Check the latest regulatory updates on TradingView

The Regulatory Foundation of Cryptocurrency Lending

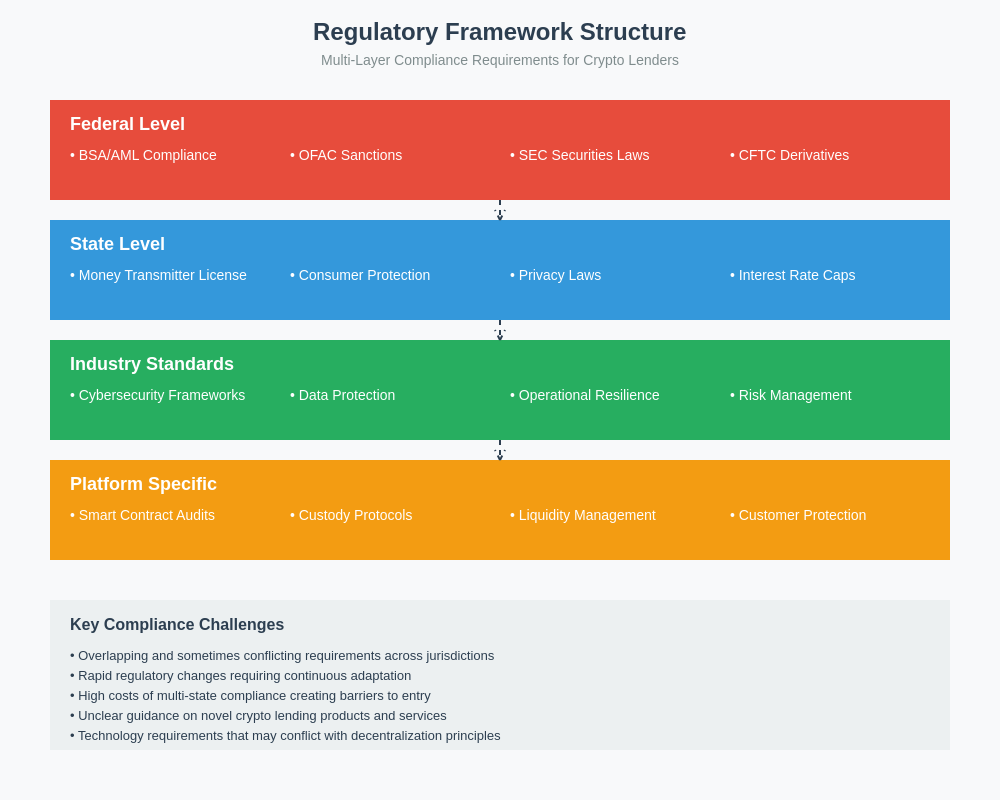

The cryptocurrency lending industry operates within a complex regulatory framework that requires careful navigation of state and federal money transmission laws, with most crypto lending platforms falling under the purview of state money transmitter licensing requirements that vary significantly across jurisdictions. These licensing requirements have become increasingly critical as regulators seek to provide consumer protection while fostering innovation in the digital asset space, creating a patchwork of compliance obligations that crypto lenders must carefully manage to operate legally across multiple states.

The fundamental question of whether cryptocurrency lending activities constitute money transmission has been subject to extensive regulatory interpretation and litigation, with different states adopting varying approaches to classifying these activities under existing money transmitter statutes. The traditional definition of money transmission typically involves the acceptance of currency or monetary value from one person for transmission to another location or person, but the application of this definition to cryptocurrency lending, staking, and yield generation activities presents novel challenges that regulators are still working to address comprehensively.

State banking departments and financial regulatory agencies have increasingly focused on cryptocurrency lending platforms as these services have grown in popularity and market capitalization, recognizing that many crypto lending activities share characteristics with traditional financial services that have long been subject to licensing and oversight requirements. The regulatory attention has intensified following high-profile failures of major crypto lending platforms, highlighting the need for robust consumer protections and regulatory clarity in this rapidly evolving sector.

