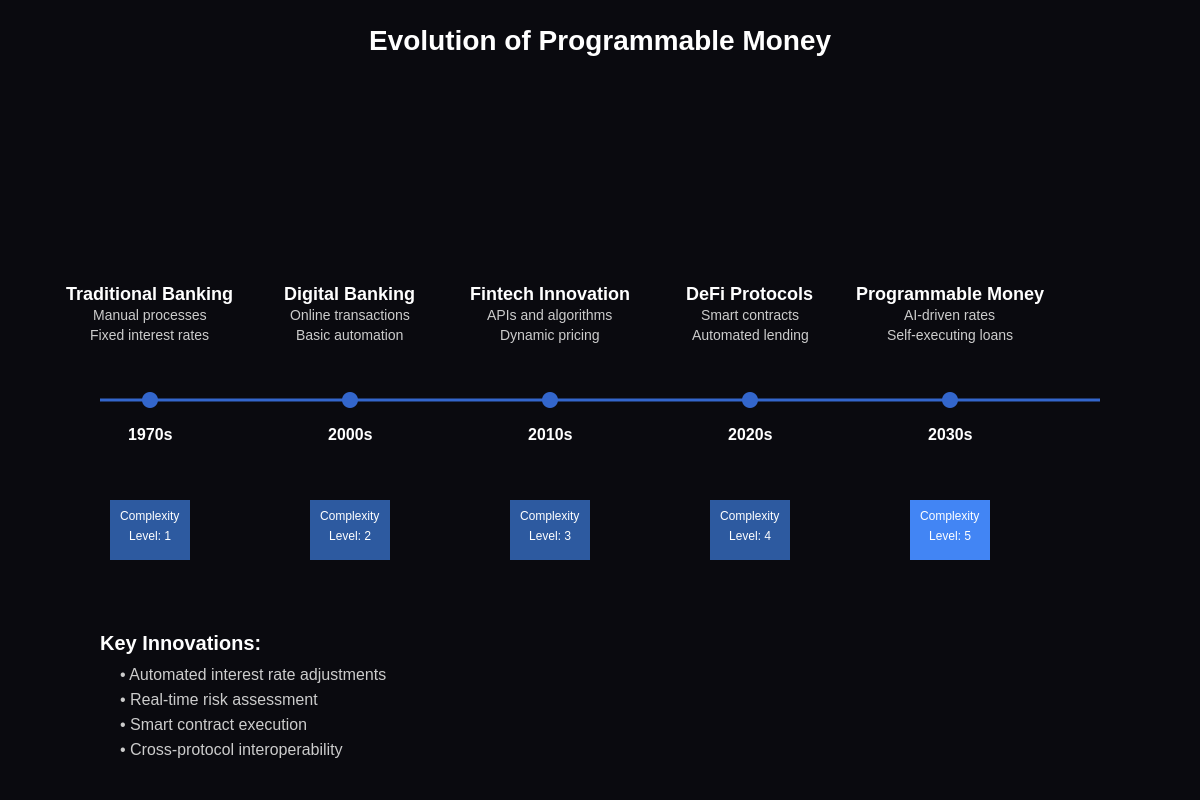

The journey toward programmable money began with the digitization of traditional banking systems in the late twentieth century, but the concept has evolved dramatically with each technological advancement. Early electronic banking systems simply replicated physical processes in digital form, maintaining the same fundamental limitations of manual oversight, fixed interest rates, and centralized control that had characterized banking for centuries. The introduction of algorithmic trading and automated clearing systems in the 1990s provided the first glimpse of what autonomous financial systems might achieve, but these early implementations remained tethered to traditional banking infrastructure and regulatory frameworks.

The emergence of peer-to-peer lending platforms in the 2000s marked a significant milestone in the evolution toward programmable finance, introducing dynamic pricing models and algorithmic risk assessment to consumer lending markets. Platforms like LendingClub and Prosper demonstrated that technology could enable more efficient capital allocation and provide better risk-adjusted returns than traditional banking, while simultaneously expanding access to credit for underserved populations. However, these platforms still relied on centralized infrastructure and traditional payment systems, limiting their ability to achieve true programmability and autonomous operation.

The launch of Bitcoin in 2009 introduced the foundational technology that would eventually enable programmable money, providing a decentralized, trustless system for value transfer that operated independently of traditional banking infrastructure. While Bitcoin itself had limited programmability, it established the blockchain as a platform for creating autonomous financial systems and inspired the development of more sophisticated smart contract platforms. The subsequent launch of Ethereum in 2015 provided the programmable infrastructure necessary for complex financial applications, enabling the creation of autonomous protocols that could execute sophisticated financial logic without human intervention.

Cryptocurrency market evolution and DeFi protocol adoption accelerated rapidly following Ethereum’s introduction, with total value locked in decentralized finance protocols growing from virtually zero in 2017 to over $200 billion by 2024. This explosive growth demonstrated the market demand for programmable financial services and validated the viability of autonomous lending protocols, automated market makers, and algorithmic interest rate models that form the foundation of modern programmable money systems.

