Explore real-world asset lending protocols on TradingView

The Evolution of Property-Backed Lending

The convergence of traditional real estate markets with blockchain technology has created unprecedented opportunities for property owners to unlock liquidity through tokenized asset lending protocols. This revolutionary approach to collateralized lending represents a fundamental shift in how real estate value can be accessed and utilized in decentralized finance ecosystems, offering property owners new mechanisms to leverage their assets without traditional banking intermediaries.

Real-world asset tokenization has emerged as one of the most promising applications of blockchain technology, enabling the fractional ownership and trading of physical assets through digital tokens that represent ownership stakes in underlying properties. This technological advancement has opened the door to sophisticated lending protocols that can accept tokenized real estate as collateral, creating entirely new markets for property-backed decentralized finance products.

The traditional real estate lending market has long been characterized by lengthy approval processes, extensive documentation requirements, geographic limitations, and significant intermediary costs that reduce efficiency and accessibility for borrowers. Tokenized property lending protocols address many of these limitations by automating collateral valuation through oracle networks, enabling global participation without geographic restrictions, and reducing counterparty risk through smart contract automation and transparent on-chain operations.

Property tokenization platforms have developed sophisticated frameworks for converting real estate assets into digital tokens that maintain legal compliance while enabling blockchain-based transactions. These platforms typically involve property appraisal by certified professionals, legal structuring through special purpose vehicles or trusts, smart contract deployment for token management, and ongoing compliance monitoring to ensure regulatory adherence across multiple jurisdictions.

Legal Frameworks and Regulatory Compliance

The legal infrastructure supporting tokenized property lending varies significantly across jurisdictions, with different regulatory approaches creating a complex landscape for platforms and borrowers navigating property tokenization and collateralized lending. Understanding these regulatory frameworks is essential for participants in tokenized property markets, as legal compliance directly affects the validity of property tokens as collateral and the enforceability of lending agreements.

Securities regulations play a central role in determining how tokenized property can be structured and traded, with many jurisdictions treating property tokens as securities subject to registration requirements, disclosure obligations, and investor protection measures. The classification of property tokens as securities typically triggers additional compliance requirements including know-your-customer procedures, accredited investor restrictions, and ongoing reporting obligations that can significantly impact platform operations and user accessibility.

Property law considerations add another layer of complexity to tokenized real estate lending, as traditional property rights must be mapped onto blockchain-based ownership structures in ways that maintain legal validity and enforceability. This often requires sophisticated legal engineering involving special purpose vehicles, trust structures, or other intermediary entities that can hold physical property while issuing tokens that represent beneficial ownership interests to token holders.

Cross-border lending transactions involving tokenized property face additional regulatory challenges related to international property law, foreign exchange regulations, and tax implications that vary significantly between jurisdictions. Platforms operating in multiple countries must navigate complex regulatory matrices that can affect everything from token structure to lending terms, creating operational challenges that require sophisticated legal and technical solutions.

The emergence of regulatory sandboxes in various jurisdictions has provided opportunities for tokenized property platforms to operate under relaxed regulatory requirements while demonstrating the viability and safety of their business models. These sandbox programs have generated valuable regulatory data and precedents that are informing the development of more comprehensive regulatory frameworks for tokenized asset markets.

