The 2025 tax season brings unprecedented complexity for cryptocurrency traders as regulatory frameworks continue to evolve and enforcement mechanisms become increasingly sophisticated. With the Internal Revenue Service implementing enhanced digital asset reporting requirements and new blockchain analysis tools, cryptocurrency investors face a labyrinth of compliance obligations that can result in severe penalties if mishandled. Understanding the intricate web of tax implications, reporting requirements, and strategic planning opportunities has become essential for anyone participating in the digital asset ecosystem.

The Evolving Regulatory Landscape

The cryptocurrency tax environment has undergone dramatic transformation since the early days of digital assets when many traders operated under the assumption that crypto-to-crypto transactions escaped tax scrutiny. The 2024 Infrastructure Investment and Jobs Act implementation has fundamentally altered the reporting landscape, introducing comprehensive broker reporting requirements that will take full effect during the 2025 tax season. Digital asset platforms now face obligations to report customer transactions using Form 1099-DA, creating an unprecedented level of transparency between cryptocurrency activities and tax authorities.

The Treasury Department’s proposed regulations on digital asset transactions have expanded the definition of taxable events to include previously ambiguous activities such as staking rewards, decentralized finance protocol interactions, and non-fungible token transactions. These regulatory clarifications eliminate much of the uncertainty that previously allowed aggressive tax positions, forcing traders to adopt more conservative approaches to compliance. Professional traders monitoring cryptocurrency market movements and tax implications must now integrate tax considerations into their trading strategies from the outset rather than treating taxation as an afterthought.

The Biden administration’s commitment to cryptocurrency enforcement has resulted in significantly increased funding for IRS digital asset compliance programs. The agency has hired specialized agents trained in blockchain analysis and cryptocurrency investigation techniques, while simultaneously partnering with private companies that provide sophisticated transaction tracking software. This enhanced enforcement capability means that the days of unreported cryptocurrency gains going unnoticed are rapidly coming to an end, making proactive compliance essential for all participants in the digital asset space.