Technical Architecture of Smart Loans

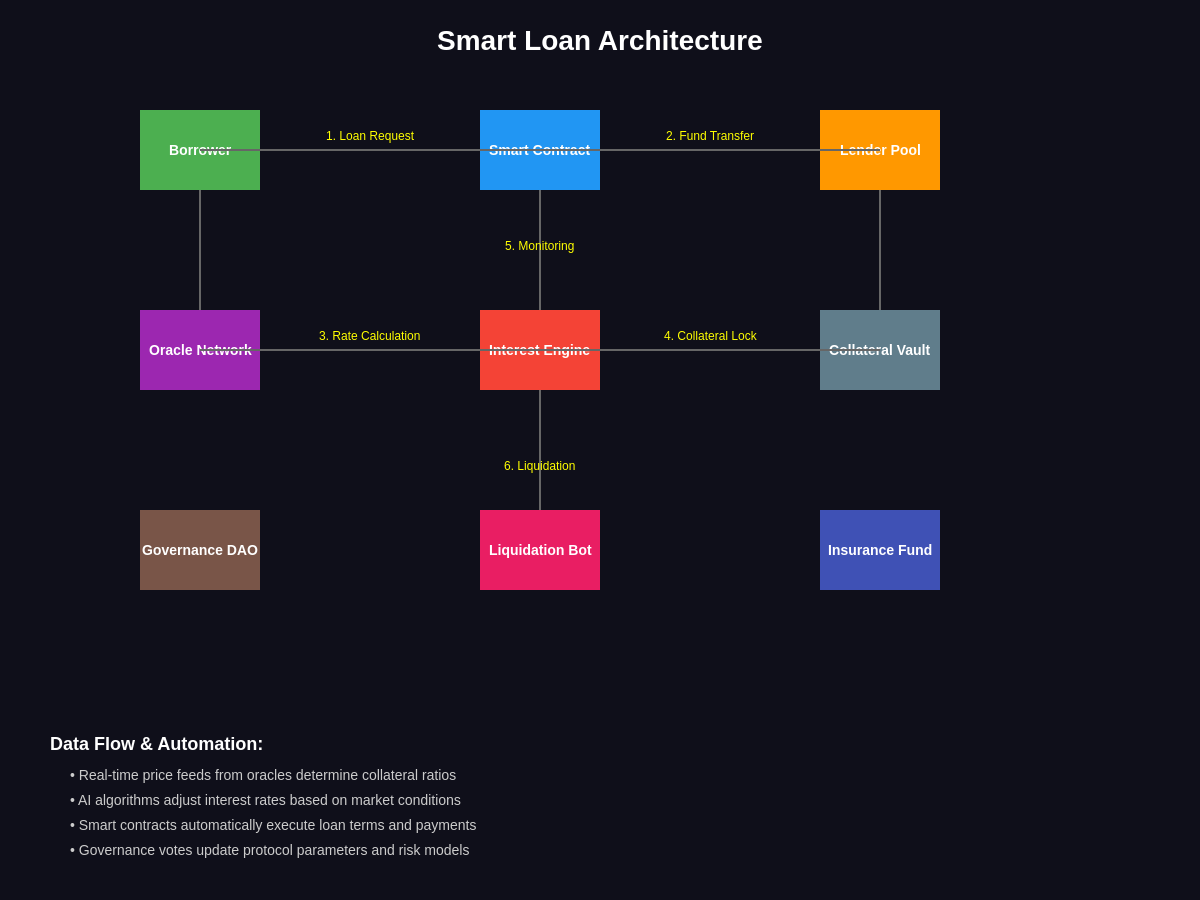

Smart loans represent a sophisticated integration of blockchain technology, artificial intelligence, and financial engineering that enables the creation of autonomous lending systems capable of operating without traditional intermediaries. The technical architecture underlying these systems involves multiple interconnected components, each serving specific functions in the loan origination, management, and settlement process. At the foundation lies the smart contract layer, which contains the immutable code that governs loan terms, interest calculations, collateral management, and liquidation procedures.

The smart contract architecture typically consists of multiple specialized contracts working in concert to manage different aspects of the lending process. Core lending contracts handle the fundamental mechanics of loan creation, fund distribution, and repayment processing, while separate contracts manage collateral deposits, interest rate calculations, and liquidation events. This modular approach enables greater flexibility and security, allowing individual components to be upgraded or modified without affecting the entire system, while also enabling formal verification of critical financial logic.

Oracle networks play a crucial role in smart loan architecture by providing external data feeds that enable contracts to respond to real-world events and market conditions. Price oracles supply real-time asset valuations necessary for collateral ratio monitoring and liquidation triggers, while interest rate oracles provide benchmark rates and market data used in dynamic pricing models. The reliability and security of these oracle systems are paramount, as they provide the bridge between on-chain smart contracts and off-chain financial data that determines loan parameters and risk assessments.

Interest rate engines represent one of the most sophisticated components of smart loan architecture, implementing complex algorithms that adjust borrowing costs based on supply and demand dynamics, risk assessments, and broader market conditions. These engines typically incorporate multiple data sources including pool utilization rates, historical default data, macroeconomic indicators, and real-time market volatility measures to calculate optimal interest rates that balance borrower accessibility with lender returns. Advanced implementations utilize machine learning models trained on historical lending data to predict optimal pricing strategies and automatically adjust parameters to maximize protocol efficiency.

Collateral management systems within smart loan architectures must handle the complex task of monitoring asset values, calculating risk-adjusted collateral ratios, and executing liquidations when necessary to protect lender interests. These systems typically implement sophisticated risk models that account for asset volatility, correlation risks, and liquidity considerations when determining appropriate collateralization requirements. Automated liquidation mechanisms are designed to trigger when collateral values fall below predetermined thresholds, with liquidation bots competing to execute these transactions efficiently while minimizing losses for all parties involved.

