The pursuit of undercollateralized lending represents one of the most ambitious and transformative goals in decentralized finance, promising to unlock trillions of dollars in credit markets while maintaining the trustless, permissionless principles that define the DeFi ecosystem. This revolutionary concept challenges the fundamental assumption that blockchain-based lending must always require overcollateralization, opening pathways to financial inclusion and capital efficiency that could rival or surpass traditional banking systems.

For the most comprehensive analysis of lending protocols and DeFi innovations, traders and analysts rely on advanced charting tools available at TradingView’s professional platform, which provides essential data for evaluating protocol performance and market trends. The evolution toward undercollateralized lending represents a paradigm shift that could fundamentally alter how we conceptualize credit, risk, and financial intermediation in the digital age.

The Fundamental Challenge of Trust in Trustless Systems

The inherent contradiction between trustless blockchain systems and traditional credit mechanisms has created one of the most complex challenges in decentralized finance, requiring innovative solutions that can establish creditworthiness and enforce repayment without relying on traditional legal frameworks or centralized authorities. Traditional lending systems depend heavily on legal enforcement, credit histories, and institutional intermediaries to manage counterparty risk, elements that are either absent or fundamentally different in decentralized environments.

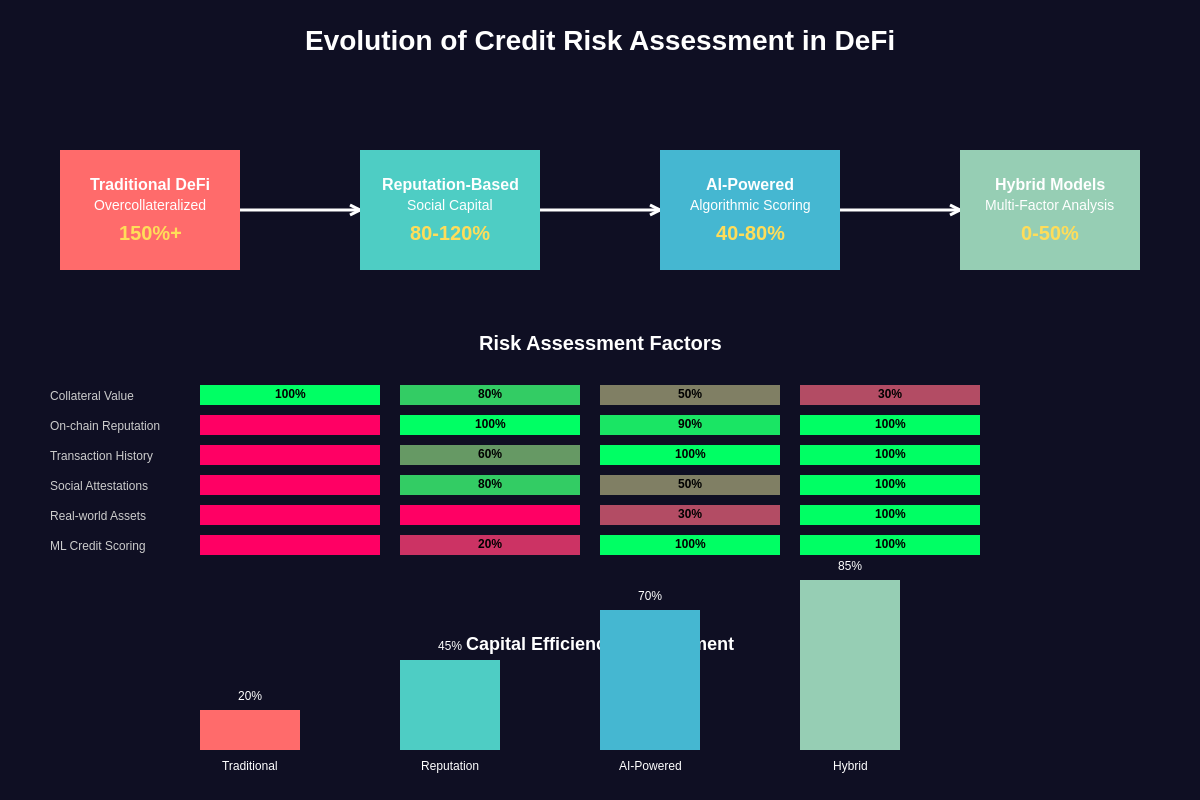

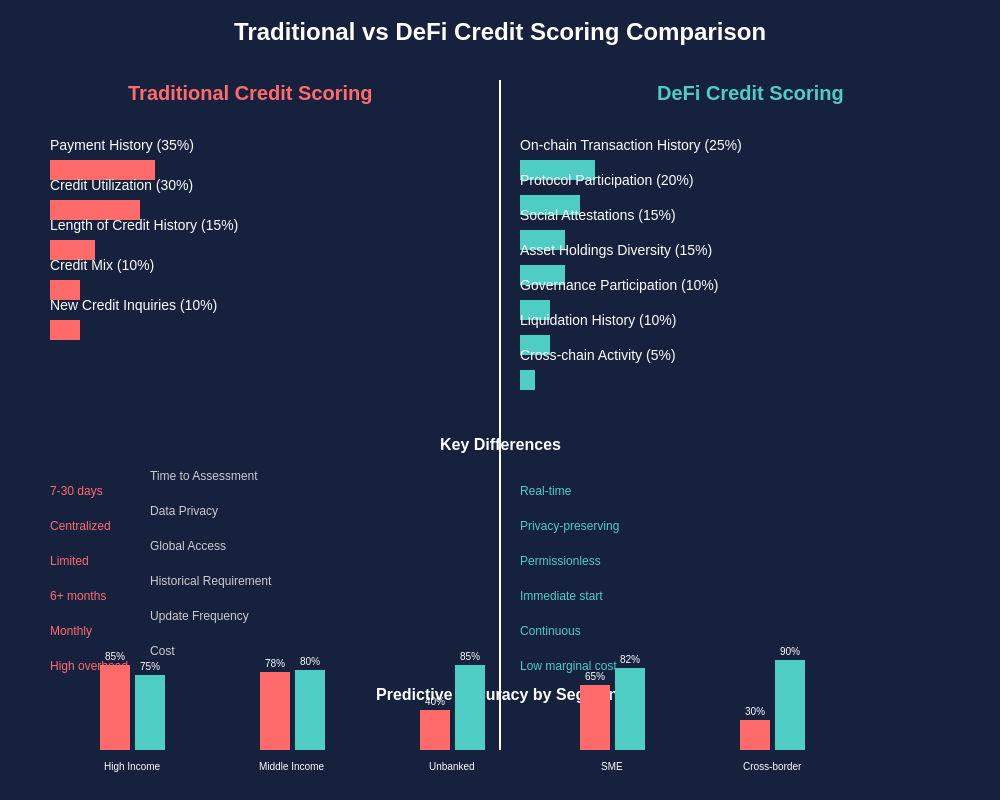

Current DeFi lending protocols like Aave, Compound, and MakerDAO require borrowers to deposit collateral worth significantly more than the loan amount, typically maintaining loan-to-value ratios between 50% and 80% depending on the underlying assets. This overcollateralization requirement severely limits the capital efficiency of DeFi lending and excludes many potential borrowers who may be creditworthy but lack sufficient cryptocurrency holdings to meet collateral requirements.