Technology Infrastructure and Smart Contract Architecture

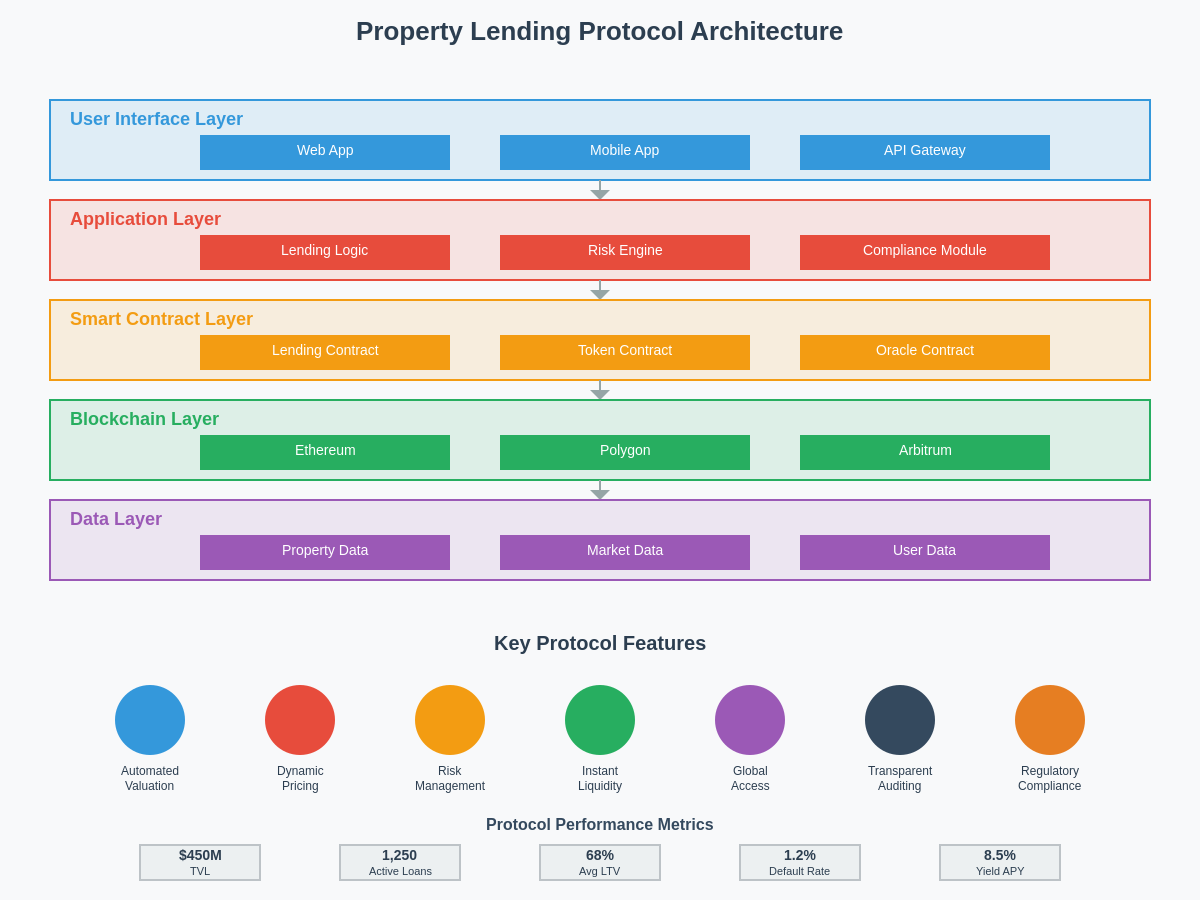

The technical infrastructure supporting tokenized property lending requires sophisticated smart contract architectures that can handle complex property valuation, collateral management, and liquidation processes while maintaining security and regulatory compliance. These systems must integrate multiple data sources including property appraisals, market pricing, legal documentation, and regulatory requirements into automated protocols that can execute lending transactions without human intervention.

Oracle networks play a critical role in tokenized property lending by providing reliable real-world data feeds that enable smart contracts to access property valuations, market conditions, and other relevant information needed for lending decisions. Real-time property market data can be tracked through advanced analytics platforms that integrate traditional real estate metrics with blockchain-based trading data to provide comprehensive market intelligence for lending protocols.

Smart contract security represents a paramount concern for tokenized property lending platforms, as vulnerabilities in contract code can result in significant financial losses for borrowers and lenders alike. Property lending protocols typically employ multiple security measures including formal verification of critical contract functions, multi-signature requirements for administrative operations, time-locked upgrades to prevent malicious modifications, and comprehensive testing procedures that simulate various attack scenarios and edge cases.

