Understanding the SEC’s Framework for Cryptocurrency Interest Products

The Securities and Exchange Commission’s approach to regulating cryptocurrency interest-bearing products has evolved into one of the most complex and contentious areas of digital asset oversight, creating a challenging landscape where traditional securities law intersects with innovative financial technologies. As crypto lending platforms, yield farming protocols, and other interest-generating products have proliferated, the SEC has struggled to establish clear regulatory boundaries while protecting investors from potentially fraudulent schemes and unregistered securities offerings. The agency’s enforcement actions against major platforms like BlockFi, Celsius, and others have sent shockwaves through the industry, forcing companies to reassess their business models and comply with regulations that were designed for traditional financial instruments rather than decentralized protocols and digital assets.

The regulatory uncertainty surrounding crypto interest products stems from fundamental questions about how existing securities laws apply to novel financial instruments that operate outside traditional banking and investment frameworks. While some crypto interest products clearly fall under securities regulations, others exist in gray areas where regulatory classification remains unclear, creating compliance challenges for both established companies and emerging DeFi protocols.

The SEC’s enforcement approach has been characterized by a “regulation by enforcement” strategy, where the agency brings legal action against companies rather than providing clear prospective guidance about what activities are permissible under existing law. This approach has created significant uncertainty for market participants while raising questions about due process and the appropriate role of regulatory agencies in shaping industry practices through legal action rather than rulemaking.