State-by-State Licensing Requirements

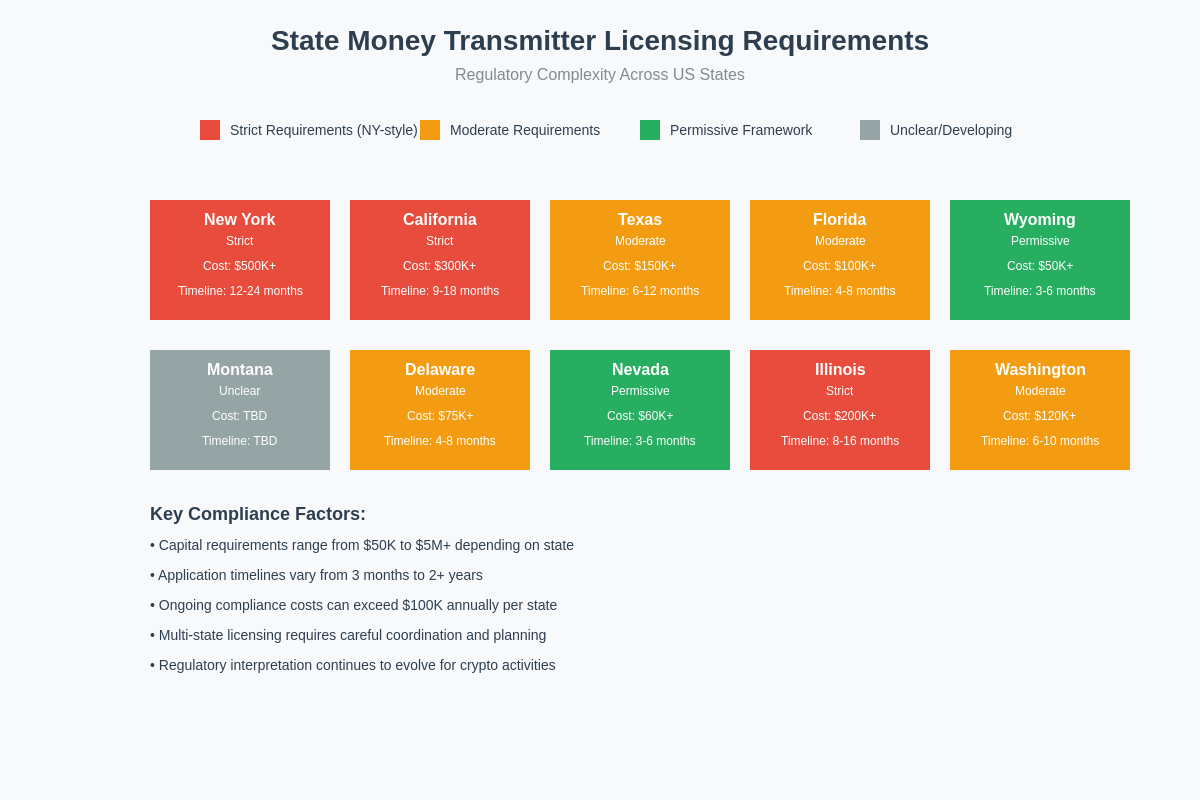

The landscape of state money transmitter licensing for cryptocurrency lending varies dramatically across the United States, with each state maintaining its own regulatory framework, application processes, and ongoing compliance requirements that crypto lending platforms must navigate to operate legally. Understanding these variations is crucial for any crypto lending platform seeking to serve customers across multiple jurisdictions, as the costs, timelines, and requirements can differ substantially between states.

New York’s BitLicense represents one of the most stringent regulatory frameworks for cryptocurrency businesses, requiring crypto lending platforms to obtain a specific license that goes beyond traditional money transmitter requirements and includes detailed cybersecurity, consumer protection, and anti-money laundering provisions. The BitLicense application process is notoriously complex and expensive, often requiring significant legal and compliance investments that can exceed hundreds of thousands of dollars, making it a significant barrier to entry for smaller crypto lending platforms while providing comprehensive regulatory oversight for approved operators.

California’s money transmitter licensing requirements under the California Financial Code require crypto lending platforms to demonstrate substantial capital reserves, maintain detailed records of all transactions, and implement comprehensive compliance programs that address anti-money laundering, know-your-customer, and consumer protection requirements. The California Department of Financial Protection and Innovation has been particularly active in enforcing these requirements against unlicensed cryptocurrency businesses, issuing cease and desist orders and pursuing legal action against non-compliant operators.