Interoperability between different blockchain networks has become increasingly important as tokenized property markets expand across multiple platforms and ecosystems. Cross-chain protocols enable property tokens to be used as collateral on different blockchain networks, expanding liquidity and creating more efficient markets for tokenized real estate lending while introducing additional technical complexity related to cross-chain communication and asset bridging.

The scalability challenges associated with property tokenization require innovative technical solutions that can handle the volume and complexity of real estate transactions while maintaining reasonable transaction costs and processing times. Layer 2 scaling solutions, sidechains, and other scaling technologies are being integrated into property lending platforms to address these challenges while preserving the security and decentralization benefits of blockchain technology.

Valuation Methodologies and Pricing Mechanisms

Accurate valuation of tokenized property represents one of the most challenging aspects of property-backed lending, requiring sophisticated methodologies that can account for real estate market dynamics, property-specific characteristics, regulatory factors, and blockchain-related considerations. Traditional real estate appraisal methods must be adapted for blockchain environments while maintaining accuracy and reliability necessary for sound lending decisions.

Automated valuation models have been developed specifically for tokenized property markets, incorporating machine learning algorithms that can analyze vast datasets including comparable sales, market trends, property characteristics, and economic indicators to generate real-time property valuations. These systems must balance accuracy with automation requirements while providing transparent and auditable valuation processes that can be verified by market participants.

Market-based pricing mechanisms for tokenized property often incorporate multiple data sources including traditional real estate markets, secondary trading of property tokens, and derivatives markets that provide additional price discovery mechanisms. Advanced charting tools help analyze property token price movements and market trends that inform lending decisions and risk management strategies for both borrowers and lenders.

Liquidity considerations play a crucial role in property valuation for lending purposes, as the ability to liquidate collateral in case of default directly affects the risk profile of property-backed loans. Tokenized properties with established trading markets and higher liquidity typically command better loan terms, while unique or illiquid properties may require higher collateralization ratios or additional risk mitigation measures.

The integration of external data sources including economic indicators, local market conditions, regulatory changes, and environmental factors creates comprehensive valuation frameworks that can account for various factors affecting property values. These systems must process and weight multiple data inputs to generate valuations that accurately reflect current market conditions while remaining responsive to rapid changes in property markets.