Understanding Taxable Events in 2025

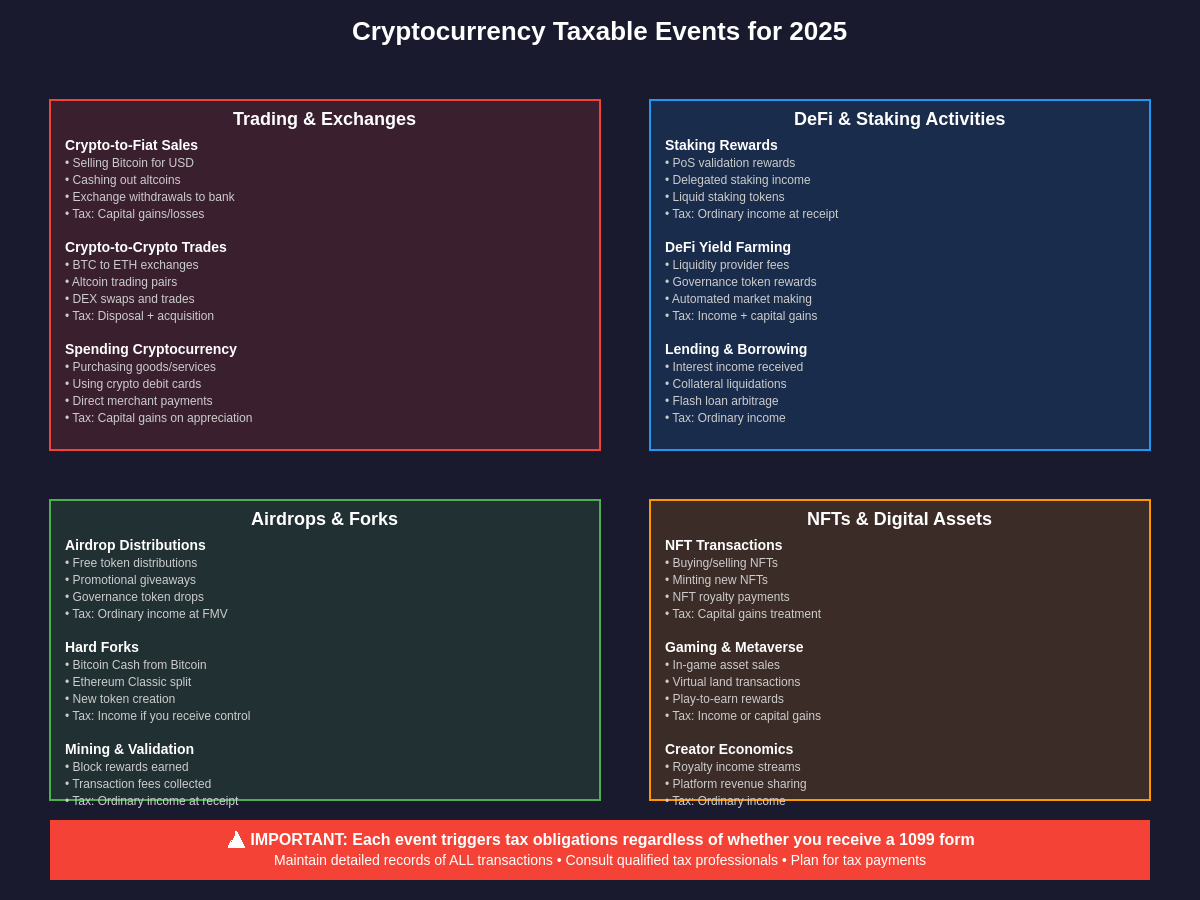

The fundamental principle underlying cryptocurrency taxation remains that digital assets are treated as property rather than currency for federal tax purposes, creating taxable events whenever cryptocurrency is disposed of for consideration. However, the practical application of this principle has become increasingly complex as the cryptocurrency ecosystem has evolved to include sophisticated financial instruments and decentralized protocols that challenge traditional tax concepts.

Trading cryptocurrency for fiat currency represents the most straightforward taxable event, triggering capital gains or losses based on the difference between the asset’s cost basis and its fair market value at the time of disposal. The challenge lies in accurately tracking cost basis across multiple exchanges, wallets, and transaction types, particularly for active traders who engage in frequent transactions across various platforms. Advanced portfolio tracking and analysis tools have become essential for maintaining accurate records and calculating precise tax obligations.

Cryptocurrency-to-cryptocurrency exchanges constitute taxable events that many traders continue to misunderstand, despite years of IRS guidance clarifying this position. Each crypto-to-crypto trade must be treated as a disposal of the original cryptocurrency followed by an acquisition of the new cryptocurrency, requiring fair market value calculations for both assets at the time of exchange. This requirement creates significant complexity for traders who engage in frequent altcoin trading or participate in automated trading strategies that generate hundreds or thousands of transactions annually.

The emergence of decentralized finance has introduced entirely new categories of taxable events that lack clear regulatory precedent. Yield farming activities, liquidity provision to automated market makers, and participation in governance token distributions all create potential tax obligations that must be carefully analyzed based on the specific facts and circumstances of each transaction. The IRS has indicated that future guidance will address these activities more comprehensively, but current participants must navigate these waters using general tax principles and conservative interpretations.

Staking, DeFi, and Advanced Crypto Activities

Proof-of-stake consensus mechanisms have created a new category of income that presents unique challenges for tax compliance. Staking rewards are generally treated as ordinary income at their fair market value when received, requiring validators and delegators to track the precise timing and valuation of each reward distribution. This treatment applies regardless of whether staking rewards are immediately accessible or subject to lock-up periods, creating potential cash flow challenges for taxpayers who owe taxes on illiquid assets.

The complexity increases significantly for participants in liquid staking protocols, where staking rewards may be automatically compounded into derivative tokens that fluctuate in value relative to the underlying staked assets. These protocols often blur the lines between staking rewards and capital appreciation, requiring careful analysis to determine the appropriate tax treatment for each component of returns. Validators using cryptocurrency analysis platforms must track both staking rewards and the performance of their validator operations for accurate tax reporting.

Decentralized finance protocols present perhaps the most complex tax challenges in the cryptocurrency ecosystem, as they often involve multiple simultaneous transactions that must be analyzed individually for tax purposes. Providing liquidity to automated market makers typically involves depositing two different cryptocurrencies and receiving liquidity provider tokens in return, creating multiple taxable events that must be carefully tracked. The subsequent receipt of trading fees and governance token distributions adds additional layers of complexity that require sophisticated tracking systems.

Yield farming strategies that involve moving funds between different protocols to maximize returns can generate extensive transaction histories that become nightmarish to analyze for tax purposes. Each movement between protocols potentially triggers taxable events, while the receipt of governance tokens, airdrops, and farming rewards creates additional income recognition requirements. The temporary loss phenomenon known as impermanent loss adds another dimension of complexity, as these losses may not be deductible until liquidity positions are actually closed.