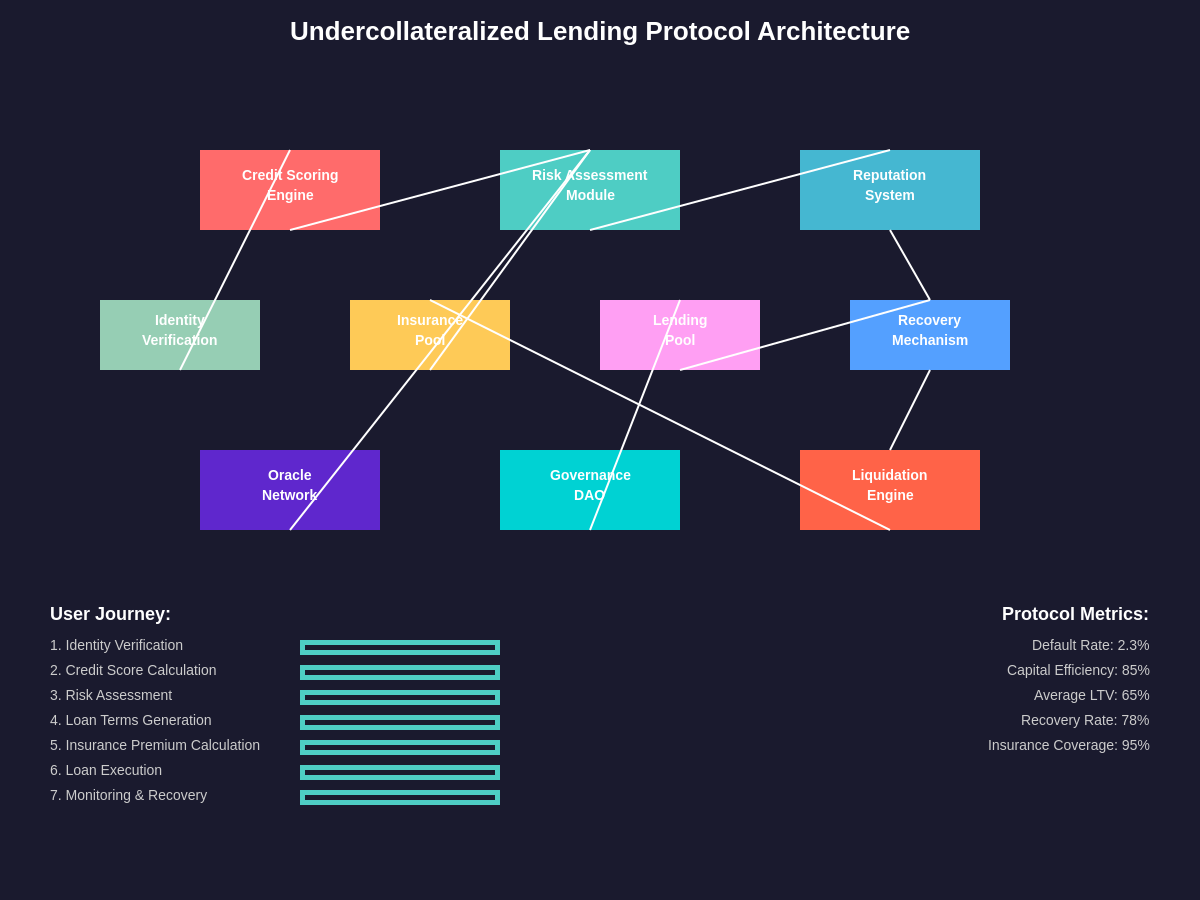

The challenge of creating undercollateralized lending systems in DeFi involves developing mechanisms that can assess creditworthiness, enforce repayment, and manage default risk without compromising the decentralized, permissionless nature of blockchain systems. Early approaches have focused on reputation systems, social collateral, real-world asset tokenization, and algorithmic risk assessment models that can operate within decentralized frameworks.

Identity verification and reputation systems represent one approach to establishing creditworthiness in DeFi, utilizing on-chain activity history, social graphs, and attestation mechanisms to create credit profiles for borrowers. These systems must balance privacy concerns with the need for sufficient information to make accurate credit decisions, often employing zero-knowledge proofs and other privacy-preserving technologies to protect user data while enabling credit assessment.

Reputation-Based Lending Models and Social Capital

The development of reputation-based lending systems in DeFi represents a fascinating intersection of social psychology, game theory, and blockchain technology, creating new forms of social capital that can be quantified, transferred, and leveraged for financial purposes. These systems attempt to replicate the trust mechanisms that have historically enabled lending in traditional communities, where reputation and social connections serve as informal collateral for loans.

On-chain reputation systems analyze various metrics including transaction history, protocol participation, governance voting patterns, and network effects to create comprehensive credit profiles for potential borrowers. Protocols like Spectral Finance and ARCx have pioneered approaches that combine multiple data sources to generate credit scores based entirely on blockchain activity, creating new forms of financial identity that exist independently of traditional credit systems.

Social collateral mechanisms leverage community relationships and peer-to-peer vouching systems to enable undercollateralized lending, where community members can provide social guarantees for borrowers in exchange for various incentives or rewards. These systems create network effects where established community members have incentives to help newcomers build reputation, fostering growth and inclusion within DeFi ecosystems.

The effectiveness of reputation-based systems depends heavily on their resistance to manipulation and their ability to accurately predict borrower behavior over time. Sophisticated attackers might attempt to build false reputations through wash trading, multiple identity creation, or other forms of system gaming, requiring robust detection mechanisms and continuous evolution of reputation algorithms.

Data analytics platforms like TradingView’s institutional solutions provide essential infrastructure for analyzing on-chain reputation metrics and borrower behavior patterns, enabling more sophisticated risk assessment models for undercollateralized lending protocols. The integration of traditional financial data with blockchain metrics creates opportunities for hybrid reputation systems that can serve both DeFi and traditional finance markets.