Collateralization and Risk Management

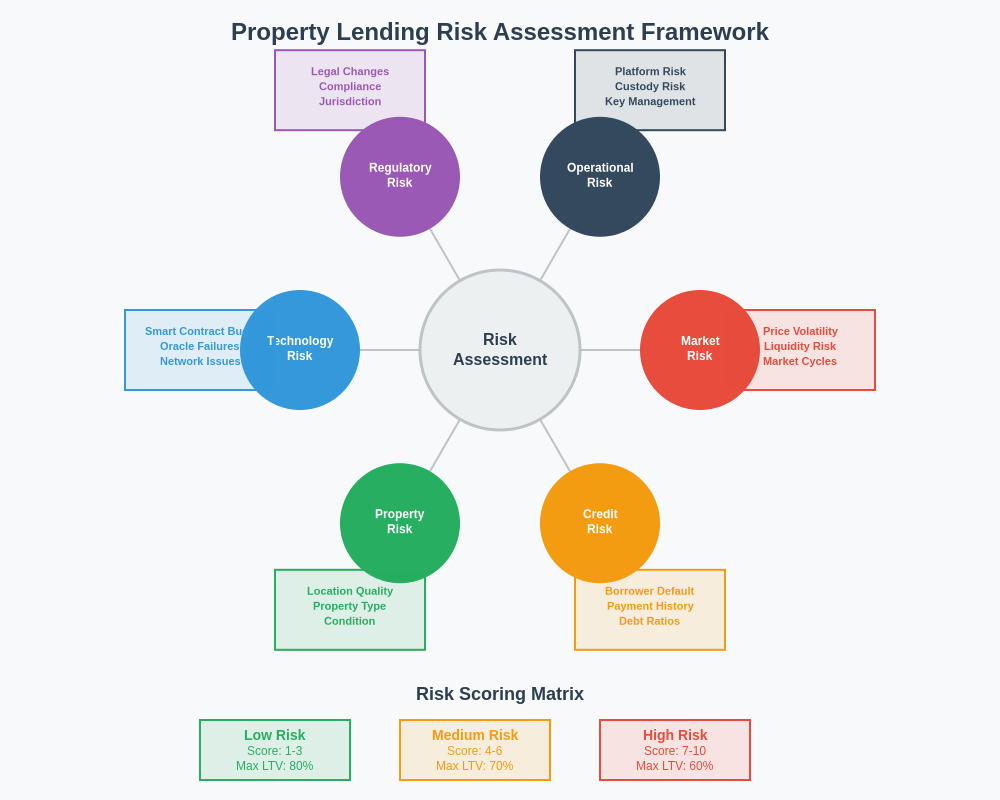

Effective risk management in tokenized property lending requires sophisticated collateralization frameworks that can account for the unique characteristics of real estate assets while providing adequate protection for lenders against default and market volatility. These frameworks must balance borrower accessibility with lender protection while maintaining operational efficiency and regulatory compliance.

Loan-to-value ratios for tokenized property lending typically reflect the illiquid nature of real estate assets and the volatility associated with emerging tokenized asset markets. Conservative LTV ratios help protect lenders against property value declines while providing borrowers with reasonable access to liquidity, though optimal ratios vary significantly based on property type, location, market conditions, and platform risk tolerance.

Dynamic collateralization mechanisms allow loan terms to adjust automatically based on changing property values, market conditions, and borrower circumstances. These systems can trigger margin calls when collateral values decline below predetermined thresholds, automatically adjust interest rates based on risk assessments, or modify loan terms in response to changing market conditions, providing more responsive risk management than traditional static loan structures.

Portfolio diversification strategies for property lending platforms involve spreading risk across multiple properties, geographic regions, property types, and borrower profiles to reduce concentration risk and improve overall portfolio performance. Advanced portfolio management systems can optimize lending allocations to maximize returns while maintaining acceptable risk levels across diverse property portfolios.

Insurance and protection mechanisms for tokenized property lending include traditional property insurance coverage, smart contract insurance against technical failures, and specialized insurance products designed for blockchain-based lending activities. These protection mechanisms help mitigate various risks associated with property ownership and lending while providing additional security for both borrowers and lenders.

Market Participants and Platform Ecosystems

The tokenized property lending ecosystem encompasses a diverse range of participants including property owners seeking liquidity, investors looking for yield opportunities, technology platforms providing infrastructure, service providers offering specialized expertise, and regulatory bodies overseeing market development. Understanding the roles and incentives of these various participants is essential for comprehending how tokenized property markets function and evolve.

Property owners represent the primary borrowers in tokenized property lending markets, seeking to unlock liquidity from their real estate holdings without selling underlying assets. These participants range from individual property owners with single assets to institutional property holders with large portfolios, each bringing different needs, risk profiles, and technological sophistication to tokenized lending platforms.

Institutional investors have emerged as significant participants in tokenized property lending markets, attracted by the potential for diversified exposure to real estate assets through blockchain-based protocols that offer transparency, liquidity, and global accessibility. These institutions often bring significant capital and sophisticated risk management capabilities that enhance market depth and stability.

Technology platforms provide the infrastructure and services necessary for tokenized property lending, including smart contract development, oracle integration, user interfaces, compliance systems, and ongoing platform maintenance. These platforms typically generate revenue through fees charged on lending transactions while competing on factors including security, user experience, regulatory compliance, and market liquidity.

Service providers play crucial roles in tokenized property ecosystems by offering specialized expertise in areas including legal compliance, property appraisal, asset management, insurance, and regulatory affairs. The quality and reliability of these service providers directly affects the success and scalability of tokenized property lending platforms.