Record Keeping and Documentation Requirements

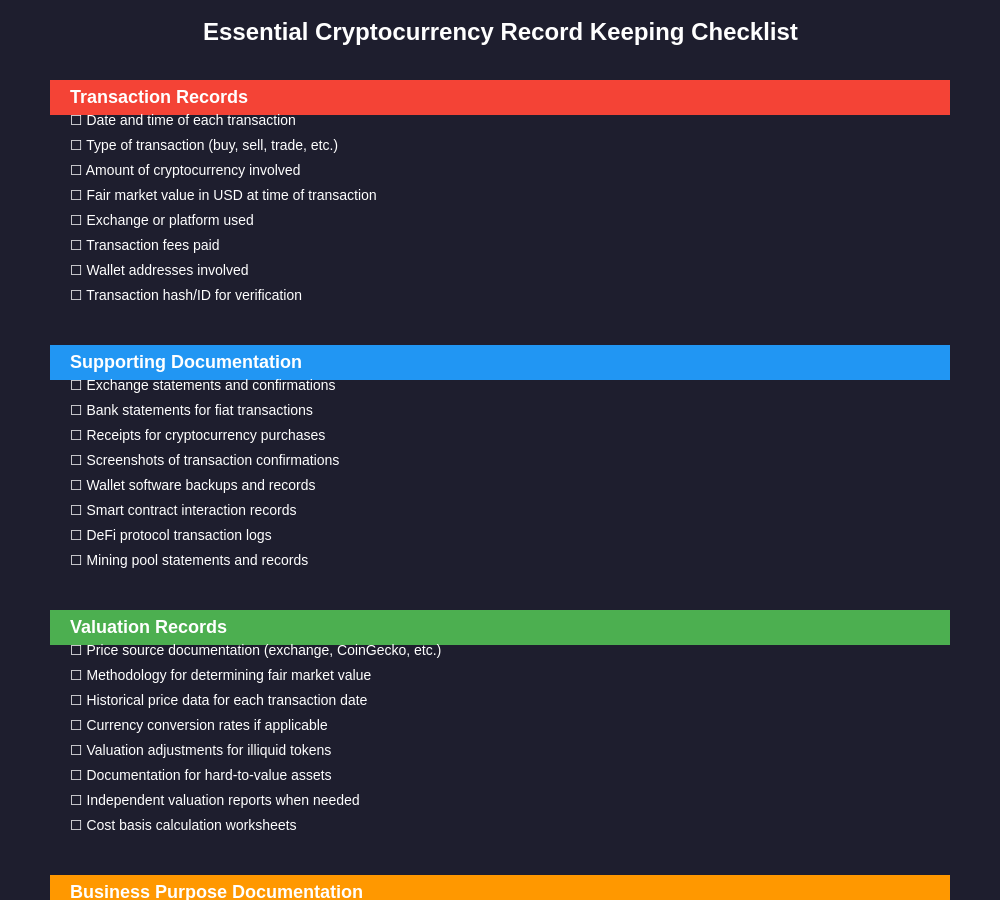

The foundation of successful cryptocurrency tax compliance lies in maintaining comprehensive records that can withstand IRS scrutiny during audits or investigations. The agency has made clear that the burden of proof lies with taxpayers to demonstrate the accuracy of their reported cryptocurrency transactions, making meticulous record keeping essential rather than optional. This requirement extends beyond simple transaction logs to include detailed documentation of the business purpose, fair market value calculations, and supporting evidence for each reported position.

Transaction records must include complete information about each cryptocurrency transaction, including the date, time, counterparties involved, transaction amounts, fair market values in USD, and the business purpose or nature of each transaction. For traders using multiple exchanges or decentralized protocols, this information must be aggregated across all platforms and reconciled to ensure completeness. The complexity of this requirement has driven many serious cryptocurrency participants to invest in specialized tax software or professional services.

Fair market value documentation presents particular challenges in the cryptocurrency space, where prices can vary significantly between different exchanges and pricing sources. Taxpayers must establish consistent methodologies for determining fair market value and maintain documentation supporting these calculations. For less liquid altcoins or newly launched tokens, establishing credible fair market values may require additional analysis and documentation to support reported positions.

The IRS has indicated that blockchain records alone are insufficient for tax compliance purposes, as they typically lack the contextual information necessary to determine the business purpose and tax treatment of transactions. Taxpayers must maintain supplementary records that explain the economic substance of their activities and support their tax positions. This requirement becomes particularly important for complex DeFi activities where the blockchain record may not clearly indicate the nature of the underlying transactions.