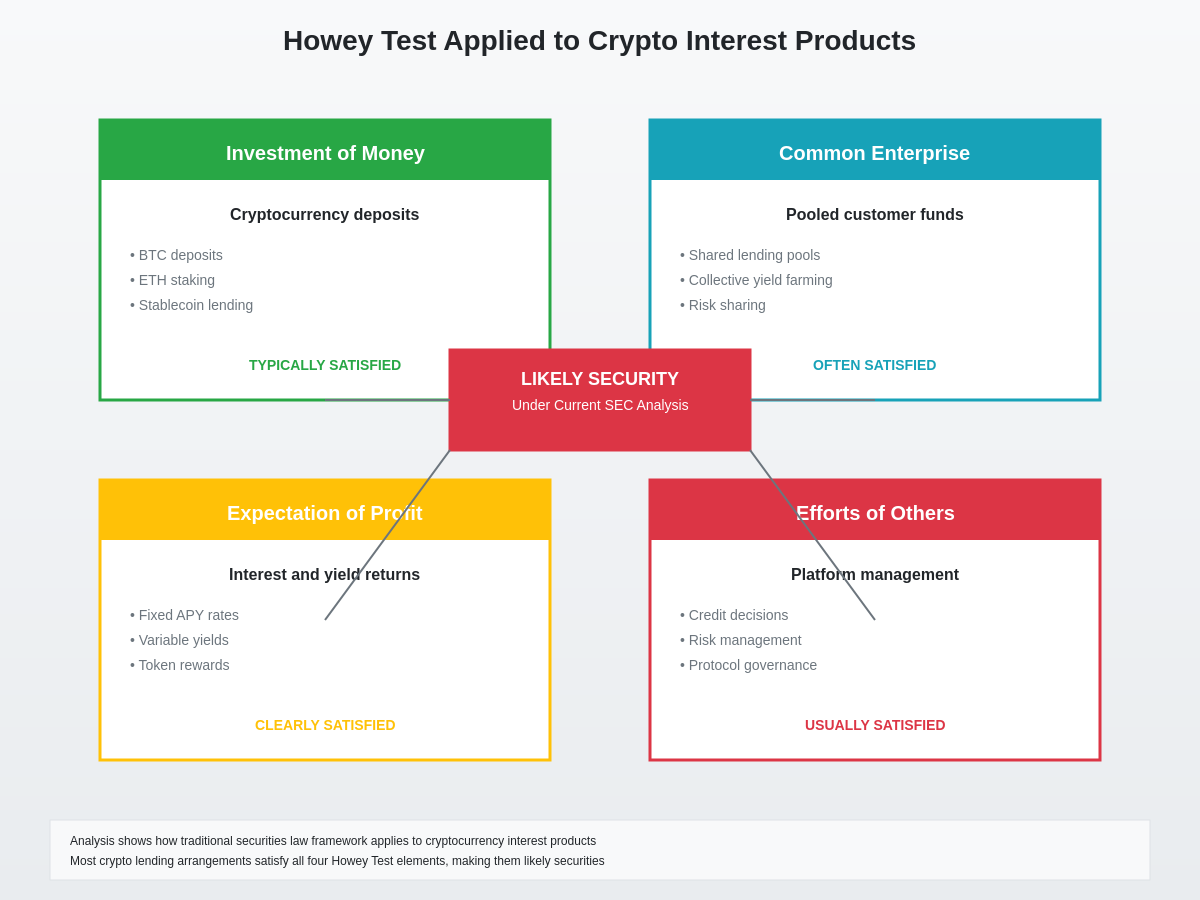

The Howey Test Applied to Crypto Interest Products

The SEC’s analysis of crypto interest products relies heavily on the Howey Test, a legal framework established by the Supreme Court in 1946 to determine whether a financial arrangement constitutes an investment contract and therefore a security subject to federal regulation. Under the Howey Test, an investment contract exists when there is an investment of money in a common enterprise with a reasonable expectation of profit derived from the efforts of others.

When applied to cryptocurrency interest products, each element of the Howey Test presents unique challenges and interpretive questions that have significant implications for regulatory compliance. The “investment of money” prong is generally satisfied when users deposit cryptocurrency or fiat currency into lending platforms, though questions remain about whether deposits of non-monetary crypto assets satisfy this requirement.

The “common enterprise” element has proven particularly contentious in the context of crypto lending platforms, with courts and regulators debating whether pooled lending arrangements, individual loan matching, or algorithm-based yield generation constitute common enterprises under traditional securities law principles. Different platforms structure their operations differently to avoid creating common enterprises, though the SEC has generally taken broad interpretations that encompass most pooled lending activities.

The “expectation of profit” component is typically straightforward for interest-bearing products, as users clearly expect to receive returns on their deposited assets through interest payments, yield farming rewards, or other compensation mechanisms. However, the source and nature of these profits can affect regulatory analysis, particularly when returns come from trading activities, lending to institutional borrowers, or participating in DeFi protocols.

The most complex element involves profits “derived from the efforts of others,” which requires analysis of whether users’ returns depend on the managerial or entrepreneurial efforts of the platform operators rather than the users’ own activities. Traditional lending platforms where operators make credit decisions, manage loan portfolios, and invest user funds typically satisfy this element, while some DeFi protocols attempt to structure operations to minimize reliance on centralized management efforts.