Network effects in reputation systems create powerful incentives for honest behavior, as borrowers who default not only lose access to future credit but also damage their standing within valuable communities and ecosystems. These social penalties can be more effective than traditional financial penalties in certain contexts, particularly within tight-knit communities or professional networks where reputation has significant economic value.

Real-World Asset Integration and Tokenization

The tokenization of real-world assets represents one of the most promising pathways toward undercollateralized lending in DeFi, enabling borrowers to leverage traditional assets like real estate, inventory, accounts receivable, and intellectual property as collateral for blockchain-based loans. This approach bridges the gap between traditional finance and DeFi while potentially unlocking trillions of dollars in previously illiquid assets.

Protocols like Centrifuge, Maple Finance, and TrueFi have pioneered various approaches to real-world asset integration, creating frameworks for asset origination, tokenization, legal structuring, and risk management that can operate within DeFi ecosystems. These systems must address complex challenges including asset valuation, legal enforceability, custody arrangements, and regulatory compliance across multiple jurisdictions.

Legal frameworks for tokenized asset lending vary significantly across jurisdictions, with some regions providing clear guidance for digital asset secured lending while others maintain regulatory uncertainty that complicates protocol development. The evolution of these frameworks will significantly impact the scalability and adoption of real-world asset lending protocols in DeFi.

Asset tokenization processes typically involve multiple parties including asset originators, legal entities, custody providers, valuation experts, and technology providers, creating complex operational requirements that must be managed while maintaining the decentralized characteristics of DeFi protocols. Smart contracts must interface with traditional legal systems and asset custody arrangements, requiring sophisticated legal and technical structures.

The integration of traditional credit enhancement mechanisms like insurance, guarantees, and credit derivatives into DeFi lending protocols creates opportunities for more sophisticated risk management while maintaining decentralized governance and operation. These hybrid approaches can provide the security and predictability required for institutional adoption while preserving the innovation and efficiency benefits of decentralized systems.

Valuation and price discovery mechanisms for tokenized real-world assets require sophisticated oracle systems and market-making infrastructure that can provide reliable pricing data for illiquid or unique assets. The development of decentralized valuation networks and asset pricing protocols represents a critical infrastructure requirement for scaling real-world asset lending in DeFi.

Algorithmic Credit Scoring and Machine Learning

The application of machine learning and algorithmic credit scoring to blockchain data represents a technological frontier that could enable sophisticated risk assessment for undercollateralized lending while maintaining the permissionless characteristics of DeFi systems. These approaches leverage the rich transaction history and behavioral data available on public blockchains to create predictive models for borrower creditworthiness.

Advanced analytics platforms process vast amounts of on-chain data including transaction patterns, smart contract interactions, token holding patterns, DeFi protocol usage, and network relationships to identify signals that correlate with creditworthy behavior. Machine learning models can identify subtle patterns and relationships in this data that might not be apparent through traditional analysis methods.

Privacy-preserving machine learning techniques enable credit scoring systems that can analyze sensitive financial behavior without compromising user privacy, using technologies like federated learning, differential privacy, and secure multi-party computation to train models on encrypted or aggregated data. These approaches address one of the fundamental tensions between the need for comprehensive credit analysis and the privacy expectations of DeFi users.

The dynamic nature of blockchain ecosystems requires credit scoring models that can adapt to changing market conditions, protocol updates, and evolving user behavior patterns. Traditional credit models often rely on stable, long-term behavioral patterns, while DeFi credit models must account for the rapid evolution and experimentation characteristic of blockchain ecosystems.

Cross-chain credit scoring presents both opportunities and challenges, as borrowers may have credit-relevant activity across multiple blockchain networks that should be considered in comprehensive credit assessments. Developing infrastructure to aggregate and analyze cross-chain data while maintaining security and privacy represents a significant technical challenge for next-generation credit scoring systems.

The integration of traditional credit data with blockchain-based behavioral analysis could create more comprehensive and accurate credit assessments than either approach alone, though this integration raises questions about privacy, regulatory compliance, and the philosophical goals of decentralized finance. For detailed analysis of various protocols and their performance metrics, TradingView’s comprehensive charting tools provide essential insights for evaluating lending protocol effectiveness and market dynamics.