Regulatory Evolution and Compliance Challenges

Regulatory frameworks governing tokenized property lending continue to evolve rapidly as authorities worldwide grapple with the implications of blockchain-based real estate markets and develop appropriate oversight mechanisms. These evolving regulations create both opportunities and challenges for platform operators and market participants who must navigate complex and changing compliance requirements.

Financial services regulations increasingly apply to tokenized property lending platforms, subjecting them to licensing requirements, capital adequacy standards, consumer protection measures, and prudential supervision traditionally applied to banks and other financial institutions. These regulatory requirements can significantly impact platform operations and business models while providing important protections for market participants.

Data protection and privacy regulations add another layer of compliance complexity for tokenized property platforms, which must handle sensitive personal and financial information while maintaining the transparency and auditability benefits of blockchain technology. Balancing privacy requirements with blockchain transparency requires sophisticated technical and operational solutions that can protect user data while maintaining platform functionality.

Anti-money laundering and sanctions compliance represent critical areas for tokenized property lending platforms, as real estate has historically been used for money laundering and the global nature of blockchain networks can complicate compliance with various jurisdictional requirements. Platforms must implement comprehensive AML procedures including customer identification, transaction monitoring, and suspicious activity reporting while maintaining efficient user experiences.

The development of specialized regulatory frameworks for tokenized assets represents an ongoing process in many jurisdictions, with regulators working to create balanced approaches that foster innovation while protecting consumers and maintaining financial stability. These emerging frameworks often incorporate elements from existing securities, banking, and real estate regulations while addressing unique characteristics of blockchain-based asset markets.