Enforcement Actions and Industry Impact

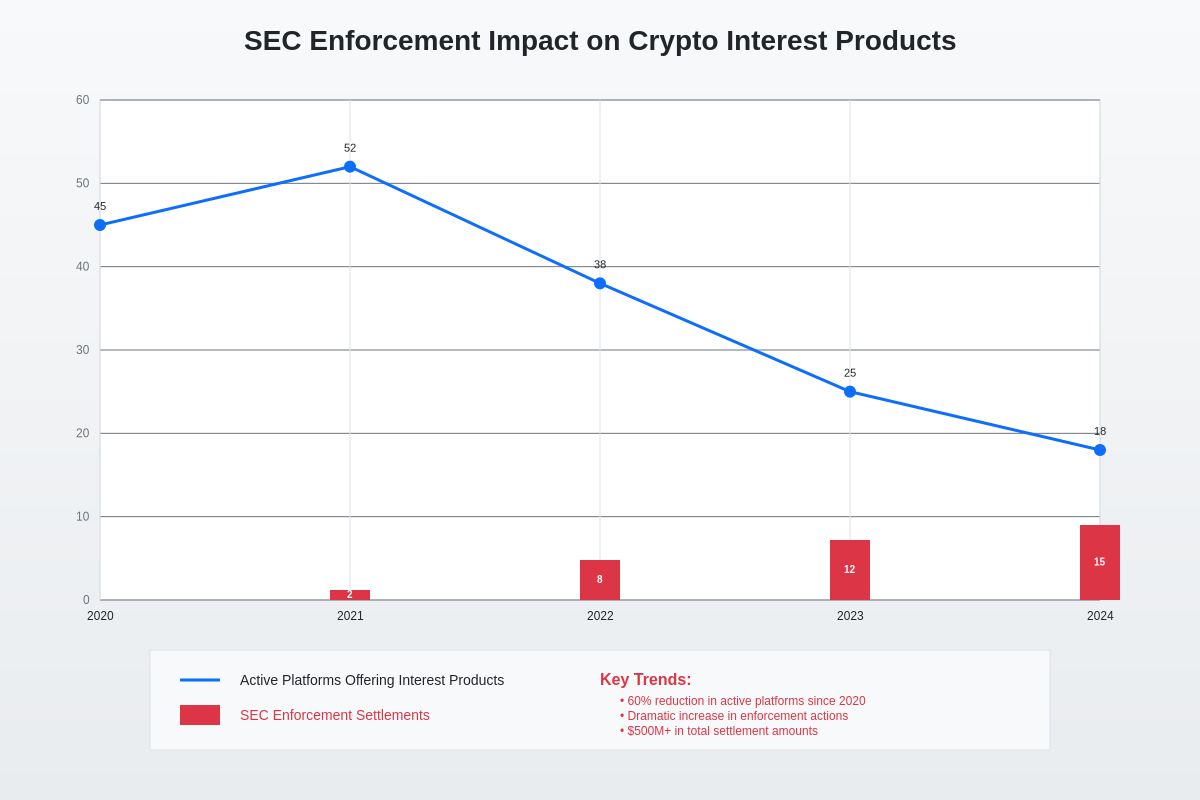

The SEC’s enforcement actions against cryptocurrency interest products have fundamentally reshaped the industry landscape, with high-profile cases against major platforms serving as cautionary tales for other market participants. The agency’s action against BlockFi in 2022 resulted in a $100 million settlement and effectively ended the company’s retail lending product, establishing precedent that many crypto lending arrangements constitute unregistered securities offerings.

The Celsius bankruptcy and related SEC investigations highlighted additional risks associated with crypto interest products, including inadequate disclosure of business models, misrepresentation of risk factors, and potential fraud in marketing materials. The collapse of Celsius revealed that the platform was engaging in high-risk trading activities and making unsecured loans to institutional borrowers while marketing itself as a safe alternative to traditional banking.

These enforcement actions have had cascading effects throughout the cryptocurrency industry, prompting many platforms to cease offering interest products to US customers, restructure their business models, or seek regulatory clarity through engagement with the SEC and other agencies. The uncertainty created by these actions has also chilled innovation in the space, with many entrepreneurs avoiding interest-bearing products altogether rather than risking enforcement action.

The SEC’s approach has drawn criticism from industry participants and legal experts who argue that the agency should provide clearer guidance rather than relying on enforcement actions to establish regulatory boundaries. This criticism has been particularly sharp regarding DeFi protocols, where the decentralized nature of operations may not fit neatly into traditional securities law frameworks designed for centralized enterprises.