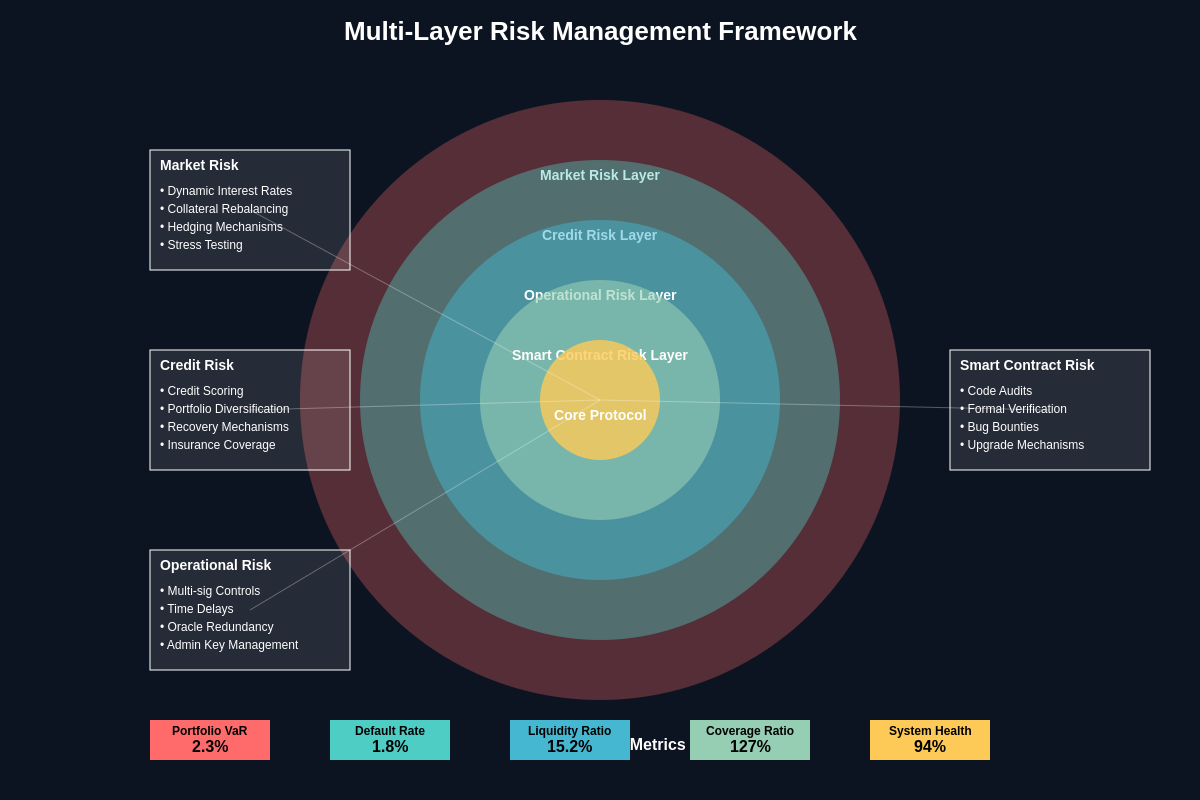

Insurance and Risk Distribution Mechanisms

The development of comprehensive insurance and risk distribution mechanisms represents a critical component of sustainable undercollateralized lending systems, providing protection for lenders while enabling borrowers to access credit without excessive collateral requirements. These mechanisms must operate within decentralized frameworks while providing the security and predictability required for large-scale lending operations.

Parametric insurance products can provide automated coverage for specific risks in undercollateralized lending, using blockchain-based triggers and oracles to automatically compensate lenders when predetermined conditions are met. These products can cover various risks including borrower default, smart contract failures, oracle manipulation, and market volatility, providing comprehensive protection for lending protocol participants.

Risk pooling mechanisms enable the distribution of default risk across large numbers of lenders and borrowers, creating diversification benefits that can reduce the overall cost of capital while providing more stable returns for participants. Advanced protocols implement sophisticated risk tranching and distribution algorithms that can optimize risk-return profiles for different participant preferences and risk tolerances.

Credit derivatives and synthetic products enable more sophisticated risk management strategies for undercollateralized lending, allowing market participants to hedge, speculate, or arbitrage various forms of credit risk. The development of liquid markets for these products could significantly improve the efficiency and scalability of undercollateralized lending systems.

Mutual insurance and cooperative risk-sharing models leverage community incentives and shared ownership structures to create sustainable insurance mechanisms for undercollateralized lending. These approaches can align the interests of borrowers, lenders, and insurers while maintaining the cooperative and decentralized principles that define many DeFi communities.

