The Banking Industry’s Digital Asset Evolution

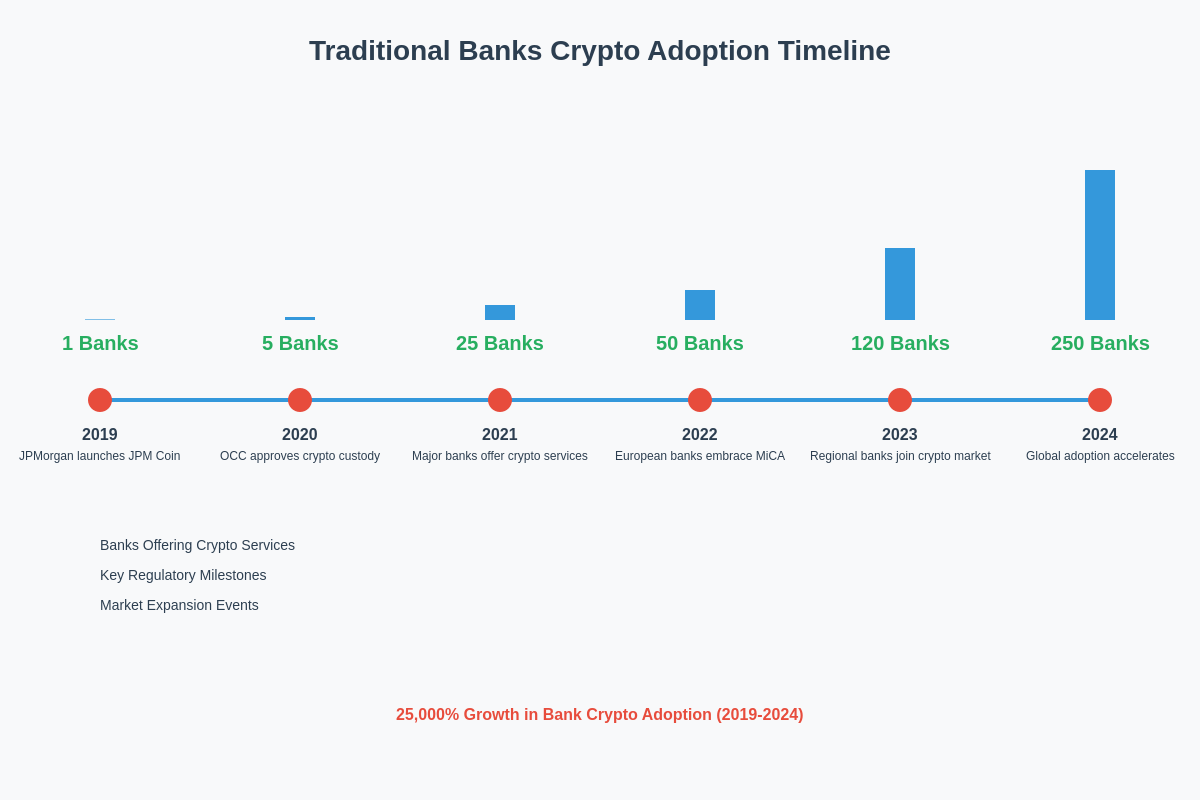

The traditional banking sector has undergone a profound transformation in its approach to cryptocurrency and digital assets, evolving from skeptical observers to active participants in what represents one of the most significant shifts in financial services since the advent of online banking. Major financial institutions that once dismissed Bitcoin and other cryptocurrencies as speculative instruments have now embraced digital assets as legitimate investment vehicles, developing sophisticated custody solutions and lending products that bridge the gap between traditional finance and the emerging cryptocurrency ecosystem.

This institutional adoption has been driven by growing client demand, regulatory clarity in key jurisdictions, and the recognition that digital assets represent a substantial and permanent addition to the global financial landscape. Banks ranging from regional community institutions to global investment banking giants have launched cryptocurrency custody services, offering professional-grade security infrastructure and regulatory compliance that appeals to institutional investors, high-net-worth individuals, and sophisticated retail clients who require the security and reliability associated with traditional banking relationships.

The convergence of traditional banking expertise with cryptocurrency innovation has created new opportunities for financial services providers while presenting unique challenges related to regulatory compliance, risk management, and operational infrastructure. Banks entering the cryptocurrency space must navigate complex regulatory frameworks, develop new risk assessment methodologies, and invest in specialized technology infrastructure while maintaining the safety and soundness standards expected by regulators and clients alike.