Programmable Interest Rate Mechanisms

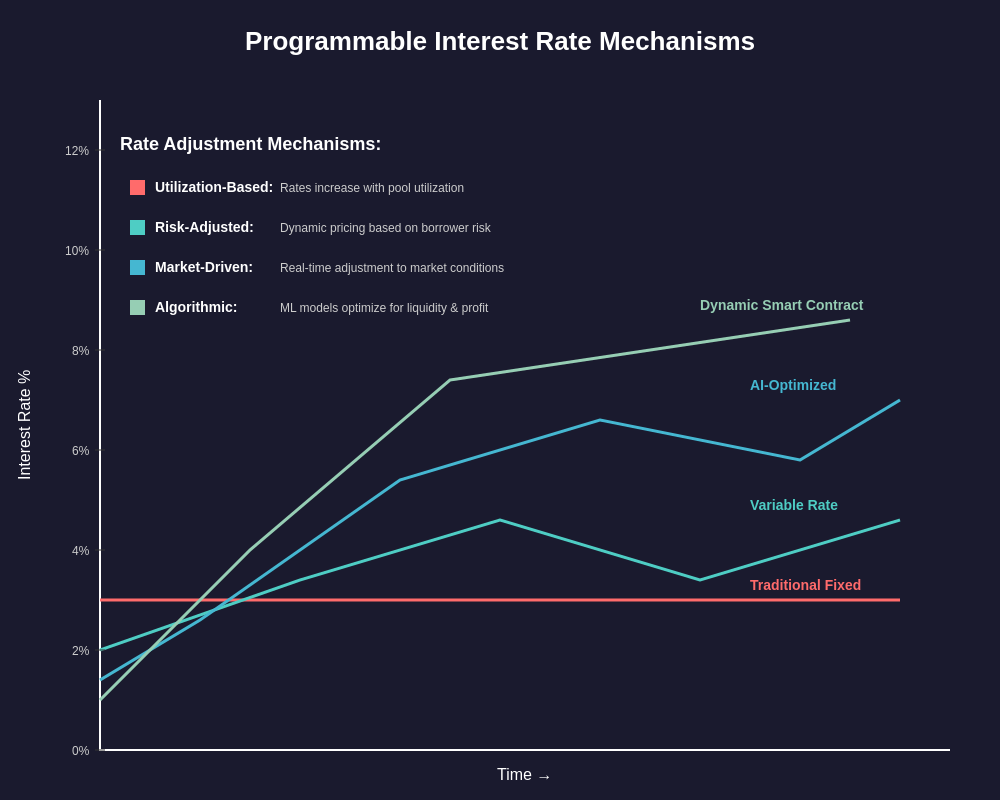

The development of programmable interest rate mechanisms represents one of the most significant innovations in modern financial technology, enabling the creation of dynamic pricing systems that can respond to market conditions in real-time while optimizing capital efficiency across lending markets. Traditional interest rate setting relies on periodic adjustments made by human decision-makers based on lagging economic indicators and subjective assessments of market conditions. In contrast, programmable interest rates utilize algorithmic models that process vast amounts of real-time data to continuously optimize pricing decisions based on objective mathematical models and predefined optimization criteria.

Utilization-based interest rate models form the foundation of most programmable lending systems, automatically adjusting borrowing costs based on the ratio of borrowed funds to total available liquidity within lending pools. These models typically implement exponential curves that gradually increase interest rates as utilization approaches capacity limits, creating natural incentives for borrowers to seek alternative funding sources and for lenders to provide additional capital when rates become attractive. The specific parameters of these curves can be dynamically adjusted based on market conditions, asset characteristics, and protocol objectives.

Risk-adjusted pricing mechanisms represent a more sophisticated approach to programmable interest rates, incorporating real-time assessments of borrower creditworthiness, collateral quality, and market volatility into interest rate calculations. These systems utilize machine learning algorithms trained on historical lending data to identify patterns predictive of default risk and automatically adjust pricing to reflect these risk assessments. Advanced implementations can incorporate alternative data sources including on-chain transaction history, social media sentiment, and macroeconomic indicators to create more comprehensive risk profiles and pricing models.

Global interest rate trends and monetary policy analysis provide crucial context for programmable interest rate systems, as these automated mechanisms must account for broader macroeconomic conditions and central bank policies when setting optimal rates. Sophisticated programmable systems can automatically adjust their base rates and risk premiums in response to changes in government bond yields, central bank policy rates, and inflation expectations, ensuring that decentralized lending rates remain competitive with traditional financial markets while accounting for the unique risks and benefits of programmable finance.

Market-driven interest rate mechanisms implement auction-based systems where borrowers and lenders can specify their desired rates and terms, with smart contracts automatically matching counterparties and executing loans at market-clearing prices. These systems enable more efficient price discovery by allowing market participants to express their preferences directly rather than accepting algorithmically determined rates. Advanced implementations can incorporate order book mechanics, yield curve construction, and sophisticated matching algorithms that optimize execution for all participants while maintaining fair and transparent pricing.