Texas has adopted a more permissive approach to cryptocurrency regulation while still requiring money transmitter licenses for certain crypto lending activities, particularly those involving the transmission of virtual currencies on behalf of customers or the conversion between different cryptocurrency types. The Texas Department of Banking has provided guidance indicating that certain decentralized finance activities may fall outside traditional money transmission definitions, though the boundaries remain subject to interpretation and ongoing regulatory development.

Florida’s regulatory approach has evolved significantly in recent years, with state regulators providing clearer guidance on when cryptocurrency lending activities require money transmitter licensing and implementing streamlined application processes for qualified applicants. The Florida Office of Financial Regulation has emphasized the importance of consumer protection while seeking to balance regulatory oversight with innovation in the cryptocurrency sector.

Compliance Requirements and Operational Challenges

Money transmitter licensing compliance for crypto lending platforms involves extensive ongoing obligations that extend far beyond the initial license application, encompassing detailed record-keeping, regular reporting, capital maintenance requirements, and comprehensive risk management programs that must be continuously updated to address evolving regulatory expectations and industry best practices. These compliance requirements create significant operational overhead for crypto lending platforms while providing important consumer protections and regulatory oversight of their activities.

Capital requirements for licensed money transmitters vary significantly by state but typically involve maintaining minimum net worth thresholds, posting surety bonds or other forms of financial security, and demonstrating ongoing financial stability through regular financial reporting and examination processes. For crypto lending platforms, these capital requirements can be particularly challenging given the volatility of cryptocurrency markets and the need to maintain adequate reserves while maximizing returns for lenders and borrowers.

Anti-money laundering and know-your-customer compliance represents one of the most complex aspects of money transmitter licensing for crypto lending platforms, requiring implementation of sophisticated transaction monitoring systems, customer due diligence processes, and suspicious activity reporting mechanisms that must be tailored to the unique characteristics of cryptocurrency transactions. The pseudonymous nature of many cryptocurrency transactions creates additional challenges for compliance teams seeking to identify potentially suspicious activity while maintaining customer privacy and operational efficiency.

Record-keeping requirements for licensed money transmitters typically mandate detailed documentation of all transactions, customer interactions, compliance activities, and operational procedures, with records often required to be maintained for multiple years and made available for regulatory examination upon request. For crypto lending platforms operating across multiple blockchain networks and serving customers in numerous states, these record-keeping requirements can create substantial data management challenges that require sophisticated technology infrastructure and comprehensive data governance policies.

Regular reporting obligations include periodic financial statements, transaction volume reports, compliance certifications, and detailed disclosures about business operations, risk management practices, and material changes to business models or operational procedures. These reporting requirements provide regulators with ongoing visibility into the operations of licensed crypto lending platforms while creating administrative burdens that must be carefully managed to maintain compliance across multiple jurisdictions.