Economic Impact and Market Development

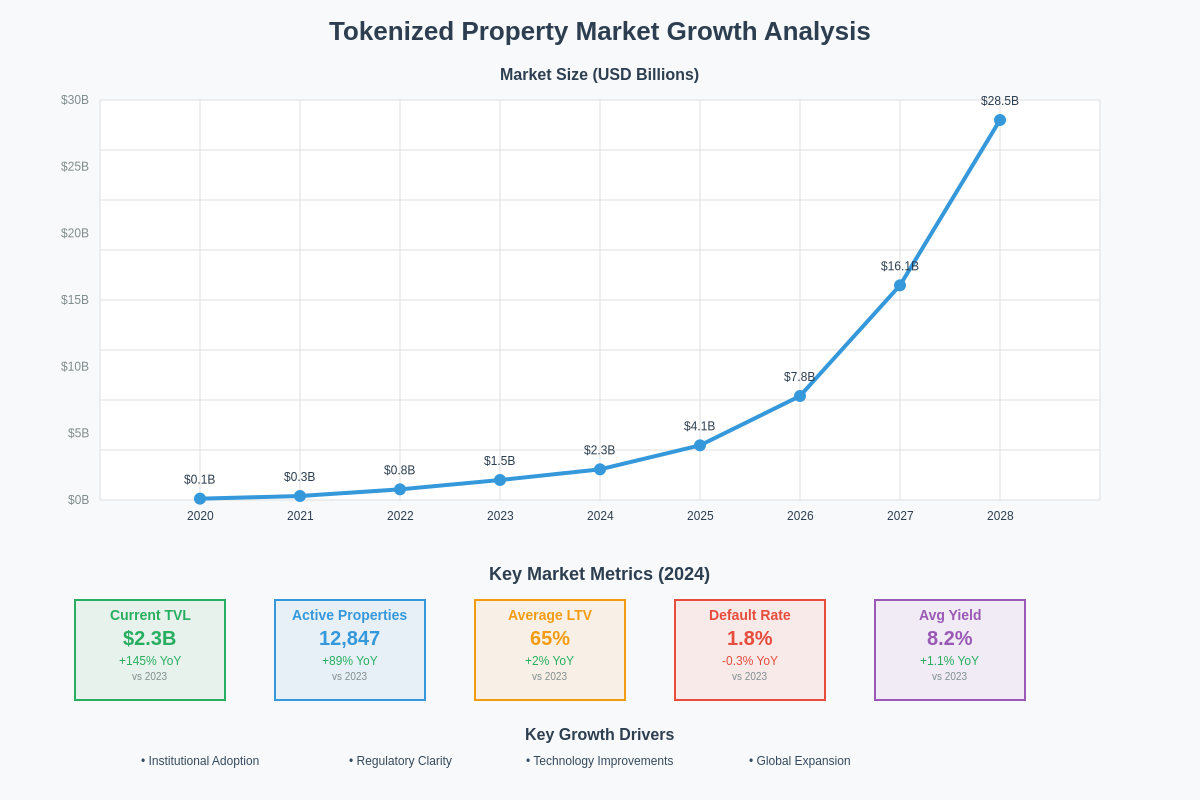

The emergence of tokenized property lending has created new economic opportunities and market dynamics that extend beyond traditional real estate and lending markets, generating value for property owners, investors, and broader economic systems through increased liquidity, efficiency, and accessibility. These economic impacts are reshaping how real estate value is accessed and utilized in modern financial markets.

Liquidity enhancement represents one of the most significant economic benefits of tokenized property lending, enabling property owners to access capital from their real estate holdings without the lengthy processes and high costs associated with traditional real estate transactions. This increased liquidity can stimulate economic activity by freeing up capital for productive investments while allowing property owners to maintain ownership of their underlying assets.

Market efficiency improvements result from the transparency, automation, and global accessibility of tokenized property lending platforms, which can reduce transaction costs, eliminate geographic barriers, and provide more efficient price discovery mechanisms compared to traditional real estate lending markets. Enhanced market data and analytics capabilities enable more informed lending decisions and better risk management across property lending portfolios.

Financial inclusion benefits arise from the accessibility of tokenized property lending platforms, which can provide lending services to property owners who might not qualify for traditional bank loans due to geographic location, credit history, or other factors. These platforms can democratize access to property-backed lending while expanding the pool of available investment opportunities for lenders.

Economic risks associated with tokenized property lending include potential market volatility, technological vulnerabilities, regulatory uncertainty, and the concentration of risk in emerging blockchain-based financial systems. Understanding and managing these risks is essential for sustainable market development and maintaining confidence in tokenized property lending platforms.

Future Developments and Innovation Trends

The future of tokenized property lending is likely to be shaped by continued technological innovation, regulatory development, market maturation, and integration with broader blockchain and traditional financial ecosystems. Several key trends are emerging that could significantly impact how tokenized property lending evolves and expands in coming years.

Artificial intelligence integration into property valuation and lending processes promises to enhance accuracy, efficiency, and responsiveness of tokenized property lending platforms while reducing costs and improving user experiences. Machine learning algorithms can analyze vast datasets to identify market trends, assess risks, and optimize lending parameters in ways that exceed traditional manual processes.

Cross-chain interoperability developments will likely enable tokenized properties to be used as collateral across multiple blockchain networks, creating more liquid and efficient markets while expanding the utility and value of property tokens. These technological advances could significantly increase the accessibility and flexibility of tokenized property lending.

Integration with traditional financial systems represents a major opportunity for tokenized property lending platforms to access larger pools of capital and expand their market reach while providing traditional financial institutions with exposure to blockchain-based real estate markets. This integration could bridge the gap between traditional and decentralized finance while maintaining the benefits of both systems.

Regulatory standardization across jurisdictions could significantly reduce compliance costs and operational complexity for tokenized property lending platforms while providing greater certainty for market participants and facilitating cross-border lending activities. International cooperation on regulatory frameworks could accelerate market development and adoption.

Investment Opportunities and Risk Considerations

Tokenized property lending presents diverse investment opportunities for various types of market participants, from individual property owners seeking liquidity to institutional investors looking for exposure to real estate markets through blockchain-based protocols. Understanding these opportunities and their associated risks is essential for making informed investment decisions in this emerging market sector.