Cost Basis Calculation Methods

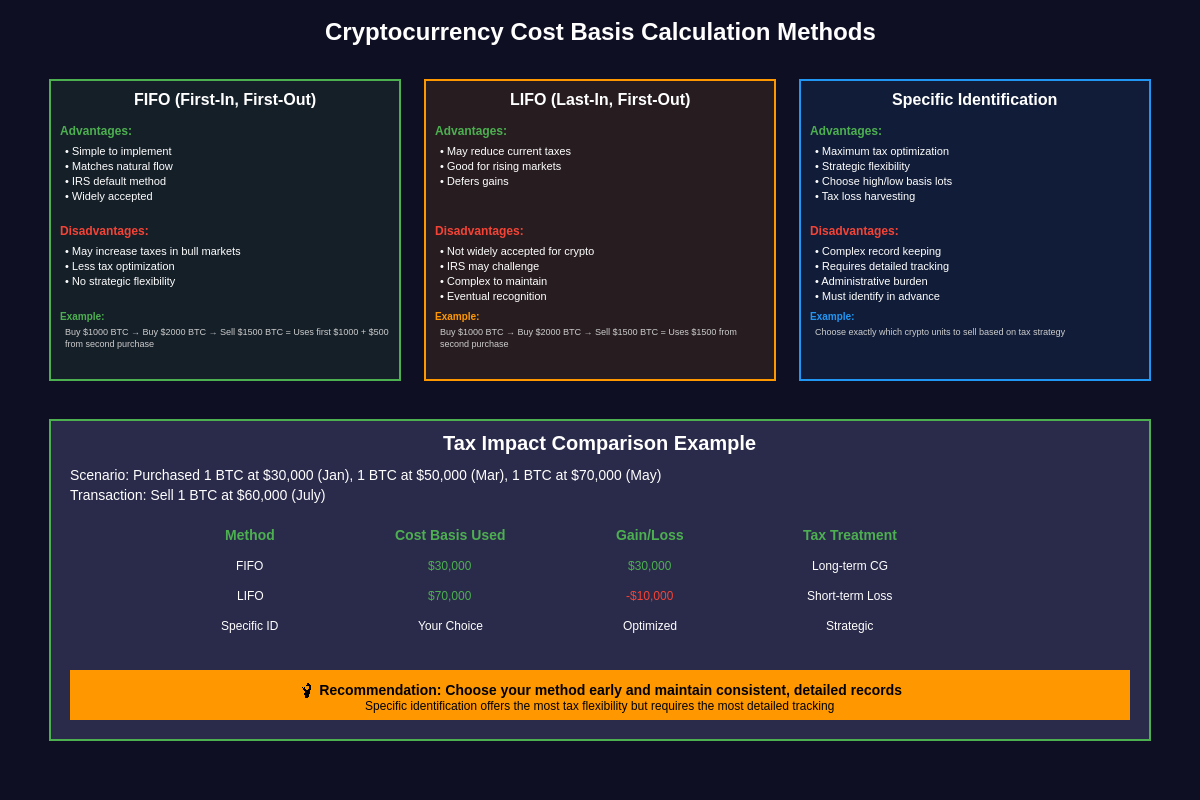

Accurate cost basis calculation forms the cornerstone of cryptocurrency tax compliance, yet it remains one of the most challenging aspects of digital asset taxation due to the fungible nature of most cryptocurrencies and the complexity of tracking individual units through multiple transactions. The IRS has provided limited guidance on acceptable cost basis calculation methods for cryptocurrency, leaving taxpayers to adapt traditional securities accounting methods to the unique characteristics of digital assets.

The specific identification method offers the most flexibility for tax optimization, allowing taxpayers to choose which specific units of cryptocurrency to sell in each transaction. This method requires maintaining detailed records that can track individual cryptocurrency units from acquisition through disposal, enabling strategic tax planning through selective realization of gains and losses. However, the administrative burden of maintaining specific identification records can be substantial for active traders, requiring sophisticated tracking systems and meticulous record keeping.

First-in, first-out accounting represents the default method for most taxpayers and generally aligns with natural trading patterns where older holdings are sold before newer acquisitions. While FIFO simplifies record keeping compared to specific identification, it can result in suboptimal tax outcomes in rising markets where older cryptocurrency holdings may have lower cost bases than recent acquisitions. Traders analyzing market trends and trading strategies should understand how their chosen accounting method impacts their tax optimization opportunities.

The average cost method, while commonly used for mutual fund investments, presents unique challenges in the cryptocurrency context due to the need to maintain separate average cost calculations for each type of cryptocurrency held. This method can simplify calculations for taxpayers who make frequent purchases of the same cryptocurrency but becomes complex when dealing with multiple digital assets or sophisticated trading strategies that involve frequent rebalancing between different cryptocurrencies.