The Application Process and Timeline

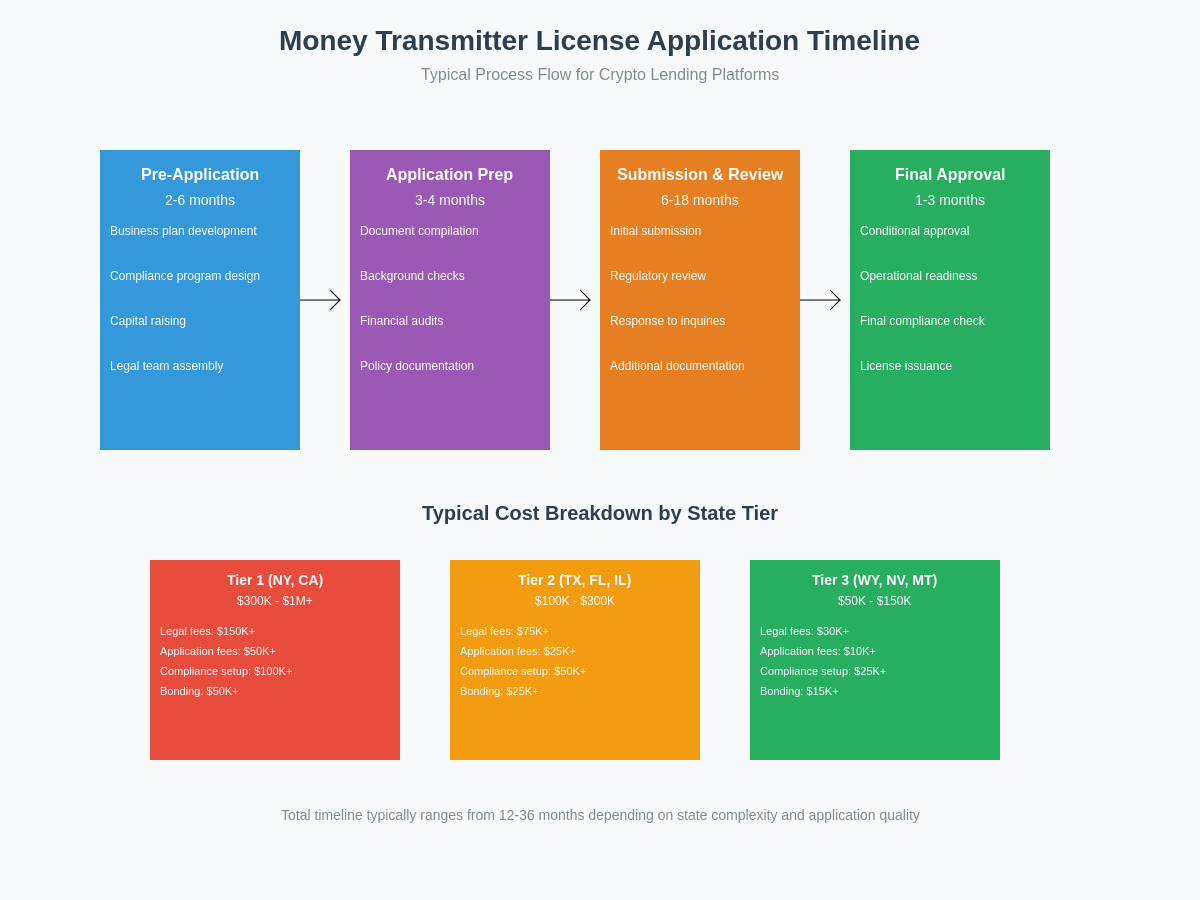

The process of obtaining money transmitter licenses for crypto lending operations typically involves multiple phases spanning several months to over a year, depending on the complexity of the business model, the number of states where licenses are sought, and the responsiveness of applicants to regulatory inquiries and requests for additional information. Understanding the typical timeline and requirements for money transmitter license applications is crucial for crypto lending platforms planning their market entry strategy and compliance budget allocation.

Initial application preparation requires extensive documentation including detailed business plans, financial projections, compliance policies and procedures, organizational charts, background checks for key personnel, and comprehensive risk assessments that address the unique characteristics of cryptocurrency lending activities. The quality and completeness of initial application materials significantly impacts the overall timeline and success rate of the licensing process, making thorough preparation essential for efficient regulatory approval.

State regulatory agencies typically conduct detailed reviews of money transmitter license applications that include examination of financial records, verification of background check results, assessment of proposed compliance programs, and evaluation of the applicant’s operational readiness to conduct money transmission activities in compliance with applicable laws and regulations. This review process often involves multiple rounds of questions and requests for additional information that can extend the timeline significantly if applicants are not prepared to respond promptly and comprehensively.

Many states require personal interviews or presentations by key personnel as part of the money transmitter licensing process, providing regulators with opportunities to assess the competence and integrity of individuals who will be responsible for compliance oversight and operational management. These interviews typically focus on the applicant’s understanding of regulatory requirements, their proposed compliance procedures, and their plans for addressing the unique risks associated with cryptocurrency lending activities.

The final approval phase often includes conditional licensing arrangements that require demonstration of operational readiness, implementation of approved compliance programs, and satisfaction of any outstanding conditions before full licensure is granted. This conditional phase provides regulators with additional oversight during the critical startup period while allowing licensed crypto lending platforms to begin limited operations under regulatory supervision.