Decentralized Finance Integration

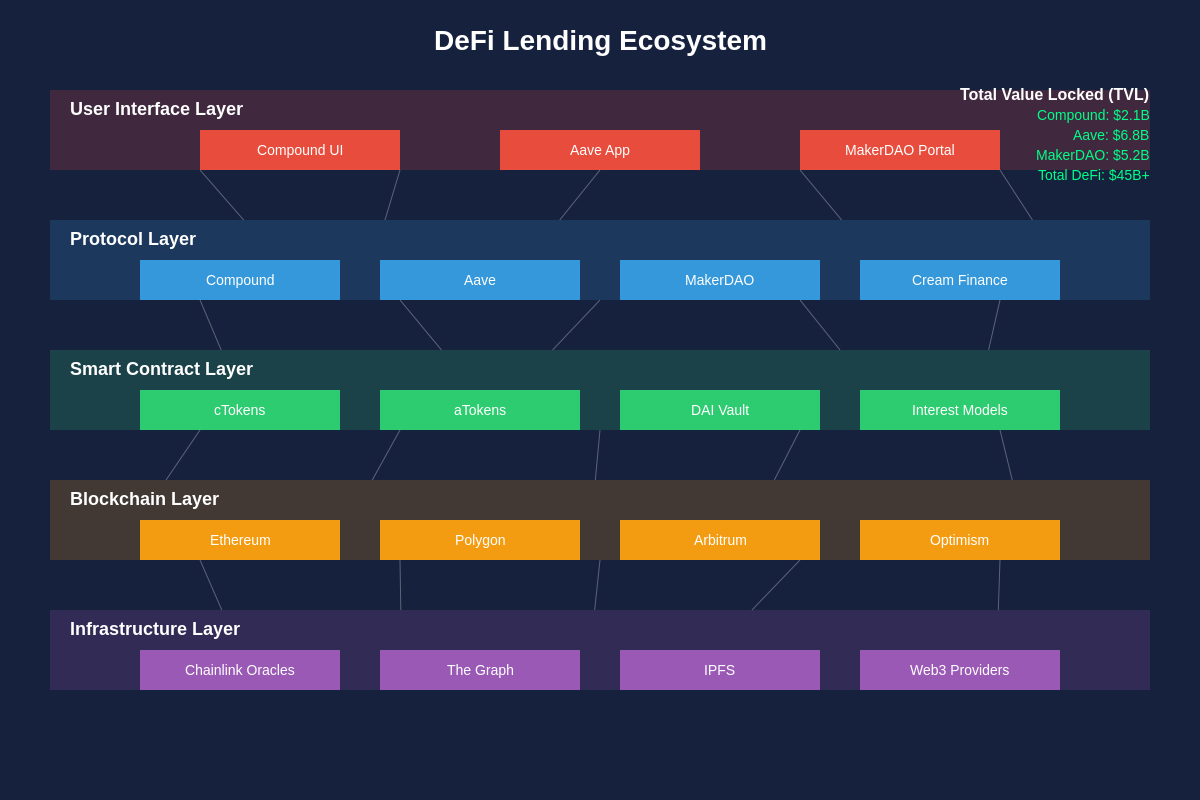

The integration of programmable money concepts with decentralized finance protocols has created a synergistic ecosystem where autonomous financial services can interact seamlessly across multiple platforms and asset types. This integration enables the creation of complex financial products that combine lending, trading, and investment functions within single programmable systems, while also facilitating the development of cross-protocol yield optimization strategies that maximize returns for participants. The composability of DeFi protocols allows programmable money systems to leverage existing infrastructure while contributing new capabilities to the broader ecosystem.

Liquidity mining and yield farming mechanisms have become integral components of programmable money systems, providing incentives for users to supply capital to lending pools while simultaneously distributing governance tokens that give participants a stake in protocol development and fee revenue. These systems typically implement sophisticated reward calculation algorithms that adjust distribution rates based on market conditions, protocol performance, and strategic objectives. Advanced implementations can automatically optimize reward distributions across multiple assets and time periods to maximize participation while minimizing dilution of existing token holders.

Cross-chain interoperability has emerged as a critical requirement for programmable money systems, enabling them to operate across multiple blockchain networks and access liquidity from diverse sources. Bridge protocols and cross-chain communication systems allow smart loans to utilize collateral from multiple networks, access price feeds from various sources, and settle transactions on the most cost-effective platforms available. This interoperability significantly expands the addressable market for programmable lending while reducing the concentration risk associated with single-chain implementations.

Automated market makers and decentralized exchanges provide essential infrastructure for programmable money systems by enabling automatic conversion between different assets and providing liquidity for loan settlements and collateral liquidations. Integration with AMM protocols allows smart loan systems to automatically swap collateral assets during liquidation events, convert between different stablecoins for optimal capital efficiency, and provide users with seamless access to different asset types without requiring multiple transaction steps or external exchange accounts.

Governance mechanisms within DeFi protocols enable programmable money systems to evolve and adapt over time through decentralized decision-making processes. Token-based voting systems allow stakeholders to propose and implement changes to interest rate models, risk parameters, supported assets, and protocol features without requiring centralized control or traditional corporate governance structures. These governance systems often implement sophisticated delegation and proposal mechanisms that balance participation with technical expertise while ensuring that protocol evolution serves the interests of all stakeholders.

Risk Management and Security Protocols

The implementation of robust risk management and security protocols represents one of the most critical aspects of programmable money systems, as these autonomous financial platforms must protect against a wide variety of threats while maintaining operational efficiency and user accessibility. Traditional financial institutions rely on human oversight, regulatory compliance, and insurance mechanisms to manage risk, but programmable systems must encode these protections directly into their smart contract logic and operational procedures. This requirement has led to the development of sophisticated automated risk management systems that can identify, assess, and respond to threats more quickly and consistently than human-managed systems.

Smart contract security forms the foundation of risk management in programmable money systems, requiring extensive auditing, formal verification, and testing procedures to ensure that financial logic operates correctly under all conditions. Security audits by specialized firms have become standard practice for major lending protocols, with multiple independent audits typically required before protocols handle significant amounts of user funds. Formal verification techniques enable mathematical proof that smart contracts will behave correctly according to their specifications, providing higher assurance levels than traditional testing approaches for critical financial logic.