State Tax Considerations

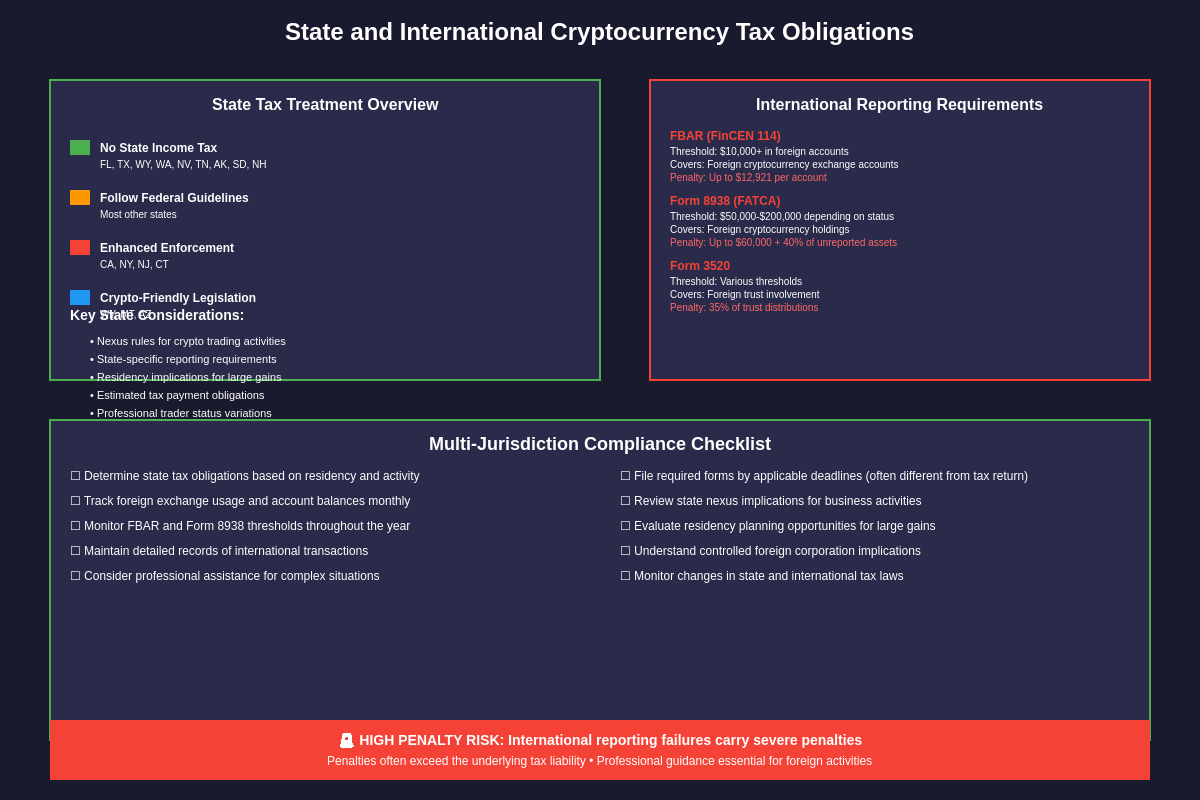

State taxation of cryptocurrency adds another layer of complexity to an already challenging compliance environment, as states have adopted widely varying approaches to digital asset taxation that often conflict with federal treatment. While most states generally follow federal tax principles for cryptocurrency transactions, significant differences exist in areas such as income recognition, deduction allowances, and reporting requirements that can dramatically impact overall tax liability.

States like California and New York have implemented aggressive enforcement programs specifically targeting cryptocurrency transactions, often exceeding federal requirements in their scope and complexity. California’s Franchise Tax Board has developed sophisticated blockchain analysis capabilities and regularly conducts audits of cryptocurrency traders, while New York’s Department of Taxation and Finance has issued detailed guidance that clarifies state-specific requirements for digital asset reporting. These states often impose additional documentation requirements and may challenge positions that are acceptable at the federal level.

Conversely, states like Wyoming, Texas, and Florida have adopted more favorable approaches to cryptocurrency taxation, with some implementing explicit protections for digital asset activities or providing clarifications that reduce compliance burdens. The emergence of state-level cryptocurrency havens has created opportunities for tax planning through strategic residency planning, though such strategies must be implemented carefully to avoid challenges from former states of residence.

The question of state nexus for cryptocurrency activities has become increasingly important as states expand their definitions of taxable activity to include digital asset transactions. Traders who operate across multiple states or use exchanges located in different jurisdictions may face complex sourcing questions that require careful analysis to ensure compliance with all applicable state tax obligations.