Ongoing Compliance and Regulatory Changes

Licensed money transmitters in the cryptocurrency lending space face continuous compliance obligations that require ongoing investment in compliance infrastructure, regular updates to policies and procedures, and proactive monitoring of regulatory developments that may impact their operations. The dynamic nature of cryptocurrency regulation means that compliance requirements are constantly evolving, requiring licensed platforms to maintain flexibility and adaptability in their compliance programs while ensuring continuous adherence to existing requirements.

Regular examination and audit processes conducted by state regulatory agencies provide ongoing oversight of licensed money transmitters while creating opportunities for regulators to assess compliance effectiveness and identify areas for improvement. These examinations typically involve detailed review of transaction records, compliance documentation, risk management practices, and operational procedures, with findings that can result in enforcement actions, additional compliance requirements, or recommendations for operational improvements.

Regulatory reporting obligations continue throughout the life of money transmitter licenses, requiring licensed crypto lending platforms to provide regular updates on their financial condition, transaction volumes, compliance activities, and material changes to their business operations. The frequency and detail of these reporting requirements vary by state but generally increase during periods of regulatory concern or following significant industry events that may impact consumer protection or financial stability.

Staff training and compliance education represent ongoing obligations for licensed money transmitters, requiring regular updates to ensure that personnel understand current regulatory requirements, emerging compliance risks, and best practices for managing cryptocurrency lending activities in compliance with applicable laws. The rapid pace of change in cryptocurrency regulation makes continuous education particularly important for maintaining effective compliance programs and avoiding inadvertent violations of licensing requirements.

Technology infrastructure maintenance and cybersecurity compliance have become increasingly important aspects of ongoing compliance for licensed crypto lending platforms, with regulators placing greater emphasis on data protection, system security, and operational resilience as cryptocurrency businesses face evolving cyber threats and technological challenges. These requirements often necessitate significant ongoing investment in technology infrastructure and security measures that must be balanced against operational efficiency and profitability considerations.

Economic Impact and Market Dynamics

The implementation of comprehensive money transmitter licensing requirements for crypto lending platforms has created significant economic impacts across the cryptocurrency industry, affecting market structure, competition dynamics, and the availability of lending services to consumers in different jurisdictions. Understanding these economic implications is crucial for stakeholders seeking to assess the long-term effects of regulatory compliance requirements on the development and accessibility of cryptocurrency lending services.

Compliance costs associated with obtaining and maintaining money transmitter licenses create substantial barriers to entry for new crypto lending platforms, particularly smaller companies that may lack the financial resources to navigate complex regulatory requirements across multiple states. The high cost of regulatory compliance tends to favor larger, well-funded platforms while potentially limiting innovation and competition from smaller market participants who might otherwise contribute to market diversity and consumer choice.

Geographic market fragmentation has emerged as a significant consequence of state-by-state licensing requirements, with some crypto lending platforms choosing to limit their operations to states with more favorable regulatory environments rather than pursuing comprehensive multi-state licensing strategies. This fragmentation can limit consumer access to crypto lending services and create competitive advantages for platforms willing to invest in comprehensive compliance programs that enable nationwide operations.

The cost of regulatory compliance has been passed on to consumers in various forms, including higher borrowing rates, lower lending yields, increased fees, and more restrictive terms and conditions that reflect the operational overhead associated with maintaining compliance across multiple jurisdictions. These cost increases may reduce the attractiveness of crypto lending services relative to traditional financial products or unregulated alternatives, potentially impacting market growth and adoption rates.

Institutional adoption of crypto lending services has been influenced by the availability of properly licensed and regulated platforms, with many institutional investors and corporate treasury departments requiring their counterparties to maintain appropriate regulatory licenses and comply with established financial services regulations. The availability of licensed crypto lending platforms has therefore become an important factor in the broader institutional adoption of cryptocurrency as an asset class and financial instrument.

Market consolidation trends have been accelerated by regulatory compliance requirements, as smaller platforms struggle with the costs and complexity of multi-state licensing while larger platforms benefit from economies of scale in compliance operations. This consolidation may reduce competition and innovation in the long term while potentially improving the overall stability and regulatory compliance of the crypto lending industry.

International Regulatory Harmonization

The global nature of cryptocurrency markets has created increasing pressure for regulatory harmonization and coordination between different jurisdictions, as crypto lending platforms seek to operate across international borders while regulatory agencies work to address cross-border risks and ensure effective oversight of multinational cryptocurrency businesses. The development of international regulatory standards and coordination mechanisms represents an important trend that may significantly impact the future of crypto lending regulation.

