The decentralized finance ecosystem has experienced explosive growth over the past several years, with total value locked in DeFi protocols surpassing $200 billion at various peaks, representing a fundamental shift in how financial services are delivered and consumed. However, this rapid expansion has been accompanied by significant security challenges, with over $3.8 billion lost to smart contract exploits and protocol failures in 2022 alone, highlighting the critical need for comprehensive insurance solutions that can protect both users and protocols from the inherent risks of automated financial systems. Smart contract insurance has emerged as a crucial infrastructure component for the maturation of DeFi lending protocols, offering protection against code vulnerabilities, economic attacks, and governance failures that could result in catastrophic losses for participants.

The Evolution of Risk in DeFi Lending

DeFi lending protocols represent some of the most sophisticated and complex smart contract systems ever deployed, with platforms like Compound, Aave, and MakerDAO managing billions of dollars in user funds through automated algorithms that determine interest rates, collateral requirements, and liquidation thresholds without human intervention. The complexity of these systems creates multiple attack vectors and failure modes that traditional financial institutions would typically address through comprehensive insurance coverage, regulatory oversight, and risk management frameworks that have been developed over decades of financial market evolution.

The pseudonymous and permissionless nature of DeFi protocols introduces unique challenges for risk assessment and insurance underwriting, as traditional methods for evaluating borrower creditworthiness, protocol operator reliability, and systemic risk factors may not be applicable in decentralized environments where governance is distributed among token holders and operations are executed automatically by smart contract code. Early DeFi lending protocols operated without any form of insurance protection, relying instead on overcollateralization, liquidation mechanisms, and community governance to manage risks, though these measures proved insufficient to prevent major losses when protocols were exploited or experienced unexpected market conditions.

The emergence of flash loan attacks, governance token manipulation, oracle price manipulation, and other sophisticated attack vectors specific to DeFi environments has demonstrated that traditional risk management approaches are inadequate for protecting against the novel threats posed by programmable money and automated financial systems. Flash loan attacks in particular have become a persistent threat to DeFi lending protocols, allowing attackers to manipulate prices, drain liquidity pools, and exploit smart contract vulnerabilities within single transactions that can be executed without requiring significant capital investment from the attacker.

Economic attacks targeting DeFi lending protocols often exploit the interconnected nature of these systems, where vulnerabilities in one protocol can cascade across multiple platforms through shared liquidity pools, common oracle systems, and integrated yield farming strategies that create systemic risk exposure across the entire DeFi ecosystem. The composability that makes DeFi protocols powerful also creates complex dependency chains where failures can propagate rapidly and unpredictably, making it difficult for individual protocols to assess and manage their total risk exposure.