Regulatory Framework and Compliance Infrastructure

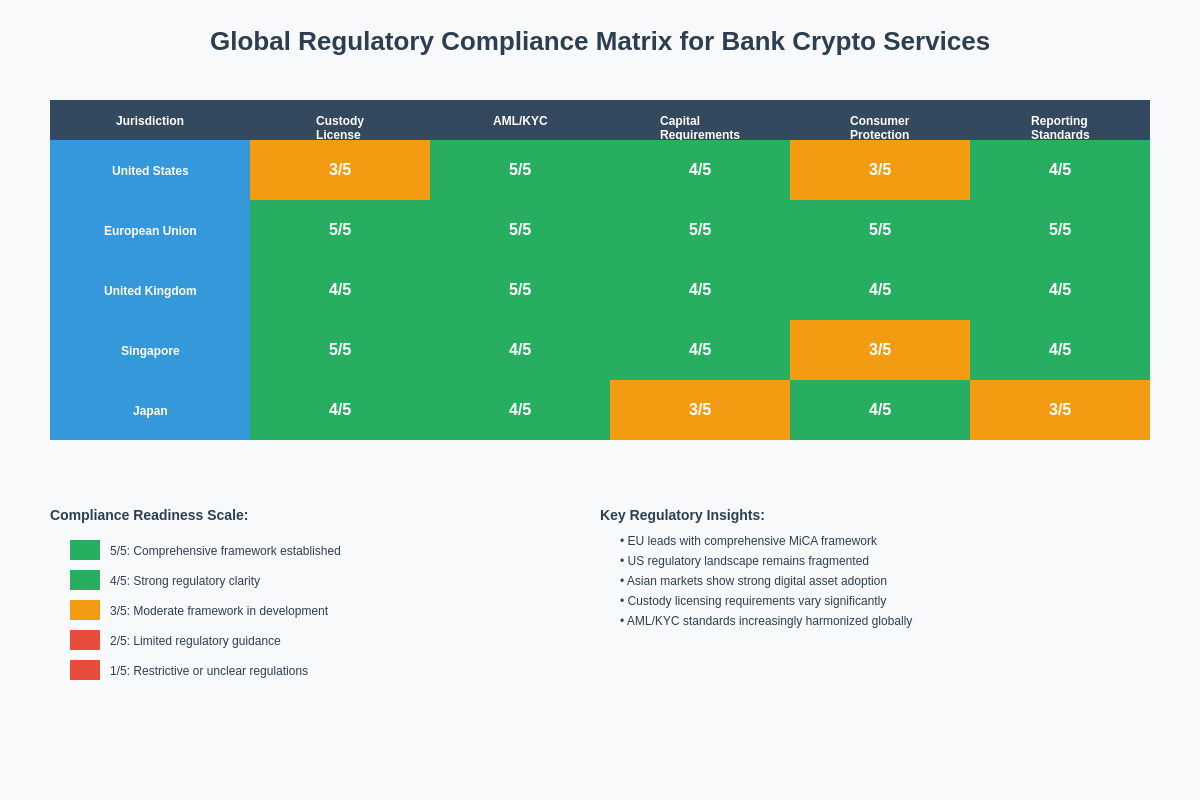

The regulatory landscape surrounding bank-offered cryptocurrency services remains complex and rapidly evolving, with different jurisdictions adopting varying approaches to digital asset regulation that directly impact how traditional banks can participate in cryptocurrency markets. In the United States, regulatory agencies including the Office of the Comptroller of the Currency, Federal Reserve, and Federal Deposit Insurance Corporation have issued guidance clarifying the circumstances under which banks can provide cryptocurrency custody and related services, though significant regulatory uncertainty persists in many areas.

European banks operate under the Markets in Crypto-Assets Regulation framework, which provides more comprehensive regulatory clarity for cryptocurrency service providers while establishing stringent requirements for operational resilience, customer protection, and risk management. This regulatory framework has enabled European banks to develop more extensive cryptocurrency service offerings compared to their American counterparts, though implementation challenges and compliance costs remain significant considerations for institutions developing digital asset capabilities.