European Union regulatory frameworks under the Markets in Crypto-Assets Regulation provide a comprehensive approach to cryptocurrency regulation that includes specific provisions for crypto lending and asset management activities, creating a potential model for other jurisdictions seeking to develop comprehensive regulatory frameworks for digital assets. The MiCA regulation’s approach to licensing and supervision may influence regulatory development in other regions and create opportunities for regulatory arbitrage as crypto lending platforms evaluate different jurisdictional options.

The Financial Action Task Force recommendations for virtual asset service providers have established international standards for anti-money laundering and counter-terrorism financing compliance that influence domestic regulatory requirements for crypto lending platforms across multiple jurisdictions. These international standards help create consistency in compliance requirements while ensuring that crypto lending platforms meet globally recognized standards for financial crime prevention and detection.

Cross-border regulatory cooperation initiatives have emerged to address the challenges of supervising multinational crypto lending platforms and ensuring effective information sharing between regulatory agencies in different jurisdictions. These cooperation agreements help reduce regulatory fragmentation while providing crypto lending platforms with clearer guidance on compliance requirements for international operations.

The development of regulatory sandboxes and innovation frameworks in various jurisdictions has provided opportunities for crypto lending platforms to test new business models and technologies under relaxed regulatory requirements while working with regulators to develop appropriate oversight mechanisms. These programs help bridge the gap between innovation and regulation while providing valuable experience for both industry participants and regulatory agencies.

Central bank digital currency developments in various countries may significantly impact the regulatory landscape for crypto lending platforms, as the introduction of official digital currencies could change the competitive dynamics and regulatory requirements for private cryptocurrency lending services. The integration of CBDCs with existing financial systems may create new opportunities and challenges for licensed crypto lending platforms seeking to serve both traditional and digital asset markets.

Technology and Compliance Innovation

The intersection of regulatory compliance and technological innovation has created opportunities for crypto lending platforms to develop sophisticated compliance tools and automated systems that can help manage the complexity of multi-state licensing requirements while maintaining operational efficiency and customer service quality. These technological solutions represent an important area of innovation that may help reduce compliance costs and improve regulatory outcomes for the crypto lending industry.

Automated compliance monitoring systems have been developed to track regulatory changes across multiple jurisdictions, alert compliance teams to new requirements, and ensure that operational procedures remain current with evolving regulatory expectations. These systems help reduce the risk of inadvertent compliance violations while minimizing the manual effort required to maintain awareness of regulatory developments across numerous states and jurisdictions.

Real-time transaction monitoring and reporting systems enable licensed crypto lending platforms to maintain comprehensive oversight of their operations while providing regulators with timely access to transaction data and compliance information. These systems help demonstrate ongoing compliance with licensing requirements while providing valuable data for risk management and operational optimization purposes.

Blockchain-based compliance solutions have emerged that leverage the transparency and immutability of distributed ledger technology to create auditable records of compliance activities, transaction histories, and regulatory interactions that can be readily accessed by both internal compliance teams and external regulators. These solutions help reduce the administrative burden of compliance reporting while providing enhanced transparency and accountability in regulatory compliance activities.

Privacy-preserving compliance technologies, including zero-knowledge proofs and selective disclosure mechanisms, enable crypto lending platforms to demonstrate compliance with regulatory requirements while protecting customer privacy and maintaining the confidentiality of sensitive business information. These technologies help balance regulatory transparency requirements with privacy expectations and competitive considerations that are important for maintaining customer trust and market position.

Application programming interfaces and standardized data formats have been developed to facilitate communication between crypto lending platforms and regulatory agencies, streamlining the submission of required reports and enabling more efficient processing of regulatory inquiries and examination requests. These standardization efforts help reduce compliance costs while improving the quality and consistency of regulatory oversight across the industry.

Consumer Protection and Market Integrity

Consumer protection considerations represent a fundamental driver of money transmitter licensing requirements for crypto lending platforms, as regulators seek to ensure that consumers who engage with these services receive appropriate protections against fraud, misrepresentation, operational failures, and other risks associated with cryptocurrency lending activities. The effectiveness of these consumer protection measures has significant implications for the long-term sustainability and public acceptance of crypto lending services.