Smart Contract Insurance Mechanisms and Coverage Types

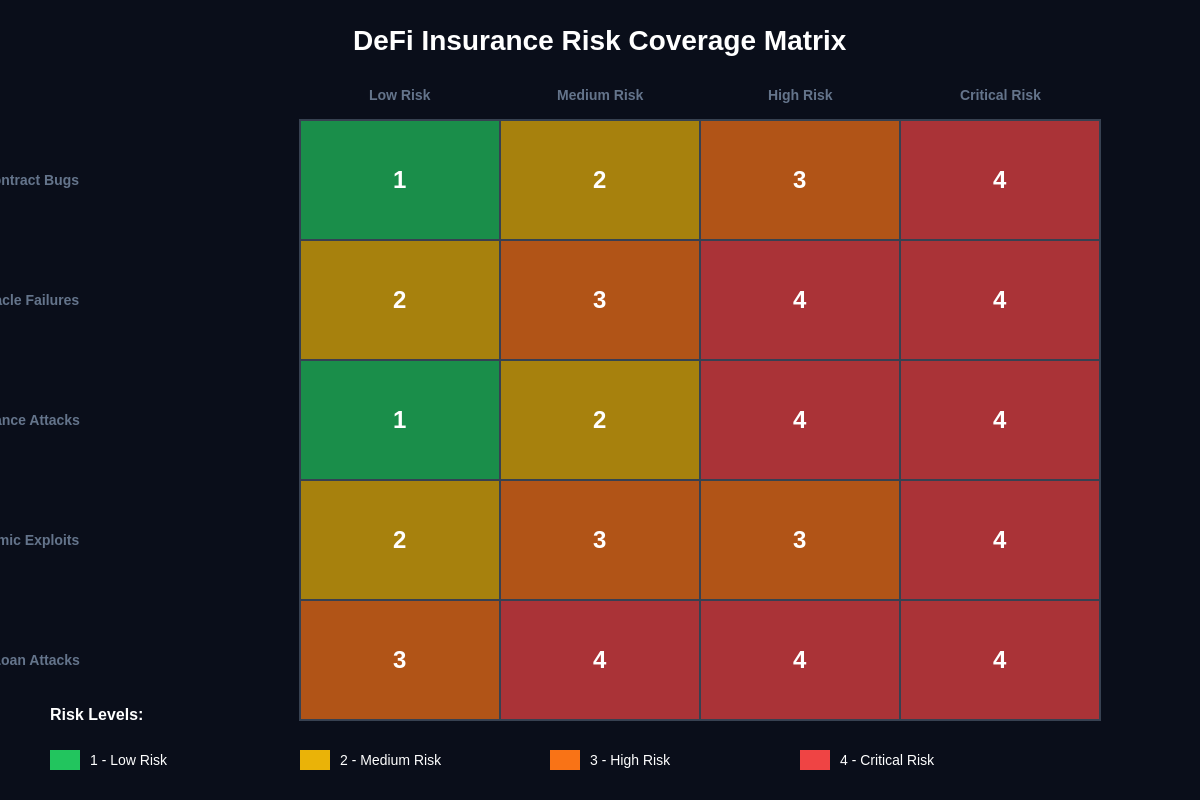

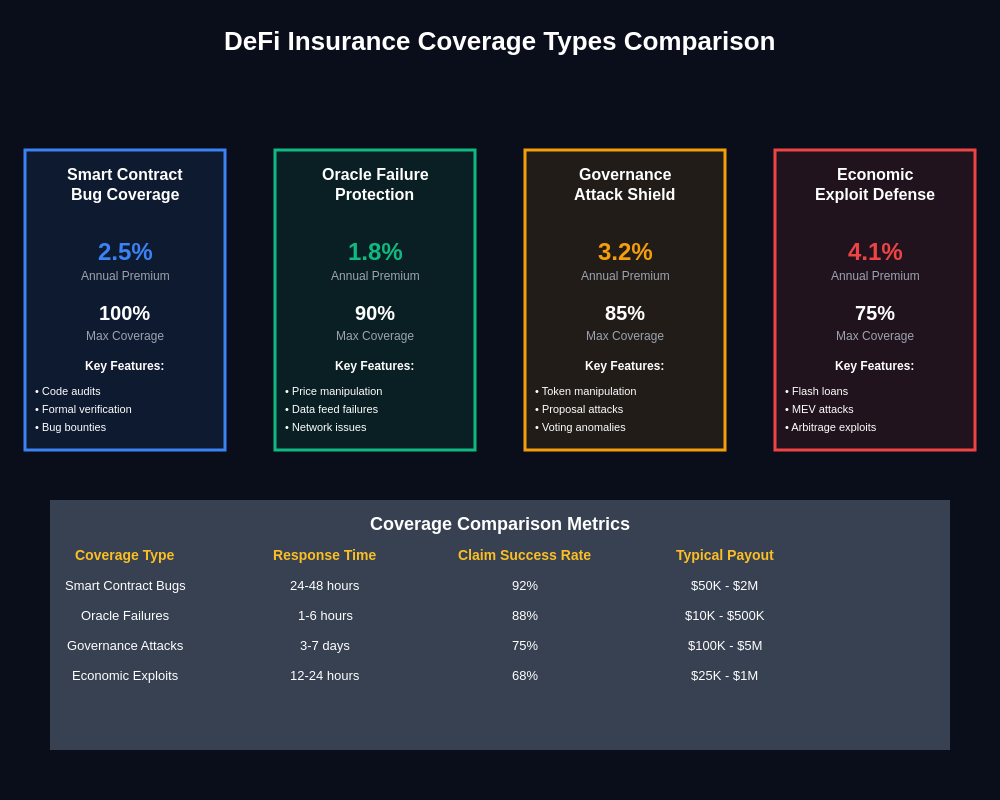

Smart contract insurance for DeFi lending protocols has evolved to address several distinct categories of risk, each requiring different coverage mechanisms, pricing models, and claim assessment procedures that reflect the unique characteristics of decentralized financial systems. Coverage typically includes protection against smart contract bugs and vulnerabilities that could be exploited to drain protocol funds, oracle failures that could trigger incorrect liquidations or enable price manipulation attacks, governance attacks where malicious actors gain control of protocol parameters, and economic attacks that exploit game theory vulnerabilities in protocol incentive structures.

Technical coverage focuses on protecting against code-level vulnerabilities including reentrancy attacks, integer overflow and underflow errors, access control failures, and other programming errors that could be exploited by attackers to withdraw funds improperly or manipulate protocol state in ways that benefit the attacker at the expense of other users. These types of coverage require sophisticated technical analysis capabilities from insurance providers, who must evaluate smart contract code quality, audit history, developer team experience, and deployment procedures to accurately assess risk levels and set appropriate premiums for coverage.

Oracle insurance represents a critical component of DeFi lending protocol coverage, as these systems rely heavily on external price feeds to determine collateral values, liquidation thresholds, and interest rate calculations that directly affect user positions and protocol solvency. Oracle failures can occur through technical malfunctions, data source manipulation, network connectivity issues, or malicious attacks targeting the oracle infrastructure itself, and the consequences of oracle failures can be severe enough to cause widespread liquidations, protocol insolvency, or user fund losses that exceed the value of collateral backing positions.

Governance insurance protects against attacks where malicious actors acquire sufficient governance tokens to propose and implement changes to protocol parameters that benefit themselves at the expense of other users, including modifications to liquidation thresholds, interest rate models, collateral factors, or treasury fund allocations. These attacks can be particularly damaging because they exploit the legitimate governance mechanisms of decentralized protocols, making them difficult to detect and prevent through technical security measures alone.