The integration of traditional insurance markets with DeFi risk management creates opportunities for hybrid products that can provide institutional-grade protection while maintaining decentralized operation and governance. Established insurance companies are increasingly exploring DeFi partnerships and products, potentially bringing significant capital and expertise to undercollateralized lending systems.

Regulatory Considerations and Legal Frameworks

The regulatory landscape for undercollateralized lending in DeFi represents one of the most complex and rapidly evolving aspects of this space, with different jurisdictions taking varying approaches to digital asset lending, consumer protection, and financial services regulation. The development of sustainable undercollateralized lending protocols must navigate these regulatory requirements while maintaining the decentralized and permissionless characteristics that define DeFi.

Consumer protection regulations in many jurisdictions include specific requirements for credit disclosure, fair lending practices, and debt collection procedures that may apply to undercollateralized DeFi lending protocols. Protocols must consider how to implement these protections within decentralized frameworks while maintaining compliance with applicable laws and regulations.

Anti-money laundering and know-your-customer requirements present significant challenges for undercollateralized lending protocols that aim to maintain privacy and permissionless access. Various approaches including zero-knowledge identity verification, decentralized identity systems, and selective disclosure mechanisms are being explored to balance regulatory compliance with privacy and accessibility goals.

The classification of lending tokens, governance tokens, and protocol revenues under securities regulations varies significantly across jurisdictions and continues to evolve as regulators develop more specific guidance for DeFi protocols. These classifications can significantly impact protocol design, tokenomics, and operational requirements.

Cross-border lending regulations become particularly complex for global DeFi protocols that serve users across multiple jurisdictions, each with different legal requirements for lending, consumer protection, and dispute resolution. Protocols must consider how to structure their operations and governance to comply with applicable laws while maintaining global accessibility.

The development of regulatory sandboxes and experimental frameworks in various jurisdictions provides opportunities for undercollateralized lending protocols to work with regulators to develop appropriate regulatory approaches that balance innovation with consumer protection and financial stability. These collaborative approaches may be essential for the long-term success and mainstream adoption of undercollateralized DeFi lending.

Economic Models and Incentive Structures

The economic design of undercollateralized lending protocols requires sophisticated incentive mechanisms that can align the interests of borrowers, lenders, protocol governance participants, and service providers while maintaining sustainable economics over long time periods. These systems must account for various behavioral factors, market dynamics, and potential attack vectors that could undermine protocol stability.

Token economics for undercollateralized lending protocols typically involve complex relationships between lending rates, governance tokens, insurance premiums, and protocol revenues that must be carefully balanced to maintain system stability while providing attractive returns for participants. The design of these tokenomics can significantly impact protocol adoption, capital efficiency, and long-term sustainability.

Dynamic interest rate models for undercollateralized lending must account for additional risk factors beyond typical supply and demand mechanics, incorporating reputation scores, collateralization ratios, insurance coverage, and market conditions to price loans appropriately. These models require sophisticated algorithms and data inputs that can operate effectively within decentralized frameworks.

Governance token incentives can align protocol participants with long-term protocol success, providing rewards for positive behaviors like accurate credit assessments, responsible borrowing, and effective risk management. However, these incentives must be carefully designed to avoid perverse incentives or gaming that could undermine protocol security or effectiveness.

Liquidity mining and yield farming programs can bootstrap adoption and provide initial liquidity for undercollateralized lending protocols, though these programs must be structured to create sustainable long-term value rather than short-term speculative activity. The transition from artificial incentives to organic protocol revenue represents a critical milestone for protocol maturity.

Network effects and ecosystem development require careful economic design to create virtuous cycles where increased adoption leads to better outcomes for all participants. Successful protocols often develop strong network effects where borrowers benefit from lower rates, lenders benefit from diversified risk, and service providers benefit from increased activity and revenue opportunities.

Institutional Adoption and Integration Challenges

The pathway to institutional adoption of undercollateralized DeFi lending faces numerous challenges including regulatory compliance, risk management requirements, operational complexity, and integration with existing financial infrastructure. However, successful institutional adoption could provide the scale and legitimacy required to establish undercollateralized lending as a mainstream financial service.

Institutional investors and lenders have specific requirements for due diligence, reporting, compliance, and risk management that may be difficult to satisfy within current DeFi frameworks. Protocols seeking institutional adoption must develop solutions that can meet these requirements while maintaining decentralized operation and governance.

Integration with traditional banking and lending infrastructure requires sophisticated technical and legal frameworks that can bridge the gap between blockchain-based protocols and legacy financial systems. This integration may involve various intermediaries, custody solutions, and compliance services that add complexity but enable broader adoption.