The compliance infrastructure required for bank-offered cryptocurrency services extends beyond traditional anti-money laundering and know-your-customer requirements to include specialized controls for digital asset transactions, blockchain analysis capabilities, and enhanced due diligence procedures for cryptocurrency-related activities. Banks must implement sophisticated transaction monitoring systems capable of analyzing blockchain transactions, maintain detailed records of digital asset holdings and transfers, and develop new procedures for managing the unique risks associated with cryptocurrency custody and lending operations.

Risk management frameworks for bank cryptocurrency services must address novel risk factors including private key security, blockchain network risks, smart contract vulnerabilities, and the potential for rapid value fluctuations that can impact collateral values in lending arrangements. Traditional banking risk management practices require adaptation to address these cryptocurrency-specific risks while maintaining consistency with established risk management principles and regulatory expectations for safety and soundness.

Custody Architecture and Security Models

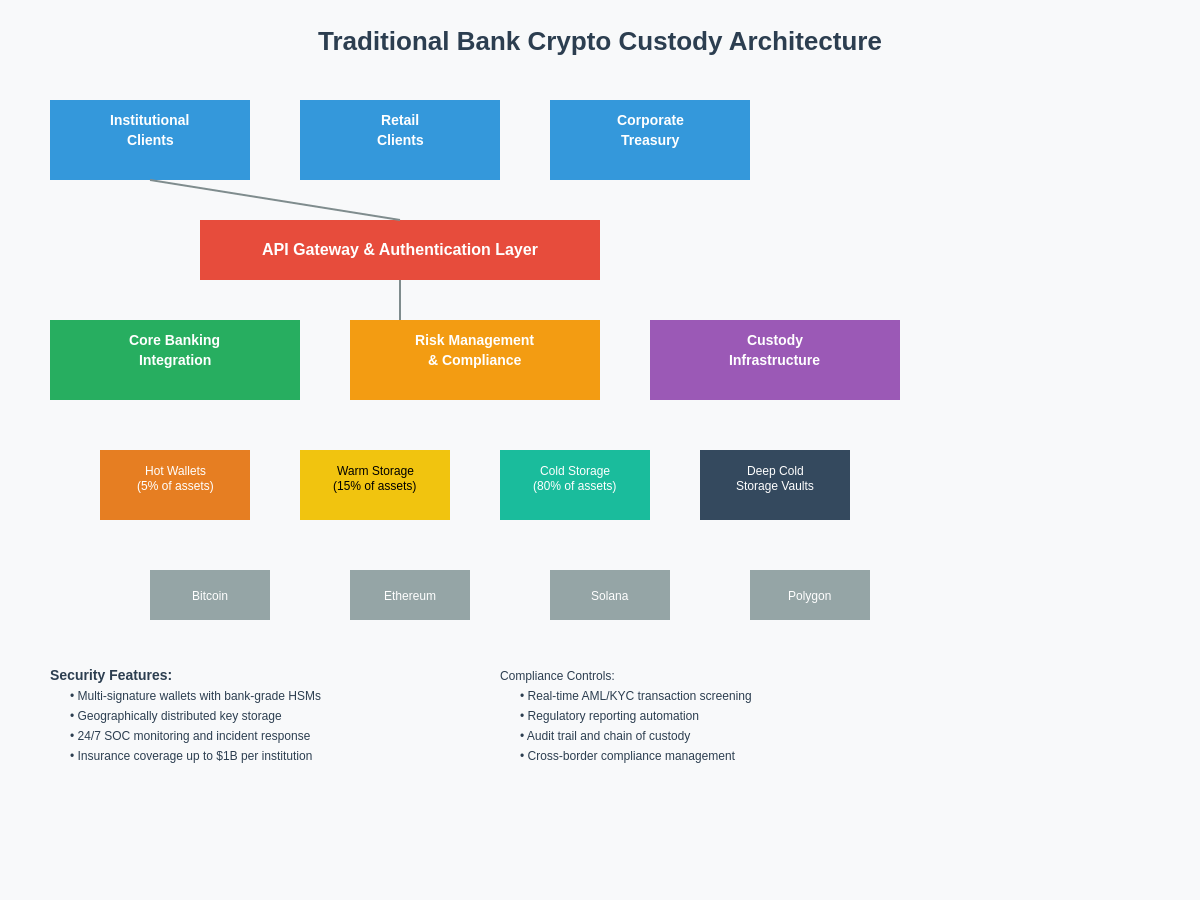

The technical architecture underlying bank-provided cryptocurrency custody services represents a sophisticated blend of traditional banking security practices and cutting-edge blockchain technology infrastructure designed to meet institutional-grade security requirements while providing the operational flexibility necessary for professional asset management. Banks offering cryptocurrency custody typically employ multi-layered security models that combine hardware security modules, multi-signature wallet configurations, and cold storage systems with traditional banking security controls including physical security, access controls, and operational procedures designed to prevent unauthorized access to client assets.