Permissible Structures and Compliance Strategies

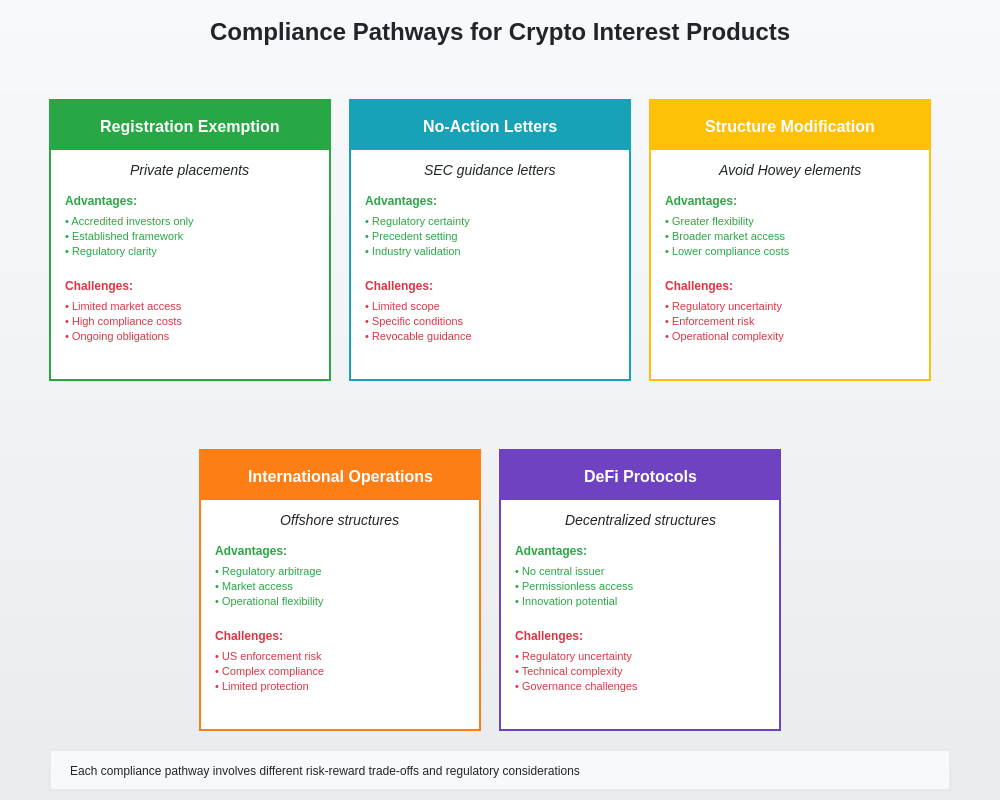

Despite the challenging regulatory environment, certain structures and compliance approaches have emerged as potentially viable paths for offering crypto interest products while minimizing regulatory risk. The key to successful compliance lies in careful structuring of business models, comprehensive legal analysis, and often significant limitations on target markets and product features.

Registered investment advisers and broker-dealers operating under existing SEC oversight have greater latitude to offer crypto interest products, though they must comply with extensive regulatory requirements including capital adequacy rules, customer protection measures, and reporting obligations. These regulated entities can potentially offer crypto lending or yield products as part of broader investment management services, though they must navigate complex custody requirements and operational challenges.

Some platforms have successfully obtained no-action letters or other regulatory guidance by structuring their operations to avoid creating investment contracts under the Howey Test. These structures typically involve eliminating pooling of customer funds, providing customers with direct control over their assets, or structuring arrangements as loans rather than investments.

DeFi protocols present unique challenges and opportunities for regulatory compliance, as truly decentralized systems may not have identifiable issuers or promoters subject to securities regulation. However, many protocols that market themselves as decentralized retain significant centralized control, making them potentially subject to traditional securities law analysis.

International regulatory arbitrage has become common, with many platforms restricting services to US customers while continuing to serve customers in jurisdictions with more permissive regulatory frameworks. However, this approach creates ongoing compliance challenges and may not provide complete protection against SEC enforcement if platforms maintain significant US connections.

State vs Federal Jurisdiction and Regulatory Coordination

The regulatory landscape for crypto interest products is further complicated by overlapping state and federal jurisdiction, with state regulators, federal agencies, and self-regulatory organizations all claiming authority over different aspects of cryptocurrency operations. State money transmitter laws, banking regulations, and securities rules can all apply to crypto interest products, creating complex compliance obligations that vary significantly across jurisdictions.

State securities regulators have been particularly active in investigating and taking enforcement action against crypto interest products, often working in coordination with the SEC but sometimes pursuing independent enforcement theories. The coordination between state and federal regulators can create efficiency gains but also increases the complexity and cost of compliance for industry participants.

Banking regulators including the Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, and Federal Reserve have also asserted jurisdiction over certain crypto interest products, particularly those offered by traditional banks or involving integration with the traditional banking system. These regulators focus on safety and soundness concerns, consumer protection, and systemic risk implications rather than securities law violations.

The Commodity Futures Trading Commission has claimed jurisdiction over certain cryptocurrency derivatives and spot markets, creating additional regulatory complexity for platforms that offer interest products tied to commodity-classified cryptocurrencies like Bitcoin and Ethereum. The CFTC’s approach has generally been more industry-friendly than the SEC’s, though this has created jurisdictional conflicts and regulatory uncertainty.

International Regulatory Approaches and Best Practices

Examining international regulatory approaches provides valuable insight into alternative frameworks for governing crypto interest products while highlighting the challenges and opportunities associated with different regulatory philosophies. European Union regulations under the Markets in Crypto-Assets framework provide a comprehensive regulatory structure that addresses many of the uncertainties present in US law, though implementation remains ongoing.

The United Kingdom has taken a more principles-based approach that emphasizes regulatory clarity while maintaining flexibility for innovation, though recent developments suggest increasing alignment with more restrictive approaches similar to those adopted by US regulators. UK regulators have focused on clear categorization of different crypto activities and proportionate regulatory responses based on risk assessments.