Oracle security represents another critical component of risk management, as programmable money systems depend on external data feeds to make critical decisions about interest rates, collateral values, and liquidation triggers. Robust oracle systems typically implement multiple independent data sources, outlier detection algorithms, and time-weighted average pricing to prevent manipulation and ensure data accuracy. Advanced implementations can automatically detect and respond to oracle failures or attacks by temporarily suspending operations or switching to backup data sources until normal operation can be restored.

Liquidation mechanisms must be designed to operate effectively under extreme market conditions while protecting both borrowers and lenders from excessive losses. Effective liquidation systems typically implement progressive liquidation schedules that sell only the minimum amount of collateral necessary to restore healthy collateral ratios, while also providing incentives for external parties to execute liquidations promptly when they become necessary. Advanced systems can incorporate predictive models that identify loans at risk of liquidation before they reach trigger thresholds, enabling proactive risk management and potentially avoiding liquidation events entirely.

DeFi security analysis and risk assessment frameworks have become essential tools for evaluating the safety and reliability of programmable money systems, providing standardized methodologies for assessing smart contract risks, economic security models, and operational procedures. These frameworks typically evaluate multiple dimensions of risk including technical implementation quality, economic incentive alignment, governance structure effectiveness, and operational security practices to provide comprehensive risk assessments for investors and users.

Insurance mechanisms specifically designed for DeFi protocols have emerged to provide additional protection against smart contract failures, oracle manipulations, and other technical risks that are unique to programmable money systems. These insurance protocols typically operate through decentralized mutual organizations where participants pool capital to cover losses in exchange for premiums and governance rights. Coverage can extend to technical failures, economic attacks, and operational disruptions that could result in user losses despite proper protocol operation.

Economic Models and Tokenomics

The economic design of programmable money systems requires careful consideration of incentive structures, token distribution mechanisms, and long-term sustainability models that align the interests of all participants while creating viable business models for protocol development and maintenance. Unlike traditional financial institutions that generate revenue through interest rate spreads and fee collection, programmable money systems must create value through efficient capital allocation, reduced intermediation costs, and innovative financial products that provide superior risk-adjusted returns to participants.

Token-based governance systems have become the predominant model for aligning stakeholder interests in programmable money protocols, with governance tokens typically distributed to users based on their participation in lending, borrowing, and liquidity provision activities. These tokens provide holders with voting rights on protocol parameters, fee structures, and development priorities while also serving as a store of value that captures the success of the underlying protocol. The distribution mechanisms for governance tokens must balance fair access with sustainable incentive structures that encourage long-term participation over short-term speculation.

Revenue models for programmable money systems typically involve capturing a portion of the interest rate spreads generated by lending activities, along with fees for specialized services such as liquidation processing, cross-chain transactions, and premium features. These revenue streams must be sufficient to fund ongoing development, security audits, oracle services, and other operational expenses while providing returns to token holders and maintaining competitive rates for users. Successful protocols often implement dynamic fee structures that adjust based on market conditions and protocol utilization to optimize revenue generation.

Deflationary tokenomics mechanisms have gained popularity as a means of creating long-term value accrual for governance token holders while reducing token supply over time. These mechanisms typically involve using protocol revenue to purchase and permanently remove tokens from circulation, creating upward pressure on token prices as protocol adoption and revenue generation increase. Advanced implementations can automatically adjust the rate of token burns based on market conditions, protocol performance, and predetermined monetary policy rules.

Liquidity incentive programs play a crucial role in bootstrapping programmable money systems by providing additional returns to early participants while building the critical mass of liquidity necessary for efficient operation. These programs typically involve distributing governance tokens to lenders and borrowers based on their usage of protocol services, with distribution rates often weighted to encourage utilization of new features or underused asset types. The design of these incentive programs must balance rapid growth with long-term sustainability, ensuring that programs can be maintained as protocols mature and token values appreciate.

Regulatory Landscape and Compliance

The regulatory environment surrounding programmable money and smart loans remains complex and rapidly evolving, with different jurisdictions taking varying approaches to the oversight of autonomous financial systems and decentralized lending protocols. Traditional financial regulations were designed for centralized institutions with clear legal entities and human decision-makers, creating challenges for regulators seeking to apply existing frameworks to decentralized, autonomous systems that operate without traditional intermediaries or geographic boundaries.

Securities regulations represent one of the most significant compliance challenges for programmable money systems, particularly regarding the classification of governance tokens and the operation of automated lending protocols. Many jurisdictions are grappling with questions about whether governance tokens constitute securities, how automated protocols should be regulated, and what disclosure requirements should apply to decentralized systems. Some projects have proactively engaged with regulators to establish compliant structures, while others have adopted decentralized governance models designed to minimize regulatory exposure.

Anti-money laundering and know-your-customer regulations present additional challenges for programmable money systems, as traditional compliance procedures rely on identity verification and transaction monitoring by centralized institutions. Some protocols have implemented compliance layers that require identity verification for certain services or transaction amounts, while others have focused on developing privacy-preserving compliance solutions that can satisfy regulatory requirements without compromising user privacy or system decentralization.

Cross-border regulatory coordination has become increasingly important as programmable money systems operate globally and serve users across multiple jurisdictions simultaneously. International organizations and regulatory bodies are working to develop coordinated approaches to decentralized finance regulation, while individual jurisdictions are implementing their own frameworks for oversight and compliance. This patchwork of regulatory approaches creates complexity for protocol developers and users while potentially fragmenting the global market for programmable financial services.