International Reporting Requirements

The global nature of cryptocurrency markets and the borderless operation of many digital asset platforms create significant international tax reporting obligations that many US taxpayers overlook to their peril. The Foreign Bank Account Report and Form 8938 requirements can apply to cryptocurrency holdings stored on foreign exchanges or in foreign custody arrangements, creating substantial penalties for non-compliance that often exceed the underlying tax liability.

The FBAR filing requirement applies when the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year, including cryptocurrency holdings on foreign exchanges that meet the definition of foreign financial accounts. The challenge lies in determining which cryptocurrency platforms constitute foreign financial accounts, as the regulations were written before the emergence of digital assets and do not clearly address modern cryptocurrency custody arrangements.

Form 8938 reporting requirements operate in parallel with FBAR obligations but use different thresholds and definitions that can create confusion for taxpayers attempting to determine their compliance obligations. The specified foreign financial asset reporting requirements can apply to cryptocurrency holdings even when FBAR filing is not required, creating potential trap for unwary taxpayers who assume that domestic cryptocurrency activity exempts them from international reporting obligations.

The intersection of cryptocurrency activities with controlled foreign corporation and passive foreign investment company rules creates additional complexity for US taxpayers who own interests in foreign cryptocurrency businesses or investment vehicles. These rules can result in current income inclusion and punitive tax treatment that dramatically exceeds the tax burden associated with domestic cryptocurrency investments.

Professional Tax Planning Strategies

Strategic tax planning for cryptocurrency activities requires a sophisticated understanding of both traditional tax principles and the unique characteristics of digital assets, enabling taxpayers to optimize their tax positions while maintaining full compliance with applicable regulations. The volatile nature of cryptocurrency markets creates both challenges and opportunities for tax planning that require careful timing and execution to achieve optimal results.