Disclosure requirements for licensed crypto lending platforms typically mandate clear and comprehensive communication about the risks associated with cryptocurrency lending, including market volatility, counterparty risk, technological risks, and the potential for total loss of invested funds. These disclosure requirements help ensure that consumers make informed decisions about crypto lending participation while providing legal protection for platforms that comply with regulatory communication standards.

Segregation of customer assets represents a critical consumer protection measure that requires licensed money transmitters to maintain clear separation between customer funds and operational assets, ensuring that customer deposits are protected in the event of platform insolvency or operational difficulties. For crypto lending platforms, implementing effective asset segregation can be particularly challenging given the programmable nature of cryptocurrency assets and the complexity of multi-party lending arrangements.

Insurance and bonding requirements for licensed money transmitters provide additional consumer protection by ensuring that platforms maintain financial resources to compensate customers in the event of losses due to operational failures, security breaches, or other covered events. The development of specialized insurance products for crypto lending platforms has been an important innovation that helps bridge the gap between traditional financial services insurance and the unique risks associated with cryptocurrency operations.

Operational resilience and business continuity requirements ensure that licensed crypto lending platforms maintain appropriate backup systems, disaster recovery procedures, and operational redundancy to minimize service disruptions and protect customer assets during adverse events. These requirements are particularly important for crypto lending platforms given their reliance on digital infrastructure and the potential for cyber attacks or technical failures to disrupt operations.

Complaint handling and dispute resolution procedures mandated for licensed money transmitters provide consumers with avenues for addressing problems with crypto lending services while giving platforms opportunities to resolve issues before they escalate to regulatory enforcement actions. The effectiveness of these procedures significantly impacts consumer satisfaction and regulatory relationships for licensed crypto lending platforms.

Future Regulatory Developments

The regulatory landscape for crypto lending continues to evolve rapidly as regulators, industry participants, and other stakeholders work to develop comprehensive frameworks that balance innovation promotion with consumer protection and financial stability considerations. Understanding likely future regulatory developments is crucial for crypto lending platforms planning their long-term compliance strategies and business development initiatives.

Federal regulatory involvement in cryptocurrency oversight has been increasing, with various federal agencies asserting jurisdiction over different aspects of crypto lending activities and working to coordinate regulatory approaches across different regulatory bodies. The potential for comprehensive federal legislation addressing cryptocurrency regulation could significantly impact state money transmitter licensing requirements and create more uniform regulatory standards for crypto lending platforms operating across multiple jurisdictions.

Stablecoin regulation represents a particularly important area of development that could significantly impact crypto lending platforms that rely on stablecoins for lending operations, collateral management, and customer transactions. Proposed federal stablecoin legislation could create new licensing requirements, operational standards, and consumer protection measures that would directly affect the operations and compliance obligations of crypto lending platforms.

Environmental, social, and governance considerations are becoming increasingly important in financial services regulation and may be incorporated into future regulatory requirements for crypto lending platforms, particularly regarding the environmental impact of cryptocurrency mining and transaction processing. These considerations could create additional compliance obligations and operational requirements for licensed crypto lending platforms seeking to maintain regulatory approval and market access.

Cross-border payment regulation and international cooperation initiatives may create new requirements for crypto lending platforms that facilitate international transactions or serve customers in multiple countries, potentially requiring additional licenses, compliance procedures, and reporting obligations that could significantly impact operational complexity and costs for internationally active platforms.

The integration of artificial intelligence and machine learning technologies in compliance and risk management may create new regulatory expectations for technological sophistication and operational capabilities, requiring crypto lending platforms to invest in advanced compliance technologies to maintain competitive positions and regulatory compliance across multiple jurisdictions where they operate.

Monitor crypto lending market developments on TradingView

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. Cryptocurrency lending involves significant risks including the potential for total loss of invested funds. Regulatory requirements for crypto lending platforms vary by jurisdiction and are subject to change. Readers should consult with qualified legal and financial professionals before engaging in cryptocurrency lending activities or making investment decisions. The information contained in this article may not reflect the most current regulatory developments and should not be relied upon as a substitute for professional legal or compliance advice.