Regulatory developments and policy announcements continue to shape the evolution of programmable money systems, with major regulatory decisions often triggering significant market reactions and protocol adaptations. Industry participants closely monitor regulatory developments and often adjust their technical implementations and business models in response to new guidance or enforcement actions from financial regulators.

Regulatory technology solutions specifically designed for decentralized finance are emerging to help protocols maintain compliance while preserving their autonomous and decentralized characteristics. These solutions include automated compliance monitoring systems, privacy-preserving identity verification protocols, and risk assessment tools that can help protocols identify and address regulatory concerns proactively. The development of these RegTech solutions is crucial for the long-term viability and mainstream adoption of programmable money systems.

User Experience and Accessibility

The success of programmable money systems ultimately depends on their ability to provide superior user experiences compared to traditional financial services while maintaining the security and autonomy that define these systems. Early DeFi protocols often required significant technical knowledge and cryptocurrency expertise to use effectively, limiting their adoption to sophisticated users who could navigate complex interfaces and understand the risks associated with programmable finance. Modern implementations focus heavily on user experience design that abstracts away technical complexity while preserving user control and transparency.

Wallet integration and user interface design have become critical differentiators for programmable money platforms, with successful projects investing heavily in intuitive interfaces that make complex financial operations accessible to mainstream users. Mobile-first design approaches recognize that many potential users will access these services primarily through smartphones, requiring interfaces optimized for small screens and touch interactions. Progressive web applications and native mobile apps provide seamless experiences that rival traditional banking applications while providing access to programmable financial services.

Educational resources and user support systems play crucial roles in user adoption and retention, as programmable money systems often introduce concepts and risks that are unfamiliar to traditional finance users. Comprehensive documentation, interactive tutorials, and community support forums help users understand how to use these systems effectively while making informed decisions about their financial activities. Some platforms have implemented gamification elements and guided experiences that help users learn about programmable finance through hands-on interaction with simplified versions of their full platforms.

Gas fee optimization and transaction cost management represent significant user experience challenges for blockchain-based programmable money systems, as high transaction costs can make small loans economically unviable and create barriers to accessibility. Layer 2 scaling solutions, gas optimization techniques, and subsidized transaction programs help reduce these costs while maintaining security and decentralization. Some platforms implement batch processing and aggregation techniques that allow multiple users to share transaction costs for common operations.

Cross-platform compatibility and ecosystem integration enable users to access programmable money services through familiar interfaces and existing financial applications. Integration with popular wallets, DeFi aggregators, and traditional fintech applications reduces the friction associated with accessing programmable financial services while expanding the potential user base. API and SDK development enables third-party developers to build applications and services that leverage programmable money infrastructure while providing their own user experiences and value propositions.

Market Impact and Adoption Trends

The growing adoption of programmable money and smart loans is reshaping financial markets by creating new forms of competition for traditional banking services while enabling entirely new categories of financial products and services. Total value locked in decentralized lending protocols has grown exponentially since 2020, demonstrating strong market demand for automated, transparent, and efficient lending services. This growth has been accompanied by increasing institutional interest and adoption, with traditional financial institutions beginning to explore programmable finance technologies and partnerships with DeFi protocols.

Interest rate spreads in programmable lending markets have generally been more favorable to both borrowers and lenders compared to traditional banking, reflecting the reduced overhead costs and increased capital efficiency achievable through automation and disintermediation. These efficiency gains have attracted significant capital from institutional investors seeking higher yields, while also providing better borrowing rates for users who meet collateralization requirements. The competitive pressure from programmable lending has begun to influence traditional bank pricing and service offerings in some markets.

Geographic adoption patterns for programmable money systems reflect both technological infrastructure availability and regulatory environments, with higher adoption rates typically observed in regions with favorable regulatory frameworks and strong cryptocurrency infrastructure. Emerging markets have shown particular interest in programmable finance as an alternative to traditional banking systems that may be less accessible or efficient. Cross-border lending facilitated by programmable systems has enabled new forms of international capital flow that bypass traditional correspondent banking networks.

Integration with traditional finance systems is accelerating as banks and financial institutions recognize the potential benefits of programmable money technologies. Some institutions are developing their own programmable lending systems, while others are partnering with DeFi protocols or providing infrastructure services to support programmable finance adoption. Central bank digital currencies and stablecoins are creating additional bridges between traditional and programmable finance systems, facilitating adoption and reducing technical barriers.

Financial sector performance and fintech adoption metrics demonstrate the broader market impact of programmable money systems, with traditional financial institutions increasingly investing in blockchain technology and automated lending systems to remain competitive. This investment is driving innovation in both traditional and programmable finance sectors while creating new hybrid models that combine the benefits of both approaches.

Market infrastructure development continues to support programmable money adoption through improved scalability, reduced transaction costs, and enhanced security measures. Layer 2 networks, improved consensus mechanisms, and specialized financial infrastructure are reducing the technical barriers to programmable finance adoption while enabling support for larger transaction volumes and more complex financial products.

Future Technological Developments

The trajectory of programmable money evolution points toward increasingly sophisticated systems that incorporate artificial intelligence, quantum-resistant security measures, and seamless integration with both traditional finance and emerging technologies. Machine learning algorithms are becoming more prevalent in interest rate optimization, risk assessment, and fraud detection, enabling programmable systems to continuously improve their performance based on historical data and market conditions. Advanced AI systems may eventually enable fully autonomous financial institutions that can adapt their strategies and products in real-time based on market conditions and user needs.