Economic insurance coverage addresses more subtle attack vectors where protocol incentive structures are exploited through sophisticated strategies that may not involve any code vulnerabilities but still result in value extraction from other protocol participants. These attacks often involve complex multi-step strategies that manipulate market conditions, exploit arbitrage opportunities, or take advantage of information asymmetries to generate profits that reduce returns for other protocol users.

Leading Insurance Protocols and Market Structure

The smart contract insurance market for DeFi lending protocols has developed through several distinct models, with different approaches to risk assessment, premium pricing, claim validation, and coverage provision that reflect the experimental nature of insurance in decentralized environments. Mutual insurance models where protocol users collectively provide coverage for each other have gained traction as they align incentives between coverage providers and coverage purchasers while distributing risks across a broad user base that has direct exposure to protocol performance.

Nexus Mutual emerged as one of the first and most prominent decentralized insurance protocols, operating as a discretionary mutual where members assess claims through a decentralized governance process and provide coverage funding through staking the platform’s native NXM tokens. The mutual model allows for flexible coverage terms and community-driven claim assessment, though it requires significant governance participation from members and can face challenges in scaling coverage capacity and maintaining consistent claim assessment standards across different types of losses.

InsurAce and other competitive insurance platforms have developed alternative models that emphasize automated claim processing, multi-chain coverage capabilities, and professional underwriting services that aim to provide more predictable coverage terms and faster claim resolution processes. These platforms often employ hybrid models that combine decentralized governance with professional insurance expertise to balance the benefits of community participation with the need for technical competence in risk assessment and claim validation.