Hot wallet systems used by banks for operational cryptocurrency management incorporate advanced security features including multi-party computation protocols, threshold signature schemes, and real-time monitoring systems that can detect and respond to suspicious activities before they result in asset losses. These systems must balance security requirements with operational efficiency, enabling banks to process client transactions promptly while maintaining the highest levels of security expected by institutional clients and required by banking regulators.

Cold storage solutions employed by banks for long-term cryptocurrency custody typically involve air-gapped systems, geographically distributed key storage, and elaborate key ceremony procedures that ensure no single individual or system can access client assets without proper authorization. The implementation of these cold storage systems requires significant investment in specialized facilities, security personnel, and operational procedures that meet banking industry standards for asset protection while accommodating the unique characteristics of cryptocurrency storage.

Banks must also develop comprehensive disaster recovery and business continuity procedures specifically tailored to cryptocurrency custody operations, including procedures for key recovery, transaction processing during system outages, and coordination with blockchain networks during periods of network congestion or technical difficulties. These procedures must account for the irreversible nature of many cryptocurrency transactions and the potential for permanent asset loss if proper recovery procedures are not followed during emergency situations.

Institutional Custody Services and Product Offerings

The institutional custody services offered by traditional banks have evolved to encompass a comprehensive suite of digital asset management capabilities designed to meet the needs of pension funds, endowments, family offices, and other institutional investors seeking professional-grade cryptocurrency exposure. These services typically include segregated asset custody, transaction processing, reporting and analytics, and integration with existing investment management platforms that enable institutional clients to incorporate cryptocurrency holdings into their broader investment portfolios.

Banks offering institutional cryptocurrency custody services provide detailed reporting capabilities that include real-time asset valuations, transaction histories, tax reporting support, and performance analytics that enable institutional clients to monitor their digital asset holdings with the same level of detail and accuracy they expect from traditional asset custody services. Integration with existing portfolio management systems allows institutional clients to view their cryptocurrency holdings alongside traditional investments, facilitating comprehensive risk management and asset allocation decisions.

The pricing models for bank-provided cryptocurrency custody services typically reflect the higher operational costs and specialized infrastructure required for digital asset management, with custody fees that may exceed those charged for traditional securities custody while remaining competitive with specialized cryptocurrency custody providers. Banks often structure these fees to include both custody charges and transaction processing fees, with volume discounts available for larger institutional clients who maintain substantial digital asset holdings or generate significant transaction volumes.

Institutional clients using bank cryptocurrency custody services benefit from the established relationships, credit facilities, and comprehensive financial services capabilities that traditional banks can provide, enabling them to leverage their cryptocurrency holdings for additional financial products including loans, derivatives, and structured products that may not be available through specialized cryptocurrency service providers. This integration of cryptocurrency services with traditional banking capabilities represents a significant competitive advantage for banks entering the digital asset market.

Cryptocurrency Lending and Credit Products

The development of cryptocurrency-backed lending products by traditional banks represents one of the most significant innovations in digital asset financial services, enabling clients to access liquidity against their cryptocurrency holdings without requiring asset sales that might trigger taxable events or result in missed appreciation opportunities. These lending products typically allow clients to pledge Bitcoin, Ethereum, and other major cryptocurrencies as collateral for USD-denominated loans, with loan-to-value ratios and interest rates that reflect the volatility and risk characteristics of different digital assets.

Banks offering cryptocurrency lending services must develop sophisticated collateral management systems capable of monitoring cryptocurrency values in real-time, implementing automated margin calls when collateral values decline below specified thresholds, and managing the liquidation of cryptocurrency collateral when borrowers are unable to meet margin requirements. These systems must integrate with both traditional banking loan processing systems and cryptocurrency custody infrastructure to provide seamless management of collateralized lending relationships.