Custodial solutions for institutional participation in undercollateralized DeFi lending must provide institutional-grade security, compliance, and operational capabilities while maintaining access to DeFi protocols and yield opportunities. The development of these solutions represents a significant business opportunity and technical challenge for service providers.

Risk management frameworks for institutional participation must translate DeFi-specific risks into traditional risk management language and processes, enabling institutional risk managers to understand and evaluate undercollateralized lending opportunities within their existing frameworks. This translation requires deep expertise in both traditional finance and DeFi systems.

The development of hybrid protocols that can serve both retail and institutional participants while maintaining DeFi principles represents a complex design challenge that requires careful balance between accessibility, compliance, and operational efficiency. For institutional investors seeking comprehensive market analysis and protocol evaluation, TradingView’s professional trading tools provide essential capabilities for analyzing DeFi lending markets and opportunities.

Technological Infrastructure and Scalability

The technological infrastructure required to support large-scale undercollateralized lending in DeFi presents significant challenges in terms of transaction throughput, computational requirements, data management, and integration complexity. Current blockchain infrastructure may not be sufficient to support the transaction volumes and complexity required for mainstream adoption of undercollateralized lending.

Layer 2 scaling solutions and alternative blockchain architectures offer potential pathways to achieve the performance requirements for large-scale undercollateralized lending, though each approach involves trade-offs in terms of security, decentralization, and compatibility with existing DeFi infrastructure. The choice of underlying blockchain infrastructure significantly impacts protocol design and capabilities.

Oracle infrastructure for undercollateralized lending must provide reliable, tamper-resistant data feeds for various inputs including asset prices, credit scores, economic indicators, and off-chain events that may trigger loan conditions or insurance payouts. The security and reliability of oracle systems represents a critical component of overall protocol security.

Data availability and privacy solutions must balance the need for comprehensive credit analysis with borrower privacy requirements and regulatory constraints. Advanced cryptographic techniques including zero-knowledge proofs, secure multi-party computation, and differential privacy may enable sophisticated credit analysis while preserving user privacy.

Interoperability between different blockchain networks and DeFi protocols enables more comprehensive credit assessment and risk management by leveraging data and capabilities from multiple sources. However, cross-chain infrastructure introduces additional complexity and security considerations that must be carefully managed.

Smart contract optimization and gas efficiency become particularly important for undercollateralized lending protocols that may involve complex computations for credit scoring, risk assessment, and automated decision-making. Protocol designers must balance functionality with cost efficiency to ensure accessibility for borrowers across different economic circumstances.

Emerging Models and Innovation Frontiers

The frontier of undercollateralized lending innovation continues to expand with new models, technologies, and approaches that push the boundaries of what’s possible within decentralized finance frameworks. These emerging models often combine elements from multiple approaches while introducing novel mechanisms for credit assessment, risk management, and value creation.

Micro-lending and peer-to-peer models leverage social networks and community relationships to enable small-scale undercollateralized lending that can serve underbanked populations and provide financial inclusion opportunities. These models often emphasize social impact and community development alongside financial returns.

Dynamic collateralization systems can adjust collateral requirements based on borrower behavior, market conditions, and risk assessments, potentially starting with higher collateralization that decreases over time as borrowers establish positive credit histories. These systems provide pathways for borrowers to gradually access more capital-efficient lending terms.

Revenue-based financing models enable borrowers to access capital based on future revenue projections rather than current asset holdings, creating opportunities for businesses and individuals to leverage future earning potential. Smart contracts can automatically adjust repayment terms based on actual revenue performance, creating more flexible and sustainable lending arrangements.

Decentralized autonomous organization lending pools enable communities to create their own lending systems with custom risk parameters, governance structures, and member benefits. These systems can serve specific communities or use cases while leveraging the broader DeFi ecosystem for liquidity and infrastructure.

Prediction market integration can provide additional data sources for credit assessment by incorporating market predictions about borrower success, economic conditions, and other relevant factors into lending decisions. These systems leverage collective intelligence and market mechanisms to improve credit assessment accuracy.

Quadratic funding and other novel mechanism design approaches can create more equitable and efficient allocation of lending capital while incentivizing positive behaviors and community participation. These mechanisms draw from research in economics, computer science, and social choice theory to create better outcomes for lending ecosystem participants.