The parametric insurance model has gained particular attention for DeFi lending protocol coverage, as it allows for automated claim payouts based on objective criteria such as smart contract exploit detection, significant price deviations, or protocol TVL drops that can be verified on-chain without requiring subjective claim assessment processes. Parametric coverage can provide faster claim resolution and reduce disputes over coverage terms, though it may not cover all types of losses and can face challenges in designing parameters that accurately capture all relevant risk scenarios.

Cover protocols that operate as decentralized marketplaces for insurance coverage allow independent underwriters to provide coverage for specific protocols while enabling coverage purchasers to choose from multiple coverage options with different terms, prices, and coverage limits. This marketplace model can improve coverage availability and price discovery while allowing for specialization among underwriters who may have particular expertise in specific types of protocols or risk categories.

Risk Assessment and Pricing Models

Accurate risk assessment represents one of the most challenging aspects of providing smart contract insurance for DeFi lending protocols, as traditional actuarial methods based on historical loss data may not be applicable to novel protocols that have limited operating history and face rapidly evolving threat landscapes. Insurance providers must develop new methodologies that combine technical analysis of smart contract code, economic modeling of protocol incentive structures, and assessment of operational risk factors including development team experience, governance quality, and integration risks with other DeFi protocols.

Technical risk assessment typically involves comprehensive smart contract audits conducted by specialized security firms that evaluate code quality, identify potential vulnerabilities, and assess the effectiveness of security measures implemented by protocol developers. Multiple audit rounds, formal verification processes, and ongoing security monitoring can significantly reduce technical risk levels, though the complexity of modern DeFi protocols means that even extensively audited code may contain subtle vulnerabilities that could be exploited under specific conditions.

Economic risk modeling requires sophisticated analysis of protocol game theory, including evaluation of incentive alignment, attack profitability calculations, and stress testing under various market conditions that could create opportunities for exploitation. Economic attacks often exploit edge cases or unusual market conditions that may not be apparent during normal protocol operation, requiring insurance underwriters to model complex scenarios including extreme price volatility, liquidity crises, and coordinated attacks across multiple protocols.

Governance risk assessment involves evaluation of token distribution, voting mechanisms, proposal processes, and the technical expertise of governance participants to determine the likelihood of malicious governance attacks or well-intentioned but damaging parameter changes. Concentrated token holdings, low voter participation rates, and complex governance mechanisms can increase governance risk levels and require higher insurance premiums to compensate for increased exposure to governance-related losses.

Operational risk factors include assessment of development team experience, deployment procedures, upgrade mechanisms, key management practices, and integration partnerships that could introduce additional risk vectors or single points of failure. Protocols with experienced teams, conservative upgrade practices, and robust operational security measures typically qualify for lower insurance premiums than those with less mature operational practices.