Quantum computing represents both an opportunity and a threat for programmable money systems, with quantum algorithms potentially enabling more sophisticated financial modeling and optimization while also threatening the cryptographic security that underlies blockchain systems. Quantum-resistant cryptographic techniques are being developed and implemented to ensure that programmable money systems remain secure as quantum computing technology advances. The integration of quantum computing capabilities into financial modeling could enable unprecedented levels of optimization and risk management in programmable systems.

Internet of Things integration could enable programmable money systems to interact directly with physical assets and real-world events, creating new categories of automated financial products. Smart contracts could automatically adjust insurance premiums based on IoT sensor data, execute payments based on delivery confirmations, or modify loan terms based on real-time asset performance monitoring. This integration would bridge the gap between digital financial systems and physical economic activity, creating new opportunities for automation and efficiency.

Virtual and augmented reality technologies may transform how users interact with programmable money systems, providing immersive interfaces for managing complex financial portfolios and understanding the implications of different financial decisions. These technologies could enable visualization of risk scenarios, interactive financial planning tools, and social financial experiences that make programmable finance more accessible and engaging for mainstream users.

Cross-chain and interoperability solutions continue to evolve toward seamless integration between different blockchain networks and traditional financial systems. Advanced bridging protocols, universal settlement layers, and standardized communication protocols could enable programmable money systems to operate across all major blockchain networks while maintaining direct integration with traditional banking infrastructure. This interoperability would significantly expand the addressable market and utility of programmable financial services.

Privacy and Data Protection

Privacy considerations in programmable money systems must balance transparency requirements with user privacy protection, creating unique challenges that don’t exist in traditional financial systems. While blockchain systems provide transparency and auditability that can benefit users and regulators, they also create permanent records of financial activity that could compromise user privacy if not properly managed. Advanced privacy-preserving technologies are being developed to enable programmable money systems that provide necessary transparency while protecting sensitive user information.

Zero-knowledge proof systems enable programmable money platforms to verify user creditworthiness, compliance status, and transaction validity without revealing underlying personal or financial information. These cryptographic techniques allow smart contracts to access necessary data for risk assessment and compliance checking while maintaining user privacy and data security. Implementation of zero-knowledge systems in programmable lending could enable more sophisticated underwriting models while providing stronger privacy protections than traditional banking systems.

Data minimization principles are being incorporated into programmable money system design to ensure that only necessary information is collected and stored, while also providing users with control over their personal data usage. Advanced systems implement privacy-by-design approaches that build data protection directly into their architecture rather than treating privacy as an add-on feature. This approach can provide superior privacy protection while maintaining the operational efficiency and security benefits of programmable finance.

Decentralized identity systems offer potential solutions for privacy-preserving compliance in programmable money systems, enabling users to prove their identity and compliance status without revealing unnecessary personal information. These systems could enable programmable lending platforms to satisfy regulatory requirements while providing users with greater control over their personal data and financial privacy. Integration with existing identity verification systems could enable seamless onboarding while maintaining privacy and security standards.

Privacy-focused cryptocurrency projects and data protection technologies are driving innovation in privacy-preserving financial systems that could be integrated into programmable money platforms. These developments include advanced cryptographic techniques, decentralized data storage systems, and privacy-preserving computation methods that enable sophisticated financial services while protecting user privacy and data security.

Regulatory compliance for privacy protection requires programmable money systems to implement appropriate data protection measures while satisfying financial regulations that may require certain information disclosure. Balancing these requirements involves implementing sophisticated access control systems, audit trails, and selective disclosure mechanisms that can provide regulators with necessary information while protecting general user privacy. This balance is crucial for mainstream adoption of programmable money systems in regulated markets.

Institutional Adoption and Integration

The integration of programmable money systems into institutional finance represents a significant milestone in the maturation of these technologies, with major banks, asset managers, and financial service providers beginning to explore and implement programmable lending solutions. Institutional adoption brings substantial capital, expertise, and credibility to programmable finance while also introducing new requirements for compliance, risk management, and operational standards that influence the development of these systems.

Enterprise implementations of programmable money often require customization and integration with existing institutional infrastructure, including risk management systems, compliance platforms, and reporting tools. These implementations typically involve hybrid architectures that combine programmable finance capabilities with traditional institutional controls and oversight mechanisms. The resulting systems can provide the efficiency and transparency benefits of programmable finance while satisfying institutional requirements for governance, compliance, and risk management.

Custody solutions for institutional programmable finance must meet stringent security and insurance requirements while providing seamless integration with programmable lending protocols and other DeFi services. Qualified custodians are developing specialized services that enable institutional participation in programmable finance while satisfying regulatory requirements and providing appropriate insurance coverage. These custody solutions often implement multi-signature security, hardware security modules, and comprehensive audit trails to meet institutional security standards.

Asset management integration enables traditional investment funds and portfolio managers to access programmable lending markets as an asset class, providing their clients with exposure to the yields and diversification benefits of programmable finance. This integration requires sophisticated risk assessment tools, performance measurement systems, and reporting capabilities that enable institutional investors to evaluate and monitor their programmable finance exposures alongside traditional investments.

Regulatory dialogue between institutions and regulators is helping to establish frameworks for institutional participation in programmable finance, with industry associations and regulatory bodies working together to develop appropriate oversight mechanisms and compliance standards. These efforts are crucial for enabling broader institutional adoption while maintaining appropriate consumer protections and systemic risk management.