Singapore’s regulatory framework has been particularly influential in demonstrating how clear regulatory guidance can promote innovation while maintaining appropriate consumer protections. The Monetary Authority of Singapore has provided detailed guidance on different types of crypto activities and established clear pathways for regulatory compliance, resulting in a vibrant but well-regulated cryptocurrency industry.

These international approaches demonstrate that regulatory clarity can coexist with innovation and consumer protection, suggesting that the current US approach of regulation by enforcement may not be the only viable path forward. However, differences in legal systems, market structures, and regulatory philosophies mean that international models cannot be directly transplanted to the US context without significant adaptation.

Technology-Specific Considerations and DeFi Protocols

The unique technological characteristics of different cryptocurrency platforms and protocols create additional layers of regulatory complexity that traditional securities law frameworks struggle to address effectively. Smart contract-based lending protocols, automated market makers, and other DeFi innovations operate according to pre-programmed rules that may eliminate traditional concepts of managerial discretion and entrepreneurial effort.

Truly decentralized autonomous organizations present perhaps the greatest challenge to traditional regulatory frameworks, as they may lack identifiable promoters, issuers, or other parties who could be held responsible for securities law compliance. However, the reality is that most purportedly decentralized protocols retain significant elements of centralized control, particularly during development phases and when protocol upgrades are implemented.

The SEC has indicated that the presence of decentralized technology does not automatically exempt projects from securities regulation, focusing instead on the economic realities of arrangements and the presence of investment contract characteristics. This approach has created uncertainty for protocol developers and users who may be unsure about their regulatory obligations and exposure to enforcement action.

Cross-chain protocols and interoperability solutions add additional complexity by potentially involving multiple blockchain networks and jurisdictions simultaneously. These systems may create regulatory obligations in multiple jurisdictions while making compliance monitoring and enforcement more challenging for both operators and regulators.

Consumer Protection and Risk Disclosure Requirements

The SEC’s focus on consumer protection in the crypto interest product space reflects broader concerns about retail investor participation in high-risk and often poorly understood financial products. The agency has emphasized the importance of adequate risk disclosure, particularly regarding the lack of federal deposit insurance, credit risks associated with lending activities, and the potential for total loss of invested funds.

Many enforcement actions have focused on allegedly misleading marketing materials that promoted crypto interest products as safe alternatives to traditional banking while failing to adequately disclose risks. The SEC has been particularly critical of marketing that emphasized returns while downplaying or omitting discussion of how those returns were generated and what risks investors faced.

The collapse of several high-profile crypto lending platforms has validated many of the SEC’s concerns about inadequate risk disclosure and consumer protection measures. These failures have revealed that many platforms were engaging in much riskier activities than disclosed to customers, including making unsecured loans, engaging in proprietary trading, and investing in illiquid assets.

Current regulatory guidance emphasizes the importance of clear, prominent, and comprehensive risk disclosures that explain the specific risks associated with crypto interest products in language that retail investors can understand. However, the effectiveness of disclosure-based regulation in protecting retail investors from complex financial products remains subject to ongoing debate.

Institutional vs Retail Market Considerations

The SEC’s regulatory approach has generally distinguished between institutional and retail markets, with greater regulatory tolerance for crypto interest products offered to sophisticated institutional investors who are presumed to have greater resources for due diligence and risk assessment. However, this distinction has created market segmentation that may limit access to potentially beneficial financial products while raising questions about regulatory fairness.

Qualified institutional buyers and accredited investors face fewer restrictions on access to crypto interest products, though platforms serving these markets still must navigate complex regulatory requirements and potential securities law violations. The institutional market has seen continued growth even as retail products have faced increasing regulatory scrutiny.

The rationale for differential treatment of institutional and retail markets rests on assumptions about sophistication, risk tolerance, and resources for independent analysis that may not always reflect reality. Some institutional investors may lack expertise in cryptocurrency markets, while some retail investors may be highly sophisticated in digital asset technologies and markets.

Market data analysis shows significant differences in risk-return profiles between institutional and retail crypto interest products, with institutional products often offering more conservative approaches but also requiring much larger minimum investments that exclude most retail participants.