Claims Assessment and Dispute Resolution

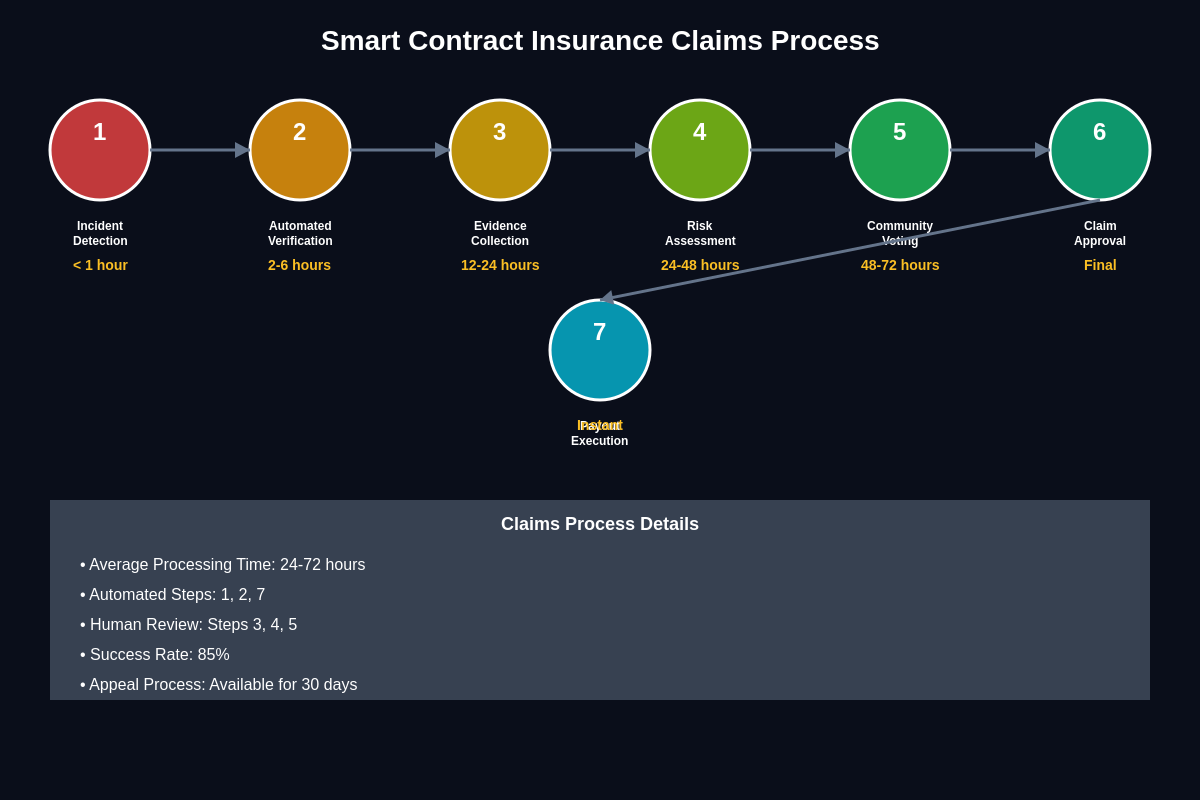

The process of validating and settling insurance claims for DeFi lending protocol losses presents unique challenges that require new approaches to evidence collection, loss verification, and dispute resolution that can operate effectively in decentralized environments where traditional legal frameworks may not apply. Claims assessment must be both technically sophisticated enough to accurately evaluate complex smart contract exploits and accessible enough to allow protocol users to navigate the claims process without requiring extensive technical expertise.

On-chain evidence analysis forms the foundation of most smart contract insurance claims, as blockchain data provides an immutable and transparent record of all protocol interactions, fund movements, and state changes that can be analyzed to determine the cause and extent of losses. Specialized analytics tools and forensic techniques have been developed to trace fund flows, identify attack vectors, and quantify losses with the precision required for insurance claim validation, though the complexity of modern DeFi protocols can make this analysis challenging even for experienced blockchain investigators.

The objective nature of blockchain data enables automated claim processing for certain types of parametric coverage where claims can be triggered automatically when predefined conditions are met, such as smart contract exploit detection, oracle price deviations exceeding specified thresholds, or protocol TVL drops indicating potential fund losses. Automated processing can significantly reduce claim settlement times and eliminate disputes over whether coverage terms have been met, though it requires careful design of trigger conditions to avoid false positives while ensuring legitimate claims are properly covered.

Community-driven claim assessment processes leverage the collective expertise of insurance protocol participants to evaluate complex claims that may not be suitable for automated processing, including disputes over whether losses resulted from covered events, assessments of user negligence or protocol misuse, and evaluation of novel attack vectors that may not have been explicitly covered in insurance terms. These processes typically involve governance token holder voting, expert witness testimony, and structured debate periods that allow for thorough examination of evidence before final claim decisions are made.

Appeal mechanisms and dispute resolution procedures provide additional layers of protection for both coverage purchasers and providers, ensuring that claim decisions can be reviewed and potentially overturned if new evidence emerges or if initial assessments are determined to be flawed. Multi-stage appeal processes with increasing levels of scrutiny can help balance the need for efficient claim processing with the requirement for accurate and fair claim resolution.