The risk management frameworks for cryptocurrency lending require banks to establish appropriate loan-to-value ratios that account for the historical volatility of different cryptocurrencies while providing sufficient buffer to protect against rapid price declines that could result in under-collateralized positions. Banks typically implement conservative loan-to-value ratios ranging from 25% to 50% for major cryptocurrencies, with lower ratios applied to more volatile or less liquid digital assets.

Interest rates for cryptocurrency-backed loans generally reflect both the underlying risk-free rate and a premium that accounts for the additional risks associated with cryptocurrency collateral, including volatility risk, operational risk, and the potential for technological disruptions that could affect the value or accessibility of pledged collateral. Banks may offer both fixed and floating rate cryptocurrency loans, with pricing that remains competitive with specialized cryptocurrency lenders while providing the additional security and regulatory protection associated with traditional banking relationships.

Retail Banking Integration and Consumer Products

The integration of cryptocurrency services into retail banking platforms represents a significant expansion of digital asset accessibility, enabling ordinary consumers to purchase, hold, and transact in cryptocurrencies through familiar banking interfaces with the security and consumer protections associated with traditional bank accounts. Retail banks offering cryptocurrency services typically provide simplified purchase and sale capabilities, basic custody services, and integration with existing online and mobile banking platforms that make cryptocurrency ownership accessible to mainstream consumers who might otherwise be intimidated by specialized cryptocurrency exchanges or wallets.

Consumer cryptocurrency products offered by traditional banks often include features such as recurring purchase plans, automatic rebalancing capabilities, and educational resources designed to help retail clients understand cryptocurrency markets and make informed investment decisions. These products are typically designed with user experience and simplicity as primary objectives, abstracting away much of the technical complexity associated with cryptocurrency ownership while providing professional-grade security and regulatory compliance.

The pricing structures for retail cryptocurrency services offered by banks typically include transaction fees for purchases and sales, annual fees for custody services, and spreads on cryptocurrency transactions that reflect the costs of providing regulatory-compliant cryptocurrency services to retail clients. While these fees may be higher than those charged by specialized cryptocurrency platforms, many consumers are willing to pay premium pricing for the security, convenience, and regulatory protection provided by traditional banking relationships.

Banks offering retail cryptocurrency services must implement comprehensive consumer protection measures including clear disclosure of risks associated with cryptocurrency investment, robust security controls to protect consumer accounts from unauthorized access, and customer service capabilities that can address cryptocurrency-related inquiries and problems. These consumer protection measures must comply with existing consumer banking regulations while addressing the unique risks and challenges associated with cryptocurrency products.

Technology Infrastructure and Operational Considerations

The technology infrastructure required to support bank-offered cryptocurrency services represents a significant departure from traditional banking systems, requiring specialized blockchain integration capabilities, cryptocurrency wallet management systems, and real-time market data feeds that enable banks to provide professional-grade digital asset services while maintaining integration with existing banking operations. Banks must invest in both internal technology development and partnerships with specialized technology providers to build the comprehensive infrastructure necessary for cryptocurrency custody and lending operations.

Blockchain integration systems must provide banks with the ability to monitor cryptocurrency transactions, validate blockchain network status, and interact with multiple blockchain networks while maintaining the security and reliability standards expected in banking operations. These systems must handle the technical complexities of different blockchain protocols while providing standardized interfaces that enable integration with existing banking systems and procedures.

The operational procedures required for cryptocurrency services extend beyond traditional banking operations to include specialized processes for private key management, cryptocurrency transaction processing, blockchain network monitoring, and incident response procedures specifically designed to address cryptocurrency-related operational risks. Banks must train personnel in cryptocurrency operations while developing new policies and procedures that address the unique operational requirements of digital asset services.

Vendor management for cryptocurrency services requires banks to evaluate and monitor specialized service providers including blockchain infrastructure providers, cryptocurrency market data vendors, and security service providers who may not meet traditional banking vendor management standards. Banks must develop new vendor management frameworks that account for the unique risks and characteristics of cryptocurrency service providers while maintaining appropriate oversight and risk management controls.

Risk Management and Capital Requirements

The risk management frameworks for bank cryptocurrency services must address a complex array of risks that extend beyond traditional banking risks to include technology risks, market risks, operational risks, and regulatory risks that are unique to digital asset operations. Banks must develop new risk assessment methodologies that account for the volatility of cryptocurrency markets, the technical complexity of blockchain operations, and the evolving regulatory landscape surrounding digital asset services.