Future Regulatory Developments and Legislative Proposals

The regulatory landscape for crypto interest products continues to evolve rapidly, with several potential developments that could significantly alter the current framework. Congressional legislation addressing cryptocurrency regulation has been proposed by multiple committees and could provide much-needed clarity while potentially preempting some SEC enforcement authority.

The SEC’s own rulemaking agenda includes several items that could affect crypto interest products, including proposed rules on custody of digital assets, dealer registration requirements, and expanded definitions of exchange activities. These rules could significantly impact how crypto interest products are structured and offered to US customers.

Industry advocacy groups and trade associations have been actively engaged in lobbying for more favorable regulatory treatment and clearer guidance on permissible activities. These efforts have focused on highlighting the benefits of crypto interest products for innovation, financial inclusion, and competition with traditional financial services.

Judicial developments through ongoing litigation could also significantly impact the regulatory landscape, particularly if courts reject the SEC’s expansive interpretation of securities laws as applied to cryptocurrency activities. Several high-profile cases are working their way through the court system and could establish important precedents for future regulatory analysis.

Economic Impact and Market Development

The regulatory uncertainty surrounding crypto interest products has had significant economic impacts beyond the immediate effects on platform operators and their customers. The restriction of many retail crypto interest products has potentially reduced access to yield-generating opportunities for individual investors while concentrating these opportunities among institutional participants with greater regulatory compliance resources.

The compliance costs associated with offering crypto interest products under current regulatory frameworks have created barriers to entry that may reduce competition and innovation in the space. Smaller platforms and emerging protocols may lack the resources necessary to navigate complex regulatory requirements, potentially leading to market concentration among larger, well-capitalized operators.

Traditional financial institutions have been cautious about entering the crypto interest product market due to regulatory uncertainty, though some have begun offering limited services under existing regulatory frameworks. The entry of traditional financial institutions could bring greater resources and regulatory expertise to the market while potentially legitimizing crypto interest products in the eyes of regulators and consumers.

Market analysis of cryptocurrency lending rates shows that regulatory restrictions have contributed to market fragmentation and potentially reduced efficiency in capital allocation across different cryptocurrency ecosystems.

Risk Management and Best Practices for Market Participants

Market participants seeking to offer crypto interest products must develop comprehensive risk management frameworks that address both traditional financial risks and novel risks specific to cryptocurrency markets. These frameworks must account for regulatory compliance, operational security, credit risk management, and market risk exposure while maintaining competitive business models.

Legal compliance requires ongoing monitoring of regulatory developments, regular review of business practices and marketing materials, and often engagement with regulatory authorities to seek guidance on specific activities. Many successful platforms have invested heavily in legal and compliance infrastructure while maintaining close relationships with regulatory counsel.

Operational risk management for crypto interest products involves securing digital assets, implementing robust internal controls, and maintaining adequate insurance coverage against various types of losses. The technical complexity of cryptocurrency operations creates unique operational risks that traditional financial services compliance frameworks may not adequately address.

Transparency and customer communication have become increasingly important as regulatory scrutiny has intensified, with successful platforms emphasizing clear communication about business models, risk factors, and regulatory status. This transparency can help build customer trust while potentially reducing regulatory enforcement risk.

Technology Integration and Traditional Finance

The integration of crypto interest products with traditional financial services creates opportunities for innovation while introducing additional regulatory complexity that market participants must carefully navigate. Traditional banks offering crypto services must comply with banking regulations in addition to securities laws, creating layered compliance obligations.

Payment system integration allows crypto interest products to interface with traditional banking infrastructure, potentially improving customer experience while creating new regulatory touchpoints. These integrations must comply with Bank Secrecy Act requirements, anti-money laundering regulations, and other traditional financial services rules.

Custody arrangements for crypto interest products often involve third-party custodians who may be subject to additional regulatory requirements under banking or trust company regulations. The choice of custody arrangement can significantly impact the overall regulatory analysis of crypto interest products while affecting operational efficiency and customer protection.

Cross-border transactions and international custody arrangements add further complexity by potentially triggering regulatory requirements in multiple jurisdictions simultaneously. Market participants must carefully structure international operations to minimize regulatory conflicts while maintaining operational efficiency.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. Cryptocurrency regulations are complex and rapidly changing. Readers should consult with qualified legal and financial professionals before making decisions regarding cryptocurrency interest products. The regulatory landscape described in this article may have changed since publication, and readers should verify current regulatory requirements with appropriate authorities.