Yield opportunities in tokenized property lending can be attractive compared to traditional fixed-income investments, particularly in low interest rate environments where property-backed loans can provide competitive returns with tangible asset backing. However, these yields must be evaluated against the additional risks associated with blockchain technology, regulatory uncertainty, and market volatility.

Diversification benefits arise from the ability to access geographically diverse property markets through tokenized lending platforms, enabling investors to build exposure to real estate markets that might otherwise be inaccessible due to regulatory barriers, minimum investment requirements, or operational complexity. This global accessibility can enhance portfolio diversification while providing exposure to different economic cycles and market conditions.

Risk factors specific to tokenized property lending include smart contract vulnerabilities, regulatory changes, market volatility, liquidity risks, and the potential for technical failures that could impact platform operations or asset values. Investors must carefully evaluate these risks alongside traditional real estate lending risks when making investment decisions.

Due diligence requirements for tokenized property investments are often more complex than traditional investments, requiring evaluation of underlying property assets, platform technology, regulatory compliance, team expertise, and market conditions. Sophisticated investors typically employ specialized due diligence procedures that account for both traditional real estate factors and blockchain-specific considerations.

Global Market Dynamics and Regional Variations

The development of tokenized property lending markets varies significantly across different regions and jurisdictions, reflecting local regulatory environments, real estate market characteristics, technological infrastructure, and cultural attitudes toward blockchain technology and alternative financial services. Understanding these regional variations is crucial for participants in global tokenized property markets.

North American markets have seen significant development in tokenized property lending, supported by relatively favorable regulatory environments, sophisticated real estate markets, and strong technological infrastructure. However, regulatory complexity at both federal and state levels can create compliance challenges for platform operators and limit accessibility for some market participants.

European markets present both opportunities and challenges for tokenized property lending, with diverse regulatory approaches across different countries creating complex compliance requirements while offering access to large and sophisticated real estate markets. The European Union’s developing regulatory frameworks for digital assets could significantly impact how tokenized property lending evolves in the region.

Asian markets represent significant growth opportunities for tokenized property lending, driven by large real estate markets, increasing blockchain adoption, and growing demand for alternative financial services. However, regulatory uncertainty and varying approaches to blockchain technology across different Asian jurisdictions create challenges for platform operators and investors.

Emerging markets offer unique opportunities for tokenized property lending to address gaps in traditional financial services while providing access to real estate markets that might otherwise be difficult for international investors to access. These markets often present higher risks but also potentially higher returns for sophisticated participants.

Technological Integration and Platform Evolution

The continued evolution of tokenized property lending platforms reflects broader trends in blockchain technology, financial services innovation, and real estate market digitization that are reshaping how property assets are valued, traded, and utilized as financial instruments. These technological developments are creating new possibilities for property owners and investors while addressing existing limitations in traditional real estate finance.

Decentralized autonomous organization structures are being implemented by some tokenized property lending platforms to enable community governance of platform parameters, lending policies, and development priorities. These DAO structures can provide stakeholders with direct influence over platform evolution while creating more transparent and democratic governance mechanisms.

Layer 2 scaling solutions are increasingly being adopted by property lending platforms to address transaction cost and speed limitations associated with main blockchain networks while maintaining security and decentralization benefits. These scaling solutions enable more efficient and cost-effective property lending operations while supporting larger transaction volumes.

Non-fungible token integration is creating new possibilities for representing unique property characteristics and ownership structures within tokenized property lending systems. NFTs can encode detailed property information, legal documents, and ownership history while providing unique identification mechanisms for individual properties and ownership stakes.

Interoperability protocols are enabling tokenized properties to interact with multiple blockchain ecosystems and decentralized finance platforms, expanding the utility and liquidity of property tokens while creating more sophisticated financial products and services built on property-backed assets.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Tokenized property lending involves significant risks including market volatility, regulatory uncertainty, and technology risks. Readers should conduct their own research and consult with qualified professionals before making any investment decisions. The cryptocurrency and blockchain sectors are highly volatile and speculative.

Analyze tokenized asset markets with professional trading tools