Market risk management for cryptocurrency services requires banks to implement sophisticated modeling capabilities that can assess the potential impact of cryptocurrency price movements on bank capital, customer positions, and overall financial performance. These models must account for the high volatility and correlation characteristics of cryptocurrency markets while providing accurate risk metrics that enable effective risk management decision-making.

Operational risk management for cryptocurrency services must address risks including private key compromise, blockchain network disruptions, cyber attacks specifically targeting cryptocurrency operations, and human errors that could result in permanent loss of digital assets. Banks must implement comprehensive operational risk controls including redundant systems, detailed procedures for cryptocurrency operations, and incident response capabilities specifically designed for digital asset services.

Capital requirements for bank cryptocurrency services vary by jurisdiction and regulatory framework, with some regulators applying specific capital charges for cryptocurrency exposures while others require banks to apply existing capital frameworks to digital asset activities. Banks must carefully evaluate the capital implications of cryptocurrency services while ensuring compliance with applicable regulatory capital requirements and maintaining appropriate capital buffers for the risks associated with digital asset operations.

The stress testing and scenario analysis procedures for bank cryptocurrency services must incorporate extreme market scenarios that reflect the potential for rapid and significant cryptocurrency price movements, blockchain network disruptions, and regulatory changes that could impact the viability of cryptocurrency business lines. These stress testing procedures must provide banks with clear understanding of potential losses and enable appropriate risk management and capital planning decisions.

Competitive Dynamics and Market Evolution

The competitive landscape for bank-provided cryptocurrency services continues to evolve rapidly as traditional financial institutions compete with specialized cryptocurrency service providers, fintech companies, and emerging financial technology platforms that offer alternative approaches to digital asset custody and lending. Banks entering the cryptocurrency market must compete on factors including security, regulatory compliance, customer service, pricing, and product functionality while leveraging their existing customer relationships and comprehensive financial services capabilities.

Traditional banks possess significant competitive advantages in cryptocurrency markets including established regulatory relationships, existing customer bases, comprehensive compliance infrastructure, and access to capital markets that enable them to offer cryptocurrency services as part of broader financial relationships. However, banks also face competitive disadvantages including regulatory constraints, conservative risk management practices, and operational complexity that may limit their ability to innovate as quickly as specialized cryptocurrency service providers.

The evolution of cryptocurrency markets continues to create new opportunities and challenges for traditional banks, with developments including decentralized finance protocols, central bank digital currencies, and new cryptocurrency use cases that may require banks to continually adapt their digital asset strategies and service offerings. Banks must balance the need to remain competitive in rapidly evolving cryptocurrency markets with their obligations to maintain safe and sound banking practices and comply with applicable regulatory requirements.

Partnership strategies between traditional banks and specialized cryptocurrency service providers have become increasingly common as banks seek to leverage external expertise while maintaining control over customer relationships and regulatory compliance. These partnerships can enable banks to offer cryptocurrency services more quickly and cost-effectively while allowing specialized providers to access broader customer bases and benefit from established banking relationships.

Cross-Border Payments and Settlement Innovation

The application of cryptocurrency technology to cross-border payments and settlement represents one of the most promising use cases for bank integration of digital assets, offering the potential to significantly reduce settlement times, lower transaction costs, and improve transparency in international money transfers. Banks are increasingly exploring the use of stablecoins, central bank digital currencies, and blockchain-based settlement networks to enhance their cross-border payment capabilities while maintaining compliance with international banking regulations and anti-money laundering requirements.

Stablecoin integration into bank payment systems enables faster and more cost-effective international transfers compared to traditional correspondent banking relationships, while providing the price stability necessary for commercial payment applications. Banks implementing stablecoin payment capabilities must develop appropriate risk management frameworks that address counterparty risks associated with stablecoin issuers, technological risks related to blockchain infrastructure, and regulatory risks surrounding stablecoin classification and oversight.

The development of blockchain-based settlement networks specifically designed for banking applications offers the potential to create more efficient and transparent international payment systems while maintaining the regulatory oversight and consumer protections associated with traditional banking relationships. Banks participating in these networks must balance the benefits of improved efficiency with the risks associated with new technology platforms and the need to maintain interoperability with existing payment systems.

Regulatory frameworks for cryptocurrency-based cross-border payments continue to evolve as regulators seek to balance innovation benefits with consumer protection and financial stability concerns. Banks developing cryptocurrency payment capabilities must navigate complex international regulatory requirements while ensuring compliance with both domestic and foreign regulations that may apply to their cross-border payment activities.