Market Impact and Economic Implications

The successful development of undercollateralized lending in DeFi could have profound implications for global financial markets, potentially unlocking trillions of dollars in previously inaccessible credit while reducing the cost of capital for borrowers worldwide. These changes could accelerate economic development, enable new business models, and create more inclusive financial systems.

Capital efficiency improvements from undercollateralized lending could significantly increase the overall lending capacity of DeFi systems while reducing the opportunity cost for borrowers who currently must lock up valuable assets as collateral. This efficiency gain could make DeFi lending competitive with traditional lending in terms of capital requirements while maintaining the advantages of permissionless, global access.

Financial inclusion opportunities created by undercollateralized DeFi lending could provide access to capital for individuals and businesses that are underserved by traditional banking systems, particularly in developing markets where traditional credit infrastructure may be limited or inaccessible. The global, permissionless nature of DeFi could enable these users to access international capital markets directly.

Market dynamics for undercollateralized lending may create new forms of competition and collaboration between DeFi protocols and traditional financial institutions, potentially leading to hybrid systems that combine the best aspects of both approaches. This competition could drive innovation and efficiency improvements across the entire lending ecosystem.

The development of sophisticated risk assessment and management tools for undercollateralized lending could have spillover effects that benefit other areas of DeFi and traditional finance, creating new data sources, analytical techniques, and risk management approaches that improve overall financial system stability and efficiency.

Monetary policy implications of large-scale undercollateralized DeFi lending could affect central bank policy tools and financial stability considerations, particularly if these systems become significant sources of credit creation and monetary expansion. The interaction between decentralized lending systems and traditional monetary policy represents an important area for ongoing research and policy development.

Future Outlook and Development Roadmap

The future development of undercollateralized lending in DeFi will likely involve gradual evolution rather than revolutionary breakthroughs, with protocols iteratively improving their risk assessment capabilities, regulatory compliance, and operational efficiency while building trust and adoption within the broader ecosystem. This evolutionary approach allows for careful risk management while enabling continuous innovation and improvement.

Technology development roadmaps for undercollateralized lending protocols typically focus on improving scalability, security, user experience, and integration capabilities while reducing costs and complexity for both borrowers and lenders. The successful execution of these roadmaps requires coordination between protocol developers, infrastructure providers, and ecosystem participants.

Regulatory evolution will significantly influence the development trajectory of undercollateralized DeFi lending, with clearer regulatory frameworks potentially accelerating adoption while restrictive regulations could limit innovation and accessibility. The ongoing dialogue between DeFi developers, regulators, and traditional financial institutions will be crucial for establishing appropriate regulatory approaches.

Market maturation indicators for undercollateralized lending include increasing loan volumes, improving default rates, institutional adoption, regulatory clarity, and the development of secondary markets for lending positions. These indicators can help assess the progress and sustainability of undercollateralized lending innovation.

Integration with traditional finance systems may accelerate through various channels including institutional adoption, regulatory sandboxes, traditional bank partnerships, and hybrid products that combine DeFi innovation with traditional banking infrastructure and compliance frameworks. For comprehensive tracking of market developments and protocol performance, traders and analysts rely on professional charting platforms like TradingView’s advanced analytics suite, which provides essential tools for evaluating lending market trends and opportunities.

Research and development priorities for the undercollateralized lending space include improving credit assessment accuracy, developing more efficient risk management mechanisms, creating better user experiences, and solving technical challenges related to scalability, privacy, and interoperability. Academic and industry collaboration will be essential for addressing these complex challenges.

The potential for undercollateralized lending to achieve the scale and impact necessary to be considered the “holy grail” of DeFi depends on successfully addressing the multifaceted challenges of credit assessment, risk management, regulatory compliance, and technological infrastructure while maintaining the principles of decentralization, permissionless access, and global inclusivity that define the DeFi movement. Success in this endeavor could fundamentally transform global finance, creating more efficient, inclusive, and innovative lending systems that serve the needs of borrowers and lenders worldwide while advancing the broader goals of decentralized finance.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency and DeFi investments carry significant risks, including the potential for total loss of capital. The undercollateralized lending space is particularly experimental and risky, with many protocols still in development and unproven at scale. Readers should conduct their own research, understand the risks involved, and consider consulting with qualified financial advisors before participating in any DeFi lending activities. The regulatory landscape for DeFi is evolving rapidly, and future regulatory changes could significantly impact the viability and legality of undercollateralized lending protocols. Past performance does not guarantee future results, and the nascent nature of this technology means historical data may not be indicative of future performance.