Partnership models between traditional institutions and programmable finance protocols are enabling gradual integration and knowledge transfer that benefits both sectors. These partnerships often involve traditional institutions providing capital, compliance expertise, and market access while programmable finance protocols contribute technological innovation, operational efficiency, and new product capabilities. Such collaborations are accelerating the development of hybrid financial systems that combine the best aspects of both traditional and programmable finance.

Global Economic Implications

The widespread adoption of programmable money and smart loans could fundamentally alter global financial systems by reducing the role of traditional banking intermediaries while increasing the efficiency and accessibility of financial services worldwide. This transformation has the potential to democratize access to capital markets, reduce transaction costs, and enable new forms of economic organization that were previously impossible under traditional financial systems. The implications extend beyond individual transactions to encompass monetary policy, financial stability, and international economic relationships.

Monetary policy transmission mechanisms may be significantly affected by the growth of programmable finance, as central bank policy rates may have less direct influence on lending rates determined by algorithmic systems and global capital markets. Central banks are studying how to maintain effective monetary policy control in an environment where significant portions of lending occur through programmable systems that may be less responsive to traditional policy tools. Some central banks are exploring programmable central bank digital currencies that could provide more direct policy transmission channels.

Financial inclusion opportunities created by programmable money systems could enable unprecedented access to financial services for underbanked populations worldwide, as these systems can operate with lower overhead costs and reduced infrastructure requirements compared to traditional banking. Cross-border lending facilitated by programmable systems could provide capital access to emerging markets and underserved regions while enabling more efficient international capital allocation. However, these benefits depend on addressing infrastructure requirements, regulatory frameworks, and user education challenges.

Systemic risk considerations associated with programmable finance adoption include the potential for increased interconnectedness between financial institutions, concentration risks in key infrastructure protocols, and the possibility of cascading failures across automated systems. Regulators and risk managers are working to understand these risks while developing appropriate oversight mechanisms and safety measures to maintain financial stability as programmable finance adoption grows.

Global currency markets and international financial flows could be significantly impacted by programmable money adoption, as these systems enable more efficient cross-border transactions and could reduce the dominance of traditional reserve currencies in international commerce. Programmable money systems could facilitate the development of new international payment systems that are less dependent on traditional banking infrastructure and correspondent relationships.

Economic development implications of programmable finance include the potential for more efficient capital allocation, reduced financial intermediation costs, and new forms of economic organization enabled by programmable contracts and automated governance systems. These changes could accelerate economic development in regions with limited traditional financial infrastructure while creating new challenges for economic policy and regulation in developed markets.

Conclusion and Future Outlook

The emergence of programmable money and smart loans represents a fundamental shift in how financial systems operate, moving from human-mediated processes toward autonomous, algorithmic systems that can provide more efficient, transparent, and accessible financial services. This transformation is still in its early stages, but the rapid growth in adoption, technological sophistication, and institutional interest suggests that programmable finance will play an increasingly important role in global financial systems over the coming decades.

The success of programmable money systems will ultimately depend on their ability to provide superior value propositions compared to traditional financial services while addressing the legitimate concerns of regulators, users, and other stakeholders regarding security, privacy, and systemic risk. Continued innovation in areas such as user experience design, security protocols, regulatory compliance, and economic model optimization will be crucial for achieving mainstream adoption and integration with existing financial infrastructure.

Technological convergence between artificial intelligence, blockchain systems, and traditional finance is accelerating the development of increasingly sophisticated programmable money systems that can adapt to changing market conditions while providing personalized financial services to users worldwide. The integration of these technologies promises to create financial systems that are more efficient, accessible, and responsive to user needs than current alternatives, while also providing new opportunities for innovation and economic development.

The regulatory environment surrounding programmable finance will continue to evolve as regulators develop frameworks for overseeing autonomous financial systems while balancing innovation with consumer protection and systemic stability concerns. Successful navigation of this regulatory landscape will require ongoing collaboration between industry participants, regulators, and other stakeholders to develop appropriate oversight mechanisms that enable innovation while managing risks.

Global adoption patterns suggest that programmable money systems will initially see strongest growth in regions with favorable regulatory environments and strong technological infrastructure, but the benefits of these systems will eventually drive adoption worldwide as technology barriers are reduced and regulatory frameworks mature. The long-term impact of this adoption could include more efficient global capital allocation, increased financial inclusion, and new forms of economic organization that leverage the unique capabilities of programmable financial systems.

Advanced financial modeling and algorithmic trading strategies will continue to play crucial roles in the development and optimization of programmable money systems, as these platforms require sophisticated mathematical models and real-time data analysis to operate effectively. The convergence of financial technology, artificial intelligence, and blockchain systems promises to create unprecedented opportunities for innovation in programmable finance while also requiring new approaches to risk management, compliance, and user protection.

The future of money is increasingly programmable, with smart loans representing just the beginning of what becomes possible when financial systems gain the ability to execute complex logic autonomously while adapting to changing conditions in real-time. As these systems mature and gain broader adoption, they have the potential to create a more efficient, accessible, and innovative global financial system that serves the needs of users worldwide while enabling new forms of economic organization and development that were previously impossible under traditional financial infrastructure.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Cryptocurrency investments and DeFi protocols carry significant risks including potential total loss of funds. Smart contracts may contain bugs or vulnerabilities that could result in financial losses. Interest rates and returns are not guaranteed and may fluctuate significantly. Regulatory frameworks for programmable money and smart loans are still developing and may impact the availability and functionality of these services. Users should conduct thorough research and consider consulting with qualified financial advisors before participating in programmable finance protocols. Past performance does not guarantee future results, and the experimental nature of these technologies means that unforeseen risks may emerge.