Institutional Investment and Treasury Management

The use of cryptocurrency assets in bank treasury management and institutional investment strategies represents a significant development in how traditional financial institutions approach digital assets as legitimate components of diversified investment portfolios. Banks are increasingly considering cryptocurrency holdings as treasury assets, developing investment policies and risk management frameworks that enable appropriate cryptocurrency exposure while maintaining prudent risk management practices and regulatory compliance.

Treasury management applications for cryptocurrency include diversification benefits, potential hedge against inflation, and exposure to technological innovation in financial services, though banks must carefully evaluate these potential benefits against the risks associated with cryptocurrency volatility, regulatory uncertainty, and operational complexity. Banks developing cryptocurrency treasury strategies must implement appropriate governance structures, risk limits, and monitoring procedures that ensure cryptocurrency investments remain consistent with overall risk management objectives.

Institutional investment services that incorporate cryptocurrency capabilities enable banks to offer comprehensive asset management services that include digital asset allocation, rebalancing, and performance monitoring as components of broader institutional investment mandates. These services require banks to develop sophisticated investment management capabilities specifically tailored to cryptocurrency markets while maintaining integration with traditional investment management platforms and procedures.

The integration of cryptocurrency analytics and research capabilities into institutional investment services enables banks to provide clients with comprehensive analysis of digital asset markets, including fundamental analysis of blockchain projects, technical analysis of cryptocurrency price movements, and macroeconomic analysis of factors affecting cryptocurrency valuations. This research capability represents a significant competitive advantage for banks seeking to differentiate their cryptocurrency investment services from specialized providers.

Future Developments and Emerging Technologies

The future evolution of bank-provided cryptocurrency services will likely be shaped by emerging technologies including layer-2 scaling solutions, advanced privacy-preserving technologies, interoperability protocols, and artificial intelligence applications that could significantly enhance the functionality and efficiency of digital asset services. Banks must continuously evaluate these emerging technologies to identify opportunities for service enhancement while managing the risks associated with early adoption of unproven technologies.

Layer-2 scaling solutions for major blockchain networks offer the potential to significantly reduce transaction costs and processing times for bank cryptocurrency services, enabling more cost-effective custody and lending operations while improving the customer experience for both institutional and retail clients. Banks implementing layer-2 solutions must carefully evaluate the security and reliability of these systems while developing appropriate risk management frameworks for new technology adoption.

The development of central bank digital currencies represents both an opportunity and a challenge for traditional banks offering cryptocurrency services, as CBDCs could provide more stable and regulated alternatives to existing cryptocurrencies while potentially reducing demand for bank-provided digital asset services. Banks must develop strategies that position them to benefit from CBDC implementations while maintaining competitiveness in broader cryptocurrency markets.

Artificial intelligence and machine learning applications in cryptocurrency services offer significant potential for enhancing risk management, fraud detection, customer service, and investment management capabilities, though banks must carefully evaluate the appropriate use of AI technologies while maintaining human oversight and regulatory compliance. The integration of AI capabilities into cryptocurrency services must balance potential benefits with risks including algorithmic bias, operational reliability, and regulatory acceptance of automated decision-making systems.

The evolution of regulatory frameworks for cryptocurrency services will continue to shape the competitive landscape and operational requirements for bank digital asset offerings, with potential developments including international regulatory coordination, enhanced consumer protection requirements, and new capital and liquidity requirements specifically designed for cryptocurrency activities. Banks must maintain flexibility in their cryptocurrency strategies to adapt to changing regulatory requirements while continuing to meet customer needs and maintain competitive positioning in evolving digital asset markets.

For traders and institutions looking to analyze cryptocurrency market trends and develop sophisticated trading strategies, TradingView’s comprehensive charting platform provides essential tools for technical analysis and market research that complement traditional banking cryptocurrency services with professional-grade analytical capabilities.

Disclaimer: This content is for informational purposes only and should not be considered as financial advice. Cryptocurrency investments carry substantial risk of loss and may not be suitable for all investors. Past performance does not guarantee future results. Always conduct your own research and consult with qualified financial advisors before making investment decisions. The regulatory landscape for cryptocurrency services continues to evolve, and banks offering digital asset services may be subject to changing regulatory requirements that could affect service availability and terms.