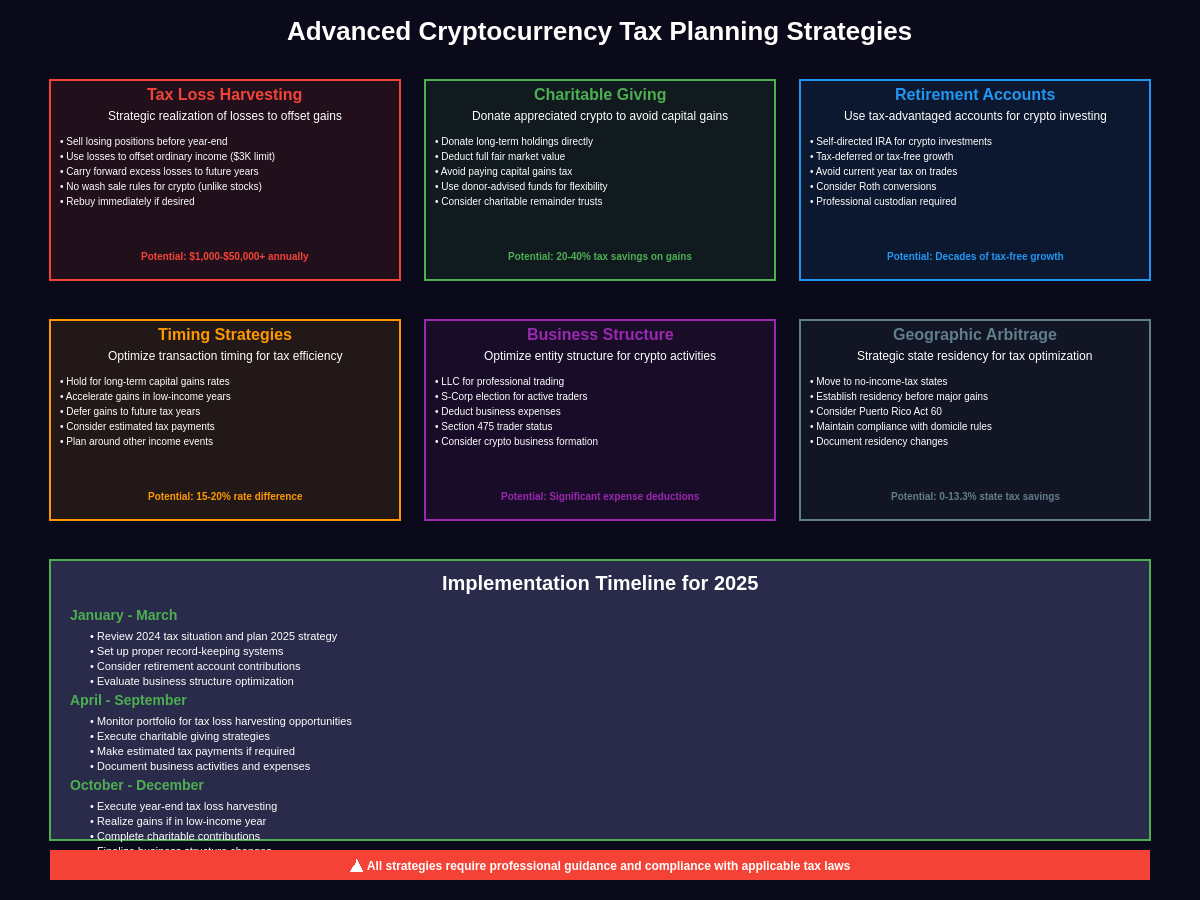

Tax loss harvesting represents one of the most accessible tax planning strategies for cryptocurrency investors, allowing the strategic realization of losses to offset gains and reduce overall tax liability. Unlike securities investments, cryptocurrency transactions are not subject to wash sale rules, enabling more aggressive loss harvesting strategies that can generate significant tax savings. However, effective loss harvesting requires careful coordination with overall investment objectives to avoid compromising long-term portfolio performance for short-term tax benefits.

The charitable contribution of appreciated cryptocurrency can provide substantial tax benefits for philanthropically inclined taxpayers, allowing the deduction of fair market value while avoiding the recognition of capital gains. This strategy becomes particularly attractive for long-term cryptocurrency holders with substantial unrealized gains who wish to support charitable causes while optimizing their tax positions. The establishment of donor-advised funds specifically designed for cryptocurrency contributions has simplified the mechanics of implementing these strategies.

Retirement account strategies for cryptocurrency investments offer significant long-term tax advantages but require careful structuring to comply with self-directed IRA rules and prohibited transaction restrictions. The use of cryptocurrency in retirement accounts can provide tax-deferred or tax-free growth opportunities while avoiding current income recognition on trading activities. However, the complexity of these arrangements requires professional guidance to ensure compliance with applicable regulations.

Audit Defense and Compliance Strategies

The increasing sophistication of IRS enforcement efforts targeting cryptocurrency transactions has made audit defense preparation an essential component of comprehensive tax planning for digital asset investors. The agency’s blockchain analysis capabilities enable the identification of unreported transactions with unprecedented accuracy, making proactive compliance far more cost-effective than reactive audit defense. Understanding the audit process and preparing appropriate documentation can significantly improve outcomes when facing IRS scrutiny.

The IRS has developed specialized audit techniques for cryptocurrency cases that focus on identifying patterns of non-compliance and quantifying unreported income through blockchain analysis. Auditors trained in digital asset investigation can reconstruct transaction histories, identify wallet addresses associated with taxpayers, and calculate unreported income with remarkable precision. This enhanced capability makes traditional audit defense strategies less effective and requires new approaches specifically designed for cryptocurrency cases.

Documentation strategies for audit defense must address the unique characteristics of cryptocurrency transactions while providing the comprehensive records necessary to support reported positions. The creation of contemporaneous business records, detailed transaction logs, and supporting valuation documentation can significantly strengthen a taxpayer’s position during audit proceedings. Professional cryptocurrency tax preparation that emphasizes documentation quality can provide substantial protection against adverse audit outcomes.

The voluntary disclosure of unreported cryptocurrency income through participation in IRS amnesty programs can provide significant benefits for taxpayers with historical non-compliance issues. These programs typically offer reduced penalties and protection against criminal prosecution in exchange for complete disclosure and payment of back taxes. However, the decision to participate in voluntary disclosure programs requires careful analysis of the potential benefits and risks associated with each specific situation.

Technology Solutions and Professional Services

The complexity of cryptocurrency tax compliance has driven the development of sophisticated software solutions and professional services specifically designed to address the unique challenges of digital asset taxation. These tools range from basic transaction tracking applications to comprehensive platforms that integrate with multiple exchanges and provide detailed tax reporting capabilities. Understanding the capabilities and limitations of available technology solutions is essential for developing an effective compliance strategy.

Automated transaction tracking software can significantly reduce the administrative burden of maintaining cryptocurrency tax records by connecting directly to exchange APIs and importing transaction data automatically. However, these solutions often require manual intervention to properly categorize complex transactions or address data inconsistencies between different platforms. The accuracy of automated solutions depends heavily on the quality of underlying data and the sophistication of the categorization algorithms employed.

Professional tax preparation services specializing in cryptocurrency have emerged to address the growing demand for expert guidance in digital asset taxation. These services typically combine advanced software tools with specialized knowledge of cryptocurrency tax law to provide comprehensive compliance solutions. The selection of appropriate professional services requires careful evaluation of the provider’s experience, methodology, and fee structure relative to the complexity of the taxpayer’s cryptocurrency activities.