Integration with DeFi Lending Protocols

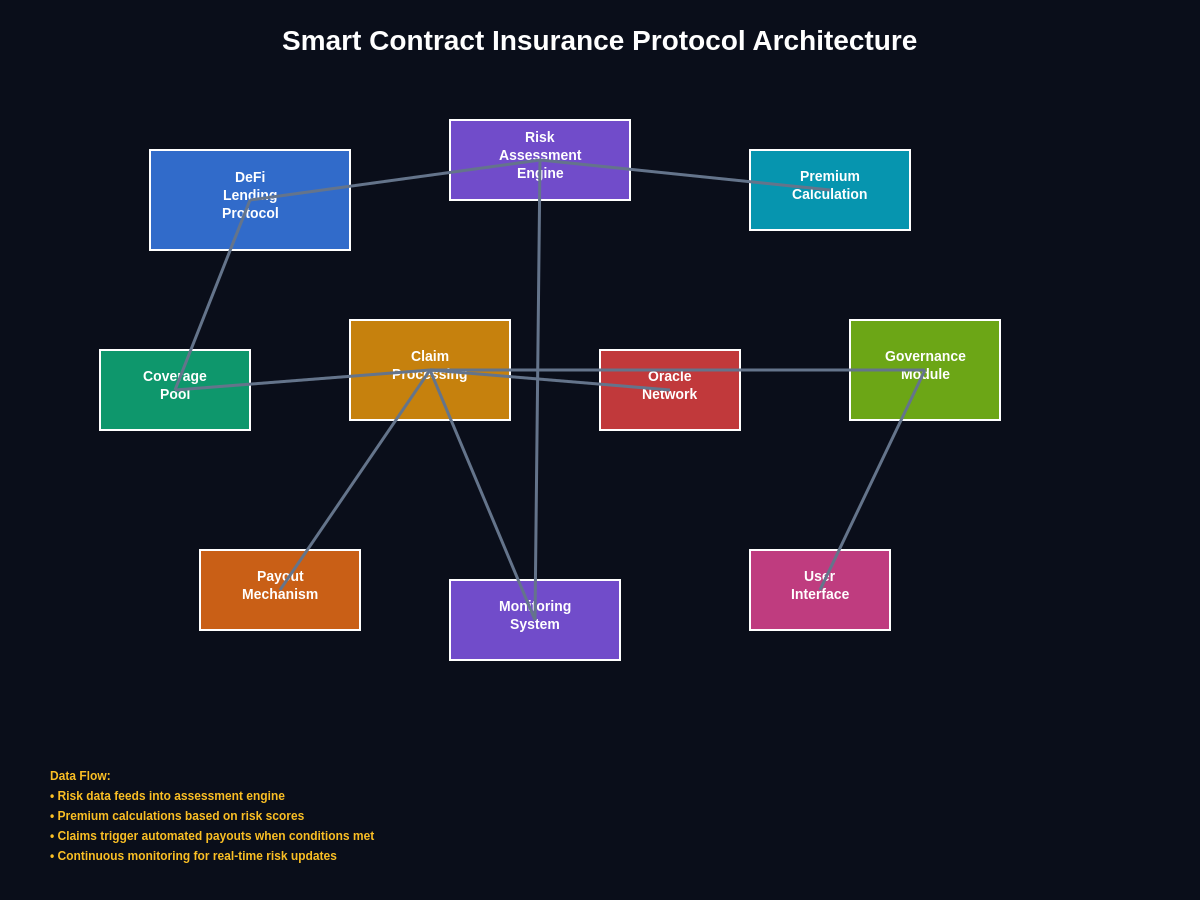

The integration of smart contract insurance with DeFi lending protocols requires careful consideration of user experience, capital efficiency, and system architecture to ensure that insurance coverage enhances rather than complicates the lending and borrowing process. Native insurance integration where coverage is automatically provided as part of protocol participation can significantly improve user adoption by eliminating the need for separate insurance purchases and reducing the complexity of risk management for individual users.

Automatic coverage enrollment systems can be implemented where a percentage of lending yields or borrowing fees is automatically allocated to insurance premiums, providing seamless protection for protocol participants without requiring active insurance management decisions. This approach can improve coverage adoption rates while ensuring that all protocol participants benefit from basic protection against major losses, though it requires careful balance between insurance costs and yield competitiveness compared to uninsured alternatives.

Risk-adjusted pricing models can be integrated directly into lending protocol interest rate calculations, where borrowing costs and lending yields reflect the insurance coverage provided and the assessed risk levels of different assets and market conditions. This integration allows for more accurate risk pricing while ensuring that insurance costs are transparently reflected in protocol economics rather than being hidden as separate fee structures.

Coverage customization options allow advanced users to select specific coverage types, coverage limits, and deductible levels that match their individual risk tolerance and usage patterns, while maintaining default coverage options for users who prefer not to manage insurance details directly. Customizable coverage can improve capital efficiency by allowing users to pay only for protection they actually need while ensuring that casual users receive appropriate default protection.

Cross-protocol coverage coordination becomes increasingly important as DeFi users typically interact with multiple protocols simultaneously through yield farming strategies, lending and borrowing across different platforms, and complex trading strategies that create exposure to risks across the entire DeFi ecosystem. Coordinated coverage approaches can prevent gaps in protection while avoiding duplicate coverage costs that reduce overall yield efficiency for active DeFi participants.

Regulatory Considerations and Compliance

The regulatory landscape for smart contract insurance in DeFi lending protocols remains complex and evolving, with different jurisdictions taking varying approaches to the classification and regulation of decentralized insurance products that operate without traditional insurance company structures or regulatory oversight mechanisms. Regulatory uncertainty can impact insurance provider business models, coverage availability, and compliance requirements that may affect how insurance products are designed and offered to different user populations.

Traditional insurance regulation typically requires licensed insurance companies with specific capital requirements, actuarial oversight, and consumer protection measures that may not be directly applicable to decentralized insurance protocols that operate through smart contracts and community governance rather than corporate structures. Regulatory authorities are developing new frameworks for evaluating decentralized insurance products while balancing innovation encouragement with consumer protection requirements.

Consumer protection considerations include ensuring that insurance terms are clearly disclosed and understood by purchasers, that claim processes are fair and accessible, and that insurance providers maintain sufficient capital reserves to pay claims when they arise. Decentralized insurance protocols must develop mechanisms for providing these protections without traditional regulatory oversight, often through transparent on-chain operations, community governance, and overcollateralized coverage pools.

Cross-border compliance challenges arise when insurance protocols serve users from multiple jurisdictions with different regulatory requirements, licensing regimes, and consumer protection standards. Global accessibility of DeFi protocols complicates compliance efforts while potentially exposing insurance providers to regulatory action in jurisdictions where they may not be properly licensed or compliant with local requirements.

Professional licensing requirements for insurance underwriting, claims assessment, and actuarial services may apply to individuals or organizations involved in operating decentralized insurance protocols, even when these activities are performed through decentralized governance mechanisms rather than traditional employment relationships. These requirements can affect governance participation and protocol operation while potentially limiting the expertise available for protocol development and operation.

Economic Impact and Market Development

The availability of smart contract insurance for DeFi lending protocols has significant implications for market development, user adoption, and capital allocation efficiency within the broader DeFi ecosystem, as insurance coverage can reduce risk premiums required by institutional investors while enabling more aggressive yield optimization strategies for individual users who are protected against major losses. Insurance availability can accelerate DeFi adoption by addressing one of the primary concerns preventing traditional financial institutions and risk-averse investors from participating in decentralized finance markets.

Capital efficiency improvements result from insurance coverage that allows protocols to operate with lower collateralization requirements and more aggressive risk parameters while maintaining appropriate safety margins for user fund protection. Insurance-backed lending can support higher loan-to-value ratios, longer-term lending products, and more sophisticated financial instruments that would be too risky to offer without comprehensive insurance coverage protecting both lenders and borrowers.

Market maturation effects include improved price discovery for risk assessment, standardization of coverage terms and pricing methodologies, and development of professional risk management practices that can support larger scale DeFi operations and institutional adoption. Mature insurance markets provide the risk transfer mechanisms necessary for sophisticated financial institutions to participate in DeFi markets while maintaining compliance with their own risk management requirements and fiduciary responsibilities.