The integration of cryptocurrency tax compliance with broader financial planning requires coordination between multiple professional service providers, including tax preparers, financial advisors, and legal counsel. This collaborative approach ensures that tax planning strategies align with overall investment objectives while maintaining compliance with applicable regulations. Investors using comprehensive market analysis tools should ensure their professional service team understands both traditional investment principles and the unique aspects of cryptocurrency taxation.

Looking Ahead: Future Developments

The cryptocurrency tax landscape continues to evolve rapidly as regulators attempt to keep pace with technological innovation and market developments. Understanding likely future changes can help taxpayers prepare for emerging compliance requirements and position themselves advantageously for new opportunities and challenges. The regulatory trajectory suggests increased reporting requirements, enhanced enforcement capabilities, and greater clarity around previously ambiguous areas of cryptocurrency taxation.

Proposed regulations addressing decentralized finance activities are expected to provide much-needed clarity around the tax treatment of complex DeFi transactions, potentially simplifying compliance requirements while closing existing loopholes. The Treasury Department has indicated that future guidance will address staking rewards, governance token distributions, and automated market maker activities with greater specificity than current general guidance provides. These developments should reduce uncertainty while potentially increasing compliance complexity.

The implementation of central bank digital currencies may fundamentally alter the cryptocurrency tax landscape by introducing government-issued digital assets that could receive different tax treatment than current cryptocurrencies. The potential for CBDC transactions to be automatically reported to tax authorities could create new compliance paradigms that extend to the broader cryptocurrency ecosystem. Early preparation for these potential changes can help taxpayers maintain compliance while optimizing their positions for future developments.

International coordination efforts aimed at standardizing cryptocurrency tax reporting across jurisdictions may result in new compliance obligations for US taxpayers with international cryptocurrency activities. The Organization for Economic Cooperation and Development’s work on global cryptocurrency tax standards could lead to automatic information exchange programs that significantly increase the transparency of international digital asset transactions.

Essential Action Items for 2025

The approaching 2025 tax deadline requires immediate action from cryptocurrency traders to ensure compliance with evolving requirements and optimize their tax positions. The complexity of current regulations combined with enhanced enforcement capabilities makes professional preparation more valuable than ever, while the strategic use of available planning opportunities can significantly reduce overall tax burdens.

Comprehensive transaction record compilation must begin immediately for taxpayers who have not maintained adequate documentation throughout the year. This process involves gathering data from all cryptocurrency platforms, reconstructing transaction histories, and reconciling records to ensure completeness and accuracy. The time-intensive nature of this process makes early preparation essential for meeting filing deadlines without compromising accuracy.

Professional tax consultation becomes increasingly valuable as cryptocurrency tax complexity continues to expand beyond the capabilities of general practitioners. Specialized cryptocurrency tax professionals can identify optimization opportunities, ensure compliance with complex requirements, and provide audit defense capabilities that justify their fees through risk reduction and tax savings. The selection of appropriate professional services should begin well before the filing deadline to ensure adequate time for thorough preparation.

Strategic planning for future tax years should incorporate lessons learned from 2024 activities while positioning for anticipated regulatory changes and market developments. This forward-looking approach enables the implementation of structures and strategies that optimize long-term tax outcomes while maintaining flexibility to adapt to changing circumstances. Professional traders utilizing advanced analytical tools and market insights should integrate tax planning considerations into their overall investment strategy to maximize after-tax returns and ensure sustainable compliance with evolving regulatory requirements.

The 2025 tax season represents a critical juncture for cryptocurrency taxation as regulatory frameworks mature and enforcement capabilities reach new levels of sophistication. Success requires a proactive approach that emphasizes comprehensive record keeping, professional guidance, and strategic planning designed to optimize tax outcomes while maintaining full compliance with applicable regulations. The investment in proper cryptocurrency tax compliance pays dividends through reduced audit risk, optimized tax positions, and the peace of mind that comes from knowing that one’s digital asset activities are properly documented and reported.

Disclaimer: This article is for educational and informational purposes only and should not be construed as tax or legal advice. Tax laws are complex and subject to change, and the application of tax rules to cryptocurrency transactions can vary based on individual circumstances. The information provided does not constitute professional tax advice and should not be relied upon for making tax decisions. Always consult with qualified tax professionals, certified public accountants, or tax attorneys who specialize in cryptocurrency taxation before making any decisions regarding your tax obligations. The author and publisher are not responsible for any tax penalties, interest, or other consequences that may arise from acting on the information provided in this article.