Innovation acceleration occurs when insurance coverage reduces the barriers to experimentation with new DeFi lending protocols and features, allowing developers to test innovative approaches while providing users with protection against potential failures or exploits that might occur during early protocol development phases. Insurance can enable more rapid iteration and feature development by reducing the consequences of early-stage protocol failures.

Systemic risk reduction benefits emerge when comprehensive insurance coverage prevents individual protocol failures from cascading across the broader DeFi ecosystem, as insurance payouts can maintain market confidence and prevent panic-driven liquidations that could affect multiple protocols simultaneously. Insurance coverage can serve as a stabilizing force during market stress periods by ensuring that covered losses do not result in broader market disruption.

Future Developments and Innovation

The future evolution of smart contract insurance for DeFi lending protocols is likely to include significant advances in automated risk assessment, real-time monitoring, and predictive analytics that can identify potential vulnerabilities and attack vectors before they are exploited, enabling proactive risk mitigation rather than reactive claim processing. Machine learning algorithms trained on historical exploit data and smart contract analysis can potentially identify subtle patterns and risk indicators that human auditors might miss.

Cross-chain insurance solutions will become increasingly important as DeFi lending protocols expand across multiple blockchain networks, requiring insurance coverage that can protect against risks specific to different blockchain architectures, bridge protocols, and cross-chain communication mechanisms. Multi-chain coverage coordination will require sophisticated risk modeling that accounts for the unique characteristics and failure modes of different blockchain networks.

Parametric insurance expansion will likely include more sophisticated trigger mechanisms that can automatically detect a wider range of exploit types and loss scenarios, reducing the need for manual claim assessment while ensuring that complex attacks are properly covered. Advanced parametric models might incorporate multiple data sources including on-chain activity, market prices, and protocol health metrics to provide more comprehensive automatic coverage.

Integration with traditional insurance markets may develop as regulatory frameworks mature and traditional insurance companies develop capabilities for underwriting smart contract risks, potentially providing larger coverage limits and more standardized coverage terms while benefiting from traditional insurance expertise in risk assessment and claims management. Hybrid models combining traditional and decentralized insurance approaches could offer the benefits of both systems.

Regulatory standardization efforts are likely to emerge as authorities develop specific frameworks for decentralized insurance products, potentially including licensing requirements, capital adequacy standards, and consumer protection measures adapted for decentralized protocols. Regulatory clarity could facilitate greater institutional participation while ensuring appropriate protections for retail users.

The integration of smart contract insurance with DeFi lending protocols represents a critical infrastructure development that addresses one of the primary barriers to mainstream adoption of decentralized finance. As insurance products become more sophisticated, affordable, and accessible, they will play an increasingly important role in enabling the continued growth and maturation of the DeFi ecosystem while providing users with the confidence and protection necessary to participate in these innovative financial systems. The ongoing development of insurance solutions specifically designed for the unique risks and characteristics of DeFi protocols will be essential for realizing the full potential of decentralized finance as a viable alternative to traditional financial services. Advanced risk modeling and comprehensive coverage options will continue to evolve as the market develops greater understanding of DeFi risk patterns and optimal insurance design principles.

The success of smart contract insurance in DeFi lending protocols will ultimately depend on the ability of insurance providers to accurately assess and price risks while providing coverage that is both comprehensive and affordable for protocol users. As the DeFi ecosystem continues to mature and evolve, insurance solutions must adapt to address new types of risks and attack vectors while maintaining the decentralized principles and permissionless access that make DeFi attractive to users seeking alternatives to traditional financial systems. The development of robust, reliable, and accessible insurance infrastructure will be crucial for enabling the next phase of DeFi growth and institutional adoption.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or insurance advice. Cryptocurrency and DeFi investments carry significant risks, including the potential for total loss of invested capital. Smart contract insurance products are experimental and may not provide complete protection against all types of losses. Users should conduct their own research and consult with qualified professionals before making any investment or insurance decisions. Past performance does not guarantee future results, and the regulatory status of DeFi insurance products may vary by jurisdiction.